LKY: Produces 99.5% antimony trioxide. Used in ~72% of military equipment. 100% USA sourced. First on the ASX.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,890,278 LKY Shares at the time of publishing this article. The Company has been engaged by LKY to share our commentary on the progress of our Investment in LKY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

It looks like the US is preparing to unleash a second wave of capital to revive its domestic critical minerals industry.

Continuing its urgent efforts to reduce its dependency on Chinese imports of critical minerals used in military applications.

It started in July last year when the US Department of War invested US$400M into the USA’s critical metals champion MP Materials, and subsequently announced billions in further funding for US-based critical minerals projects.

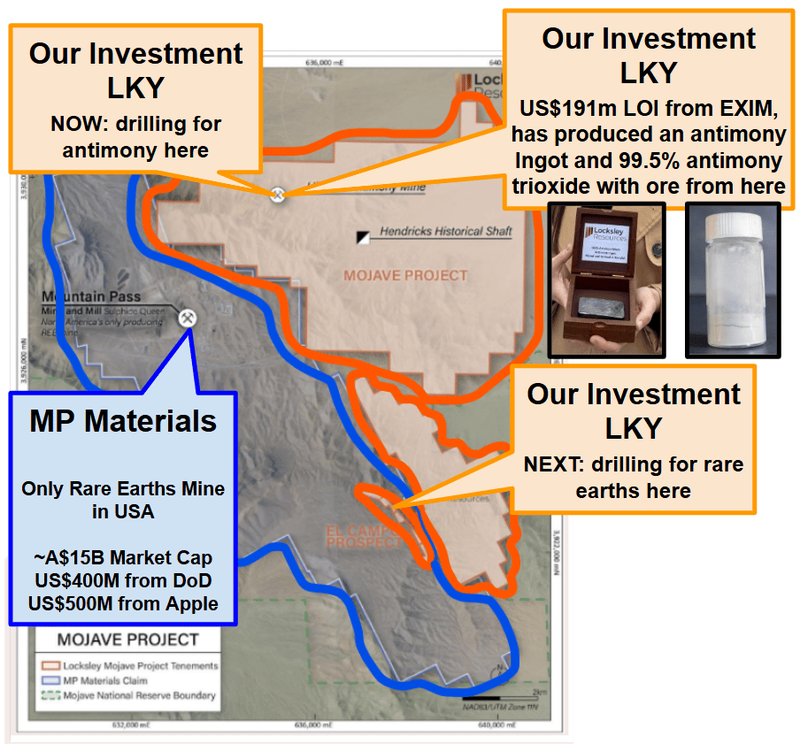

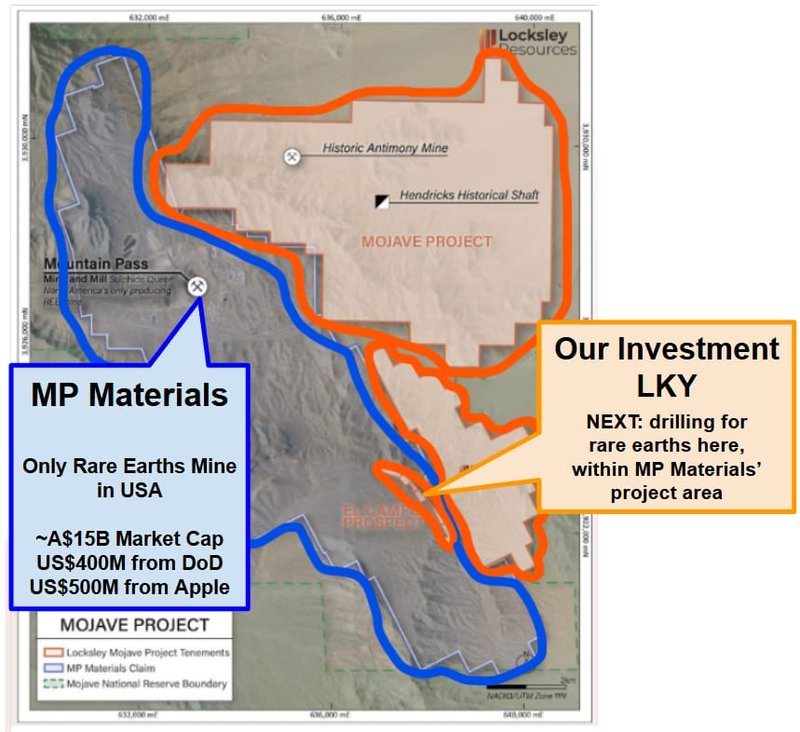

Our Investment Locksley Resources (ASX:LKY sits directly next door to the Pentagon’s first critical minerals Investment, MP Materials.

