LSR: unexplained share price run forces “visible copper” results release while drill hole is still in progress - Approaching main target now

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 35,546,000 LSR Shares and 26,627,263 LSR Options at the time of publishing this article. The Company has been engaged by LSR to share our commentary on the progress of our Investment in LSR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The great modern, global buildouts of our generation that will drive the next commodities boom are all “high tech”.

They need a LOT of electricity... meaning they need a lot of copper.

AI data centres, autonomous robots, military rebuilds and drones all want their cut of this metal.

Global copper demand is set to outstrip supply by ~10M tonnes a year by 2035.

While no major new mines have been built in over a decade...

The copper price just quietly hit the highest it’s EVER been:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our Investment Lodestar Minerals (ASX:LSR) is potentially on the cusp of a new copper discovery in Chile - assay results are pending...

Chile is the world’s leading copper supplier with 22% to 27% of global mined supply.

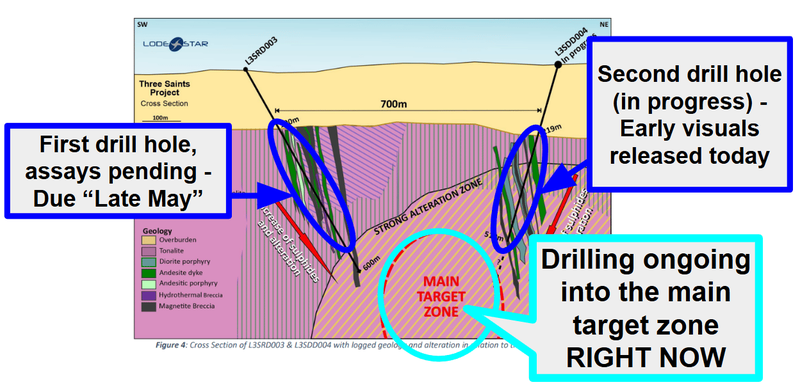

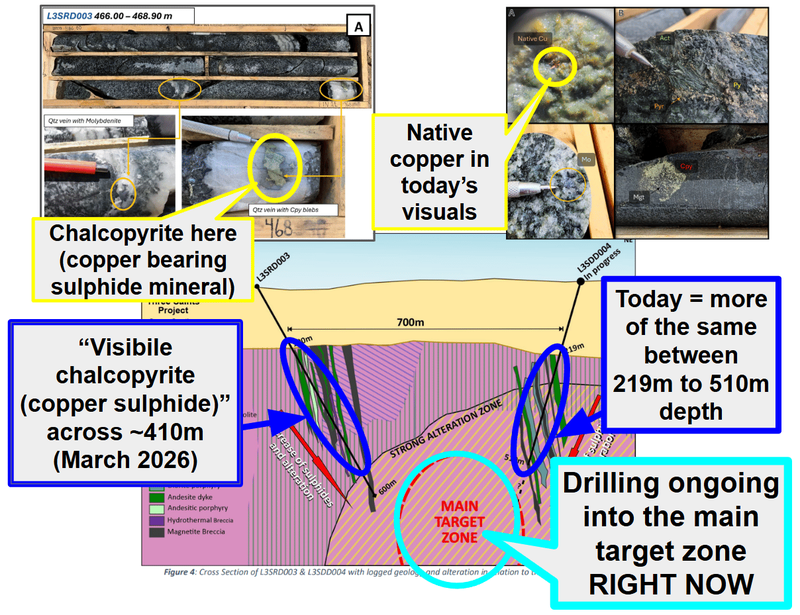

A few weeks ago LSR started drilling its project in Chile and hit “visible chalcopyrite (copper sulphide)” (zones of copper over ~410m - ending in mineralisation).

Then immediately after, LSR started drilling its second hole.

(always a good signal that the company likes what it’s seeing).

A full 700m away from the first drill hole - a proper step-out, swing for the fences exploration hole.

And today... more visual copper - like that first hole, only ~700m away.

(source)

So two sets of visual copper in holes ~700m apart, both ending in mineralisation.

So why is LSR releasing early updates on a partially completed drillhole that is still drilling towards its main target right now?

This ain’t no 3 month, deep oil & gas well, where we expect regular updates on drilling progress.

