NC1: Leverage to a rising nickel price... and guess what - it’s rising.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,785,838 NC1 Shares at the time of publishing this article. The Company has been engaged by NC1 to share our commentary on the progress of our Investment in NC1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

It feels to us like the nickel price wants to go on a run higher...

Just two days ago another major Indonesian nickel producer said it would slash production from its mines...

... this time because of sulphur supply shortages due to the Strait of Hormuz being closed (source).

It looks like the longer the Strait of Hormuz stays shut and causes chaos in global markets, the more likely a nickel bull run becomes - more on why later in today’s note. (source)

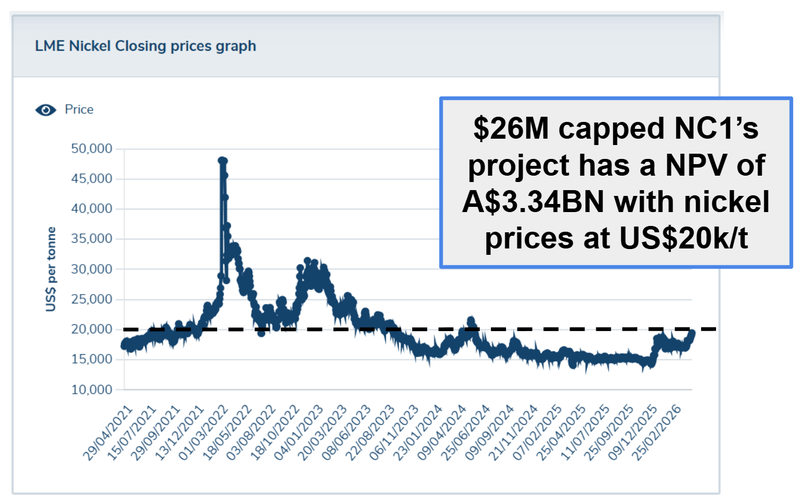

Nickel’s already up ~36% since the December low late last year.

In the last 14 days, the nickel price has broken out and started running again.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The nickel price is now at ~US$19,500 per tonne, and climbing.

Our $26M capped Investment Nico Resources (ASX:NC1) owns 100% of one of the largest undeveloped nickel projects on the planet.

It’s one of those giant Tier 1 kind of deposits that get major miners interested.

The current nickel price is just below the nickel price that NC1 assumed in its 2022 Pre-Feasibility Study (PFS).

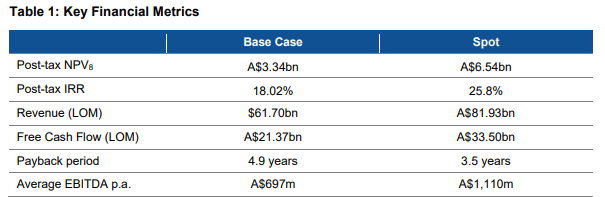

NC1 applied a US$20k/tonne nickel price in its study, which demonstrated the following project economics:

- Net Present Value (NPV) = $3.34BN.

- Payback period of 4.9 years

- Internal Rate of Return (IRR) = 18.02%

From CAPEX of ~$2.9BN.

But the reason we are Invested in NC1 is not for the nickel price today.

It’s for a world where nickel goes to US$25,000, $35,000 or $40,000 per tonne.

If any of those price scenarios come into play, NC1 could become the quickest and easiest way to get leveraged nickel exposure - for investors and producers alike.

For context, at US$30,000 per tonne, NC1’s project’s NPV would almost double to $6.5BN.

NC1 is capped at just $26M - and so we think NC1’s asset offers the most leverage to nickel prices at the junior end of the market.

