Micro cap L1M - Gold exploration drilling set for next week

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,375,696 L1M Shares and 3,773,077 L1M Options at the time of publishing this article. The Company has been engaged by L1M to share our commentary on the progress of our Investment in L1M over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

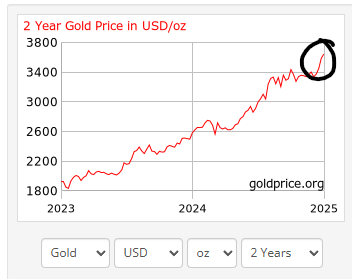

Gold just hit a new all time high overnight of US$3,640 per ounce.

(all time highs again - it's got a habit of doing this lately...)

The ASX small cap market appears ready and willing to re-rate strong gold exploration results...

Great timing for our $7.3M capped exploration Investment Lightning Minerals (ASX:L1M) - who is set to drill test its newly acquired Mt Turner gold-copper project in Queensland next week.

(the timing looks even better given another Queensland gold-copper ASX stock went up ~90% yesterday on a strong exploration result - more on that later... also - past performance is not an indicator of future performance)

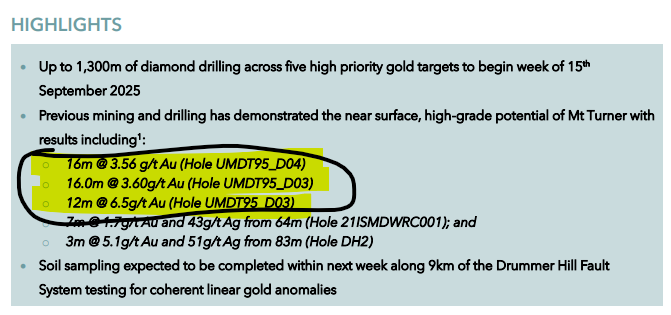

L1M is due to start up to 1,300m of diamond drilling next week, following up strong historical gold hits (scroll down to see them).

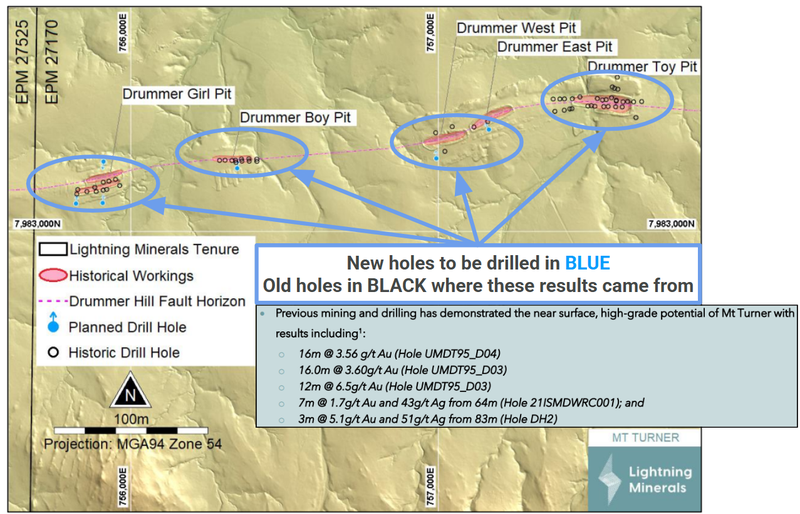

L1M will be drilling targets below five historic open pits that were mined for gold back in the 1980s and 1990s - all along a horizontal fault structure.

All of that old mining was down to max depths of ~20m - which is very shallow...

There hasn’t been much (if any) drilling on the project below 100m depths - even though previous drilling hit intercepts as thick as ~16m and grades as high as 6.5g/t gold.

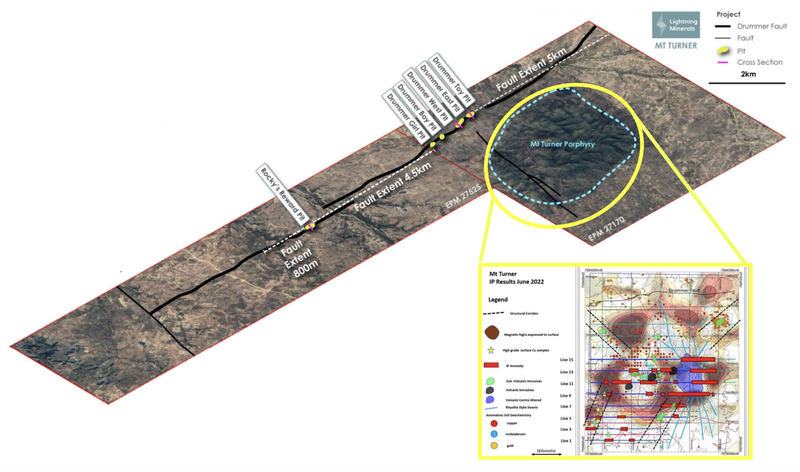

L1M will be the first company to drill test the ~12.5km of strike here and see if it can find repeats of the gold structures that were mined back in the 80s and 90s.

