LKY: Just raised $17M, now backed by US institutions - first antimony producer in the USA?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,890,278 LKY Shares at the time of publishing this article. The Company has been engaged by LKY to share our commentary on the progress of our Investment in LKY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

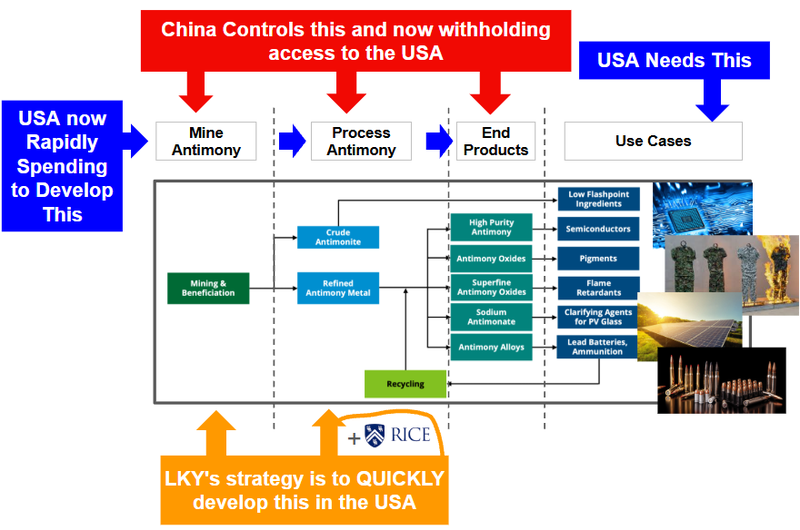

Our Investment Locksley Resources (🇦🇺 ASX:LKY | 🇺🇸 OTC: LKYRF) is executing a plan to rapidly become the first domestic supplier of the critical mineral antimony in the USA.

(and is concurrently about to drill rare earths targets INSIDE the ground held by the only rare earths mine in the USA)

The US is racing to find, secure and stockpile domestic sources of critical minerals like rare earths and antimony.

These minerals are critical to defence, AI, robotics, advanced weapons systems and technologies that will determine the winner of the race to be the next global super power.

(China has nearly all the supply of these minerals, the USA has almost none - and the USA is now rushing to fix that)

The window is now open for companies to move fast, and that is what LKY has been doing over the last 6 months.

LKY is taking advantage of the current window of urgent US market need, zero domestic US antimony supply, increased investor interest and available US government funding.

And it looks like LKY’s momentum will keep accelerating into 2026.

LKY just raised $17M in an “oversubscribed” placement “cornerstoned by well established U.S. institutional investors”. (source)

(we also put money into this placement)

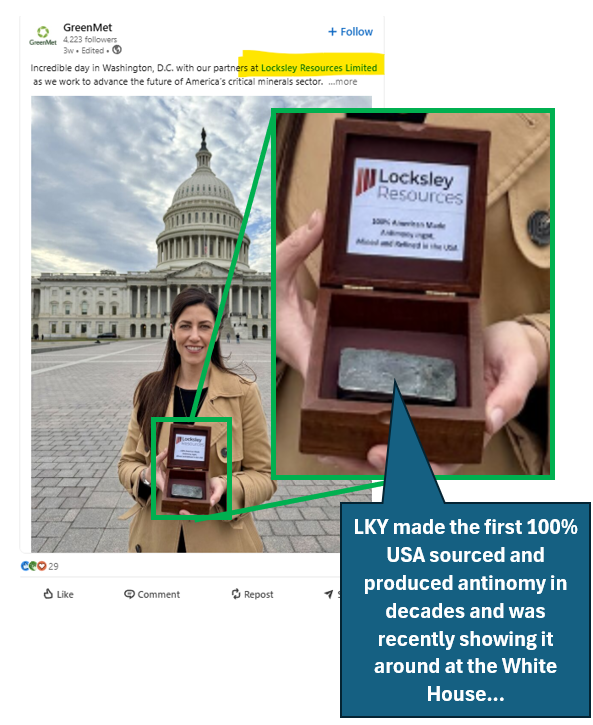

In just 6 months, LKY is working on antimony processing tech with Rice University AND produced the first 100% US-sourced antimony ingot in decades (more on this shortly).

