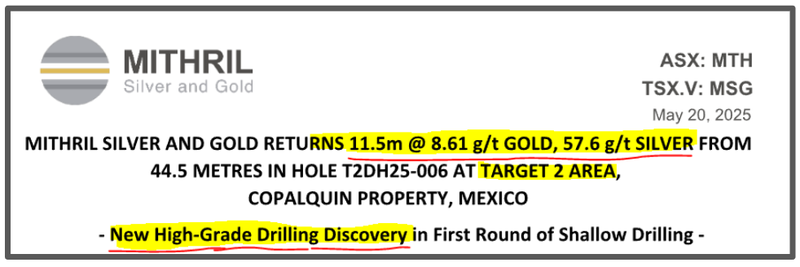

MTH Announces New Discovery: 11.5m at 8.61 g/t GOLD, 57.6 g/t SILVER

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,971,000 MTH Shares and 2,177,000 MTH Options at the time of publishing this article. The Company has been engaged by MTH to share our commentary on the progress of our Investment in MTH over time.

MTH just announced a new gold and silver Discovery.

MTH hit 11.5m at 8.61 g/t GOLD, 57.6 g/t SILVER from 44.5 metres at its “Target Area 2”:

(read the MTH announcement here)

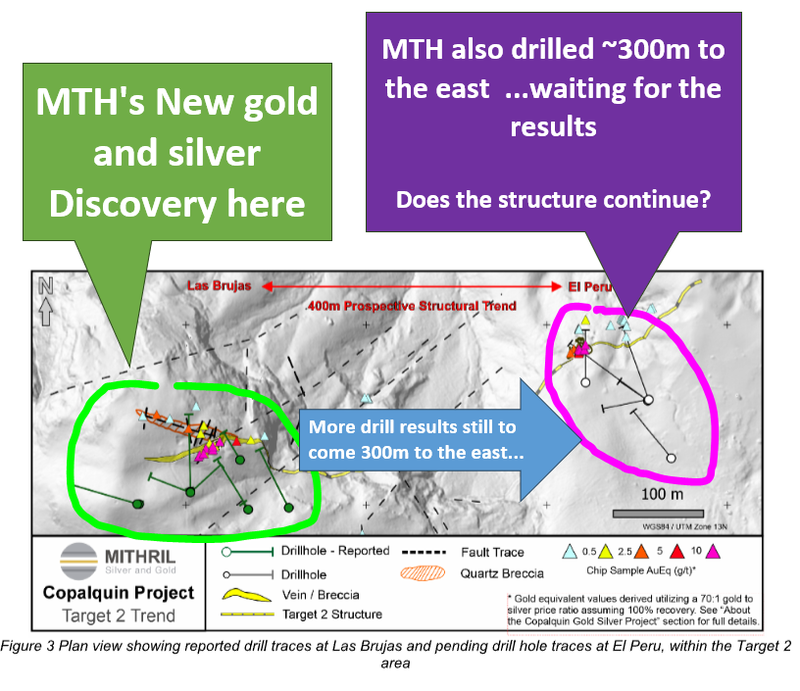

And assays are pending that could extend the discovery from drilling 300m to the east...

MTH’s new discovery today is at its “Target Area 2”.

(these are the first drill results from this Target Area)

