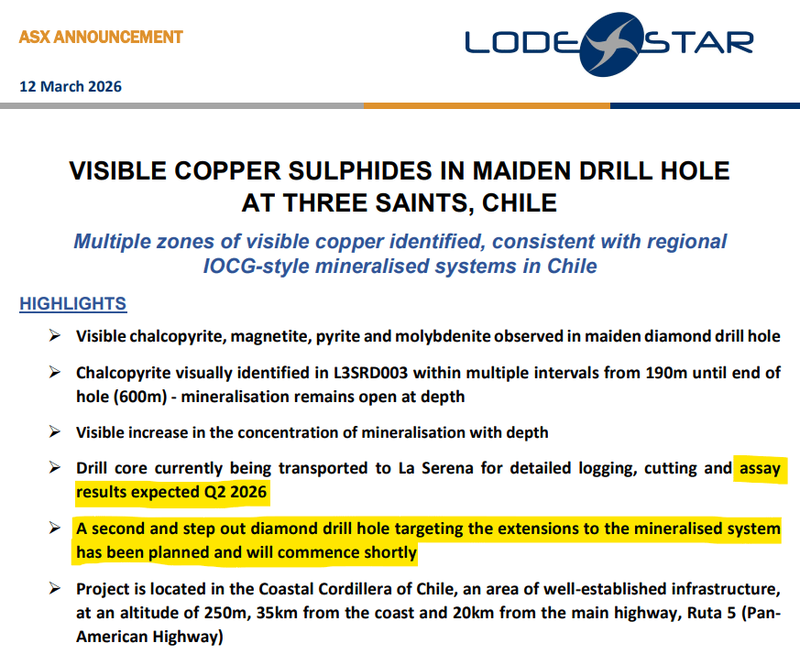

LSR's “blind” moonshot copper drilling - 1st hole: visible copper sulphides from 190m to 600m, ending in mineralisation.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 38,596,178 LSR Shares and 26,627,263 LSR Options at the time of publishing this article. The Company has been engaged by LSR to share our commentary on the progress of our Investment in LSR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

We have been talking a lot about the metals needed to feed the global AI and AI robot buildout.

AI and AI robots do work in return for electricity...

(not for salaries like us meat sacks).

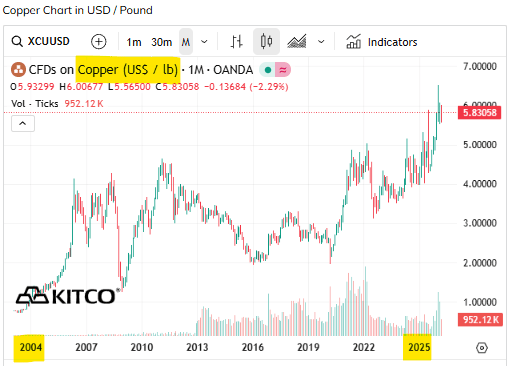

Copper will be crucial for AI and AI robots because it’s the metal that carries the massive amounts of electricity (and data) needed to run energy‐hungry data centres, smart devices, and autonomous robots.

(and as the AI and AI robot boom gathers steam, the copper price is hitting new all time highs).