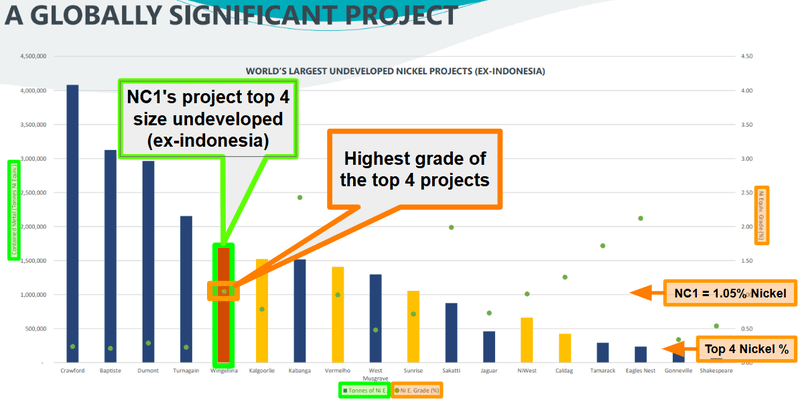

In fact it's one of the four biggest undeveloped nickel project (ex-Indonesia) - of those four projects, NC1’s has the highest grade:

(source)

NC1’s project has an initial reserve of 1.56 million tonnes of contained nickel, capable of producing approximately 40,000t of nickel and 3,000t of cobalt annually.

NC1’s asset is genuinely “Tier 1” in terms of size/scale - that term gets thrown around a fair bit with small caps, but this is a real monster - once built, it will produce nickel for over 40+ years.

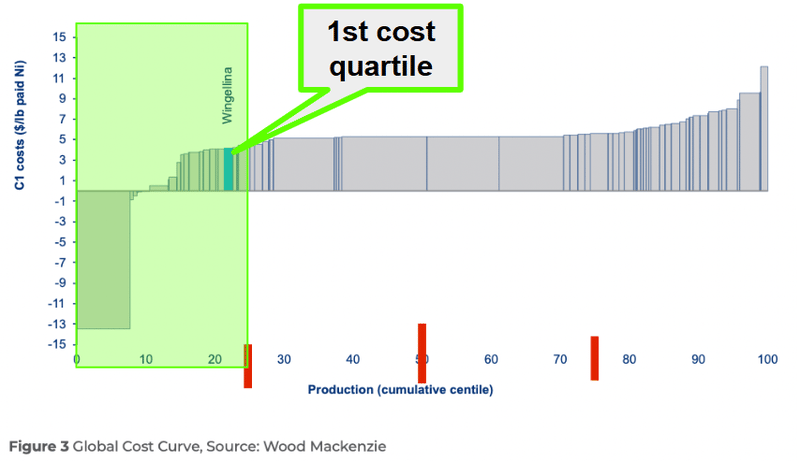

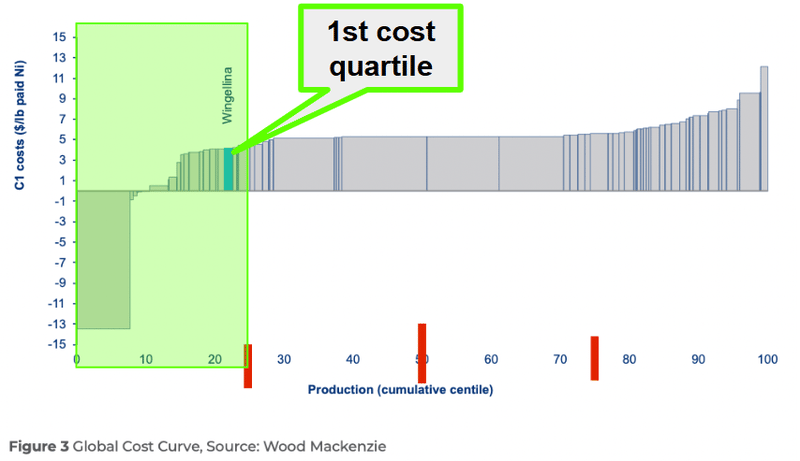

NC1’s project also sits amongst the group of assets that would be operating in the lowest cost quartile of any asset globally.

So, while it will be expensive to get going, when it's up and running, it will be among the cheapest producers of nickel globally.

(source)

As mentioned earlier, at US$20,000 per tonne nickel prices the project has an NPV of $3.4BN.

IF a nickel price of US$30,000 per tonne is used then, NC1’s project’s NPV would almost double to $6.5BN.

(Source)

NC1 is capped at $26M.

