Just 3 days ago China tightened indium export checks and threatened export controls. AW1 has the biggest indium resource in the USA.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 16,500,000 AW1 Shares and 11,148,990 AW1 Options at the time of publishing this article. The Company has been engaged by AW1 to share our commentary on the progress of our Investment in AW1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Three days ago China tightened export checks on the niche critical mineral indium:

(source)

Sending a signal that full indium export controls could be next.

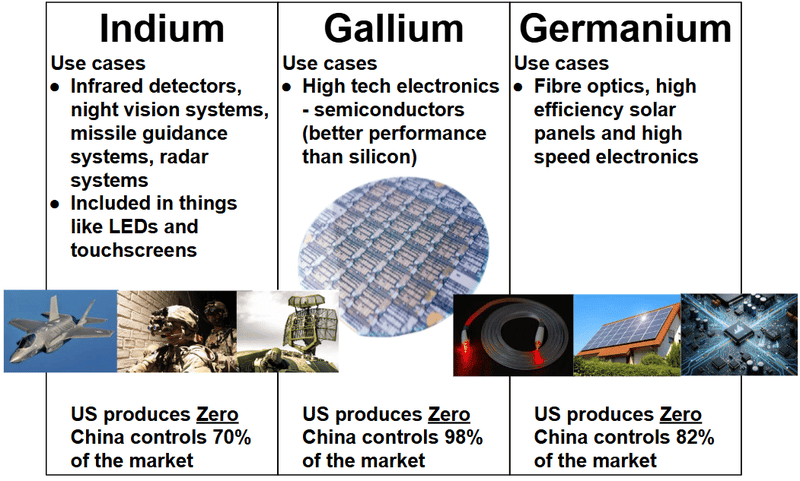

Indium is used to produce AI chips in next gen data centres, night vision systems, missile guidance radars and F-35 fighter jets.

Demand is increasing in the global race to build the best and fastest AI and advanced weapons.

China controls ~70% of global indium production.

The USA has ZERO domestic indium production.

(last month the USA flagged indium shortages for the first time)

Countries diversifying critical minerals supply away from adversaries is a key theme we have been Investing in.

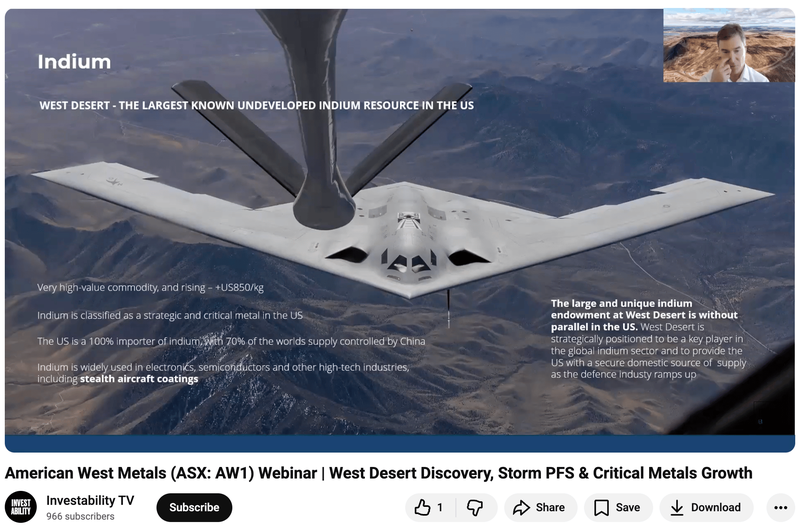

Our Investment American West Metals (ASX:AW1) holds 100% of the biggest indium resource in the USA.

AW1 is drilling its project right now and only a few weeks ago hit a new discovery hole ~430m east of its giant indium resource (more on the drilling in a second).

We Invested in AW1 in anticipation that indium could get caught up in the brewing “export controls wars” between the East and West.