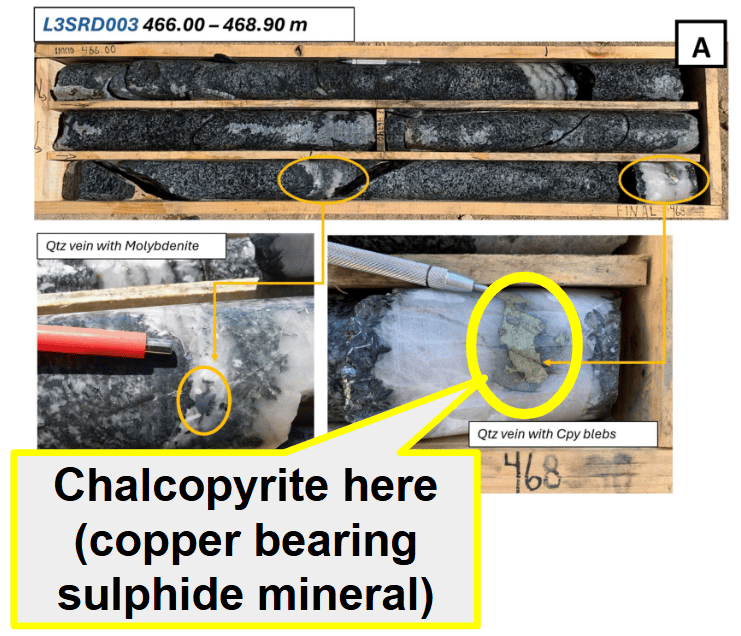

This morning, our $14M capped exploration Investment Lodestar Minerals (ASX:LSR) hit “visible chalcopyrite (copper sulphide)” across multiple intervals from 190m all the way to the end of the hole at 600m.

That's zones of copper over ~410m.

With the hole ending in mineralisation (where the intensity of visible sulphides looks to be getting stronger).

From the first ever drill hole into this project.

Here are some photos of the drill core showing visible chalcopyrite:

(source)

We note these are visual estimates only. Assay results will ultimately determine whether or not this is actually economic grade copper. We stress that visual sulphide abundance does not directly correlate with copper grade.

This is from a completely blind, never drilled before target sitting in Chile (monster copper country).

“Blind” exploration means no mineral outcrop at surface, no obvious visual expressions, and very little target generation work to figure out the best place to drill - it was more drilling on a geologist's “hunch”.

(Drilling “blind” is a high risk manoeuvre, so our and the market’s expectations on this drill were pretty low - and its looking very good so far)

Assay results are due next quarter - this is where we find out what specific copper grades are present (as opposed to a site geologist estimating by eyeball).

This is when we will really find out what LSR could be sitting on...

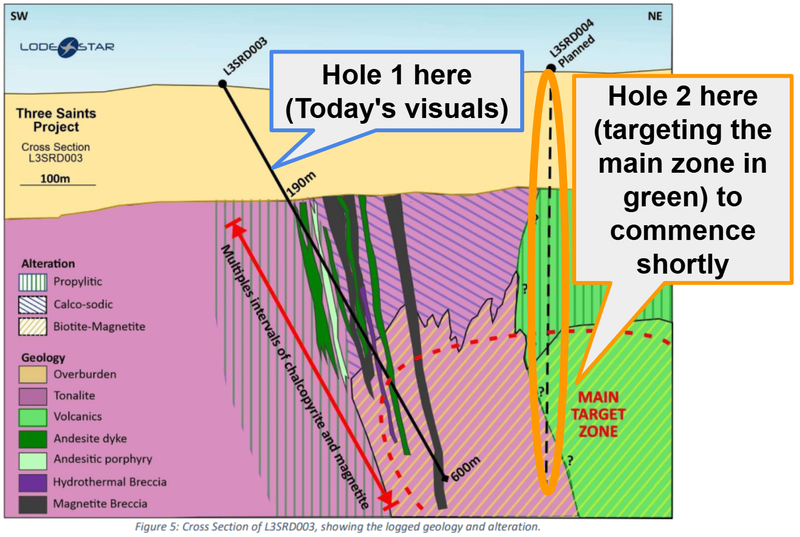

LSR is confident enough in today’s result that a second hole is planned to start in the next few days drilling into the “Main Target Zone”.

At a time when AI datacentres and autonomous robots’ growing hunger for copper is driving up the copper price to record all-time highs:

Last week we said:

“We think there is almost no expectation baked into LSR’s share price for this drilling - which means if it does come in it could catch the market off guard and be a catalyst for a re-rate.”

Hundred of meters of visible copper sulphides is a great first pass result... no we just wait for the assay results.

The key takeaways for us on hole 1 are that:

- LSR has hit the right type of rocks

- from a “blind” target no one in the market really expected anything from

- the hole ended in mineralisation

- AND LSR has a second hole starting on the project within days.