Three days ago, the LSR share price started running on no news.

It looks like they have been forced to “cleanse” the market by releasing an non-usual update on a drill hole that is still in progress (Today: LSR response to ASX price query):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

As we said above, this second drill hole is not even finished yet. Drilling is approaching the main target area right now:

(source)

The “Main Target Zone” is the zone LSR is hoping to be “sulphide rich”.

(sulphides are what copper is hosted in).

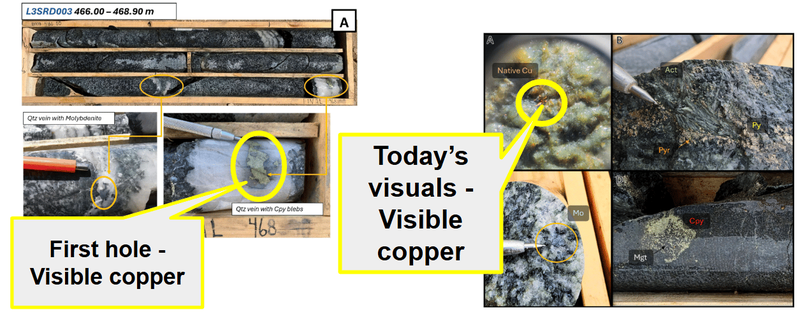

Before we go on, it's important to note that the current sulphides and visual copper reported by LSR are eyeball observations by geologists only, not lab assay results.

We won't know what the copper grades actually are until the assay results come back.

Visual chalcopyrite in the core does not necessarily mean economic copper grades - so be mentally and emotionally prepared that the assays could come back disappointing.

That being said, here’s what the visuals from look like (so far):

Assay results from the FIRST hole are due any week now.

Assay results from the SECOND (more important) hole should be a few weeks after that.

(they need to finish drilling it first and hit that Main Target Zone)

Assays from the first hole will tell us the types of grades sitting around the Main Target Zone.

The second hole - ESPECIALLY assays from the part LSR is still drilling right now will confirm whether or not LSR has made a major new copper discovery.

So we should know whether or not LSR’s made a big new discovery within the next couple of months...

(source)

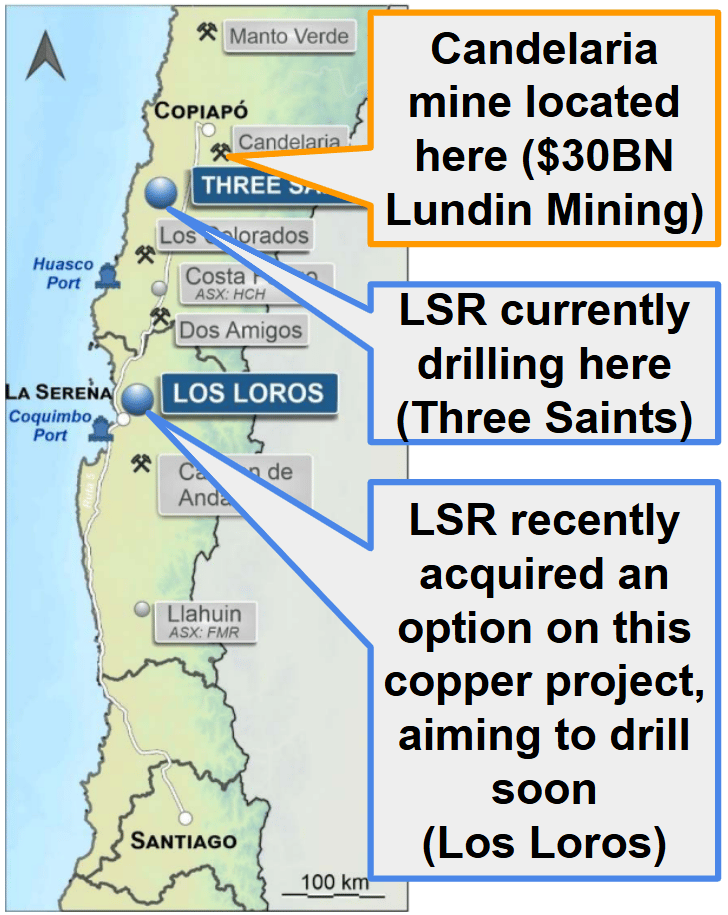

What we have now with LSR is two holes that are both hitting the right type of rocks - similar to what’s usually found above large IOCG copper systems.