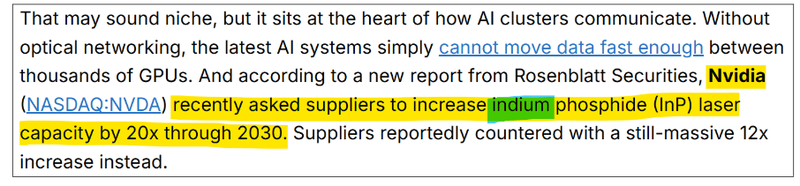

Surging demand for high tech use cases has seen the value of indium increase by more than 90% year on year.

World leading end users like NVIDIA Corp (NASDAQ: NVDA) (currently the most valuable company on the planet) have requested a 20x increase in the supply of indium phosphide by 2030.

(source)

A week ago the US put export restrictions on Anthropic’s (AKA Claude’s) latest AI model.

That meant no one outside of the US could use the model.

China’s “hold my beer” response has been to lay the groundwork for potential near term export controls on indium.

China’s way of saying - no software for us? - fine, then no minerals to build and power your software.

Leading up to that, in May, for the first time, the US flagged potential domestic indium shortages.

(source)

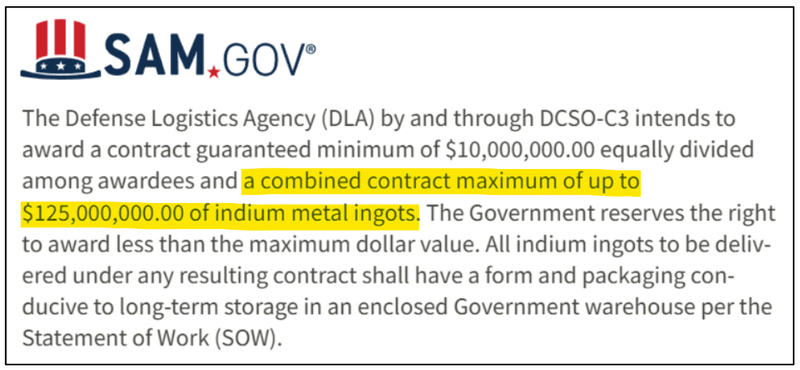

And before that, in February this year, the US Defense Logistics Agency (DLA) released a contract opportunity for the supply of indium worth up to US$125M.

(source)

That was the second time the DLA has gone looking for indium supply - the first time was in August last year.

So the US has been looking for supply for a while - but the urgency went up a level over the last 72 hours.

(Just in case China decides to put in outright export bans)

As mentioned earlier, our Investment AW1 holds 100% of the largest indium JORC resource estimate in the USA.

AW1's project is already fully permitted for an open-pit mine and exploration shaft construction.

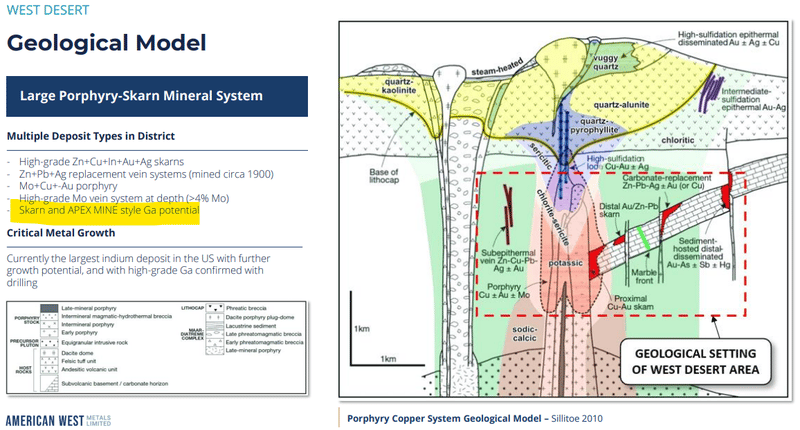

The project might also contain critical minerals gallium and germanium too.

(historic core samples showed a 518m continuous gallium intersection with peak grade of ~77.3 g/t).

So AW1’s project could actually be a source for three critical minerals that the US is 100% reliant on imports for.

(China produces 70% of the world's indium, 98% of the world's gallium, and 60% of the world's germanium.)

AW1 is drilling its project right now.