Two days ago:

The Pentagon was reported to be headhunting investment bankers from Goldman Sachs, Morgan Stanley, JPMorgan and Bank of America to build an “economic defense unit”....

To help deploy funds over three years into other projects to support the military. (source)

12 days before that:

The Pentagon was out soliciting a domestic supply of 13 specific critical minerals “from over 1,500 companies”. (source)

And on that same day:

The Defence Industrial Base Consortium (DIBC) opened up funding for projects (up to US$500M per proposal) that can produce critical minerals inside the US with a strict 20th of March deadline for proposals. (source)

That’s all inside the last few weeks...

There is also everything else that happened last year (deals by JP Morgan, Apple... the list goes on).

LKY has a previously producing antimony project that sits right next door to MP Materials, the first company to receive a big funding package from the US government (and Apple).

(LKY also owns that block inside MP Material’s project area - prospective for rare earths).

LKY is working to get its multi-level, historically producing antimony mine back into production (more on this in a second).

(Including drilling to find more antimony right now, so assay results could be announced any day)

LKY was also one of the first on the ASX to really start positioning its project as a potential source for critical minerals supply - in California on the Nevada border.

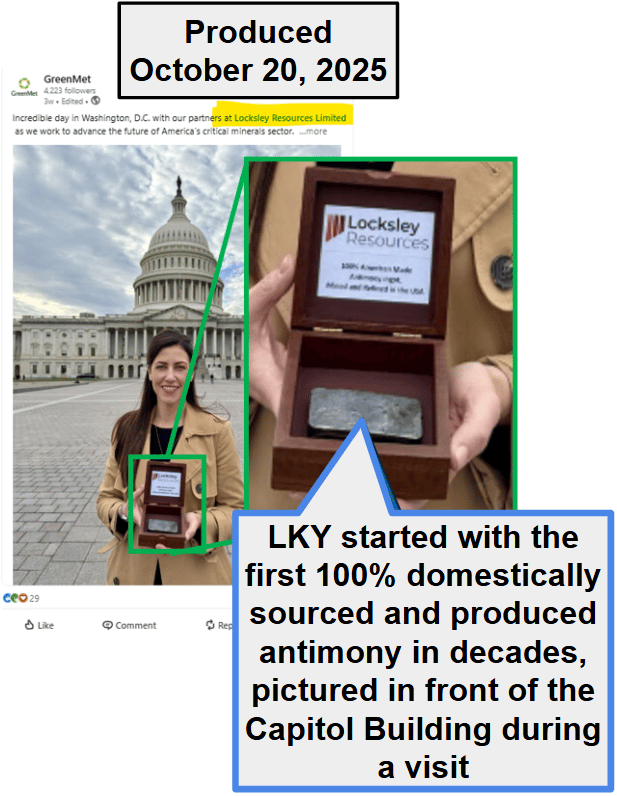

Five months ago, LKY produced the first US-sourced, US-processed antimony ingot in decades.

(source)

BUT...

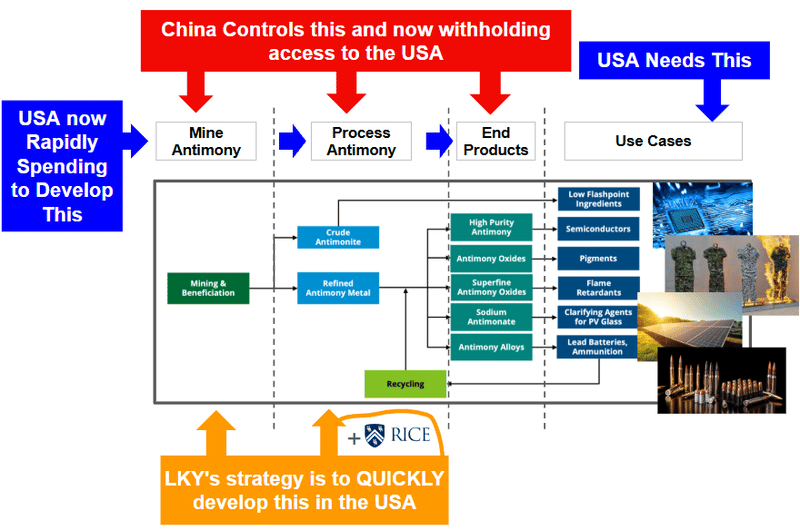

It’s not just the SUPPLY of raw critical military metals that China dominates.

China also dominates the complex PROCESSING of the raw materials into the final form needed by the military.