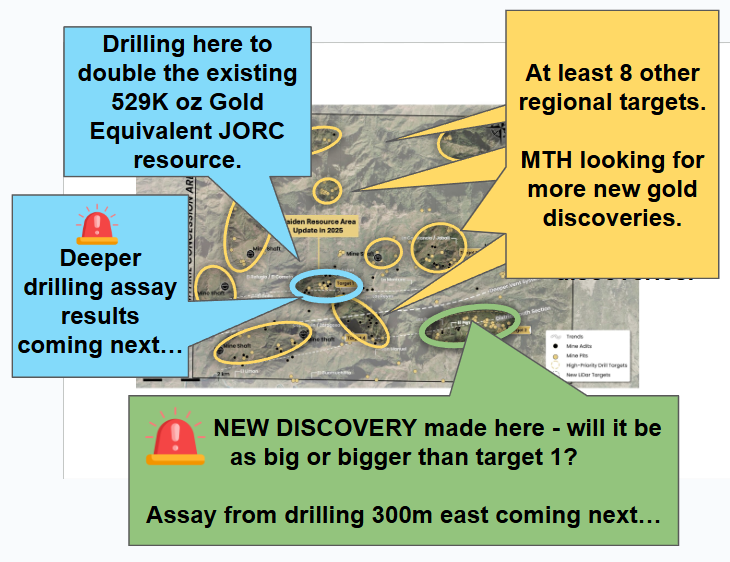

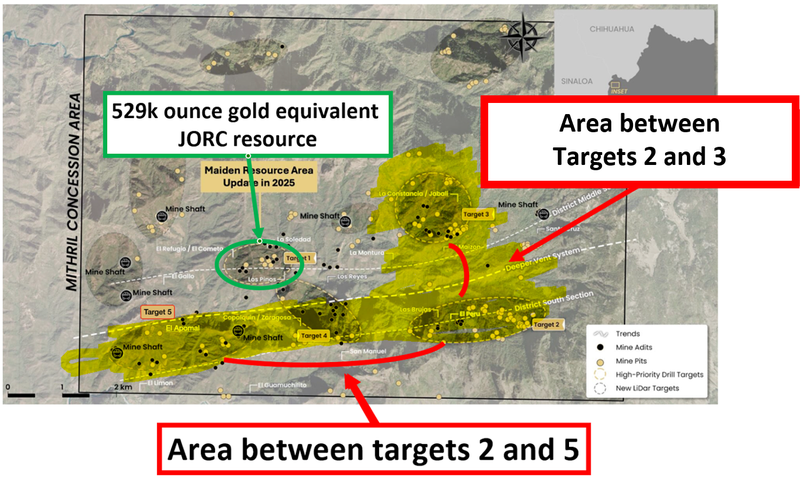

MTH already has a 373Koz gold and 11Moz of silver JORC resource (529,000 ounces of gold equivalent) at its “Target Area 1”...

Where a second drill rig is at work to try and double this JORC resource.

In today’s announcement MTH said that deeper drilling at Target Area 1 “continues to intercept the targeted zone, with samples dispatched for assay”.

Meaning more drill results to watch for in the coming weeks from MTH, from both Target Areas 1 and 2:

MTH is now in a position where it has ~$14.2M in cash (at 31 March 2025), two drill rigs on site and some major catalysts due in the next few months.

We think good news from any of the following catalysts could start to build strong positive momentum in MTH’s share price inside the next 6 months:

- Drill results from today’s discovery - Assays pending 300m to the east and more drilling to come.

- Drill results at depth from existing JORC resource - MTH is still drilling deeper holes below its resource, a big surprise hit here could be material for MTH.

- Doubling of the existing JORC resource - MTH is aiming to have a resource upgrade out inside the next few months.

- More drilling across other regional targets - MTH has $14.2M cash in the bank and plans to drill at least 35,000m across its regional targets this year. Maybe we see more discovery announcements like today?

Why today’s news is big for MTH

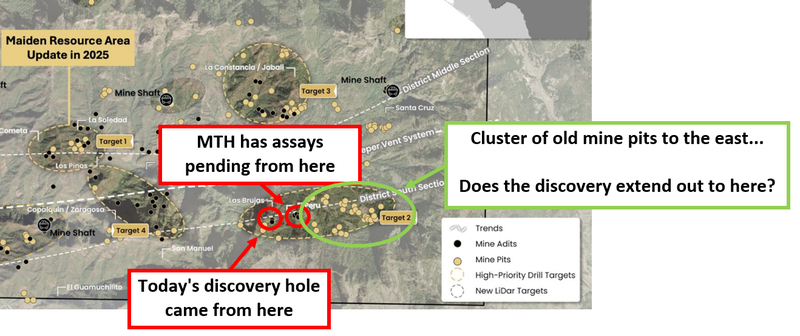

- MTH’s “district scale” theory has been proven - MTH has been talking about the idea of its project having “district scale” meaning there is silver and gold scattered around its entire 70km^2 project area. That theory was proven today with drill results, and there are still at least 8 more regional targets to test.