Similar in style to the mineralisation found at the giant Candelaria Mine, owned by the $30BN Lundin Mining.

Candelaria is one of the biggest copper-gold mines in Chile with a resource containing over 5BN pounds of copper.

Here is where that project sits relative to where LSR is drilling right now - only ~65km away:

(source)

We think the style of mineralisation (IOCG deposit) is important because this type of asset is very well understood in Chile and these type systems have been put into production in the country in the past.

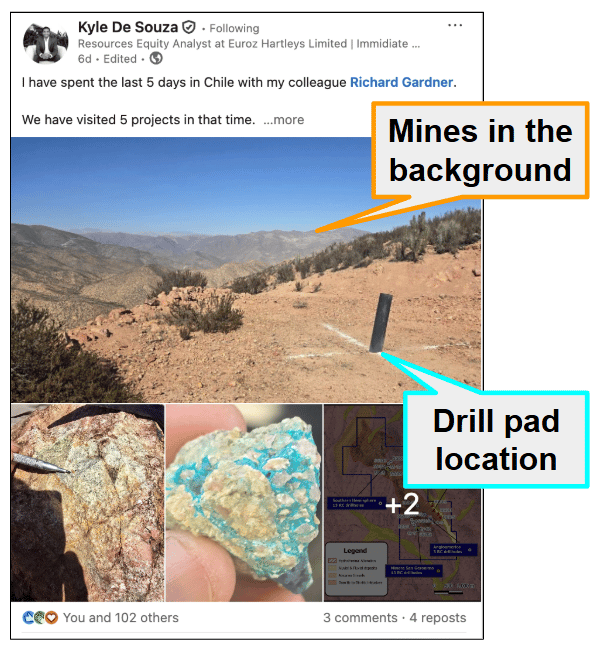

We also came across is a LinkedIn post by stock broking firm Euroz Hartley’s Resources Equities analyst Kyle De Souza, pointing out two operating mines visible from one of LSR’s project’s (yep, he went to Chile to see it):

(source)

Obviously, it's very early days, and there is a massive gap between "visible copper sulphides in a first hole" and discovering a world-class copper deposit.

But the geological style and setting look like the right ingredients...

Now we wait for the assays (and the second hole to drill into that Main Target Zone).

A reminder - all of this is from what we thought was the "side salad" asset (maybe now becoming the main course?) for the US heavy rare earths asset LSR owns.

(We first Invested in LSR for the US heavy rare earths asset).

A quick overview of LSR’s US heavy rare earths asset

For now, the focus with LSR is on the Chilean copper asset.

But the main reason we first Invested in LSR was for its US heavy rare earths exploration asset.

Which contains high-grade heavy rare earths like dysprosium, terbium and lutetium.

The type of rare earth elements that the US needs the most (and has very little of).

We also found out that LSR’s project has three of the highest-value heavy rare earths, all on the US critical minerals list, and all export-controlled by China.

Dysprosium, terbium and lutetium - all of which are used to produce:

- Artificial Intelligence (AI)

- AI-driven defence

- Autonomous war robots and drones

- Quantum computing, and

- Advanced energy technologies.