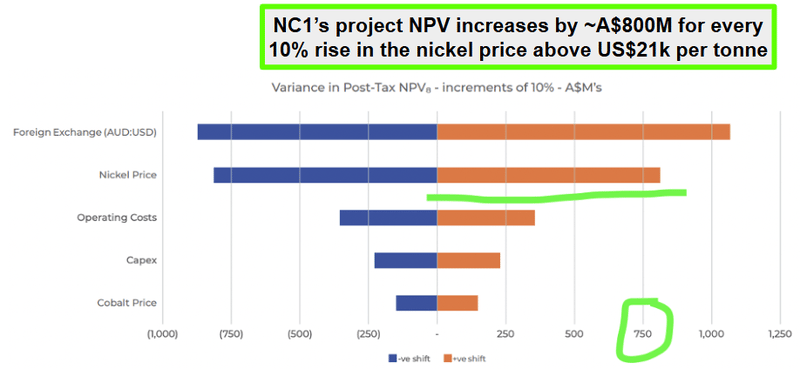

That PFS done back in 2022 showed the project’s NPV increases by ~A$800M for every 10% rise in the nickel price above US$21k per tonne:

(Source)

The reason why NC1 trades where it does today is because of how sensitive the project is to nickel prices – and because nickel prices have traded lower than its base case price for the past ~3 years.

But that looks like it could change any day now...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The two macro triggers we are watching for a nickel bull run

All we need now is for a shift in macro sentiment and a big nickel bull run to re-energise the

market on NC1.

The two reasons we think 2026 could be the year for nickel is because:

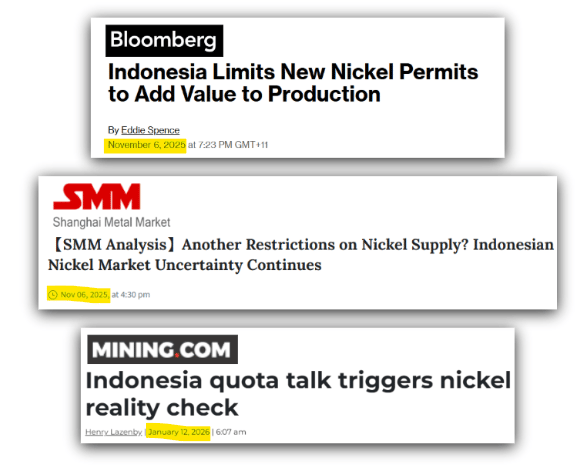

- In February there was the news that the world's biggest producer Indonesia would put quotas on producers:

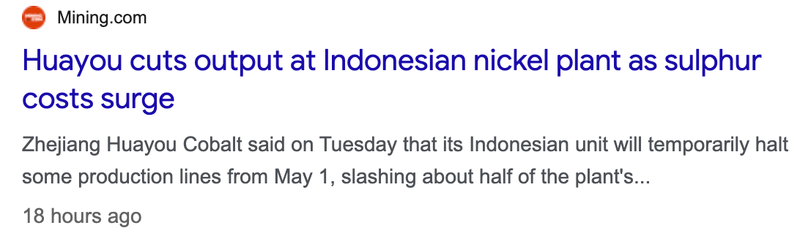

- Just yesterday, a second geopolitical risk hit the nickel market - one of the big producers announced (on their own, without government-enforced quotas) a potential 50% cut to production starting May 1st:

(source)

AND the production cut came as a result of a shortage (and increase in the price of sulphur).

The connection to sulphur comes from most of the Indonesian nickel mines needing sulphur.

That’s because most of the nickel mined in Indonesia is from laterite hosted orebodies which require sulfuric acid for processing.

And ~75-80% of Indonesia's sulfur comes from the Middle East. (source)

Here are two good takes on the impact it’s having on nickel markets (both released before that Indonesian miner said it would cut production):

So the odds of a short term rally in the nickel price is increasing the longer the Strait of Hormuz is closed.

That's all in the short-term.

In the long-term, we think nickel could find itself in the middle of one of the biggest megatrends in markets over the next decade...

Nickel as an exposure to the robotic thematic

Does anyone remember the 2020-2021 battery minerals bull run?

We will probably never forget it.

Small caps with lithium rock chips were capped at $100-200M.

