The final ingredient SS1 needs in our "recipe for an 8,000% VUL style price run"... but ingredient #6 is the hardest one to get...

Published 26-JUL-2025 18:15 P.M.

|

16 minute read

Commentary: Silver FOMO - is the price about to break out? Recipe for the next VUL?

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

We have not felt proper, itchy “FOMO” in a long, long time.

It’s now week four of the small end of the ASX being up and about, for the first time in over 3 years.

FOMO (fear of missing out) mainly hit us this week on the silver price looking like it could break out to new highs any day now.

While we could always be wrong, we decided to scratch this FOMO itch by opening up one of those awful leveraged CFD and options trading accounts we swore we would never touch and placed a modest bet on silver hitting US$80/oz before February 2026 via some $80 silver call options.

(it's sort of like the pre season commencement “Freo Dockers to win the flag” bet you have to put on each year just in case it finally happens this time...)

Anyway, the point is is we think the silver price looks like it could be about to go on a serious run.

(and again, we could be wrong, like we were during the “almost silver squeeze” of 2021 - Commodity prices go down as well as up.)

But if silver DOES go on a big run in the coming months, it could deliver the illusive ingredient #6 needed for Sun Silver (ASX:SS1) to complete our recipe for a VUL style run.

Our best ever Investment Vulcan Energy Resources (ASX:VUL) was up over 8,000% at its peak, and is still up 2,070% from our Initial Entry Price.

VUL is still our best Investment to date, so naturally we think a lot about how and why it happened, and how to try and repeat it.

But of course past performance like this is extremely hard to replicate, most Investments don't turn out anywhere near as successful.

14 months ago, we analysed what we thought led to VUL’s success, and distilled it into a 6 ingredient recipe that we thought SS1 could emulate, with a bit of luck needed.

You can read it here “Can SS1 deliver a VUL style result? - May 2024”.

We go into it more in today’s note but the TLDR; is the VUL recipe needs 6 ingredients:

- Acquired a project in a down cycle for a commodity

- A project with size and scale

- In the green theme (or today, in the precious metals and/or USA critical metals theme)

- In a country with demand for the end product

- Be the first mover

- Then wait for that commodity price run....

Ingredients #1 to #5 are in the company's control when acquiring the project, and in the investors control when choosing the company.

Ingredient #6 - this is the hard one to get: a significant price run in the commodity to happen.

This is where you need luck and timing, and nobody can control that.

VUL had all 5 ingredients and then lithium went on a generational price run...

SS1 (in our opinion) has the first 5 ingredients (which is why we Invested) and now we are hoping the silver price keeps on rising over the next 6 months (ingredient #6).

(not to mention SS1’s emerging US critical metal antimony potential. This was just blind luck and perfect timing for SS1 investors - surely they can’t get 2x of ingredient #6 at the same time?)

Before we get into an update on SS1’s potential to deliver our “6 ingredient VUL recipe”, we picked up another notable similarity this week after SS1 successfully closed its $30M cap raise.

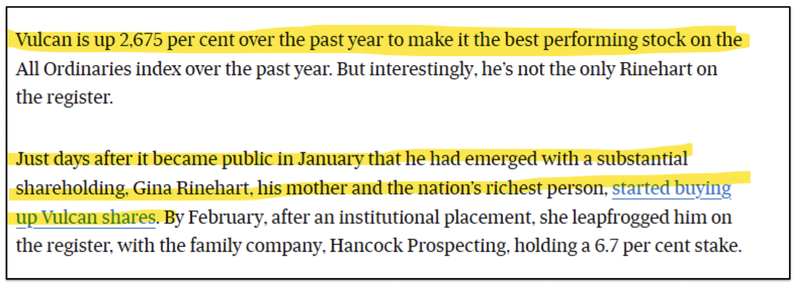

Back before VUL’s big run to $16, John Hancock popped up on the VUL’s shareholder register with 5.23%.

This revealed that he had invested in the 40c VUL raise and was adding to his position on market (source).