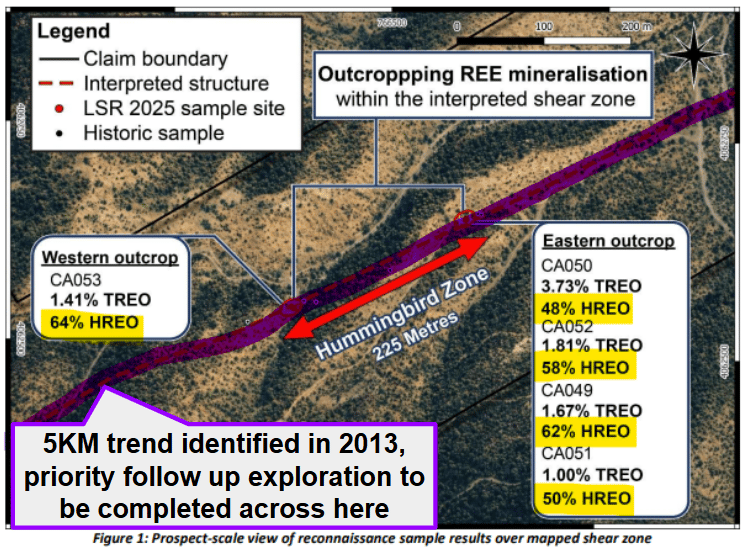

LSR’s project has rock chip samples up to 3.73% TREO, with 64% of that being HEAVY rare earths across a ~225m outcrop within a ~5km interpreted structural trend.

It’s very early days in exploration though - so far LSR is yet to drill the project.

(source)

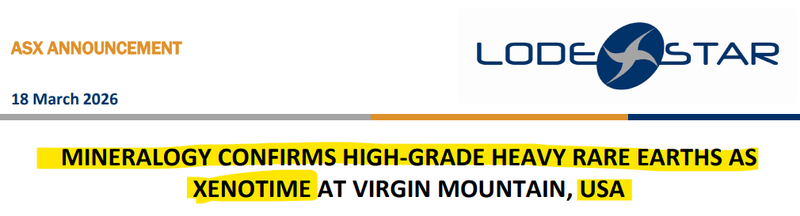

More recently, LSR announced that mineralogy testing of its project showed the rare earths are hosted in “xenotime” - a well-known rare earth host rock that the west understands and can extract with conventional processing.

(unlike most rare earth projects, which are more like “chemistry experiments” to try and economically extract the goodies)

(source)

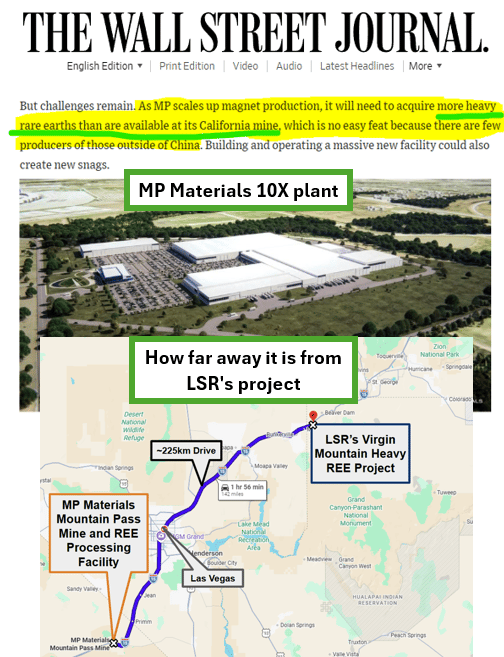

One of the main reasons we Invested in LSR was because we think the US, which already has light rare earth production coming from $15BN MP Materials’ mine in California, will need domestic heavy rare earth feedstock to feed MP’s expanded magnet production facility.

MP (helped along by funds from the US Pentagon) is building a plant, literally called the “10X plant” and has been on the record saying they will need to source heavy rare earths to feed into it. (source)

That plant sits ~225km away from LSR’s project:

We think that urgency within the US recently went up a notch (post the Iran war starting). So, IF LSR’s project shows any signs of size/scale it could become a strategically important asset inside US borders.

Again, it's worth noting that at this stage, it is still very early days for this project, we really need to see it drilled to find out if anything potentially economic sits on it.

See our deep dive on the US asset here: LSR: Dysprosium, terbium and lutetium in xenotime... huh? The market liked it.

LSR is also drilling its WA gold project right now - first assays due in 7-10 days

LSR also has one more project - which we think the market isn’t really factoring into LSR’s current valuation.