(source)

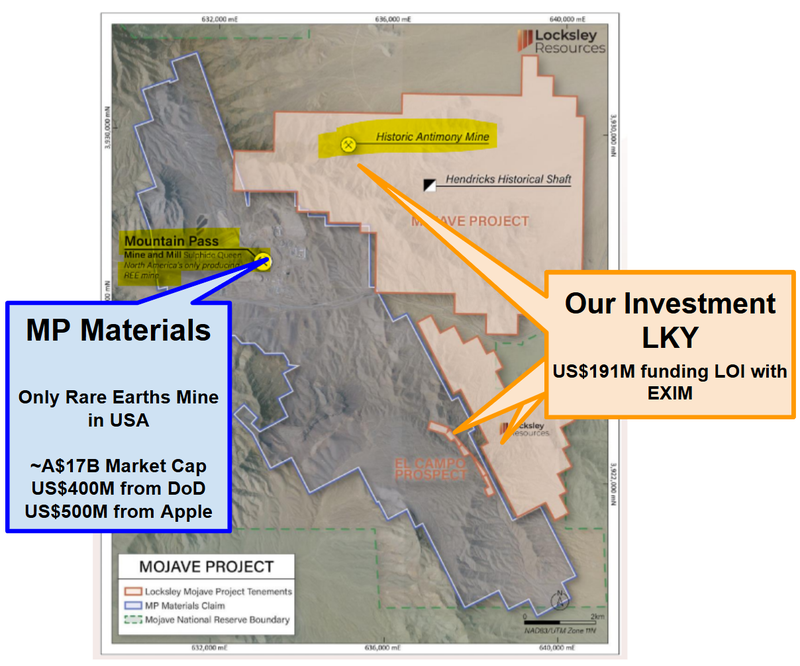

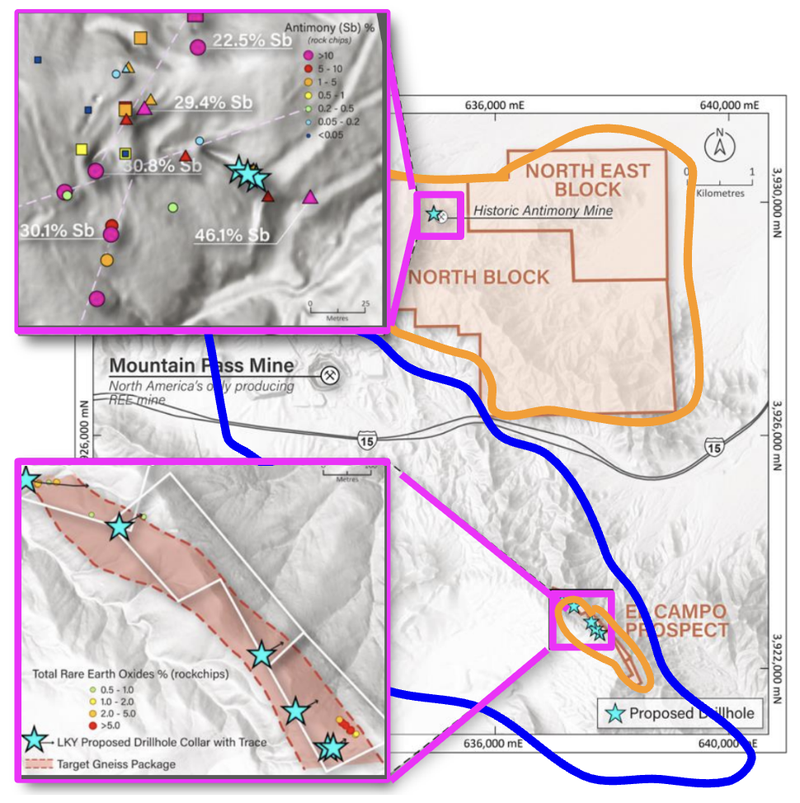

LKY’s project sits in a highly strategic critical minerals corridor in the USA - Mountain Pass, California.