(John Hancock is the son of Australia’s richest person Gina Rinehart).

(Source)

Days after his involvement was revealed, Gina Rinehart started buying up VUL shares on market too:

(Source)

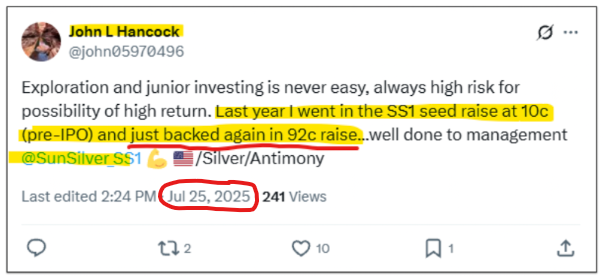

On Friday we noticed this tweet from John Hancock, saying he participated in the 92c SS1 cap raise this week:

(Source)

We wont read into it too much just yet... but we will certainly be watching with interest to see what the SS1 top 20 shareholders look like when it is revealed in the SS1 annual report that is due next month.

Below is our deeper dive into the “6 ingredient recipe” we identified that helped VUL deliver its 8,000% plus price run and an update on how SS1 is progressing against it.

IMPORTANT: The past performance of VUL IS NOT an indicator that SS1 will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong. Only invest what you can afford to lose.

The recipe: How VUL rallied to a peak price run of ~8,000%

Here is the 6 ingredient recipe in more detail (again you can read the full write up we did on it back in May “Can SS1 deliver a VUL style result”.

In general, we identified the ingredients that DID work really well for us back in 2020 and our Investment in VUL was to find a company that:

- Acquired the project in a down cycle - Acquired a project in an “unloved” commodity, for a very good price.

- Project size and scale is big - the project has to have genuine size/scale potential so that investors see it as the most leveraged exposure to any particular thematic. That way it captures the biggest audience if things go in its favour... including major funds and potential acquirers.

- In the green theme - Project/commodity has applications in the “decarbonisation / green energy” area, meaning lots of financial incentives and investor interest in this space.

JULY 2025 UPDATE: Today the rapidly emerging thematic is silver/gold or USA critical metals. - In a country with demand for the end product - located in a region that is prioritising the particular initiative and directly needs a new, preferably local supply of the critical commodity (...hello government incentives and subsidies).

- Be the first mover - First to go public with their project when the commodity sentiment isn’t in full swing... yet (all the “copycat companies” will come later once the first mover starts showing share price success)

- Then wait for that commodity price run.... 100% NOT in our control - this is where a bit of luck with timing comes into play.

How this recipe worked for our 8,222% gain in VUL

Remember - this was a rare outsized success in our Portfolio, and they don't come around often.

We first Invested in VUL when nobody cared about lithium, because it fit ingredients 1 - 5 of the above recipe...

And then ~4 months later the lithium price started moving up...

... then 6 months later the lithium price really started running hard.

The elusive and hard to get “Ingredient #6” had appeared - it was a ~12 month wait.

Here’s how the VUL investment looked like in our 6-step recipe:

- Acquire a project in a down cycle - VUL picked up a geothermal lithium brine project at a time when lithium was hated by the market and hard rock lithium mines were going into administration.

In 2019 when nobody liked lithium, VUL acquired the project for ~$1M paid in stock (with another $2M in stock payments on achieving performance milestones - full deal terms here) - VUL is now at a market cap of ~$1 Billion. - A project with a big size and scale - VUL’s project at the time had one of the largest lithium resources in the world and the single biggest inside the EU.

- In the green theme - VUL’s plan was to turn its project into the world’s first ZERO carbon lithium project, a theme where a lot of interest, investment and government incentives are flowing.

- In a country with demand for the end product - VUL’s project was in the heart of the EU's auto industry in Germany. The carmakers started announcing plans to transition their car fleets to EVs which signalled upcoming lithium demand in Germany... not to mention the EU’s critical raw materials act which is now at play.