(~80% of all processed antimony comes from China) (source)

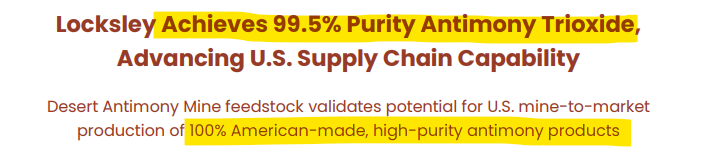

Yesterday, LKY announced it had successfully processed its raw antimony into a 99.5% purity antimony trioxide product at bench scale:

(source)

100% USA sourced and made antimony trioxide:

Antimony ore is one thing - but really it's the high purity antimony trioxide that is the critical input for military applications - stuff like munitions primers, military electronics and flame retardant systems.

Clearly not ideal for the USA if their key adversary China dominates ~80% of antimony processing (source).

Why Antimony Trioxide Matters to the Pentagon and US Department of War:

- Bullets and armor-piercing rounds - hardens lead and improves ballistic performance

- Primers and detonators - key precursor for munitions ignition systems

- Flame retardancy - the #1 synergist, found in 72% of US military equipment with no viable substitute

- Nuclear weapons - critical input in production

- Night vision and infrared - enables thermal imaging, missile tracking, and precision-guided weapons

- Military batteries - powers submarines, radar, and battlefield vehicles

- Defense electronics - used in electronic warfare and missile sensors by Lockheed, Northrop, and Raytheon

- Supply crisis - US imports ~90% of its antimony, while China has cut exports by 97%

- Pentagon response - ~$1B deployed to secure domestic supply, the largest mineral stockpile effort since the Cold War.

The bench scale 99.5% purity Antimony Trioxide sample LKY has just produced can be used for qualification with strategic offtake partners, metals traders and government supply chain participants.

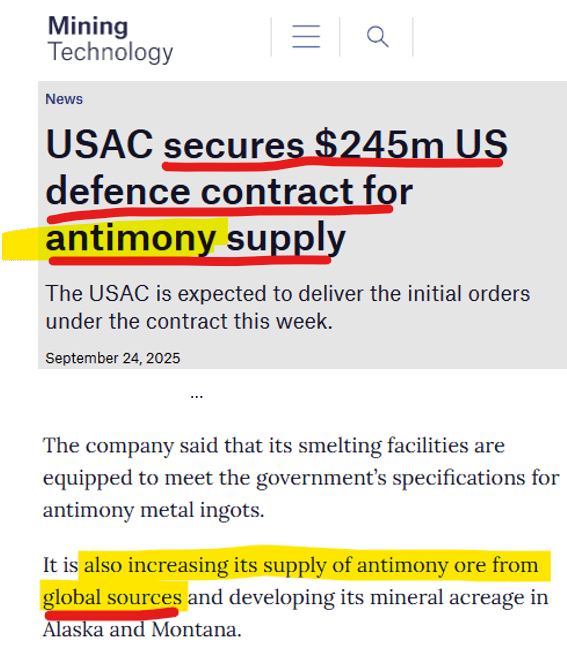

As far as we know, the only other company to produce an antimony ingot and antimony trioxide inside the US is A$2BN US Antimony Corp (USAC). (source)

And subsequently secured a US$245M US government contract for antimony supply...

(Even then, USAC are doing it with antimony feedstock sourced OUTSIDE of the US)

(source)

Antimony trioxide is the most commonly traded form of antimony, and as we flagged above, it's a critical input for defence technologies.

It's the precursor material for things like munitions primers, flame retardants for military vehicles/equipment, military electronics, and even nuclear weapons production.

(especially as a flame retardant, which are needed in a LOT of military equipment and uniforms to stop it catching fire, and there is no viable substitute for antimony trioxide)

All of these things that are likely to be in the forefront of the US government's mind right now with everything happening in the Middle East.

Antimony trioxide looks like it may have also been the motivating factor behind the US$27M the Pentagon INVESTED into USAC under the Defense Production Act Title III, too.

That announcement said specifically that the funding was to produce antimony for flame retardants, batteries, munitions, and other defence applications.

(source)

(remember early we flagged that a few days ago it was reported that the Pentagon is head hunting a team of investment bankers, likely to help do a lot more of these type of deals - read it here)

We think after yesterday’s LKY announcement of successful production of 99.5% antimony trioxide, LKY has thrown its hat in the ring as a potential solution for the Pentagon which looks like it is scrambling for supply from wherever it can find it right now.

And is also now a much stronger contender for any government funds willing to back companies who can provide that solution.