(source)

So far, so good from what was a pure greenfield target.

We should know exactly what LSR has found with the next hole - a 500m vertical hole directly into the “Main Target Zone”:

(source)

Assays from the first hole will tell us the types of grades sitting around the Main Target Zone and the second hole (being drilled right now) should confirm (or not) that the system extends into the Main Target Zone for the project.

Before we go on, it's important to note that these are visual observations only, not assay results. We won't know what the copper grades actually are until the assay results come back.

Visual chalcopyrite in the core does not necessarily mean economic copper grades - assays could come back disappointing. That's the risk.

But what we do know right now is that there are visible copper sulphides over 410m in the FIRST hole drilled into a never-before-drilled target.

And the mineralisation styles LSR is seeing are consistent with IOCG-style (Iron Oxide Copper Gold) mineral systems.

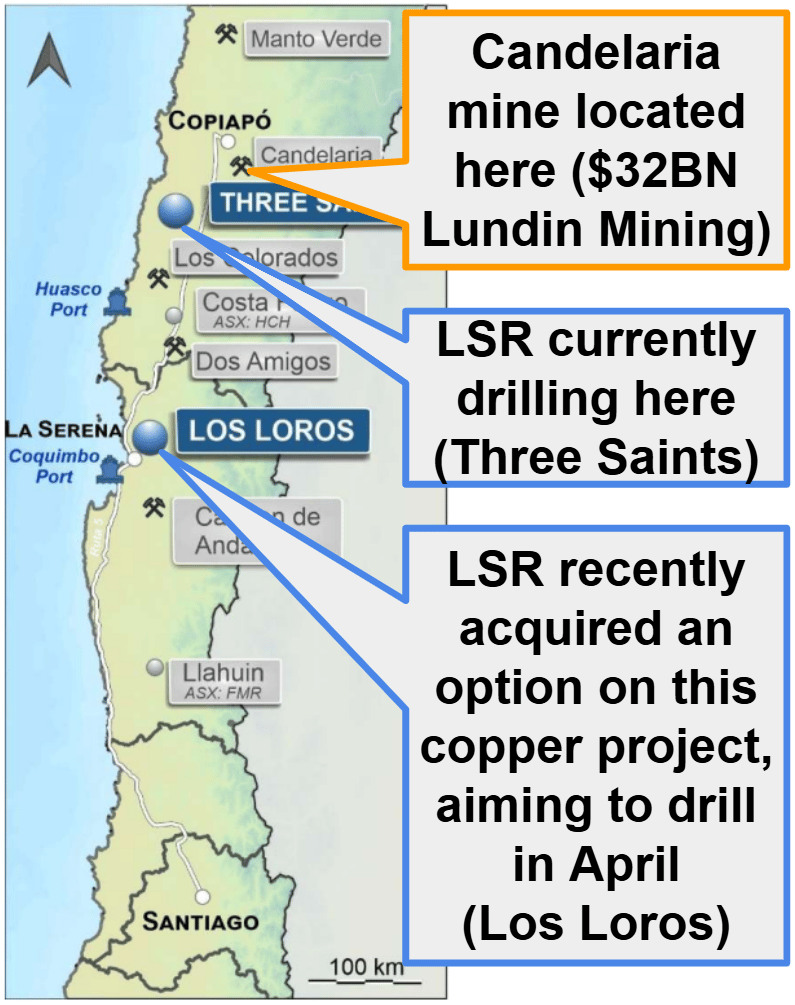

The same style system as the Candelaria Mine (owned by the $32BN Lundin Mining), one of the biggest copper-gold mines in Chile, sitting in the same regional belt as LSR's project:

(source)

We think the style of mineralisation (IOCG deposit) is important, because when they come in, they tend to be fairly big.

For example, Candelaria’s resource contains over 5BN pounds of copper.

Obviously, it's very early days, and there is a massive gap between "visible copper sulphides in a first hole" and a world-class copper deposit.

But the geological style and setting look like the right ingredients...