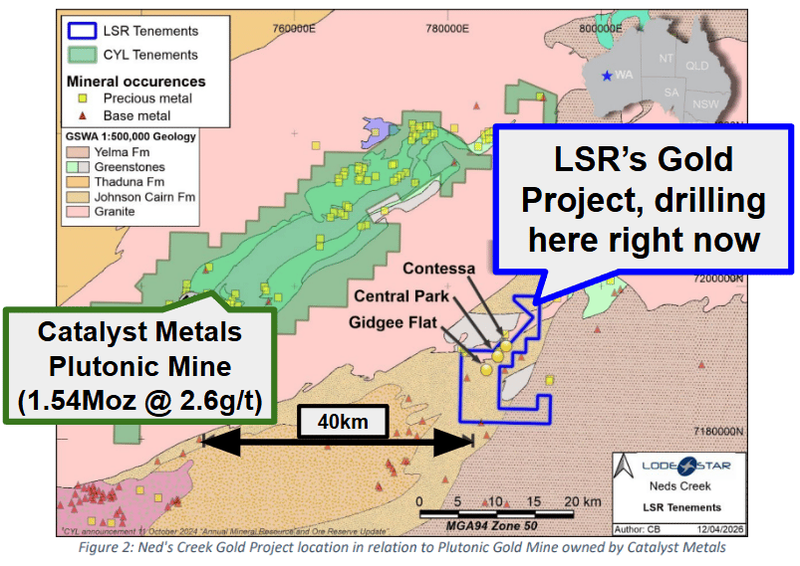

LSR owns 100% of a gold project in WA ~40km from $1.6BN Catalyst Metals' Plutonic Gold Mine (1.5M ounces in reserves) AND within trucking distance of nearby mills.

(source)

A few months ago, LSR announced a gold exploration target for the project of ~250,000-300,000 ounces.

(source)

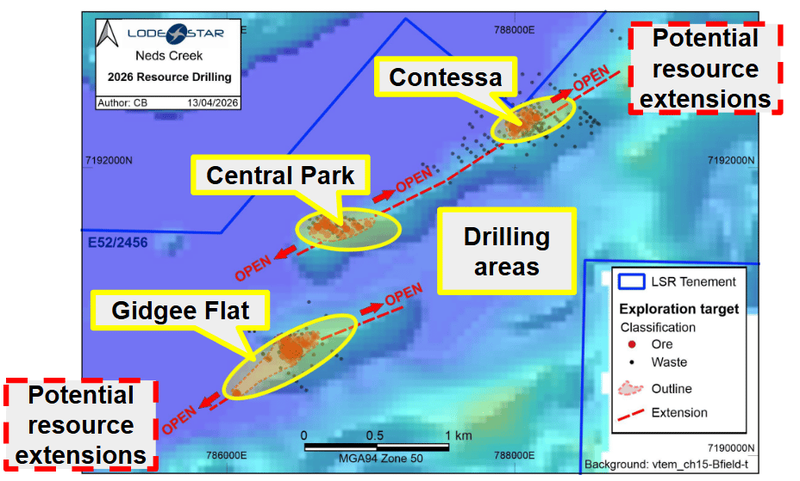

And then on the 16th of April, LSR started a 10,000m drill campaign on the project, aiming to convert that exploration target into a maiden gold resource.

(source)

So over the next few months we also get exposure to LSR drilling out this project.

(and hopefully defining a fairly large gold resource estimate before the end of the year).

LSR says drilling is expected to run for approximately two months, with first assay results anticipated in the next 7-10 days.

And that the maiden resource is being targeted for completion this calendar year.

Here is where the drilling is targeting:

(source)

Ultimately though, in the short term we think the main driver of LSR’s share price will be the results from the copper asset.

Obviously, with the share price running from ~1.1c to ~2.8c at last close, there is a fair bit of expectation being built into LSR’s share price about what will come from the assays.

BUT LSR’s market cap is still only just $33M.

(past performance is not an indicator of future performance)

We think that IF LSR does make an economic copper discovery in Chile, then LSR’s current valuation is still leveraged to a re-rate much higher.

(and of course, the opposite outcome if the results disappoint - there is no guarantee’s here, exploration is extremely risky and more often than not assays fail to confirm new discoveries)

Anything from LSR’s other two assets will be an added bonus - and may even catch the market off guard to the upside.

Again, with LSR’s current market cap only $33M, we think any unexpected wins, could be a trigger for a re-rate in LSR’s share price - which could help the company achieve the second half of our Big Bet as follows:

Our LSR Big Bet:

"LSR makes an economic discovery on its US heavy rare earths projects and re-rates 1,000% from our Initial Entry Price"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our LSR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's next for LSR?

