Konekt takes advantage of dominant position in workplace injury industry

Published 24-AUG-2017 15:07 P.M.

|

6 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

There are few situations more demoralising than being unable to work due to health problems. Health issues can be a pre-existing or unrelated conditions not linked with the person’s place of employment, or on the other hand, the workplace can be the very reason why an employee is suffering an injury or illness.

Regardless of the circumstances, not only are these issues prominent in the minds of individuals, they are also at the forefront of strategies and funding undertaken at both the government and corporate level.

Australia’s largest provider of organisational health, risk management and return to work solutions, Konekt (ASX: KKT) provided some interesting data when it delivered an impressive fiscal 2017 result earlier this month.

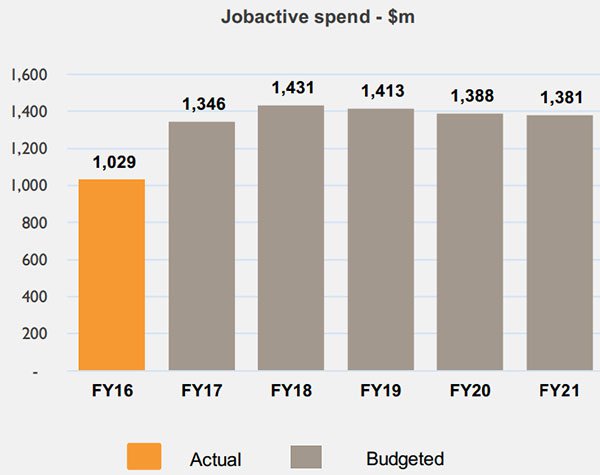

The company noted that Federal Government funding for the jobactive program is approximately $1.4 billion per annum through to fiscal 2020. Konekt has valuable relationships at a government level in terms of maximising workforce participation through its expertise in the areas of injury management and return to work programs.

The following graph which reflects data from the Department of Employment Budget Statements demonstrates the uptick in spending in this area since 2016, and the proposed substantial investment through to fiscal 2021.

Industry leading position in niche fragmented market with high barriers to entry.

As part of its role as Australia’s leading provider of return to work solutions, KKT also provides employers with strategies regarding injury prevention and/or the minimisation of workplace injury, effectively minimising the costs and drags on productivity which are normally associated with employee injuries.

KKT has over 350 allied health professionals providing workplace and injury management services to its clients and their employees. It is the industry leader in this segment with a market share of circa 12%.

KKT’s clients include major employers in both public and private sectors, as well as Australia’s largest insurance companies.

While KKT is the industry leader, the market remains highly fragmented and opportunities for growth by acquisition have assisted the company and growing revenues and entering new markets/regions. Working in KKT’s favour is the fact that it has a strong balance sheet and on this note the company was debt free as at June 30, 2017.

However, investors should still seek professional financial advice for further information if considering this stock for their portfolio.

However, an opportunity to acquire a business which was both complementary and provided access to revenues from a relatively new industry segment emerged in August. KKT was able to complete the $24 million acquisition of Mission Providence with the assistance of a part placement and rights issue.

Transformational acquisition to provide the next leg of growth

Mission Providence is a leading provider of employment services and the New Enterprise Incentive Scheme (NEIS) under the Federal Government’s jobactive program. The enterprise is a joint venture between Mission Australia and the Providence Service Corporation (US).

Mission Providence is one of 43 providers holding a jobactive contract with the Federal Government’s Department of Employment. The contract has nearly 3 more years to run when it is expected to be put up for review prior to expiry, which may include tender, rollover or restructuring of the program. NEIS revenues represented 15% of the group’s fiscal 2017 income.

Commenting on the acquisition, KKT Managing Director, Damien Banks said, “The acquisition of Mission Providence makes strategic sense for our business and delivers value for all our stakeholders, enabling us to expand into adjacent employment markets with scale, consistent with our focus and purpose of maximising outcomes for the individuals with whom we work.”

Fundamentals look attractive

On a pro-forma basis the merged business is expected to approximately double revenue and EBITDA while delivering earnings per share (before amortisation) accretion of 20% in fiscal 2018.

While the earnings per share impact will be even more pronounced in fiscal 2019, crunching the numbers relative to the company’s fiscal 2017 result indicates that KKT is in a fundamentally strong position, and perhaps undervalued relative to its current share price.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance

The company’s fiscal 2017 underlying net profit of $3.2 million represented earnings per share of 4.4 cents, implying year-on-year growth of 15%. An increase of 20% in fiscal 2018 would translate into earnings per share of approximately 5.3 cents.

This indicates that the company is trading on a PE multiple of approximately 10. Given its demonstrated ability to generate strong growth in recent years, while also taking into account the robust incremental impact of the Mission Providence acquisition, it wouldn’t be surprising to see the company trade on a more aggressive multiple once the financial impact of the acquisition begins to materialise.

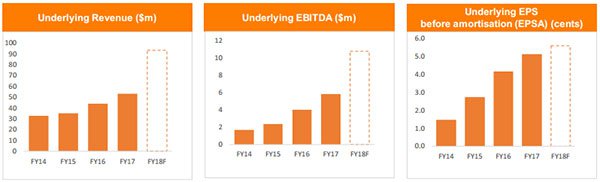

However, it is worth noting that management has an established record of delivering strong growth while maintaining financial discipline, and this is reflected in the following four year data shot which also encompasses guidance incorporating the acquisition.

Management has demonstrated its ability to efficiently integrate acquisitions

This raises the question as to whether investors are perhaps better off snapping up KKT at what would appear a discount price, or whether it would pay to wait for evidence to emerge regarding the fiscal 2018 earnings outlook based on the success of the acquisition, as well as the traditional organic earnings growth that the company has been able to generate over the last four years.

Regards the latter it would pay to bear in mind that KKT should benefit from a number of developments that occurred in the last 12 months including the execution of a new Medibank health solutions contract in May 2017, its panel appointment in the Commonwealth Government sector and its appointment to icare New South Wales Workers Compensation panel for fiscal 2018.

On the score of assessing its ability to efficiently integrate Mission Providence, it is worth considering the fact that management has in the past successfully bedded down businesses acquired in various sectors of its operations, including SRC Solutions and CommuniCorp in 2016, with the latter improving its position in the high-growth psychological health market segment.

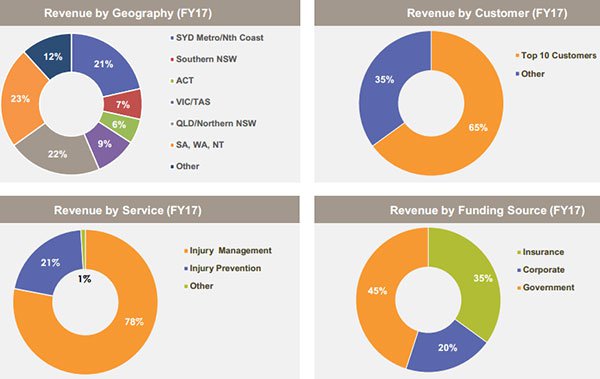

The company has a healthy spread of income across geographic regions, and the fact that it generates revenues from multiple sources such as the government sector, corporations and insurance companies helps to provide insulation against one-off events such as contract losses.

As indicated in the graphs below, the company also generates revenue from injury management which many corporations see as an investment rather than an expense. This is often the source of recurring income as KKT provides ongoing services to its existing client base.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.