(We travelled to visit LKY's project a few months ago to see it with our own eyes - read our site visit note here)

LKY has ground directly next door to (and even inside of) the $16.6BN capped MP Materials, the only rare earths miner (and aspiring rare earths magnet producer) in the US.

(MP is backed by the US Department of War and Apple via large financing packages.)

(Source)

LKY’s rare earth targets (El Campo prospect) are literally INSIDE MP Materials' land area.

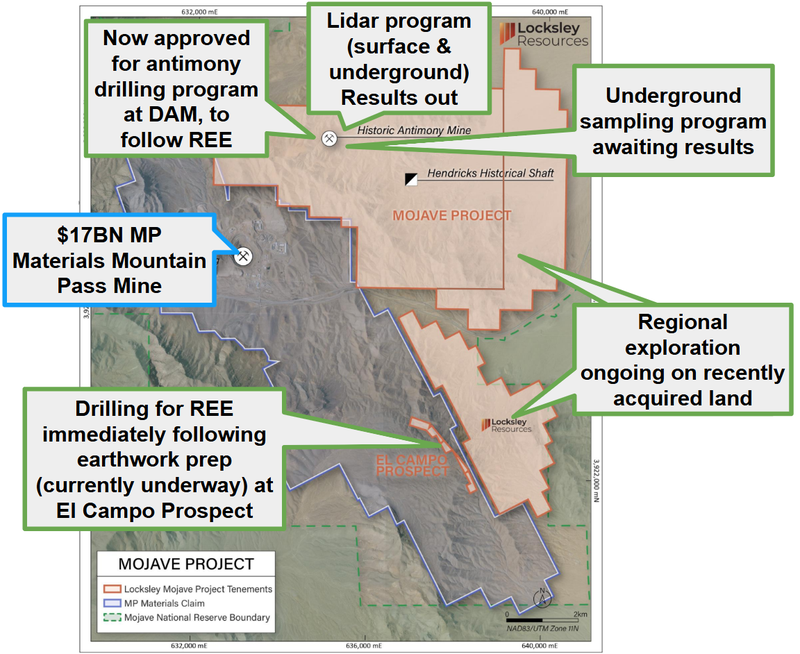

Two weeks ago, LKY started ground operations ahead of drilling this rare earths target. (source)

(any big rare earth hits announced by LKY in the coming weeks would be a nice bonus to the antimony story)

Once the rare earths drilling is finished, drilling will move directly to LKY’s antimony project to the north.

So LKY has back to back drill programs about to start in the coming weeks.

Results from the drilling are expected in Q1-Q2 2026.

LKY fast track “mine to market” plan is to get product to the market as fast as possible...

Again, LKY is taking advantage of the current window of urgent US market need, zero domestic US antimony supply, increased investor interest and available US government funding.

(fast tracked production as opposed to the usual 7 to 10 year traditional mine build that doesn't cut it for this situation)

LKY is currently working on processing tech with Rice University and has already produced the first US sourced, US refined antimony brick in decades.

LKY has been one of the faster movers in 2025.

So with a fresh $17M in the bank to keep up this momentum AND two drill programs back to back - LKY is going to be delivering lots of news in the next 90 days...

Check out this recent ~3 minute video for a concise summary of what LKY is doing.

Following the $17M capital raise announced this morning, LKY will be hosting a webinar on its “US Development Progression and Execution Strategy” on December 9th at 1:00pm AEDT / 10:00am AWST.

Click here to register for the webinar

We are Invested in LKY as we think US critical minerals could end up a bigger macro investment thematic than the battery minerals boom of 2020-2021.

Battery minerals are important for emissions reductions.

Critical minerals are important for national security and international competitiveness.

(with security at stake, governments and countries are more motivated to win this race)

Whoever has local supply chains, mineral supply and manufacturing capability to mass produce the biggest and best autonomous robot army, best AI, best advanced technologies and military weapons will win the race to be the next global super power.

The US government recognises this AND their current lack of domestic critical mineral supply - so has started making direct equity investments in critical minerals stocks.