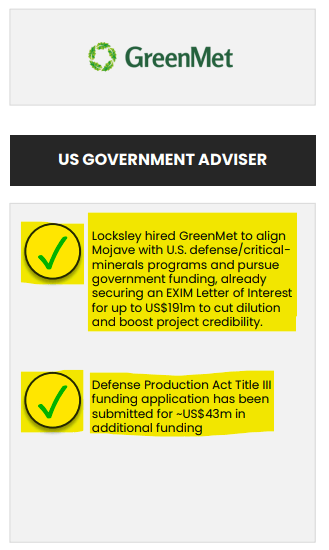

We note that LKY has an application in right now for US funding under the same US Defense Production Act Title III for US$43M.

(LKY is currently capped at A$76M)

(source)

We think any success in getting some sort of US funding deal could be big for LKY.

Especially considering LKY could be offering a solution for both sides of the supply chain issue - processing (from its US-located partnerships) and feedstock (from its project in California).

We think LKY’s “back to front” development plan for its Desert Antimony Mine in California is starting to look like the right way to go about it (even though it is unconventional for a mining company).

Late last year LKY raised $17M at 24c/share and ended last year with $19.47M in the bank.

LKY is currently trading below that capital raise price that brought in cornerstone US support to the company.

LKY has spent the last 6 months:

- Developing downstream processing tech to show it can produce a refined end product (LKY did this again yesterday). ✅

- Get funding support for a mine and processing restart (US$191 EXIM LOI already received, further funding applications currently in progress) 🔄

- Then do the drilling to prove scale. (drilling recently started) 🔄

Most mining companies do everything in reverse to LKY’s strategy - i.e. drill first, then figure out processing years later.

Instead LKY is working backwards to get its multi-level, historically producing antimony mine back into production.

Develop downstream processing tech > produce a downstream end product > get funding support for a restart > then do the drilling needed to prove scale for a final investment decision.

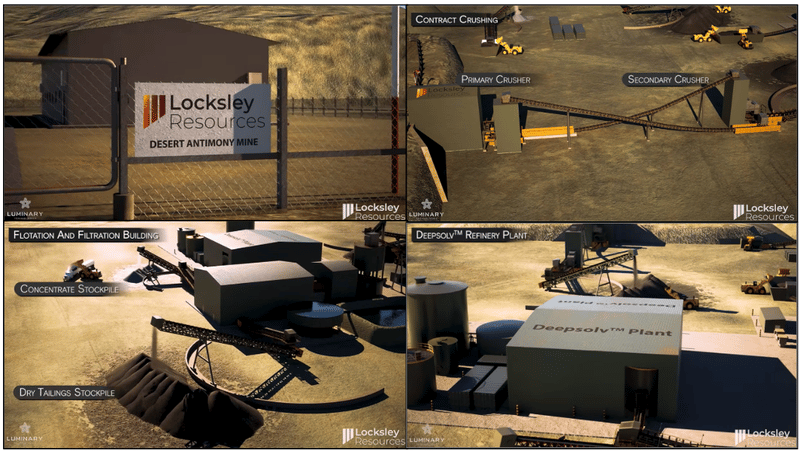

Plus LKY has already commenced the design and engineering works process with an expression of interest sent out to potential firms for a small-scale plant would look like when it's up and running - check out this video for that plan:

(a nice video to present to any potential financiers...)

Watch: LKY Desert Antimony Mine Restart Plan

Locksley Resources

Over the last few months, leading up to drilling LKY has:

- LKY Produced the first 100% US-sourced and refined antimony ingot in decades (October 2025)

- Has a US$191M Letter of Interest from US EXIM Bank for project financing (November 2025)

- Applied for US$43M in grant funding under the Defence Production Act Title III (December 2025)

- High grade batch sampling results averaging 18.7% antimony across 287kg of samples (with individual batches hitting 25.7% Sb).

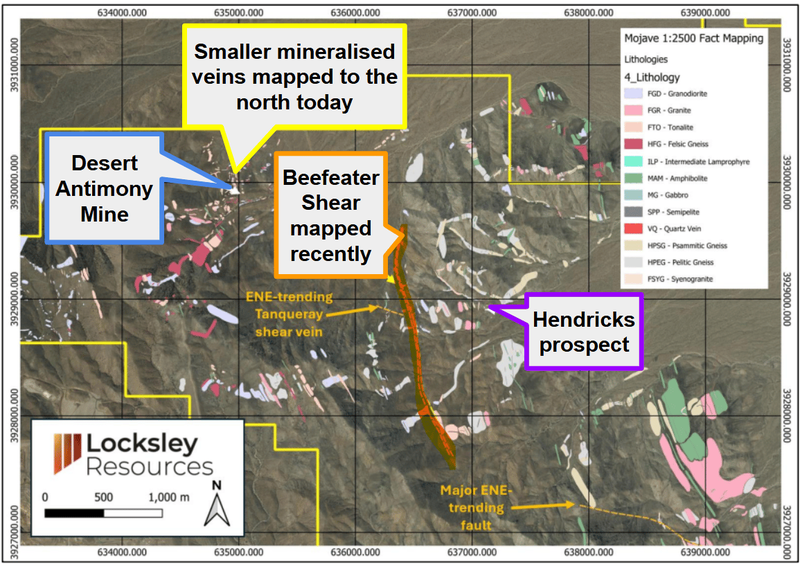

- Mapping of potential extensions to the old Desert Antimony Mine ~60m to the north-east.