- There are big clusters of old mine pits to the east - there are giant clusters of old mine pits to the east of today’s discovery hole. Clearly there was enough at surface to get the old timers interested in this part of MTH’s project. Now we know there is gold beneath the surface, there is a good chance this structure extends out towards those old mine pits.

- Assays are pending to the east - To confirm whether or not the structure extends, MTH has drilled to to east, with assays pending. This could increase the strike length of today’s discovery ~600m to the east. These assays will give us a first hint at how big the discovery could be.

We think that with some drilling to the east and west we could start to get a sense of how big MTH’s new discovery could be:

MTH’s current resource sits on Target area 1 - a tiny portion of MTH’s ~70km^2 project area.

Beyond the discovery at Target 2 there is still a huge part of MTH’s project that hasn't seen any drilling yet.

And yet, the bulk of the old mine pits and adits (horizontal tunnels) are still yet to be tested properly.

MTH has already started working on that with a “second exploration camp” having been built to start “aggressive mapping and target generation at Targets 2 and 3”.

Today’s announcement also mentions a “1,000m vertical relief” between Targets 2 and 5... could there be gold/silver veins underneath the surface?

So clearly, MTH is focusing on the areas between those targets (the highlighted areas) in the image below:

Relative to the current JORC resource area, there is clearly still a LOT of exploration left to do here by MTH.

With two rigs on site, we want to see MTH focus most of the 35,000m of drilling in and around those highlighted areas.

Ultimately, we think it will be exploration results that drive a re-rate in MTH’s market cap from where it is today.

Then, as MTH starts to show serious size/scale across its project area we think the competitive tension amongst corporates who may have MTH ‘watchlisted’ will start to increase.

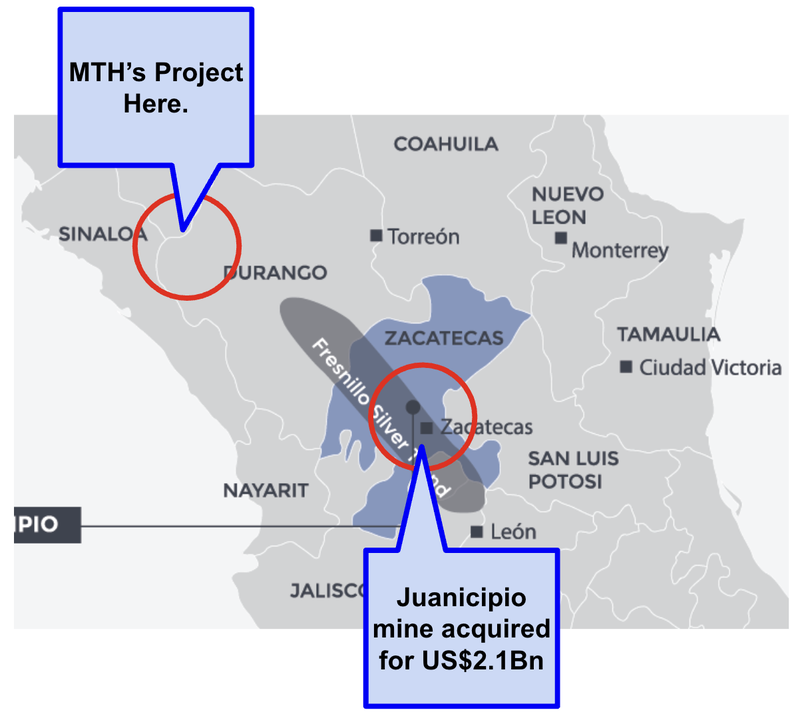

Mexican silver and gold assets are in the spotlight now

In our last MTH note we wrote about how Mexican silver and gold assets could become an M&A hotspot with gold and silver prices trading where they are now.