(and it seems like they are just getting started)

(Source)

The biggest bank in the USA, JP Morgan, has also made a US$1.5 trillion commitment to invest in industries in the US national interest (including critical minerals).

The first asset JP Morgan backed was an antimony project in the US.

We think we are still very early into this macro thematic.

We first Invested in LKY at 9.5c, and again in the US led, “oversubscribed” placement announced today at 24c.

We are backing LKY because we think the company is applying the right strategy to capture US government and market attention.

LKY is going for speed to market...

(and clearly its working - today’s $17M raise was “oversubscribed” and “cornerstoned by well established U.S. institutional investors”)

Usually, resource exploration companies will focus on drilling first, then feasibility studies and then development.

LKY worked backwards, and has already shown:

- It can produce a downstream antimony product that is military spec.

- That its project can be re-developed and put back into production.

- Which was enough to receive a US$191M Letter of Interest from the US Export Import Bank to finance the re-development of its project.

(Source)

And now LKY has begun drilling operations on site, with back to back drilling programmes to occur over the coming months.

We are hoping that with some strong drill results, LKY will have what it needs to be able to secure big non-dilutive funding deals.

Similar to the US$245M deal US listed antimony refiner US Antimony Corp did with the Pentagon. (source)

Or like the deals signed for other pre-production assets - like JP Morgan’s US$75M equity investment into Perpetua Resources. (source)

That Pentagon contract for US Antimony Corp was what re-rated the stock to a market cap above US$3BN.

We are hoping IF LKY can secure a big financing deal, we could see a significant re-rate in LKY.

Of course like anything in life, there are no guarantees of this happening. This is ASX small cap investing - anything can happen. At this end of the market, only invest what you can afford to lose.

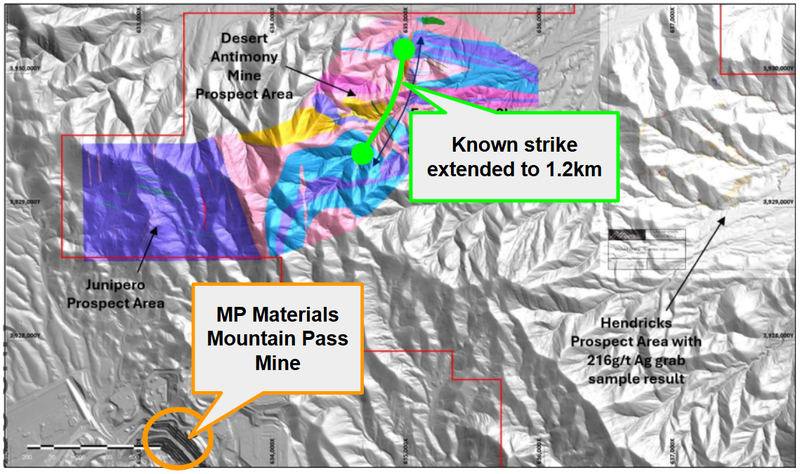

LKY holds ground next to USA’s only rare earths mine, owned by US “national champion” - MP Materials.

(Source)

LKY has ground next door to MP (and inside of its ground) that are prospective for rare earths and antimony.

LKY will be drilling for both over the next couple of months. (source)

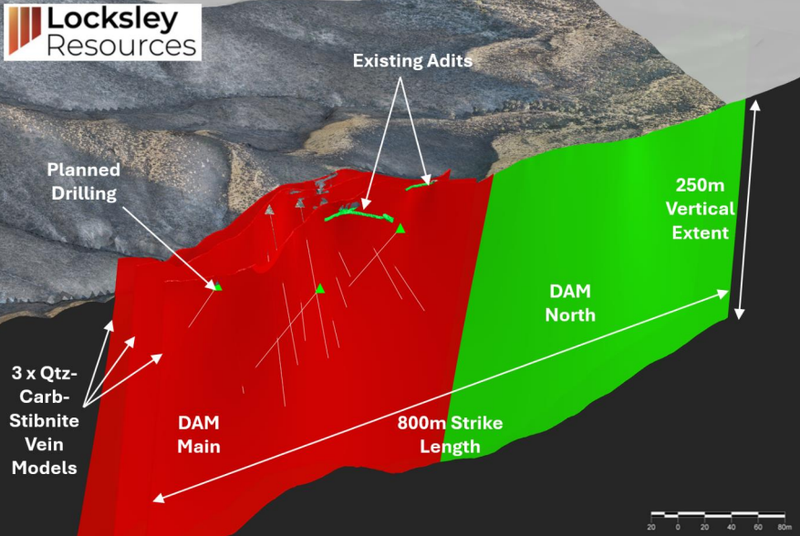

More on LKY’s historic antimony mine - can it be re-started?