- Mapping of a new target area (a potential DAM repeat?) - the "Beefeater Shear" a 10-15 metre wide structure that could significantly expand the project.

- Starting engineering partner selection for the pilot processing plant design.

- Product qualification work - the precursor to discussions with potential customers/offtakers.

- LKY produced 99.5% purity antimony trioxide - meeting the key threshold for defence qualification (Yesterday - March 2026)

(source)

What we don't know at the moment is the scale potential of LKY’s assets.

Well we sort of do... LKY’s project does have an exploration target of 772K-1.38M tonnes at 2.5-4.9% antimony for ~19,400 tonnes to 67,700 tonnes of antimony metal. (source)

We covered the exploration target in detail here: LKY: Just raised $17M, now backed by US institutions - first antimony producer in the USA?

Now that drilling has started it's about how much of that exploration target is still actually where LKY thinks it is.

We are hoping this next round of drilling answers those questions.

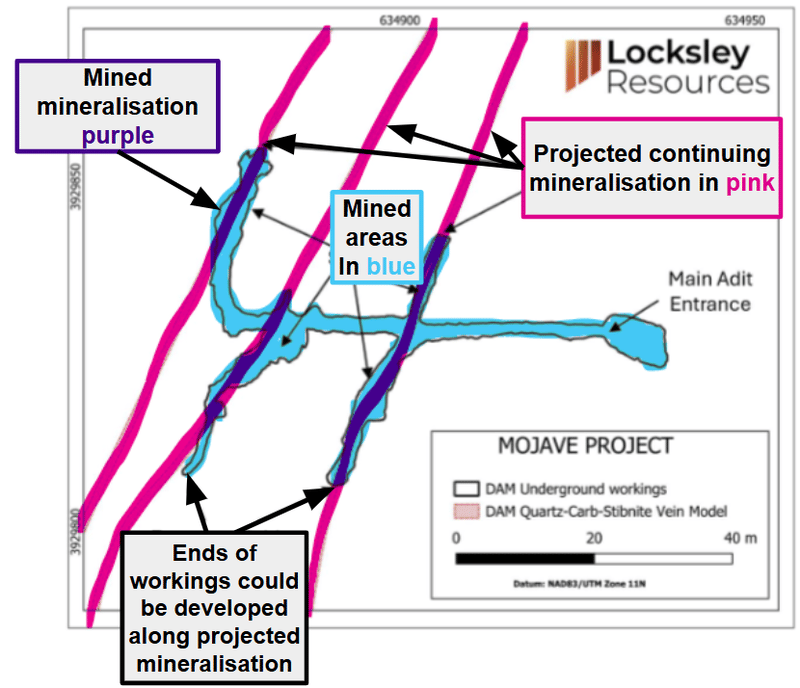

Here was our working theory based on all of the mapping/sampling/surveys LKY had done to date:

(source)