The last time we wrote about AW1 it had reported visuals from a hole ~430m away from its giant resource. (source)

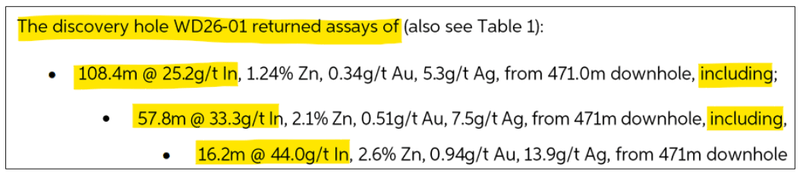

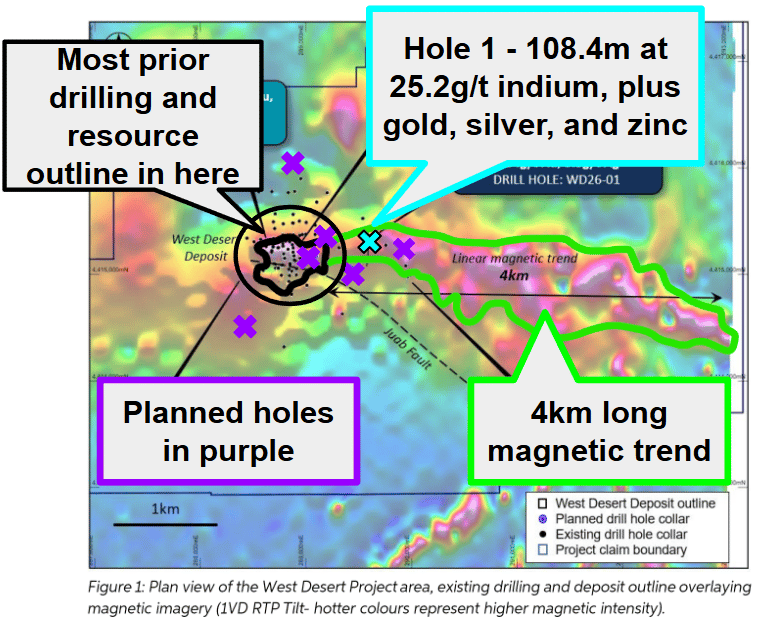

That hole came in and was declared a new discovery with a ~108.4m hit - extending the USA’s biggest indium JORC resource.

The hit also came in above the current resource’s average grade:

(source)