Mexico is the world’s biggest producer of silver.

Silver is a big part of Mexican DNA - back in the mid 1800s Mexico accounted for ~50% of the world’s silver supply.

Nowadays, it makes up ~25% of all global supply.

Mexico’s established silver mining industry is a big part of the reason why we think corporates are getting active in this part of the world.

(Source)

Here is where that Mag Silver asset sits relative to MTH’s project:

In the months leading up to that Mag Silver deal, we saw two other big deals get done in Mexico:

1. $4.2BN First Majestic bought Gatos Silver for US$970M.

AND

2. $7.4BN Coeur Mining bought Silvercrest in a deal worth US$1.7BN.

One of our long standing investment ideas is that high underlying commodity prices and deals happening amongst the majors could eventually lead to capital trickling down into the smaller end of the market.

Especially into jurisdictions where there is an established mining industry but where the market isn't rewarding assets the same way it is in places like Western Australia (for example).

We watched the following interview with fund manager Adrian Day where we learnt a bit more about this. He talked about M&A, specifically in Mexico starting at 6:00 - and said:

“The opportunity for a company to go in and start acquiring some good Mexican assets - producing or non-producing - and acquire them relatively cheaply, is probably very compelling”

“Someones going to do that sooner or later”

(Source)

As gold and silver prices increase, big company valuations re-rate to a point where they are being asked questions about “growth pipelines” and where they will deploy all of the cash their projects are generating.

Companies then try to answer that question by picking up “growth assets” with a lot of exploration upside.

We have seen the wave of deals start to happen in the gold sector.

We think that a big run up in the silver price could mean the same happens for silver stocks.

However if this happens for silver, , there will be far fewer opportunities out there because of how few pure-play silver companies there are on listed markets (especially here on the ASX).

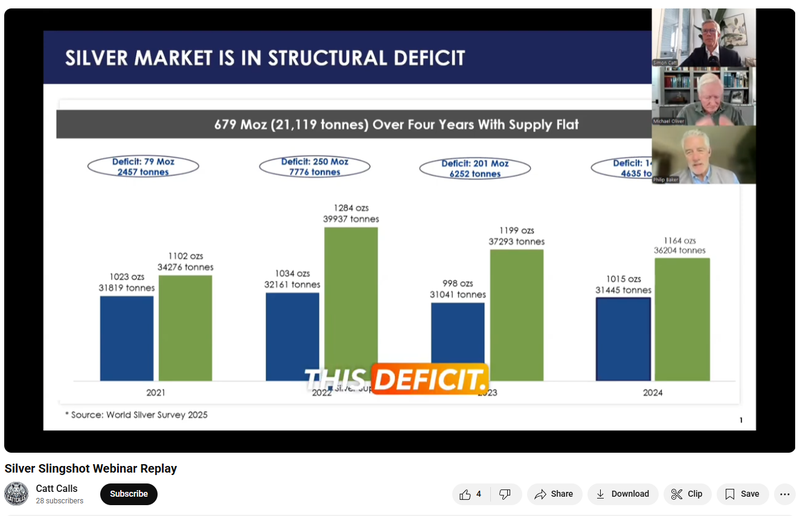

We listened to the following webinar hosted by Simon Catt - the director of Arlington Group Asset Management:

In the webinar he hosts “‘three Masters of the Silververse” who all make a case for why silver prices are about to go on a generational run:

- Eric Sprott (Billionaire investor and legendary silver bull)

- Michael Oliver from Momentum Structural Analysis (charting guru)

- Phil Baker the President & CEO, Hecla Mining (the biggest silver producer in the US and Canada).