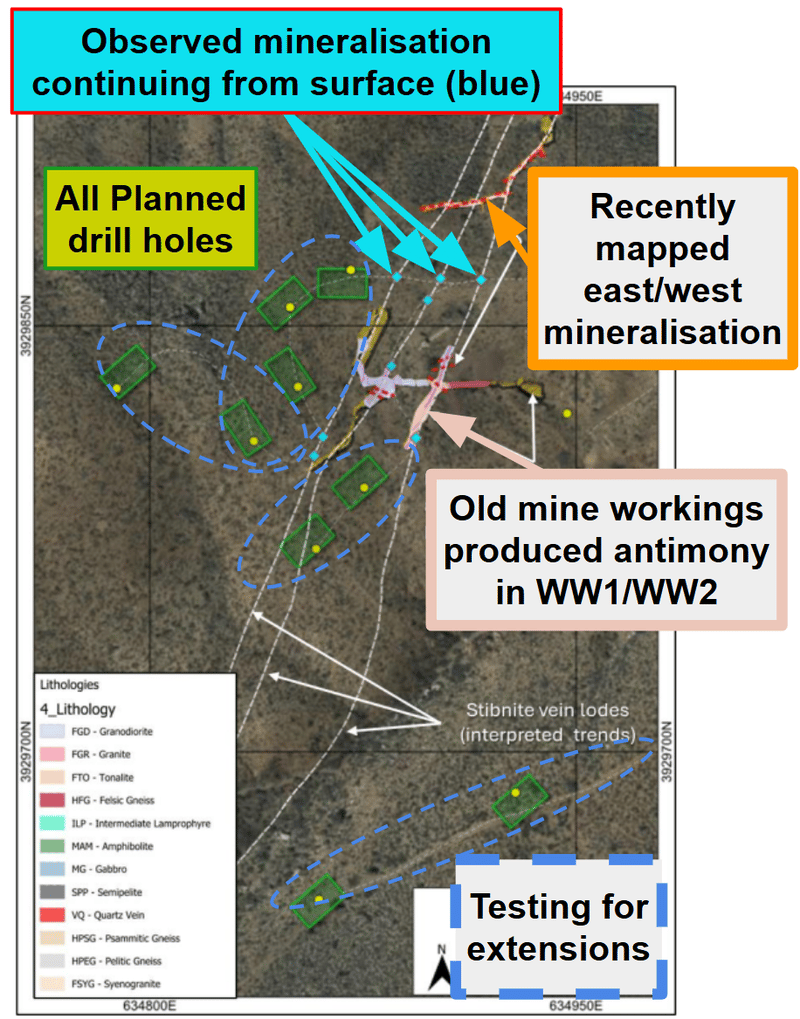

And here is where LKY will be targeting with its first batch of holes:

(source)

We note the holes are all extensional to the old workings - so we should get a fairly good sense of how much bigger LKY can make that old mine.

Now we wait to see if drilling results deliver big extensions (or repeats) to the old workings.

Drilling results to bring in corporate/government interest to LKY?

We think corporates (companies) and the US government will be watching LKY’s drilling program.

As mentioned earlier LKY’s already got potential support from the US Export Import Bank. (source)

We think that any other potential financier for LKY’s project will be watching to see the outcome of the drill program.

We also think US corporates who are looking for antimony feedstock may all of a sudden look at LKY as a potential supply source.

(Especially now that LKY’s shown its ore can be processed into a trioxide and an ingot)

Assuming the drilling results come in, which they may not - exploration drilling carries risk of failure.

There’s also no guarantee that LKY will be able to secure any kind of corporate or government funding.

In a previous note, we wrote about potential interest from US Antimony Corp:

- The Pentagon set aside US$245M to buy antimony from US Antimony Corp, and

- US Antimony Corp immediately went out looking for assets to backfill that (and potential future demand) by buying ASX listed Larvotto.

That takeover bid was rejected, but it shows how “motivated” US Antimony Corp is to secure “friendly” antimony feedstock to fulfil their Pentagon contract.

Now here's why we think LKY could be of interest.

LKY already has one of the highest grade known occurrences of antimony in the USA.

LKY has already proven its Mojave Project can produce high-grade antimony concentrates at 68.1% antimony.

(remember that photo above of LKY’s CEO holding the antimony ingot at the White House)

LKY has already proven that those concentrates can be turned into antimony ingots suitable for US military specifications.

And then yesterday, LKY proved it can be turned into antimony trioxides too.

LKY has already received potential funding support from the US Export Import Bank (up to US$191M).

Whilst it's early days in LKY determining how much antimony it can mine, surely now, LKY's domestic USA project is in the conversation as a potential feedstock option for anyone looking for locally-produced antimony concentrates.

At the same time this is an early stage story and there’s no guarantee that everything will fall into place here.

LKY is also working on critical minerals processing tech

LKY also has a processing “X factor”.

LKY is working on processing tech with three different partners - Rice University, Hazen Research and Columbia University.

Aside from digging up rocks, processing the minerals is also something the US market is thinking about deeply.

In fact the principal barrier for a US domestic antimony mining industry is not necessarily ore availability but a lack of US processing and refining capability.

(this is yet another critical area where China currently has almost total dominance)

We listened to an All-in podcast episode a few months ago where the whole topic of why the US stopped processing things like rare earths was discussed. (Listen to that here ~33:16)

The main discussion point was about the potential environmental shortfalls and how it was just too hard for the US to even try to solve those problems.

LKY is trying to solve that environmental problem, especially with respect to antimony.

LKY is working on tech with Rice University using Deep Eutectic Solvents (green, biodegradable, non-toxic solvents) to process its antimony concentrates and turn them into a final product.