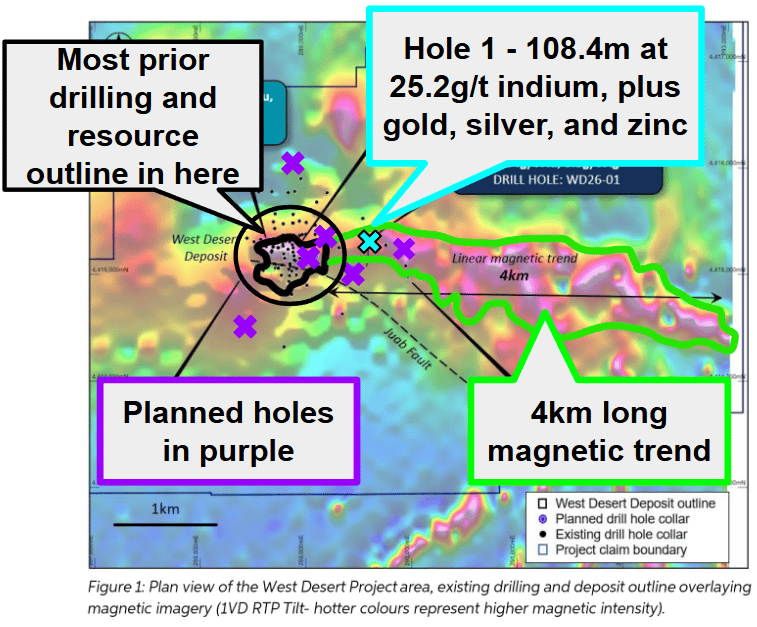

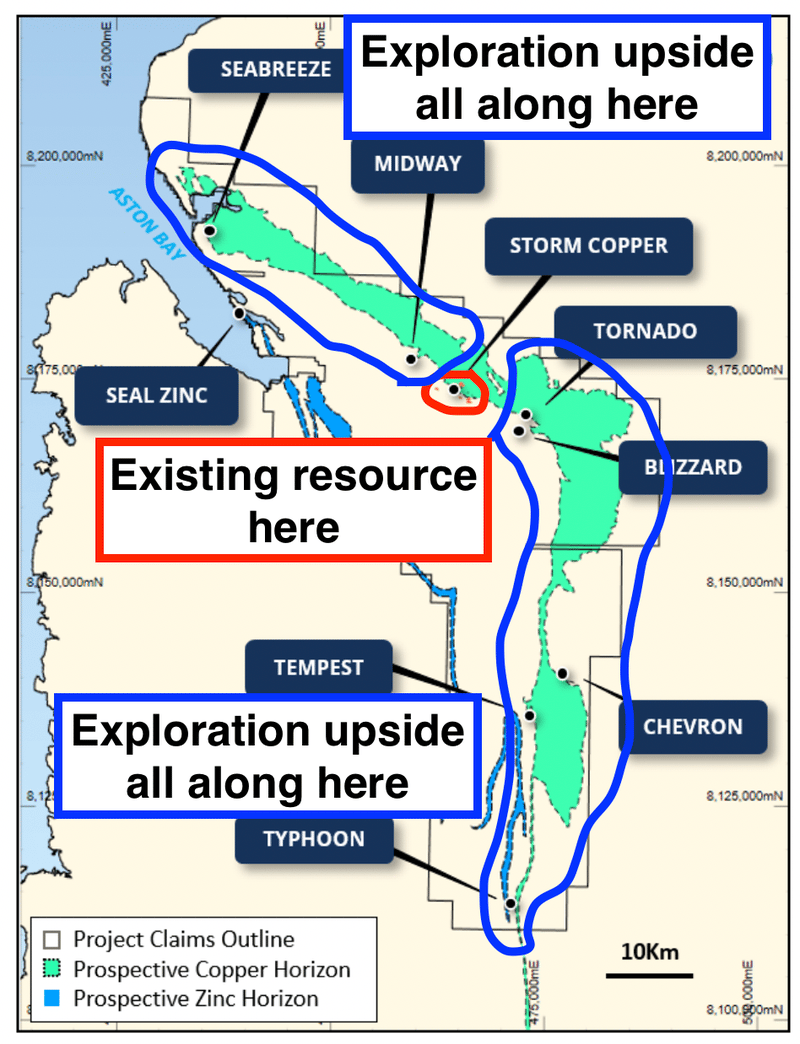

The bigger kicker was that the hole validated AW1’s theory that its resource could actually extend all the way across a ~4km long magnetic anomaly:

(source)

So with one drill result, AW1 has opened up potential extensions ~4km to the east and shown that the resource average grade could be a lot higher too.

So far so good for the first hole of the program.

Another win for AW1 was that hole averaged 0.34g/t gold - which is more than 3x the gold grade of AW1’s existing defined resource (0.10g/t).

Gold credits are good because pairing a strategic critical mineral (like indium) with a predictable-revenue commodity (like gold) could make it easier to finance AW1’s project.

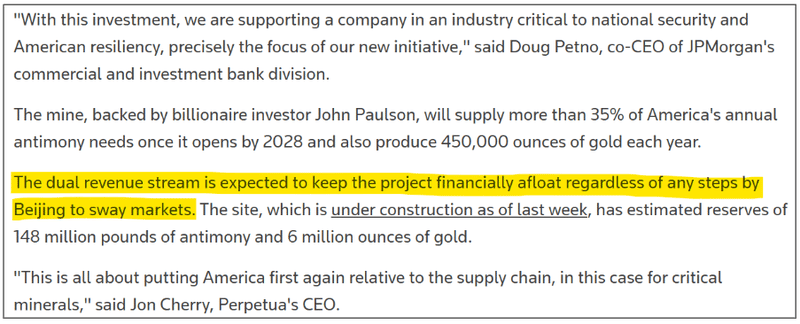

A case in point is JP Morgan investing US$75M into the biggest antimony resource in the US, owned by $4.3BN Perpetua Resources.

Comments from JP Morgan's co-CEO still live rent free in our heads about dual revenue stream critical minerals projects.