(Source)

Anyone who wants to know what the smart institutional money is thinking about the forward silver price should definitely watch this webinar.

For MTH, a higher silver price will mean MTH’s asset becomes more valuable to corporates (and hopefully before that, listed equities investors).

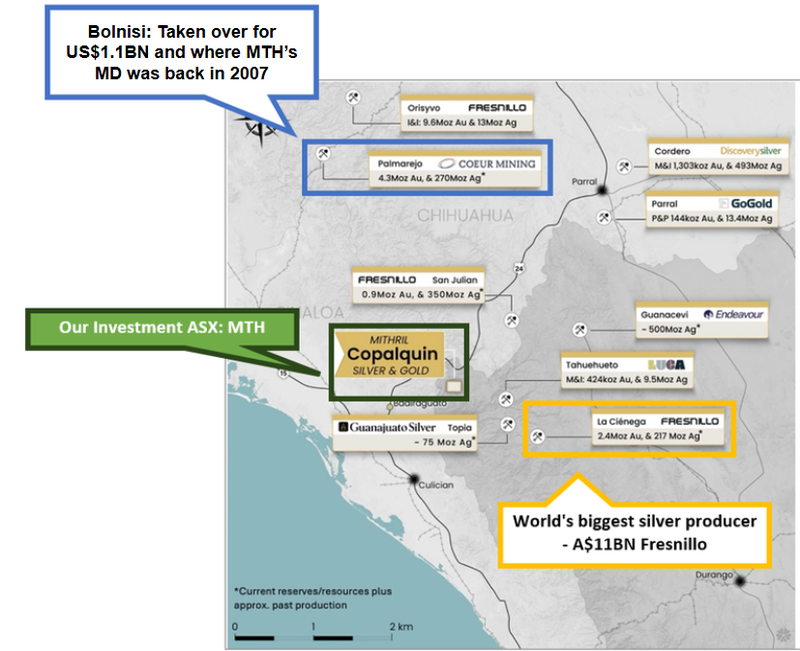

MTH’s MD was behind the US$1.1BN sale of a Mexican asset

One of the key reasons we first Invested in MTH was because of Managing Director John Skeet’s background.

John knows how to take a project in Mexico from exploration stage through to a big takeover deal.