LKY could potentially have this tech developed with Rice, that is not only applicable to its own project but also other antimony projects across the US (which would be valuable on its own).

NEXT, LKY is currently supplying flotation concentrates and Run of Mine (ROM) ore from the Desert Antimony Mine to Rice University to advance the DeepSolv (DES) program.

This collaboration has already established preliminary process parameters for a green hydrometallurgical extraction process.

So this is now being used to initiate the design and scoping of a pilot demonstration plant for 100% US based antimony production.

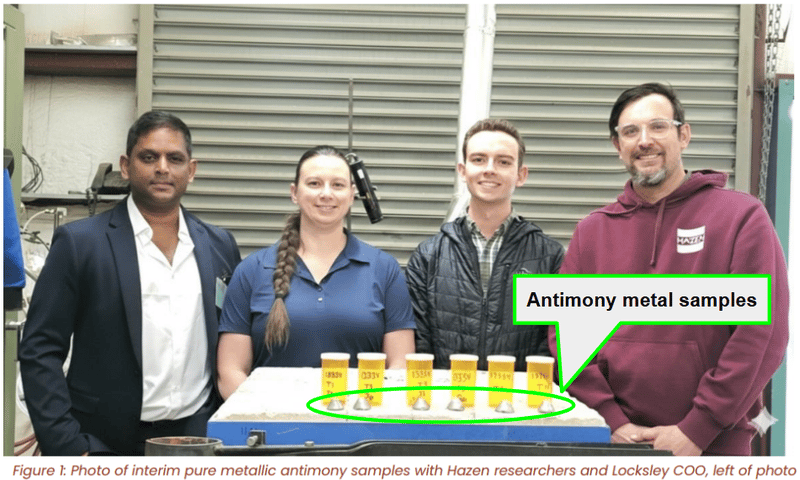

With Hazen Research - LKY has successfully produced metallic antimony ingots with a purity exceeding 99% (measured via XRD analysis).

AND NEXT LKY is testing its ore to produce Antimony Trisulphide for customer qualification.

Yesterday’s news means LKY has achieved a major milestone by producing 99.5% purity antimony trioxide - meeting a key threshold for entry into US defense and industrial qualification.

Here is a picture of LKY’s COO Danny George on the left at Hazen with some of the antimony metal samples produced:

(source)

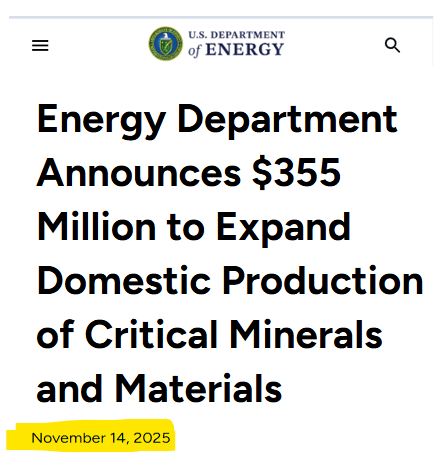

Another reason processing matters is because a lot of that capital we wrote about earlier is also going into processing technologies.

As mentioned earlier, processing of all critical minerals is done almost exclusively offshore (and in China)... which is why the US is now ready to try and reshore it with funding support.

(for antimony - China, Russia, Tajikistan control ~87.5% of mined product source and China alone ~80% of refinement (source)

Like the US$355M that has been allocated by the US Department of Energy with the goal to “expand domestic production of critical minerals”:

(source)

We are hoping either the processing or the mine restart strategy leads to LKY getting government funding and achieving our Big Bet which is as follows:

(of course this may never happen, this is our aspirational goal for LKY - there is no guarantee the company ever receives any US government funding).

Our LKY Big Bet

“LKY to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our LKY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for LKY?

Drilling at historical mine for antimony

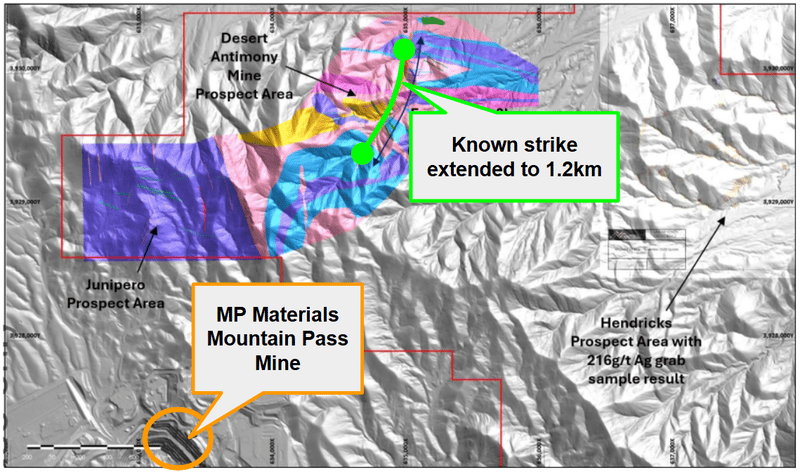

LKY has recently started drilling at the Desert Antimony Mine (DAM). (source)

LKY will be targeting to confirm extensions to the known antimony mineralisation to the north and south plus test for any east-west shear zones.