JP Morgan were attracted to that asset’s “dual revenue stream” from gold production and antimony - which would keep the project “financially afloat” even if critical minerals prices fell:

(source)

So groups like JP Morgan are out there funding the “biggest of its kinds” critical minerals projects capable of absorbing JP Morgan sized cheques.

Good news for AW1 - the biggest of its kind for indium in the USA.

And AW1’s project could potentially have multiple revenue streams too.

(AW1’s asset has ~49,000 tonnes of copper in its resource and then there is the gallium/germanium we mentioned earlier too - source)

We think that after this weekend's news, the attractiveness of AW1’s indium project for any critical minerals earmarked funding in the US has got a lot stronger.

And we note AW1 is currently working with Washington DC firm Ervin Graves Strategy Group on potential US government funding pathways - including the Defence Production Act Title III program.

AW1's MD Dave O'Neill talked about the US funding discussions in a recent webinar - skip to 18:43 where he says:

“I can't talk to what is going on behind the scenes. Obviously, there's confidentiality around the US discussions and things like that. John's (Prineas, co founder of AW1 and Non-Executive Director) in Washington DC as we speak... he’s attending the defense and aerospace conference at the moment for critical metals”

(source)

We think that as AW1 drills out its project and is able to define an even larger resource - its attractiveness as a potential source of a critical mineral where the US has no current domestic supply becomes a lot harder to ignore.

AW1 is drilling the project 24/7 right now

As it stands, AW1’s project is the only primary indium JORC resource on US soil, AND:

- Only ~35% of historical drill cores have ever been assayed for indium.

- Only ~10% of historical drill cores have been assayed for gallium and germanium.

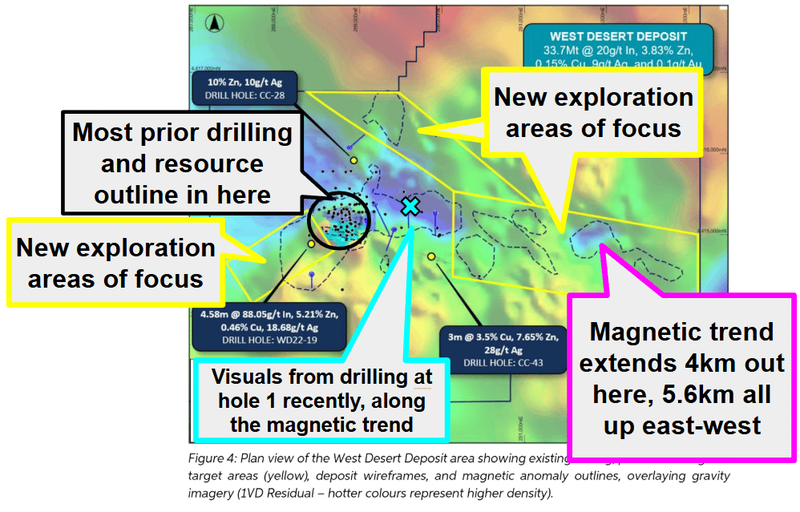

This is the first drill campaign in the project's history where AW1 is systematically assaying all of indium, gallium, germanium, zinc, copper, silver, tellurium AND gold.

And from the first hole AW1’s hit a ~430m extension to the east along a previously untested 4km magnetic anomaly.

(source)

Immediately after, AW1 confirmed that:

- A second diamond rig was arriving to site to accelerate the drilling,

- A third hole is already underway ~350m further east of the extensional hole assays were announced from along the same 4km trend, and

- Assays for the second hole (WD26-02) were expected within “the next week”.

That was two weeks ago now - so we could see assay results any day now.

We also note AW1 will be doing some down-hole electromagnetic (DHEM) surveys to generate more targets on the project.

So there is a steady stream of assays and new targets coming over the next few weeks and months.

If assays keep coming in across that magnetic anomaly, AW1’s project could have mineralisation sitting across ~5.6km... which in terms of mining projects, is massive.

Most orebodies are hundreds of metres long and rarely in the kms long in terms of scale.

Of course - the mineralisation might not keep going when drill tested.