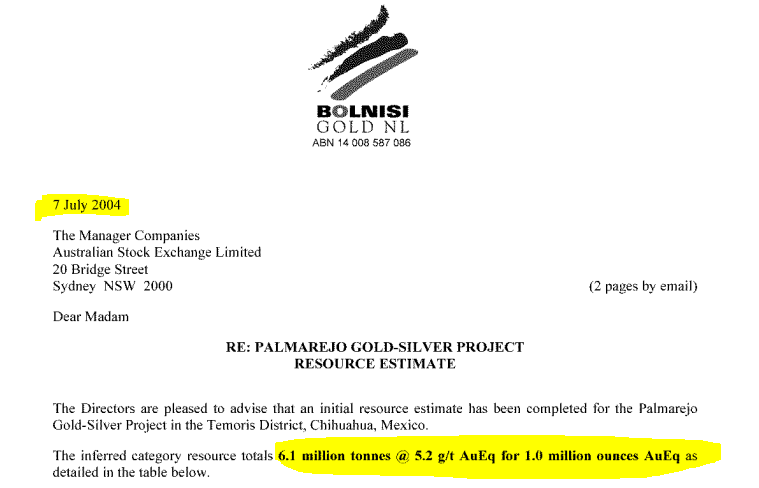

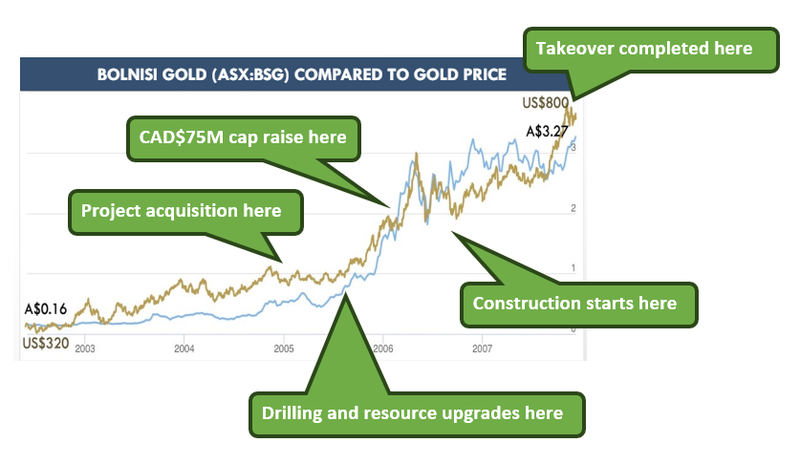

He was the General Manager of Projects for ASX listed Bolnisi which was taken over for ~US$1.1BN ~ 15 years ago.

The early days of Bolnisi remind us a lot of where MTH is now.f

In 2002, Bolnisi acquired the Palmarejo Project in Mexico - at the time the project didn't even have a JORC resource yet.

It wasn't until 2004 that Bolnisi declared the project’s first JORC resource of ~1m gold equivalent ounces.

(Source)

Over the next few years with some more drilling, Bolnisi made new discoveries and increased the project's resource to ~3m ounces of gold.

Off the back of that exploration success, the company raised tens of millions of dollars and moved its resources into higher confidence categories (indicated/measured).

In parallel, Bolnisi got all of its permits sorted, and then took its project into the construction phase.

It was at this time that Bolnisi was taken out by Coeur Mining for US$1.1 billion.

In just a few years, Bolnisi share price went up from ~A$0.16 to ~A$3.27.

A 20x return in just three years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

MTH bought 50% of its project in Mexico in May 2020 and has an option to purchase the remaining 50%.

By mid-2021, MTH had defined an initial 373Koz gold and 11Moz of silver JORC resource.

(529,000 ounces of gold equivalent)

By the middle of this year, MTH aims to double its existing resource to ~1m ounce of gold equivalent.

AND MTH is drilling to make replica or bigger discoveries all over its project area.

Below is where MTH’s project sits relative to that US$1.1BN Bolnisi deal:

MTH has the right backing to make it happen

Bolnisi style success only happens when a small cap stock can get the right mix of technical skill leading the drill programs on the ground, a bullish capital market environment AND institutional corporate backing.

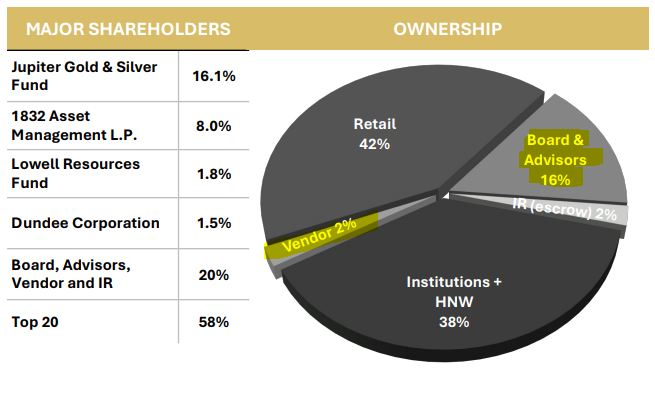

When we first Invested in MTH, the company was majority owned by its directors, and the rest of its register was made up of retail investors.

Now, MTH is in a far stronger position - MTH had ~$14.2M cash in the bank at 31 March 2025 AND it is now backed by some seriously strong institutional investors.

Exactly what’s needed to be able to fund drill programs to see how big this project can get.