LKY’s Desert Antimony Mine was in production during WW1 and WW2 producing between 100 and 1,000 tonnes of antimony. (source).

It was one of the highest grade antimony mines in the US.

High enough grade to warrant the old timers to mine over four underground levels...

So far, for the Desert Antimony Mine, LKY has:

- An exploration target: 772K–1.38M tonnes at 2.5–4.9% Sb for ~19,400 tonnes to 67,700 tonnes of antimony metal.

- US$191M in potential financing lined up from the US Export Import Bank (EXIM).

- Development planning for extraction, permitting and financing underway.

- Letters of interest sent to engineering contractors for a possible mine re-start scenario.

- Safe underground access confirmed with an engineering consultant sign off.

- High-grade antimony samples extracted and tested successfully - producing military spec ingots from bulk samples...

Here is a picture of that glorious antimony ingot - the first US sourced, US refined antimony ingot produced in decades:

(source)

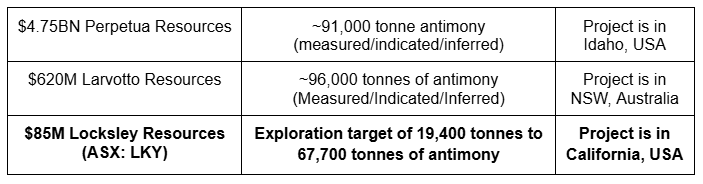

LKY’s exploration target is approaching a level comparable with the resource estimates of two of the most popular antimony stocks.

The USA antimony national champion, the $4.75BN capped Perpetua Resources, has a ~91,000 tonne antimony resource estimate. (source)

And ASX first mover, the $620M capped Larvotto Resources, plans to produce ~39,000 tonnes of antimony over an 8-year mine life from its construction stage project in Australia. (source)

Here is how the three stack up in terms of overall resources/exploration targets:

At this stage, LKY’s exploration target is conceptual - there is no guarantee drilling will deliver a resource inside that target range.

IF drilling does come in then LKY’s number could of course get bigger... or get smaller if the first round of drilling is not successful.

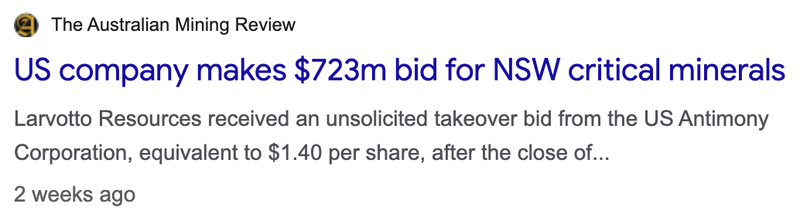

Our view is that as LKY’s project gets closer toward development it could potentially become a target for someone looking for US based antimony feedstock.

Someone like a $1.35BN US Antimony Corp.

US Antimony Corp recently received a big purchase order from the Pentagon for US$245M.

Then it started scrambling, trying to buy a company that is the closest to production to try and backfill feedstock into their refineries...

(Source)

USAC came for ASX listed Larvotto Resources with an offer of A$723M... which Lavrotto rejected.

(Source)

So US Antimony Corp hasn’t really found that feedstock they will need to deliver those Pentagon contracts... yet.

LKY’s project is inside US borders and has shown its ore can be processed into antimony ingots suitable for US military specifications.

US Antimony Corp has every incentive to move as quickly as possible to show it can deliver on its Pentagon deal.

The initial purchase order accounts for only ~1/8th of annual demand in the US.