(source)

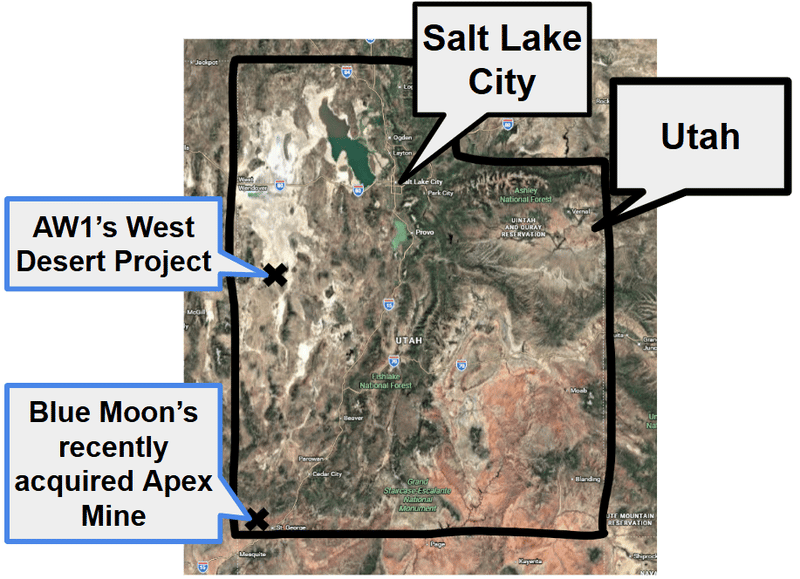

AW1’s next assay result to test the APEX mine comparison

One of AW1’s exploration theories is that its project shares geological similarities to the Apex Mine, ~300km away.

The Apex mine is the only primary gallium mine that has EVER operated in the United States.

At its peak, the Apex was producing germanium at grades of up to 7,000 g/t and gallium at up to 20,000 g/t.

Since that mine was shut down, the US has produced no gallium domestically.

Interestingly, the mine wasn’t just producing gallium-germanium but also copper in the 1980s and 1990s.

(As we mentioned above, AW1’s asset also has some copper - an estimated 49,000 tonnes - a JORC indicated and inferred estimate - source)

We already know AW1’s got gallium in an old core that's been resampled (up to 77.3g/t).

Now, with the current drill program, we get to see those Apex-style targets tested properly for the first time.

Why does that APEX mine comparison matter right now?

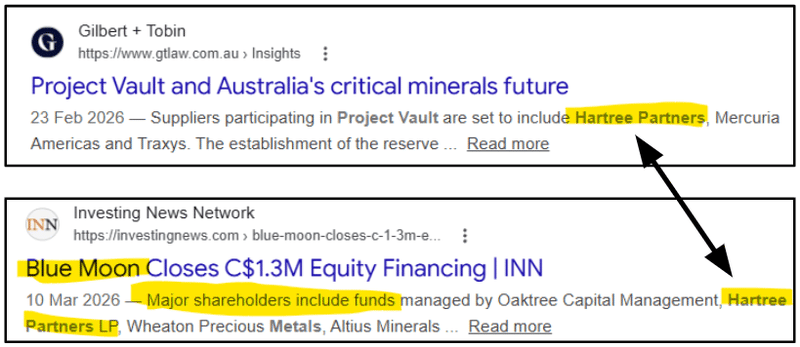

Because earlier in the year, the old Apex mine was purchased by NASDAQ-listed ~A$820M Blue Moon Metals in a deal worth ~US$32M.

(source)

Blue Moon has Hartree Partners (a key partner with the US government on the recently announced US$12BN critical metals stockpile "Project Vault"), Wheaton Precious Metals, and Oaktree Capital on its register.

We think that the Apex mine deal shows there is demand for assets like AW1’s in the US.

AND if a partner to the US critical minerals stockpiles is backing the Apex mine - then some solid drill hits from AW1 could put its project on their radar too.

(only this time, they will get indium to go with the gallium/germanium too)

The next assay result due (hole #2) will be the one testing for “APEX style” mineralisation and based on the last bit of guidance that result could drop any day now.

(source)

Of course, there is no guarantee that AW1's drilling will return economic grades.