... and then later this year, L1M is planning to put the first drill holes into three copper porphyry targets that sit to east of the gold targets:

The drill rig is locked in and drilling is to start the “week of 15th September 2025” - which, by our calculations, is next week:

(Source)

We first Invested in L1M for its lithium exploration ground in Brazil which was near LRS’ discovery that was bought out by lithium producer Pilbara Minerals for over half a billion dollars.

We still like Brazil as a jurisdiction and lithium as a commodity - however we are also conscious of the market not really rewarding lithium drilling right now.

(that could all change if the lithium price starts to really move up again - but for now it's all about gold.)

Like any good ASX micro cap explorer, L1M has pivoted to a commodity that is hot right now - and that’s gold.

With the gold price where it is and the market willing to take good drill results to market caps close to $100M, we think it’s a good move by L1M.

Queensland gold hits are getting rewarded - can L1M deliver too?

Just yesterday another ASX listed Queensland gold explorer, Zenith Minerals, saw its share price re-rate by ~90% in one day.

At its peak, Zenith is up almost 500% from its lows back in early August.

Yesterday, Zenith released assay results from its first hole on the project and hit 139.7 m at 1.05g/t.

Off the back of that result the share price briefly hit ~15c per share yesterday.

At yesterday’s high of 15c, Zenith was capped at ~$80M...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Zenith has now set a very recent precedent for the type of re-rate that can come from strong exploration results on a gold project in QLD.

And we think our Investment L1M - capped at just $7.3M, is leveraged to strong exploration results from these levels too.

We also noticed that in Zenith’s broader 139.4m intercept, there were two high grade sections - 14.2m at 4.62g/t gold and 9.45m at 5.29g/t gold.

L1M’s ground has delivered similar length intercepts with slightly lower grades intercepts - and given Zenith’s move yesterday, we think this might start to bring heightened market appreciation to what L1M has recently acquired.

Here are some of those old hits on L1M’s ground:

(Source)

With drilling to start imminently, we are looking to see what L1M can follow these up with over the coming months.

What we are looking for over the next 3 months from L1M

We think that strong exploration results could make for L1M share price catalysts before the end of the year (assuming the drilling comes in).

Over the next couple of months as drilling takes place and we await results, the three things we will be watching out for is:

- Visuals in drillcores - this one isn’t an expectation, especially with L1M going for gold, which is relatively hard to see visually in drillcore BUT given the company is using a diamond rig it could happen. This would be an unlikely upside scenario, and even if we don't get visuals during drilling, the lab assays can still deliver very strong assays...

- Assay results from the drilling - ultimately we think this is what will get the L1M share price moving (assuming results are good).

- Soil and rock chip sampling along the ~12.5km of strike to rank new follow up drill targets for the project - the market should like new targets being announced, especially if the first round of drilling comes in.

(Of course, this is early stage exploration and there is no guarantee L1M finds any economic mineralisation on the current round of drilling).

Here is where L1M will be drilling on the map:

(Source)

And here is the ~12.5km of strike that we want to see the soil sampling be done on:

(Source)

Later in today’s note we will share our updated L1M Investment Memo which will cover:

- What L1M does

- The macro theme for L1M

- Our L1M Big Bet

- What we want to see L1M achieve

- Why we are Invested in L1M

- The key risks to our Investment Thesis,

- Our Investment Plan

But before that, here is more on L1M’s newly acquired Australian projects.

L1M’s Queensland gold project also has copper upside

We mentioned earlier that the project L1M is drilling for gold on also has big undrilled copper porphyry targets sitting on it:

Previous geophysics has already mapped these targets across ~16km^2 (which is massive for any drill target) and all three targets are drill ready.

At some point over the next few months, we want to see L1M go out and drill these targets.

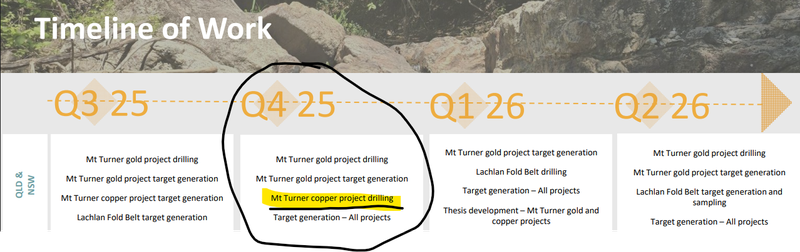

We note L1M did say in a recent investor presentation that drilling on the copper target would happen in Q4 2025... which is next quarter.