Those who made discoveries or with advanced assets went on to get taken out in deals worth billions of dollars OR become the cornerstone projects for companies like $19BN Pilbara Minerals today.

We actually had two big wins in that period - Vulcan Energy Resources which up 8,225% at its highest point from our original Investment.

And Latin Resources, which made a new lithium discovery and got taken over by Pilbara Minerals (we first Invested at 1.765c and it was taken out at ~20c valuation in equivalent PLS shares, a ~1033% increase)

The past performance of those stocks is not an indicator of future performance of our current or future Investments.

We think that over the next decade, battery minerals like nickel are about to make a big comeback because of the great robot build out...

... billions of autonomous robots are expected to be built over the coming decade.

It just so happens the same “battery minerals” that were loved, then hated by the market, go into batteries that power autonomous AI robots.

Robots that are expected to soon be in the home, in factories and in the military:

(source)

(source)

(source)

The country to win the AI and AI robot race will likely become the new global superpower, both from robot driven productivity gains and robot driven military dominance.

So securing minerals supply domestically OR from allies has become urgent and of strategic importance.

So, the autonomous AI robots are coming

“Billions and billions” of them, according to Elon Musk.

Elon’s company Tesla has a “late 2026 or early 2027” launch date planned for his similar Optimus robot.

(source)

Tesla is just one of many US companies entering the AI robot market - the West's answer to what appears to be China’s head start in mass producing autonomous AI robots.

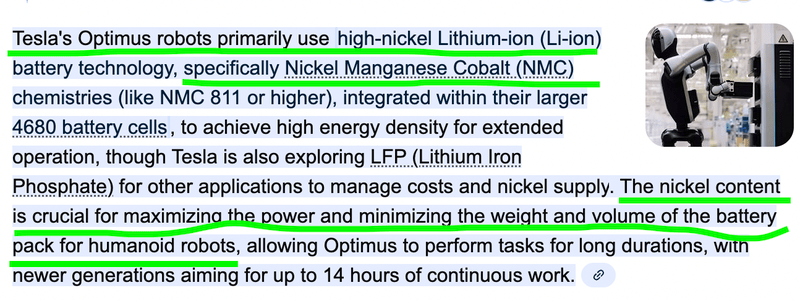

Tesla’s choice of battery chemistry for its robot strategy could mean that those billions of robots need millions of tonnes of nickel:

NC1 has already proven its nickel can be turned into battery grade product (MHP):

(source)

So as the buildout gets stronger, we expect demand for nickel to increase (and eventually that demand shows in higher nickel prices).

As we said earlier, our Investment in NC1 is speculation on the nickel price surging, and global supply not keeping pace with new demands such as autonomous robots.

Which might be the tailwinds needed to get NC1’s Tier 1 nickel asset out of the development stages and into production.

The major catalysts for NC1 over the coming months

Clearly, NC1’s share price is most correlated to movements in the nickel price.

BUT we think NC1 still has three major catalysts we could see over the next 6-12 months:

- infill drilling program would be run to upgrade the project’s resource classification. NC1 confirmed in its March quarterly report that an

- “greenfields exploration opportunities in the musgraves region”. (more on this in a second) The March quarterly also teased a potential return to

AND then of course there is the Definitive Feasibility Study that NC1 is working toward.

We like that NC1 has been forced to do its DFS in what has very clearly been a “bear market” for nickel assets.

Basically, NC1 has been forced to cut costs wherever possible, and make the project capital efficient enough for it to stand on its two feet in the toughest of nickel markets.

NC1 has also had years to refine its project’s metallurgy - meaning the processing will be as efficient as possible too.

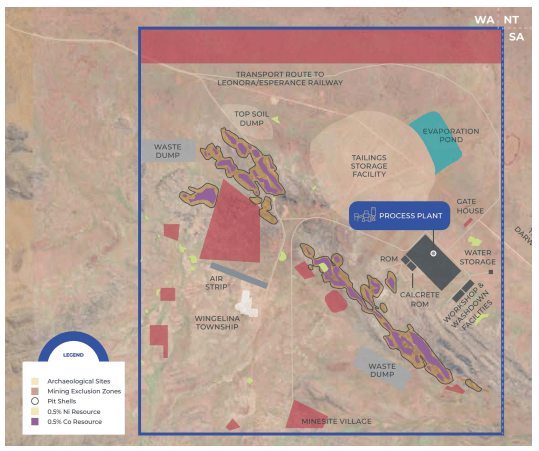

Here is an overview of the planned development:

(source)

Given that costs were already in the first quartile of any nickel assets globally - we think any improvements could make the project stand out even more:

(source)

And so when the next nickel bull market rolls around - NC1 hold a giant pre development asset, that’s been financially optimised and stress tested in bear market scenarios.