We are especially looking forward to seeing if LKY can prove whether or not its Desert Antimony Mine extends over the entire 1.2km of strike mapped earlier in the year.

(Source)

Drilling at rare earths at El Campo target

Following the drilling for antimony, LKY will move to its rare earths targets (that sit within MP Material’s ground package).

There, LKY will be testing areas where previous rock chip sampling returned grades as high as ~6.87% TREO (rare earths) - here is where those targets sit.

(source)

Updates on LKY’s processing tech partnerships

Now LKY has signed partnership agreements with Rice University, Columbia University and Hazen Research.

Broadly, we want to see LKY progress the following across the three partnerships:

- Pilot plant design and metallurgical test work (Hazen and Rice)

- Production of representative samples for US industrial and defence qualification (Hazen)

- Commercial analysis and process optimisation (Hazen and Rice)

- Rare earth processing tech development (being done with Columbia University)

As we have said a few times in this note already, LKY has produced a 100% American sourced and made antimony ingot in October last year (source) and has now produced a 99.5% pure antimony trioxide (source). So LKY is now taking this product for qualification from potential offtake partners, metals traders and government supply chain participants.

So we could see updates on both improvements to the processing of these antimony products or updates with potential future customers which may come with funding opportunities.

US government funding decisions

LKY has a US$191M LOI from US EXIM and a US$43M US Defense Production Act Title III application pending. (source)

With the Pentagon actively deploying capital into antimony projects right now, we think LKY could be in conversation the next time expressions of interest go out.

What could go wrong?

LKY has now started drilling, so the main risk in the short term is around “Exploration / Drilling Risk”.

LKY has conducted sampling and mapping at and near the historic mine which appears to show extensions to the antimony mineralisation.

If LKY is not able to prove that the mineralisation continues and/or that it is of uneconomical grade/tonnage, then it could have a negative impact on the share price.

Exploration / Drilling risk

There is no guarantee that LKY’s extensional drilling programs at the historic mine and on the sampled areas which indicate that mineralisation continues will be successful resulting in LKY failing to uncover enough economic mineralisation.

Source: “What could go wrong” - LKY Investment Memo 01-Aug-2025

LKY’s valuation is also where it is today because of the interest in US critical minerals stocks, so there is also “Market Risk”.

Any drops in market sentiment toward the macro thematic could impact LKY’s valuation negatively.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking LKY’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Source: “What could go wrong” - LKY Investment Memo 01-Aug-2025

Other risks

Like any small cap exploration company, LKY carries significant risk, here we aim to identify a few more risks.

The company has just commenced its first drilling program at its Desert Antimony Mine.

There is no guarantee that drilling will replicate the high grades seen in recent sampling or define a resource with sufficient scale to justify a commercial mining operation. If drill results are underwhelming or fail to prove extensions to the historic mine, the market could re-rate the stock lower.

LKY is relying on developing novel processing technology (Deep Eutectic Solvents) in partnership with universities to process its antimony in an environmentally friendly way.

There is a risk that this technology does not work effectively at a commercial scale, or that the costs to implement it are prohibitive, potentially leaving the company without a viable, environmentally friendly processing pathway.

While LKY has applied for substantial US government funding (US Ex-Im Bank, Defence Production Act Title III), there is no guarantee these applications will be successful.

If LKY fails to secure these non-dilutive grants, it may need to fund development through equity raises, which could result in significant dilution for existing shareholders.

The project is located in California, a jurisdiction known for strict environmental regulations. Even though the Desert Antimony Mine is a historic site, restarting mining operations and permitting a new processing facility could face significant regulatory hurdles, delays, or opposition.

Finally, LKY’s valuation is currently benefiting from the strong "US critical minerals" macro theme and high antimony prices due to geopolitical tensions. If US government policy shifts, or if supply chains normalise and antimony prices fall, the strategic premium currently attached to LKY’s assets could diminish.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LKY Investment Memo

You can read our LKY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LKY Investment Memo covers:

- What does LKY do?

- The macro theme for LKY

- Our LKY Big Bet

- What we want to see LKY achieve

- Why we are Invested in LKY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.