Now we wait for the assays (and the second hole to be drilled).

A reminder - all of this is from the "side salad" asset (maybe now becoming the main course?) for the US heavy rare earths asset LSR owns.

(We first Invested in LSR for the US heavy rare earths asset).

More on LSR’s US heavy rare earths asset

While the Chilean copper has our attention right now, given drilling is happening, the main reason we first Invested in LSR in October last year was for its US heavy rare earths asset in Arizona.

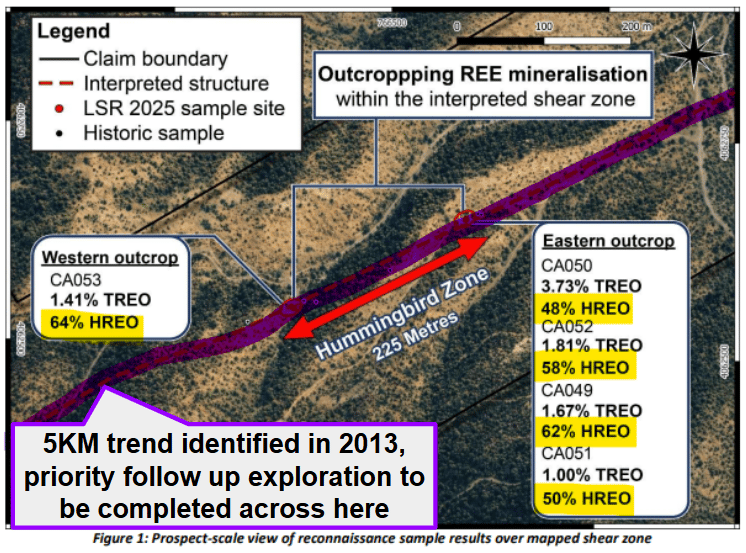

A few weeks ago, LSR returned rock chip samples up to 3.73% TREO, with 64% of that being HEAVY rare earths across a ~225m outcrop within a ~5km interpreted structural trend.

(source)

Heavy rare earths are the harder to find, scarcer suite of rare earths, critical for building, sustaining and upgrading next-generation:

- Artificial Intelligence (AI)

- AI-driven defence

- Autonomous war robots and drones

- Quantum computing, and

- Advanced energy technologies.

We think access to and control over HEAVY rare earths will likely determine who leads the world in these technologies (and who becomes the next global superpower).

So it's kinda important to NOT be 100% sourcing the heavy rare earths you need to win this race (USA) from your main adversaries (China), who also want to win the race.

A few weeks ago, the US Department of War put this statement outlining “securing rare earth elements a national security imperative”:

(source)

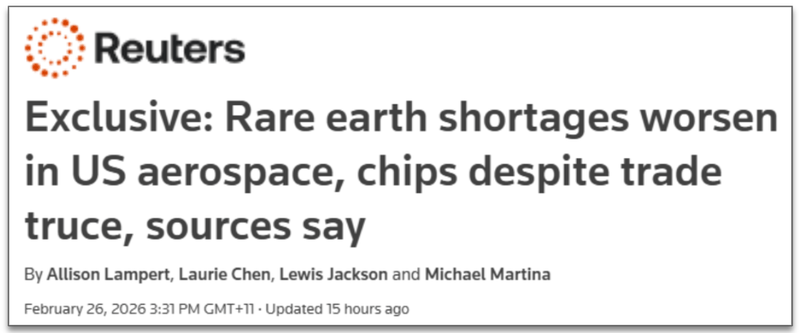

Then two days later, Reuters had a special report on the US rare earth shortages (especially in US aerospace) getting worse inside the US... here is that Reuters report:

(source)

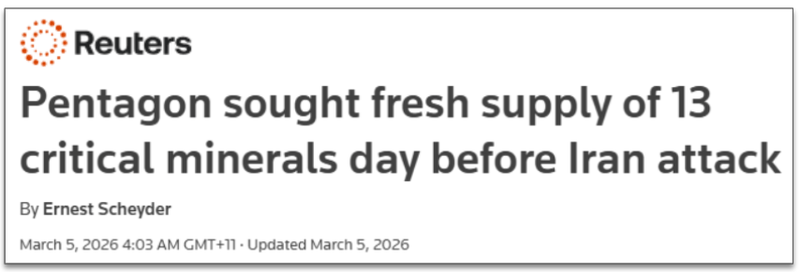

Then just last week, we found out that the Pentagon (US Department of War) is asking a group of domestic companies and research organisations to help boost the supply of 13 critical minerals...