(Source)

L1M’s newly acquired NSW assets

As part of the recent Lotus Minerals (the vendor of the gold project L1M is due to drill next week) acquisition, L1M also acquired three NSW and one Victorian Lachlan Fold Belt projects.

Long time shareholders of Latin Resources may recognise these assets, which were previously held by Latin Resources.

Once Latin Resources made a giant lithium discovery in Brazil, it naturally shifted from being a multi asset explorer to being focussed on a single core asset.

When Latin was eventually acquired for A$560M by Pilbara Minerals, the NSW assets had spun out into a private company... and now find their way back to L1M today.

Here is our old quick take on the news: Latin Resources increases landholdings in Lachlan Fold Belt

The Lachlan Fold Belt is known for its porphyry discoveries, discoveries that contain high tonnage gold and copper.

While these projects are in an incredibly early stage, we think that they provide optionality to L1M when it comes to exploration.

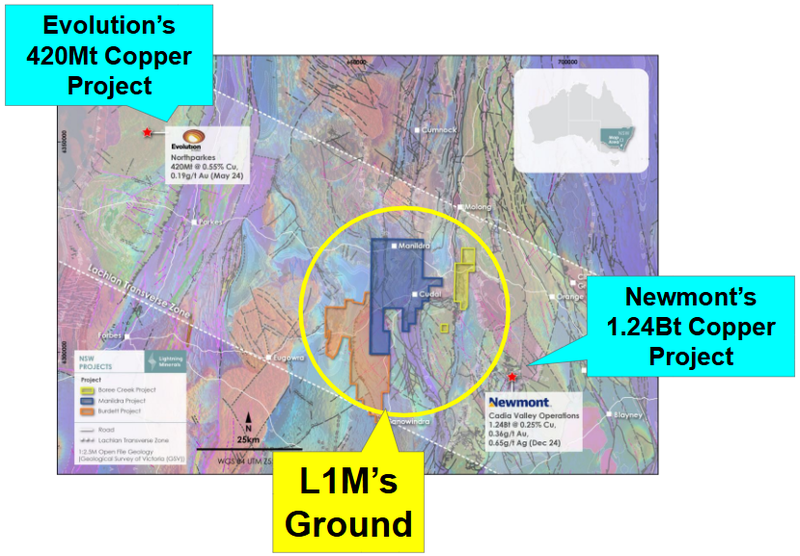

The three NSW projects are sandwiched between $12.3BN Newmont’s Cadia Valley mine (one of the largest gold mines in the country) and the Northparkes mine - which just 18 months ago $19.5BN Evolution Mining took an 80% interest in:

The “bet” with large porphyry potential projects is that if a discovery is made, they could become multi-million ounce projects that are worth billions of dollars over a long, long period of time.

Porphyries can be expensive to drill even if a discovery is made, they require a lot of deep diamond drilling which is usually out of the scope of a junior to fund.

So even if a discovery is made (chances are low), it's a long hard road, especially for a junior company.

On these assets, we want to see L1M generate interesting drill targets (doing all of the technical target generation work) and eventually look to de-risk the drilling costs through some sort of partnership.

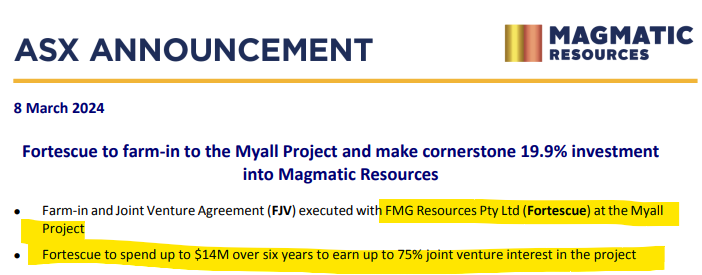

We saw ~18 months ago $57BN Fortescue Metals farmed-in to a project ~50km from that Evolution asset committing to spend ~A$14M over 6 years as well as taking an interest in Magmatic.

(Source)

We think something similar to that for L1M would be a big win on these projects.

(no guarantees of course, this is an upside scenario that may not eventuate.)