- Was the first mover - VUL basically invented the “Zero Carbon Lithium” concept. VUL was a first (listed) mover in the Direct Lithium Extraction (DLE) from lithium brines space, and the first in “Zero Carbon Lithium”. Up until 2020, most of the ASX’s focus in the lithium industry was on getting old operating mines back into production OR ramping up small scale operations. No one was looking at DLE from brine assets...

- Then wait for that commodity price run... This is where a bit of luck comes into play... VUL completed its deal and started trading a few months before the lithium price took off.. Between 2020 and 2022 the lithium price went up by over 600%... and VUL went up over 8,000%.

Again - past performance is not an indicator of future performance. These kinds of successes don't come around often.

In May 2024 we said SS1 had the same ingredients, now we just need a serious silver price run to happen

Over recent months, a fair few positive surprises have come into play for our Investment in SS1 and we actually think SS1 is in an even stronger position now than it was in 2024:

... If the small cap gods just bless us with a “2020 lithium” style generational price run in SS1’s key commodity - silver (and/or antimony).

14 months later, here is an update on how SS1 has progressed in the key 6 ingredients to the VUL recipe:

Ingredient #1: Acquire a project in a commodity down cycle - SS1 ✅

SS1 picked up its project in August 2023 when there weren’t many people talking about or invested in silver.

At the time the silver price had been trading in a range for over a decade and most capital was not interested in primary silver projects.

The silver price is now trading at 14 year highs and the technical analysis community is calling for a breakout near all time highs around that US$50 per ounce mark.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Silver price aside, SS1 has also re-assayed old drillholes and found that its project could actually host a large antimony resource too...

This was an unexpected surprise for us and wasn’t originally part of our Investment Thesis.

SS1 announced the project's antimony potential BEFORE antimony became a very popular investment theme, so it ticks this box too.

Now with the US Government funding critical minerals projects in the US, we think the antimony potential is the dark horse that could make SS1’s project strategically important to the US.

Now we wait for the market to re-rate this project as silver and US critical metals themes emerge.

Ingredient #2: A project that has size and scale - SS1 ✅

SS1’s project is now the biggest pre-production silver asset on the ASX and in the USA...

When we first Invested in SS1 it had the SECOND biggest silver resource on the ASX.

After some drilling and a resource upgrade SS1 now has the biggest pre-production silver asset on the ASX and in the USA...

AND SS1 is currently drilling to grow that resource even further.

Just last week SS1 announced that re-assays of old drillcores were finding grades were ~20% higher than the assays that make up SS1’s current resource.

Which could also make the resource even bigger...

(Source)

Ingredient #3: In a strong macro theme (at the time of VUL we said “green theme” but precious metals and US critical minerals are today’s emerging themes) - SS1 ✅

When we first Invested in SS1 we liked that SS1 had exposure to the decarbonisation thematic (and it still does) because of silver's use in solar panel manufacturing.

Now we think SS1 has (with a lot of luck) found itself in the middle of what we think could be the TWO biggest macro thematic on the ASX over the coming years.

Precious metals (silver) AND US based critical metals critical metals (antimony).

Just like how the lithium and battery metals took charge between 2020-2022 we think precious metals and US based critical metals projects will take centre stage of the next big bull run.

We think the big catalyst to cement SS1’s position in this will be the company announcing a maiden antimony resource estimate for its project - which is what we are hoping to see some of the $30M capital raise spent on:

(Source, SS1 announcement)

Ingredient #4: In a country with demand for the end product - SS1 ✅

Since the Trump administration came in, re-shoring of US manufacturing and supply chains has become an urgent priority, especially for critical metals.

SS1’s project is based in Nevada USA.

In March the US President Donald Trump invoked emergency powers to boost domestic production of critical minerals as part of a broad effort to offset China's near-total control of the sector. (Source - Reuters)

Large US-based mining projects have benefited including:

- MP Materials - The Department of Defence invested $400M in equity and provided long-term floor pricing for rare earths more than double that of the Chinese market price.