Now ~38% of MTH’s is now made up of institutional backers.

MTH’s biggest shareholder, Jupiter Gold and Silver Fund, has had some really big wins in the past.

They were early investors in De Grey Mining which went from a sub $15M micro cap explorer to receiving a $5BN takeover offer from Northern Star - in under 5 years.

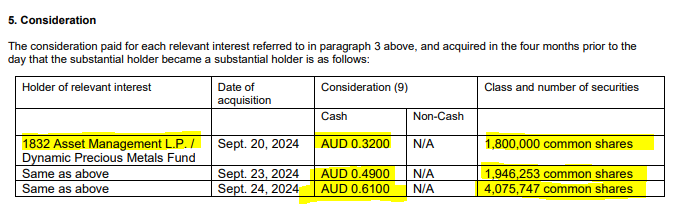

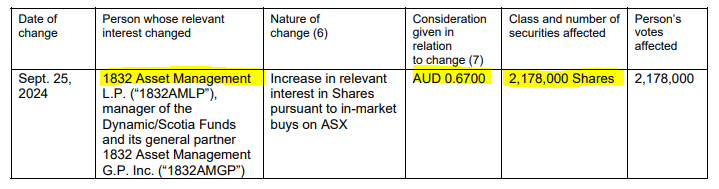

MTH’s second biggest shareholder 1832 Asset Management also has a strong track record in the silver and gold space - they have been buying MTH aggressively all the way up to ~67c per share:

The current board, advisors and vendors also still hold ~18% of MTH so we think they are incentivised to get the best out of MTH’s assets too.

We are backing John (who was one of the vendors of MTH’s project) to get the best out of this project just like he did with Bolnisi’s Plamarejo.

Ultimately, we are Invested in MTH to see it grow its resource and move its project through the development stages. We would also be very satisfied if the company was taken over off the back of a major re-rate in its share price at a big premium...

Our MTH Big Bet

“MTH re-rates to a $150M market cap by expanding its Mexican gold-silver resource with new ultra high-grade silver (and gold) drill hits, taking the project into development and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MTH Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Reminder - 10 reasons why we are Invested in MTH

We first invested in MTH back in May 2024 at 10c per share - here were the key reasons for us initially backing MTH.

Note: These are now 12 months old, so we have put a bit of an update on some that are outdated:

1. MTH was capped at >$110M in 2020 and is now recapped at $8.4M

Back in 2020 off the back of ultra high grade silver/gold intercepts, MTH’s market cap re-rated to above $110M. We made our Investment in MTH in the recap round at a market cap of $8.4M. With some drilling we hope it can re-rate back to those levels again.

Update: MTH briefly touched a ~$81M market cap in September 2024. Now MTH is trading at a market cap of ~$50M. We continue to be Investors, and MTH is one of our biggest positions.

2. High grade gold/silver JORC resource

MTH has a JORC resource with 373k ounces gold and ~11m ounces of silver. The gold grade for the resource is 4.8g/t and silver grades at 141g/t silver. Both extremely high relative to other gold/silver projects in the market.

Update: We are expecting a JORC resource upgrade soon, MTH has flagged a ‘doubling’ of the resource so we will keep an eye out for that - see more in Reason 4.

3. Drill rig already on site

MTH has a drill rig on site ready to go and so we should see a lot of newsflow over the next coming months. We are hoping the drilling leads to a material increase in the company’s JORC resource.

Update: After raising additional funds, MTH is now drilling its project with two rigs on site

4. Potential to double its existing resource

MTH has previously indicated it thinks the project has the potential for a “multi-million ounce gold and silver” deposit. Looking at some of the drill and rock chip results along the east-west trend, we think there is potential to quickly double the existing resource.

Update: MTH has hit some really got drill results in and around its existing JORC resource since our Memo was published. MTH’s JORC resource upgrade is now due within the next few months.