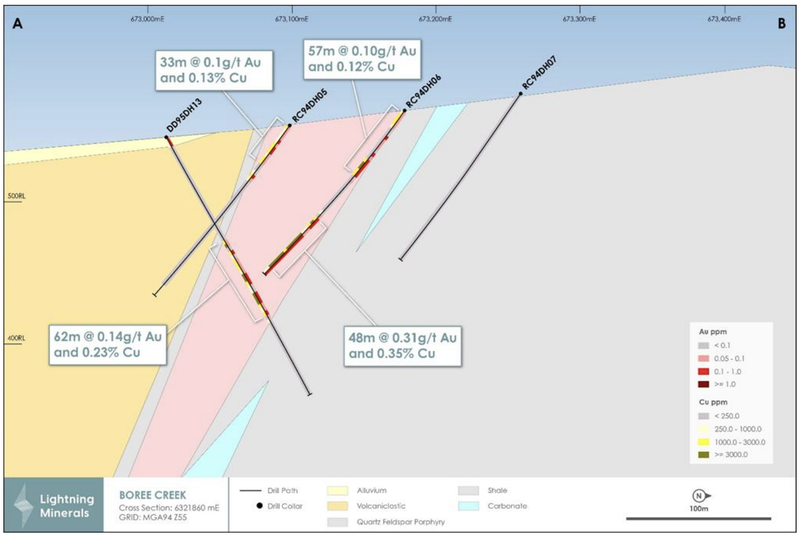

From the three projects L1M acquired in the Lachlan Fold Belt, the Boree Creek project already contains a proven porphyry system that has yet to be tested at depth or along strike.

A prior drill hole intersected 48m @ 0.35% Cu and 0.31g/t AU from 96m (amongst other drill results showing mineralisation), which we think clearly warrants further follow up.

(Source)

Whilst the Lachlan Fold Belt projects won’t be the initial focus for L1M, the project is firmly on our radar - particularly if L1M can find a farm-in partner for the project.

What’s next for L1M?

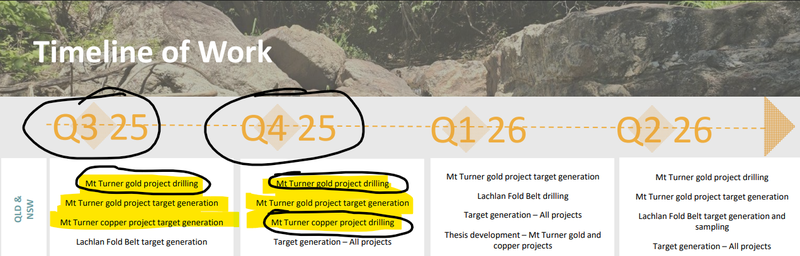

Over the next two quarters, L1M’s plan is to drill both the gold and copper targets at its newly acquired QLD asset.

With drilling set to start next week, the main thing we want to see from L1M is the completion of both those drill programs and the assay results.

(Source)

Beyond that, we will be watching out for soil sampling and more pre-drilling work across both projects:

- Along the ~12.5km of strike that extends beyond the areas L1M will be initially drilling on the gold side.

- And target generation work to finalise the drill locations on the three copper porphyry targets that are already defined.

Our new L1M Investment Memo

With L1M having completed the acquisition of additional gold and copper assets, we think now is the right time to release a new L1M Investment Memo:

In our new Investment Memo, we cover:

- What L1M does

- The macro theme for L1M

- Our L1M Big Bet

- What we want to see L1M achieve

- Why we are Invested in L1M

- The key risks to our Investment Thesis,

- Our Investment Plan

Lightning Minerals Investment Memo #2

Memo Opened: 12th September 2025

Shares Held: 8,375,696

Options Held: 3,773,077

What does L1M do?

L1M is a junior exploration company with gold-copper projects in Australia and lithium projects Brazil.

What is the macro theme behind L1M?

L1M has exposure to:

- Gold - a precious metal which is often seen as an insurance against inflation, uncertain markets and as a reserve asset. Gold is trading at all time highs at the time of this memo.

- Copper - the third most widely used metal in the world, leveraged to the global electrification thematic.

- Lithium - exposure to the electrification thematic because of its use in EV/storage batteries.

Our L1M Big Bet:

“L1M discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our L1M Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 8 Reasons We Invested in L1M

- Tiny market cap, leveraged to exploration success - L1M is capped at just $7.3M at the time of writing this Investment Memo. We think L1M’s valuation here is leveraged to exploration success.

- Multi-commodity exposure - L1M now has a mix of gold, copper and lithium exploration projects in its portfolio. We like this, especially in a very small explorer, because it means the company can pivot to a project that the market will be willing to re-rate based on the current macro momentum in any particular sector.