(Source)

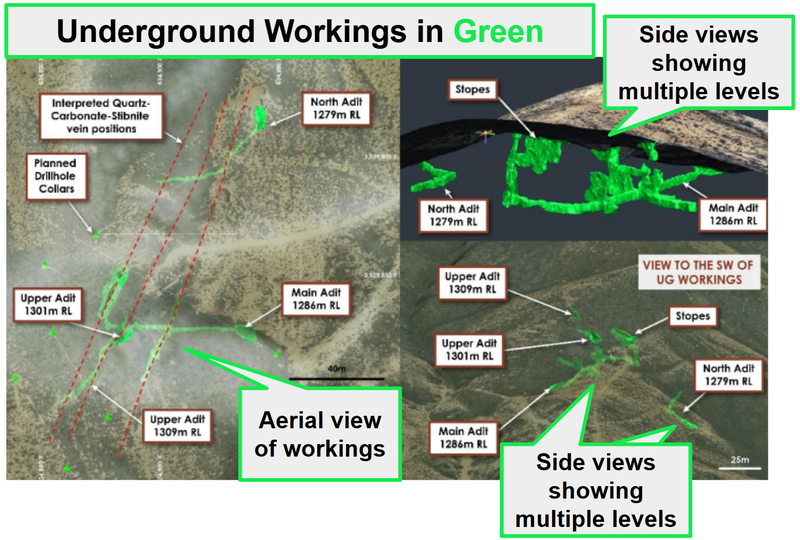

LKY ‘going for speed’ might also help from making it an attractive M&A target too (not just in terms of landing non-dilutive funding).

Especially those recent announcements showing 3D maps of the existing underground workings and how a development scenario would look for the project:

(Source)

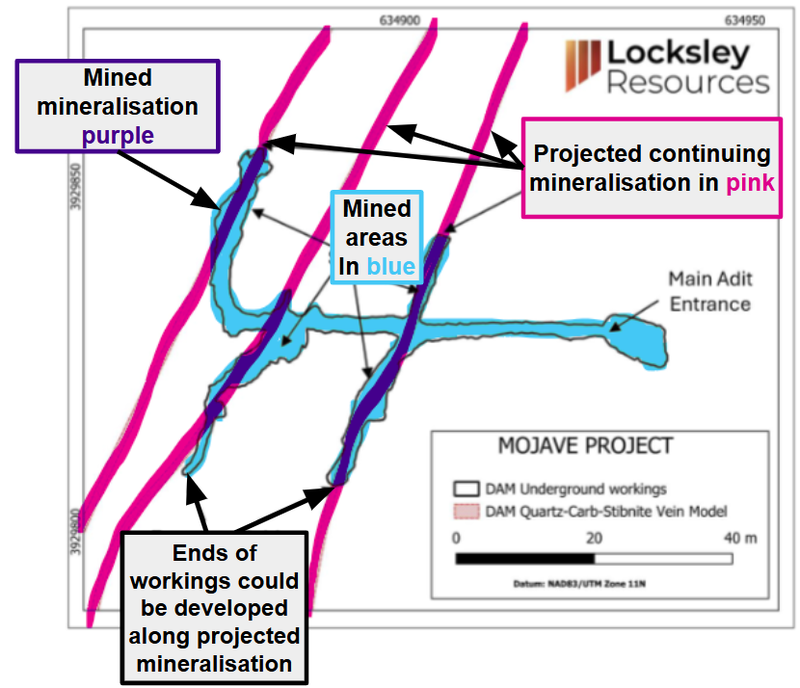

And here is how LKY was able to extrapolate where the previously mined veins could extend:

(Source)

LKY is also a processing tech option...

LKY also has a processing “X factor” too.

LKY is working on processing tech via three different avenues, with Rice University, Hazen Research and Columbia University.

Aside from digging up rocks, processing minerals is also something the US market is thinking about deeply.

We listened to a recent All-in podcast episode where the whole topic of why the US stopped processing things like rare earths was discussed.

The main discussion point was about the potential environmental shortfalls and how it was just too hard for the US to even try to solve those problems.