Hopefully that means that when the good times come for the nickel market - NC1 will own the asset everyone has their eyes on...

Now we wait for nickel prices to run...

Nico Resources

9 reasons why we Invested in NC1

These reasons were originally published on the 20th of January, 2026.

Check out our full initiation note here: Our latest Investment - Nico Resources (ASX: NC1)

Here they are again, with updates to some where the situation may have changed:

1. NC1 has one of the biggest undeveloped nickel-cobalt projects in the world

NC1 has a JORC resource of ~1.68 million tonnes of nickel and 132k tonnes of cobalt, making it one of the top four largest undeveloped projects in the world. NC1’s project was granted Major Project Status by the Australian government in 2024.

2. Current market cap is only ~$41M.

During the 2022 nickel and battery metals bull run NC1’s share price was close to $2 per share and its market cap ~$160M+. Now NC1’s market cap is ~$41M and its share price 30c per share.

We also think NC1 currently trades at a steep discount to its comparable peers such as Alliance Nickel, Ardea Resources, and Australian Mining based on project reserves and grade.

🚨Update: NC1’s market cap is less that where it was when we first Invested - now ~$26M (at 19c per share).

3. We are backing mining legend Peter Cook (“Cookie”) here.

Before today’s placement industry legend Peter Cook owned ~11.8% of NC1 shares and is the Non-Exec Chairman.

NC1 came out of his other success story Metals X (more on Metals X below).

Another spin out from Metals X was Westgold Resources, now capped at over $5.5BN.

Cookie is also Non-Exec Chairman of one of our best performers from 2025 (TTM) which was up ~132% over the last 12 months.

We are backing Cookie in NC1 to deliver as he has for decades in a string of companies.

🚨 UPDATE: After the recent capital raise, Peter Cook owns 10.7% and Metals X owns 6.75% of NC1. (source)

4. Lowest cost quartile once in production

NC1’s project, once developed, would have operating costs in the first quartile of projects around the world on a nickel equivalent basis. This means the project would be among the 25% cheapest producers once in production.

5. We think future demand for nickel will be underwritten by a mega thematic (humanoid AI robots)

We think “robot metals” will be the next big investment thematic in the resource sector.

The age of the robots is upon us, and billions of humanoid robots are expected to live, work (and fight?) alongside us over the coming years.

They are all powered by similar batteries to Electric Vehicles. We also think securing strategic nickel supply from allies to build AI robot armies will soon be a thing.

6. We think NC1 is the most leveraged nickel exposure on the ASX (basically a giant call option on nickel prices)

When commodity prices run, it's the companies with the biggest resources that are usually leveraged the most to the underlying price moves.

If nickel prices were to go parabolic, we think NC1 will be the preferred nickel development exposure the market looks for (which could re-rate the company’s share price from where it is today).

7. Project is advanced with a PFS completed in 2022 and a DFS on the way

NC1’s Pre Feasibility Study (PFS) showed a Net Present Value of ~$3.34BN using ~US$20,000 nickel prices.

We think that NC1 has had to streamline and make its project as efficient as possible which should mean the upcoming Definitive Feasibility Study is NC1’s best foot forward from an achievable development plan perspective.

8. Spin out from ~$1BN tin miner Metals X

NC1 was born as a spin-out from Metals X, which means the asset was “vend” out by a corporate and not by private vendors.

Metals X still hold their shares in NC1 which tells us the capital structure for NC1 is fairly tight (with a sticky vendor).