- Drilling to start on gold projects very soon (short term catalyst) - L1M’s QLD gold project has over 12.5km of strike that hasn’t seen any modern drilling yet. We like that L1M will be drilling the project in the coming weeks.

- QLD project has had good gold hits before - Previous drilling on L1M’s QLD gold project has hit 16m at 3.56 g/t gold, 16.0m at 3.60g/t gold and 12m at 6.5g/t gold. We think the market will like results similar to or better than this (IF L1M can deliver them).

- QLD project has multiple undrilled copper porphyry targets - L1M also has three copper porphyry targets that have already been identified on its QLD asset. We think these are strong drill targets for a company of L1M’s market cap.

- NSW copper-gold asset is in the same region as majors - L1M’s NSW asset in particular, sits next to projects owned by Newmont and Evolution Mining.

- Bear market lithium exposure - L1M has lithium ground in Brazil’s Minas Gerais next to heavyweights like Sigma Lithium (60km away) and Pilbara Minerals (20km away). If market interest returns to the lithium sector, L1M’s assets could suddenly become more valuable.

- We have had success Investing in Brazilian lithium before - One of our best Investments was Latin Resources, which made a hard rock lithium discovery and was re-rated to a high of ~42c per share—2,332% above our Initial Entry Price.

What do we want to see L1M do next?

Objective 1: Drilling at L1M’s gold targets in QLD

L1M expects drilling to start the week beginning 15th September.

Milestones

🔲 Drilling commenced

🔲 Drilling visuals

🔲 Assay results

Objective 2: Drilling on L1M’s copper targets in QLD

We want to see L1M drill its three copper porphyry targets right after the upcoming gold drilling is completed.

Milestones:

🔲 Geophysics

🔲 Program of work defined

🔲 Drilling commenced

🔲 Assay results

Objective #3: Target generation across the QLD, NSW and Vic assets

We want to see soil sampling, geophysics and other geochemical work completed across all of the newly acquired assets.

Ideally, new drill targets will be ranked across all projects ready for drilling in 2026.

Milestones

🔲 Geochemical sampling (soils, trenching)

🔲 Geophysical surveys

🔲 Identify drill targets

Objective #4: Target generation across the other assets

L1M plans to continue working on its Brazilian lithium and WA lithium/gold assets.

We are still looking forward to seeing new targets ranked across these over the coming months. Especially on the lithium which could become interesting again if the macro sentiment changes for the sector

Milestones:

🔲 Geochemical sampling (soils, trenching)

🔲 Geophysical surveys

🔲 Identify drill targets

What are the risks?

Exploration risk

L1M is still a long way from a discovery, and even further from defining a resource.

Like all micro cap minerals explorers, the risk is that L1M finds no economic mineralisation on its assets - in which case we would expect to see the share price re-rate lower.

Delay risk

L1M plans to drill two parts of its project (the gold targets and the copper targets) all before the end of the year.

There is a risk there is some slippage in these timelines and IF L1M were to have big enough delays it could lead to the market losing interest in the stock.

Significant delays could be negative for L1M’s share price as it would burn down the company’s cash balance and bring the company to a position where it needs to raise more capital and dilute existing shareholders.

Funding risk/dilution risk

As a pre revenue explorer, L1M is dependent on capital markets to fund ongoing drilling and development.

That could come at discounted prices and further dilute existing shareholders.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract.

Should gold or copper prices fall, this could hurt the L1M’s share price.

We have already seen this happen with the lithium price and what it meant for L1M’s Brazilian assets.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking L1M’s share price with it.

Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other risks

L1M is still a very early-stage gold and copper explorer with no defined resource. There is a material risk that drilling returns uneconomic results and the company makes no commercial discovery.

L1M’s valuation is highly leveraged to exploration success, and with a small market cap (~$7.3M) any disappointment in drill results could lead to share price downside.

The company is also dependent on timely regulatory approvals and drill program execution. Any delays, such as permitting setbacks or drill rig availability issues, could push out timelines and cause the market to lose interest.

As a pre-revenue junior, L1M is reliant on capital markets to fund exploration. Should market conditions tighten or investor sentiment turn negative, L1M may need to raise additional funds at lower prices, diluting existing shareholders.

L1M is also exposed to commodity price fluctuations. A sustained decline in gold or copper prices would negatively impact investor sentiment, reduce funding appetite and could make projects uneconomic, regardless of exploration success.

Finally, while the recently acquired NSW and Victorian projects sit in a highly prospective region, they are still very early-stage and may never attract a farm-in partner or deliver economic drill results.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

We are Invested in L1M to make a discovery and define a gold discovery.

Our plan is to hold the majority of our position in L1M into the upcoming drilling program.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.