Including Yttrium (a heavy rare earth).

(only a day before the Iran attack - which says a lot about the urgency)

(source)

One of the rare earth elements mentioned over and over again was Yttrium - Yttrium prices are up 69x (hehe) versus this time last year.

(source)

LSR’s US heavy rare earths asset “contains high concentrations” of that exact rare earth element (alongside many other heavy rare earths):

(Source)

Noting that LSR’s USA project is pre-discovery and still at a very early stage - so we will need to see some more exploration before we know how much of these heavy rare earths the project contains.

We Invested in LSR because we think heavy rare earths assets inside the US will be one of the big winners from the attention and capital pouring into the sector inside US borders.

We're still waiting on the mineralogical study results (expected this month), which will tell LSR what type of rocks the rare earths are hosted in and inform how they might be processed.

A quick side note - yesterday the only group of companies on our watchlist that were green were the US critical metals stocks... (hopefully a flow on effect of the above translating to interest in companies in the space again).

So we now have three

- Chile copper - visible copper sulphides in the maiden hole, second hole to start any day now, assays due Q2 2026

- US heavy rare earths - high grade sampling results, mineralogical studies due this month, and a ~5km structural trend to test.

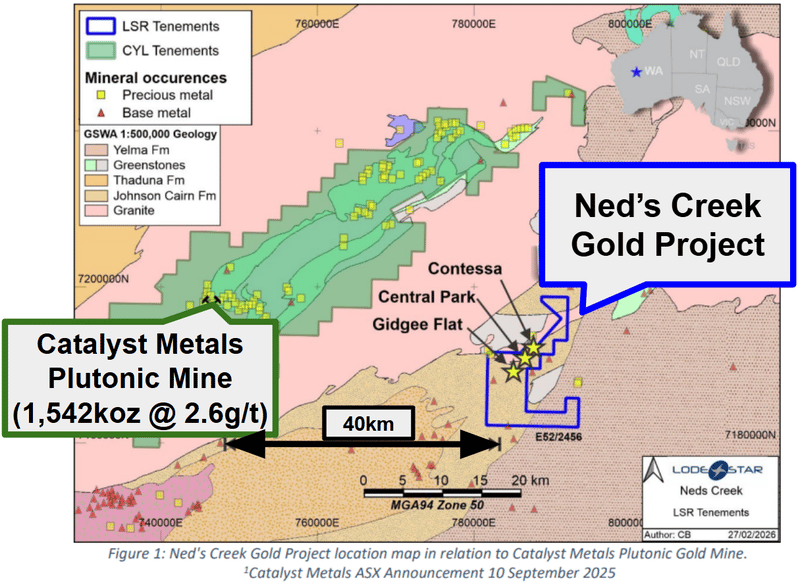

Oh, and LSR also has a 10,000m drill program planned on its WA gold project looking to drill out the 250,000 to 300,000 ounce exploration target it set a few weeks ago.

LSR expects that drill program to start in “late march” and the resource estimate to be finalised this year...

That project sits in the same part of WA as $1.8BN Catalyst Metals’s core asset - so any major resource defined could also have corporate appeal too.

(source)

With LSR capped at ~$14M, we will take success on any of the three projects, but our Big Bet for the company written when we first Invested centres around the US heavy rare earths project as follows:

Our LSR Big Bet:

"LSR makes an economic discovery on its US heavy rare earths projects and re-rates 1,000% from our Initial Entry Price"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our LSR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Lodestar Minerals

What's next for LSR?