5. CEO & MD John Skeet has been there and done that (billion $ takeover)

John Skeet was GM of projects for Bolnisi Gold from 1997 through to a US$1.1BN deal for its Palmarejo project in Mexico. The takeover was done by the current 7th largest silver company by revenue, New York listed Coeur Mining in 2006. Bolnisi picked up that project in 2004, drilled it out, upgraded its resource and eventually sold it to Coeur 2006. We are hoping Skeet is able to repeat that success with MTH.

6. Silver price is hitting decade highs

Silver demand is increasing because of demand from the solar panel manufacturing industry. Silver production on the other hand is falling. As a result, prices are looking to breakout into decade highs.

Update: At the time of writing our MTH Investment Memo silver was trading at ~US$30/ounce. Today silver is trading at ~US$32/ounce.

7. Gold price is at ALL time highs

Gold prices are currently trading at all time highs against almost every currency. MTH’s project also has exposure to gold with the current resource containing ~373k ounces of gold.

Update: At the time of writing our MTH Investment Memo gold was trading at ~US$2,300/ounce. Today gold is trading at ~US$3,226/ounce.

8. Mexico top silver and gold producer (and this is in a mature mining area)

Mexico is the largest silver producer in the world, and the 7th largest gold producer. MTH’s project sits in Durango state along the “Sierra Madre Trend” which has produced as much as 6.2 billion ounces of silver - equal to roughly 10% of total global historical production. There are major gold-silver mines throughout the trend, home to multiple large precious metals mining companies.

9. MTH drilled one of the ASX’s best gold hits in 2021

In July 2021 MTH delivered a gold-silver hit of 8.26m @ 80.3 g/t gold, 705 g/t silver from 468.34m. This was one of the ASX’s top 10 best gold hits of 2021, and drilling will be taking place around this area of the project imminently, a drill rig is on site and ready to go.

Update: MTH hit 144 g/t Gold, 1,162 g/t Silver over 7.0 metres in early September 2024 and triggered a 7X rally in its share price. We think MTH has the potential to deliver results like this again.

10. Low enterprise value relative to JORC resource

MTH currently trades at an EV per silver equivalent ounce valuation of 27c compared to its TSX and ASX peers which trade in a range of 35c to $1.98 per silver equivalent ounce. Based on the other Mexican high grade exploration/development peer group Mithril's shares could increase 2-4X based on its current resource alone (not including any resource upside potential).

Update: With rising silver/gold prices, most of MTH’s TSX/ASX peers have rallied and so we think there is still a valuation gap between MTH and its listed peers.

What is next for MTH?

🔄 Additional assays (Target 1)

In the March quarterly report we noticed MTH mention that drilling was ongoing for targets at depth around Target 1.

In Today’s announcement MTH these assays are pending.

We are looking forward to those results. Any hint of high grade mineralisation could add to MTH’s eventual resource upgrade in a big way.

🔲 Double JORC resource

We want to see MTH get close to a doubling of its current JORC resource.

This should come once MTH has officially declared a cut-off for its drilling at target area 1.

🔲 Drill results from Target 2

We are hoping to see MTH continue to drill out today’s discovery hit to see how big and high grade it is.

We are especially looking forward to the results from the east/west of today’s hits.

Risks to MTH’s share price in the short term

With drilling currently underway and more assay results to be published over the coming months, we think the key risk in the short term for MTH is “Exploration Risk”.

It’s possible that MTH is unable to find enough significant economic mineralisation, which we would expect to impact MTH’s share price negatively.

Exploration risk

There is no guarantee that MTH’s upcoming drill programs in Mexico are successful and MTH may fail to find economic silver-gold deposits.

Source: “What could go wrong” - MTH Investment Memo 22 May 2024

We list more risks to our MTH Investment Thesis in our Investment Memo here.

Our MTH Investment Memo

You can read our MTH Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our MTH Investment Memo covers:

- What does MTH do?

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.