- Perpetua Resources - The Department of Defence is investing here for the Company’s gold-silver-antimony project, which also has fast-tracked permitting to get the project into production

There are about a dozen other US-based mining projects that the US government has supported over the past six months, and we see the US as having a big demand for critical minerals.

While SS1 is primarily a silver project, we think that the US government will be most interested in its antimony potential.

The US has no primary source of antimony production and it is used in various military applications including as a hardening agent for bullets.

In 2025, approximately 59% of the world's silver demand is from industrial applications and has various uses in military applications (source).

The majority of US silver is purchased from Mexico, where Trump has indicated the potential for 30% tariffs on imports.

These tariffs (and even the potential for tariffs) are encouraging US-based projects for materials - like silver - that are important for US industrial applications.

Ingredient #5: Was the first mover - SS1 ✅

As an equities investor, there are very few options when it comes to large primary silver projects on the ASX.

SS1 IPO’d in May 2024 with a giant primary silver project, many months before the silver “thematic” started properly emerging.

When SS1 IPO’d the price of silver was around US$28 per ounce, and now it is closer to US$40.

We have seen quite a few new silver projects come onto the ASX, but SS1 was there FIRST and the project scale was big, before the macro thematic really started to heat up.

SS1 was also an early move in antimony, before it became popular.

The first antimony results that SS1 published were in August 2024, weeks later the Chinese totally banned antimony exports putting a huge spotlight on the material.

We have also seen a bunch of antimony projects emerge on the ASX over the last six months, but SS1 had a several months head start to draw attention to its story and work on a large-scale re-assay program.

Ingredient #6 Then wait for that commodity price run.... ✅

THIS is the hard one - everything can be set up perfectly on ingredients 1 to 5...

But if the epic commodity run doesn't come along, then frankly, nobody will care.

And this is where you need a big bucket of small cap luck that only comes around every few years (if at all) to certain companies in the right place at the right time with ingredients 1 to 5 already in place.

First, silver.

SS1 first acquired the project when the price of silver was around US$22 per ounce.

Then, SS1 IPO’d at a silver price of US$28 per ounce.

Now silver is almost US$40 per ounce.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The silver price over the next year is still the wild card for SS1 that we hope will work in our favour.

So far, the silver price has already been doing a great job, but what we really need is a “generational price run” like we saw lithium deliver back in 2020.

Next, antimony.

The antimony price has also run over the last 12 months.

The price started to run when China placed export restrictions on antimony in early 2024 and then really started to take off when China totally banned the export of antimony later that year.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So the antimony price and US critical metals theme is certainly doing its job here, we are more waiting for SS1 to prove it has a large, US based antimony resource.

We are seeing interest for the US-based critical metals theme to continue to grow.

You can only look as far as the price floor that the US Department of Defence gave to MP Materials for its rare earths, as a sign of what is to come for other critical minerals.

These price floors are very important for small market critical commodities like antimony, where China controls the supply and can flood the market to depress the price.

Now it’s still early for SS1 and lots of work is yet to be done on its antimony potential.

The ingredients are all there for SS1, we just need ingredient #6 (silver price moving up) to keep things humming.

And if SS1 can continue to prove up its antimony potential, and antimony and the US based critical metals theme keeps growing, it could be a second cup of the hardest to get “ingredient #6” for SS1.

The lesson we take away is that small cap investing is about acquiring and holding the right stocks in unloved commodities, and waiting for the commodity to be back in favour.

And if you are lucky, for the commodity to become hot - like silver and US critical minerals look to be right now.

Also noting that commodities don’t run forever - good companies, on the tail end of a cycle when interest in the commodity is falling, would have hopefully raised money to develop the project, and “re-rate” at a higher step-change valuation while the commodity price takes a rest.

The question is now... are these current price runs a “flash in the pan” or the start of something bigger like we saw in lithium a couple of years ago?

C’mon silver price rise!

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.