🔄 Chile drilling - Three Saints Project

The first hole has come back with visible copper sulphides. Now we wait for:

- ✅ Maiden drill hole completed (600m)

- ✅ Visible copper mineralisation identified (chalcopyrite from 190m to 600m)

- 🔄 Second diamond drill hole underway (L3SRD004, planned 500m depth - expected ~3 weeks)

- 🔲 Second hole visual results

- 🔲 Assay results from hole 1 (expected Q2 2026)

- 🔲 Assay results from hole 2

🔄 Target generation on the US rare earths project

We want to see LSR continue to advance its US asset with mineralogical studies and then plan the next round of exploration.

- ✅ Mapping and sampling (soil and rock chips)

- 🔄 Mineralogical studies (results expected March)

- 🔲 Geophysics

- 🔲 Drill targets confirmed

🔄 10,000m drilling program on WA gold project

LSR expects to be drilling the asset in “late March” - we are hoping to see the 250,000 to 300,000 ounce exploration target converted into a maiden resource estimate post drilling.

Here are the milestones we are tracking on that project:

- 🔲 Drilling starts

- 🔲 Assay results

- 🔲 Resource estimate

🔲 LSR also has a second copper project in Chile (Los Loros)

Beyond Three Saints, LSR also has an option to acquire a second copper project that was previously drilled by the United Nations and supermajor $75BN Anglo American.

(source)

Since 1969 no one has done any modern geophysics on that project - so there could be more to come on this front too.

Back in early February when LSR acquired the option, it was aiming to be drilling here in April this year, so LSR is expecting there to be newsflow from here in the near term also. (source)

What could go wrong?

The key risk right now on LSR’s copper project in Chile is assay results.

There is no guarantee that the visuals today translate to anything considered economic.

Visual chalcopyrite in drill core looks encouraging, but visual estimates of mineral abundance should not be regarded as a proxy or substitute for laboratory analysis.

There is no guarantee the copper grades will be economic - the assays could come back with low grades that don't justify further drilling.

If that were to happen, it could negatively impact LSR's share price.

Another risk is “funding risk”.

LSR just drilled its first hole and has another deep vertical hole coming.

LSR is also planning a 10,000m drill program on its WA gold project.

All of this will mean LSR has committed to a fair bit of exploration spend this quarter and going into Q2-2026.

LSR had $2.9M cash at December 31, so the company may need to raise capital to fund future exploration programs. This could create some short-term weakness in the share price.

Funding risk/dilution risk

As a pre-revenue small cap company, LSR is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, LSR could struggle to access capital on favourable terms. These capital raises may take place at a discount and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong” - LSR Investment Memo 27 October 2025

Other risks

Like any early-stage exploration company, LSR carries a high degree of risk. Here we aim to identify a few more.

LSR is operating at the very early stages of the mining lifecycle. Despite the encouraging visual results from the first hole, the Three Saints project is a single drill hole into a target with no prior drilling history. One hole does not make a discovery, and significantly more drilling and positive assays will be required before the project's potential can be properly assessed.

Even if assay results are positive, converting a visual observation into a JORC resource and then into an economic mining operation would require many years of additional drilling, feasibility work, permitting and hundreds of millions of dollars in capital expenditure. LSR is a very long way from that scenario.

For its US heavy rare earths project, LSR's current data is based solely on surface rock chips and sampling. There is no guarantee these high grades continue at depth or form a continuous, economic deposit. Heavy rare earths can also be notoriously difficult and expensive to extract, and the upcoming mineralogical studies may reveal complex metallurgy.

LSR's current share price is also partly leveraged to the "US critical minerals" macro thematic and the current geopolitical environment. If tensions de-escalate or underlying commodity prices decline, the strategic premium attached to LSR's assets could diminish.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LSR Investment Memo

You can read our LSR Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LSR Investment Memo covers:

- What does LSR do?

- The macro theme for LSR

- Our LSR Big Bet

- What we want to see LSR achieve

- Why we are Invested in LSR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.