That's the risk with exploration - what AW1 has shown so far is encouraging, but there are no guarantees with exploration drilling and lab assay results.

Here is where AW1’s project sits relative to that Apex Mine:

(source)

Ultimately, success on the US asset is a big part of our AW1 Big Bet:

Our AW1 Big Bet:

“AW1 receives capital from either the US government, a strategic partner or the capital markets to progress its Indium project in the USA, re-rating AW1 to a valuation that is multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AW1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

AW1 also has an advanced-stage Canadian copper project

Another reason we like AW1 is for its advanced-stage copper project in Canada.

We think this asset alone underpins a big chunk of AW1's current $50M market cap.

The project is an advanced-stage copper-silver asset in Northern Canada with a current JORC resource of 28.2 million tonnes at 1.0% copper and 3.3 g/t silver.

(276,000 tonnes of contained copper + 3.0 million ounces of contained silver)

The current 28.2Mt resource sits on less than 5% of the project's prospects.

The full horizon is 110km long - so it could get a whole lot bigger with more drilling.

(source)

AW1 completed a Preliminary Economic Assessment for the project back in March last year which demonstrated: (source)

- Post-tax NPV: US$149M

- Initial CAPEX: US$47.4M

- Mine life: ~6 years (with 10 years of processing)

That study was based on a copper price of US$4.60/lb and silver at US$25/oz.

Today's spot is ~US$6.31/lb copper and ~US$65/oz silver.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So the current economics of AW1’s copper project could be a lot stronger.

AW1 is currently working on a Pre Feasibility Study (PFS) for the project.

The reason we like the project is because it once had farm-in deals with both $307BN BHP and $74BN Antofagasta.

In 2016, $307BN BHP signed an earn-in deal that would have seen them spend US$50M on the project.

Mining supermajors don't farm into projects that don't meet their size/scale criteria - we think what attracted BHP to this asset was the 110km of exploration upside.

$74BN Antofagasta also JV'd into the project around the same time.

Both had walked away by 2018.

Probably more to do with the copper price tanking and both companies refocusing their efforts on the giant porphyry deposits they were developing in South America.

Copper was trading around US$2.80/lb at the time of the BHP walkaway.

We also like that AW1 already has options in place to fund the CAPEX for the project including:

- A binding offtake agreement with Ocean Partners - Ocean owned 9.4% of AW1 when this was finalised in mid 2025. The offtake deal could also provide debt finance for up to 80% of initial capital for development and receive 100% of the offtake rights for 8 years. (source)

- An A$18.8M royalty deal for non-dilutive funding - This deal would see AW1 receive US$3.5M once a PFS is completed and permitting documents submitted for development + US$4M if a resource that contains at least 400kt of copper averaging at least 1.00% is shown (AW1’s resource is currently 276Kt copper at 1.0%). (source)

We think fundamentally, the setup for copper is as good as it gets - both in the short/medium and long term.

Some might remember the “copper is the new oil” stuff from back in 2021 when copper was the backbone of the electrification/energy transition.

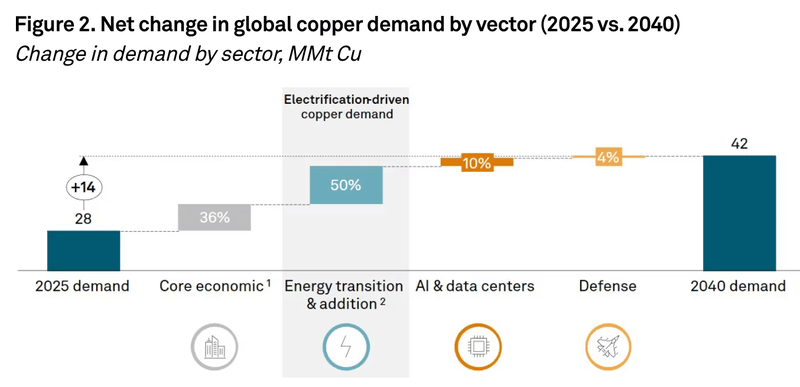

Since then, AI data centres and robots entered the chat - in a big way - and the copper demand story is seriously strong now on a 5, 10 and 20 year outlook.