(Listen to that part starting at ~33:16 here)

LKY is trying to solve that environmental problem, especially with respect to antimony...

LKY is working on tech with Rice University using Deep Eutectic Solvents (green, bio-degradable, non-toxic solvents) to process its antimony concentrates and turn them into a final product.

LKY could potentially have this tech developed with Rice, that is not only applicable to its own project but also other antimony projects across the US (which would be valuable on its own).

NEXT, LKY will start testing ore samples from its own Desert Antimony Mine to form the basis for the design of a pilot plant.

LKY is also working on two other processing technologies:

- Antimony processing tech with Hazen research. Hazen were the group who helped LKY produce that 100% US sourced and refined antimony ingot.

- Rare earth processing tech with Columbia University.

Between the three partners, LKY is working on:

- Pilot plant design and metallurgical test work

- Production of representative samples for US industrial and defence qualification

- Commercial analysis and process optimisation

Four catalysts we could see from LKY over the next 3-6 months

Now, with $17M cash raised, here are the four share price catalysts that we think could trigger a re-rate higher in LKY’s share price:

- A surprise funding announcement for non-dilutive funding to advance exploration or its downstream business

- Antimony drilling results that show the potential for an economic antimony mining operation.

- A rare earths discovery right next door to (or inside of) MP Materials’ ground, the only rare earths mine in America.

- A tech breakthrough with Rice University to develop US-based, environmentally friendly antimony processing tech.

No guarantees of course, this is speculative small cap investing.

Ultimately, our Big Bet for LKY is as follows:

Our LKY Big Bet

“LKY to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our LKY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for LKY?

Drilling (this quarter) 🔄

LKY expects drilling to start this month. (Source)

With the antimony drill program, LKY plans to test for the extent of mineralisation near and extending out from the historical antimony mine, testing along the recently seen antimony workings from the LiDAR program results showing the existing adits.

(Source)

With the rare earths drill program, LKY plans to test areas where a number of high grade rock chip samples were found, grading 1.20% to 6.87% TREO (rare earths).

Here is where LKY’s initial drilling program is scheduled from a broader view released earlier in the year (antimony in top section, rare earths in the lower):

(Source)

We are especially looking forward to seeing if LKY can prove whether or not its Desert Antimony Mine extends over the entire 1.2km of strike mapped earlier in the year...

(Source)

Secure licence agreement with Rice University and production MOU with Hazen 🔄

LKY has a partnership agreement with Rice University. The next stage will be to secure a larger licence deal over whatever technology is developed from the R&D agreement.

This will take some time to work out given the IP sharing and mutual development of the technology.

With Hazen (a leading metallurgical company), LKY recently signed a MOU to develop for processing of its antimony ore.

Between the two partners, LKY is working on:

- Pilot plant design and metallurgical test work

- Production of representative samples for US industrial and defence qualification

- Commercial analysis and process optimisation

What are the risks?

LKY hasn’t started drilling yet so the main risk in the short term is around “market risk”.

LKY’s valuation is where it is today because of the interest in US critical minerals stocks.

Any drops in market sentiment toward the macro thematic could impact LKY’s valuation negatively.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking LKY’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Source: “What could go wrong” - LKY Investment Memo 01-Aug-2025

For the full set of risks we have identified and accepted in making our Investment in LKY, see our LKY Investment Memo below.

Other Risks

The company's primary asset is a pre-discovery antimony and rare earth elements exploration project in California, and it is possible that LKY makes no economic discovery despite the proximity to the producing Mountain Pass mine.

LKY is highly sensitive to fluctuations in antimony and rare earth element prices.

While current geopolitical tensions have supported these prices, any easing of US-China trade restrictions or alternative supply sources could materially impact the project's economic viability and the market’s interest in exploring the project.

Finally, despite high-grade surface samples (up to 12.1% TREO and 46% antimony), these results may not be representative of broader mineralisation at depth, and the company has yet to conduct any drilling to verify continuity.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LKY Investment Memo

You can read our LKY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LKY Investment Memo covers:

- What does LKY do?

- The macro theme for LKY

- Our LKY Big Bet

- What we want to see LKY achieve

- Why we are Invested in LKY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.