🚨 UPDATE: NC1’s major shareholder’s CEO ($1.25BN Metals X CEO Brett Smith) said with respect to NC1’s asset on a recent Money of Mine podcast:

“it's a great asset”, “one of the best undeveloped nickel-cobalt assets in the world”

“like all of the laterite jobs, it just requires a huge amount of CAPEX to get it started”

And here’s a line he said that lives rent free in our heads:

"it'll eventually get built”...

Hey no guarantees of course, like always. He could be wrong.

9. Tight and clean capital structure

NC1 only has 136M shares on issue (post cap raise) and very few options on issue, which means the share price can move quickly, plus several large and (presumably) sticky shareholders (Chairman Peter Cook with ~11.8% and MetalsX with ~7.5%)

🚨 UPDATE: After the recent capital raise, Peter Cook owns 10.7% and Metals X owns 6.75% of NC1. (source)

Ultimately, we hope the above reasons contribute to NC1 achieving our Big Bet which is as follows:

Our NC1 Big Bet:

“NC1 re-rates to $500M+ market cap in a market where the nickel price is rising & as a result, NC1’s project is being considered a takeover target by majors looking for nickel exposure”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our NC1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Nico Resources

What do we want to see NC1 do next?

NC1 just put out its March quarterly report a few days ago (see it in full here). NC1 ended the quarter with $5.42M in cash.

Over the next few months the two main things we want to see NC1 do are:

1. Drill out and upgrade defined resources

NC1 mentioned in the quarterly that to upgrade the current resource in full into the measured category, it would need to do ~200,000m of RC drilling.

But, the focus would be on the highest grade parts of the resource first to get that upgraded.

We want to see NC1 drill out and upgrade its current resources.

Here are the milestones we will be tracking:

🔲 Drilling commences

🔲 Drilling completed

🔲 Resource upgrade completed

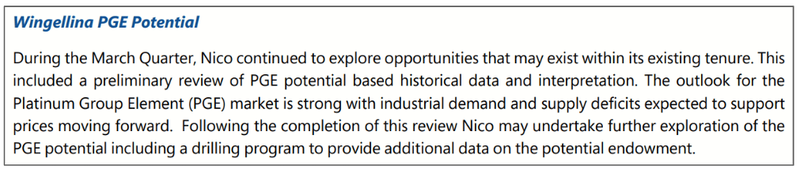

2. Greenfields exploration?

This one we didn’t really expect to see in the quarterly report.

NC1 explicitly mentioned it would “continue to review greenfields exploration opportunities in the Musgraves region” and even had a section on the PGE potential of its broader project area.

(source)

Still very early days on the greenfields stuff, but with NC1’s market cap just $26M, the market may show an interest in a few swing for the fence exploration holes.

What are the risks?

In the short term the key risk for NC1 is “commodity price risk”.

NC1’s valuation is heavily leveraged to the nickel price and market sentiment.

As a result NC1’s share price trades around fluctuations in the nickel price.

If the current supply glut from Indonesia persists or demand from the battery sector softens, nickel prices may remain suppressed.

This could impact the project's economics and potentially re-rate the stock lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should nickel prices remain low for extended periods of time, it could hurt NC1’s share price.

Source: “What could go wrong?” - NC1 Investment Memo 20 January 2026

Other risks

Like any early-stage exploration and development company, NC1 carries significant risk. Here we aim to identify a few more risks.

The estimated capital expenditure of $2.9BN is enormous relative to NC1’s current market cap, creating a massive funding hurdle. This likely means significant future share dilution or the need for a major partner to step in to get the project off the ground.

Building a "monster" project in the remote Musgrave region introduces significant logistical challenges and infrastructure costs. Any delays in permitting or construction could see costs blow out beyond the current PFS estimates.

Processing laterite nickel is technically complex and has historically faced commissioning issues at other global projects. If the metallurgical performance doesn't match lab results, the project's economics could be severely impacted.

While greenfields exploration in the Musgraves is exciting, there is no guarantee that new drilling will yield economic discoveries. Most exploration holes fail to find anything of value, and the cost of these programs can drain cash reserves.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our NC1 Investment Memo

You can read our NC1 Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our NC1 Investment Memo covers:

- What does NC1 do?

- The macro theme for NC1

- Our NC1 Big Bet

- What we want to see NC1 achieve

- Why we are Invested in NC1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.