🔄 Chile drilling - Three Saints Project

Now we have two holes with visible copper in them.

What we are hoping to see next is the assays confirm that there is economic quantities (and hopefully enough for LSR to officially declare a discovery).

Here are the milestones we are tracking:

- ✅ Maiden drill hole completed (600m)

- ✅ Visible copper mineralisation identified (visible copper from 190m to 600m)

- 🔄 Second diamond drill hole underway (reached 510m of 600m, could be extended)

- TODAY, possibly more to come) ✅ Second hole visual results (

- 🔲 Assay results from hole 1 (First results expected from “Late May”)

- 🔲 Assay results from hole 2 (Assays expected “Early July)

🔄 Target generation on the US rare earths project

We want to see LSR continue to advance its US asset with mineralogical studies and then plan the next round of exploration.

Here are the milestones we are tracking for the US asset:

- ✅ Mapping and sampling (soil and rock chips)

- ✅ Mineralogical studies

- 🔲 Geophysics/ follow up field work (starting in April)

- 🔲 Drill targets confirmed

🔄 10,000m drilling program on WA gold project

Drilling on this asset started a few weeks ago.

We are hoping to see the 250,000 to 300,000 ounce exploration target converted into a maiden resource estimate post drilling.

Here are the milestones we are tracking on that project:

- ✅ Drilling starts

- 🔲 Assay results

- 🔲 Resource estimate

🔲 LSR also has a second copper project in Chile (Los Loros)

Beyond Three Saints, LSR also has an option to acquire a second copper project that was previously drilled by the United Nations and supermajor $71BN Anglo American.

(source)

Since 1969 no one has done any modern geophysics on that project - so there could be more to come on this front too.

Back in early February when LSR acquired the option, it was aiming to be drilling here in April this year, so LSR is expecting there to be newsflow from here in the near term also. (source)

What could go wrong?

The key risk right now on LSR’s copper project in Chile is assay results.

There is no guarantee that the visuals announced today or last month translate to anything considered economic.

Visual chalcopyrite in drill core looks encouraging, but visual estimates of mineral abundance should not be regarded as a proxy or substitute for laboratory analysis.

There is no guarantee the copper grades will be economic - the assays could come back with low grades that don't justify further drilling.

If that were to happen, it could negatively impact LSR's share price.

Another risk is “funding risk”.

LSR is drilling its second deep hole (of a total four that were started/planned) on the project in Chile AND has a 10,000m program started on its WA project.

All of this will mean LSR has committed to a fair bit of exploration spend this quarter and going into the next one.

LSR had $2.9M cash at December 31, so like all pre revenue mining exploration companies, the company may need to raise capital to fund future exploration programs. This could create some short-term weakness in the share price.

Funding risk/dilution risk

As a pre-revenue small cap company, LSR is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, LSR could struggle to access capital on favourable terms. These capital raises may take place at a discount and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong” - LSR Investment Memo 27 October 2025

Other risks

Like any early-stage exploration company, LSR carries significant risk, here we aim to identify a few more risks.

Running active exploration programs across three different continents is a major logistical challenge. This can stretch management’s bandwidth thin and lead to potential operational delays or oversight issues as they juggle projects in Chile, the US, and Australia.

While early mineralogy on the US rare earths asset is encouraging, the actual extraction and processing of these elements is technically complex. There is no guarantee that LSR will be able to achieve commercial recovery rates even if they confirm high-grade mineralisation.

The ultimate value of any discovery is also highly sensitive to the global prices of copper and rare earths. A significant downturn in these volatile commodity markets could render a technical discovery uneconomic to develop into a mine.

Moving from exploration to development involves rigorous environmental and permitting hurdles in all three jurisdictions. Any delays in obtaining these necessary approvals can stall progress for years and significantly increase the company's total capital requirements.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LSR Investment Memo

You can read our LSR Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LSR Investment Memo covers:

- What does LSR do?

- The macro theme for LSR

- Our LSR Big Bet

- What we want to see LSR achieve

- Why we are Invested in LSR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.