It turns out hyperscale data centres use a massive amount of copper (sometimes ~50,000 tonnes of copper in a single data centre).

(source)

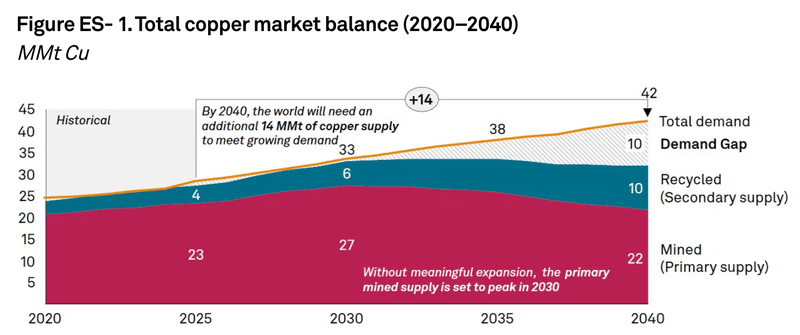

IF even half of the AI/robotics/energy transition build out happens that is a big increase in demand in a very mature market - where supply can't just be brought online overnight.

(source)

IF copper price really goes parabolic and all of the calls for a structural supply shortage plays out then this asset could be the big dark horse for AW1.

Here is another presentation from Robert Friedland - titled "Dawn of the Copper Age" where he covers the AI - copper connection really well.

Our key takeaway:

Humans will need to mine more copper in the next 18 years than we have mined in all of recorded history combined - just to meet forecast demand from AI data centres, grid upgrades, chips, weapons systems and electrification.

PRESENTATION: The dawn of the copper age

What's next for AW1?

US indium project (West Desert, Utah)

Here we want to see AW1 run its upsized drill program, grow its resource and hopefully define a gallium & germanium resource to go with it.

Here are the milestones we are tracking:

- ✅Drilling commenced

- ✅First hole hit 108.4m at 25.2g/t indium (plus gold, silver & zinc) 430m east of resource, along the 4km magnetic anomaly

- 🔄 Historical core resampling for gallium & germanium.

- 🔲 Assays from drilling

- 🔲 Resampling assay results

Strategic / Government Engagement

- 🔄 Defence Production Act Title III funding

- 🔲 Formal US government funding deal / offtake / stockpile inclusion

- 🔲 Potential US listing

Canadian copper project

The next major catalyst for this project will be the PFS that is currently underway.

Here are the milestones we are tracking for the copper:

- 🔄 Pre-Feasibility Study

- 🔲 Environmental studies and permitting milestones

What could go wrong?

The biggest risk for AW1 right now is "Exploration risk".

AW1 is actively drilling its indium project in the US.

IF the market starts to build in higher expectations from future drill results and AW1 returns disappointing results it could negatively impact AW1’s share price.

Another risk is “Critical Minerals Macro risk”

Critical Minerals Macro risk

A big part of our Investment is related to critical minerals macro sentiment strengthening and resulting in a funding deal for AW1’s US indium project. IF macro sentiment was to turn, then the chances of that asset being funded/brought online would reduce significantly. This could mean a re-rate lower in AW1’s share price.

Source: “What could go wrong” - AW1 Investment Memo 16 October 2025.

Other risks

Like any early-stage exploration company, AW1 carries significant risk, here we aim to identify a few more risks.

The underlying economics of both the Canadian copper asset and the US indium project rely heavily on global spot prices holding steady or increasing. If copper, silver, or critical mineral prices crash, the commercial viability of these projects could evaporate entirely.

A core part of the AW1 investment thesis relies on securing US government support under initiatives like the Defense Production Act. Government policies and defense priorities can shift rapidly, and there is absolutely no guarantee these strategic grants or stockpile purchases will ever materialise for the company.

Running an aggressive 24/7 drill program in Utah while simultaneously trying to advance a copper asset in Northern Canada is logistically complex. This dual focus across two completely separate international jurisdictions could severely stretch management's time, budget, and operational bandwidth.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our AW1 Investment Memo

You can read our AW1 Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our AW1 Investment Memo covers:

- What does AW1 do?

- The macro theme for AW1

- Our AW1 Big Bet

- What we want to see AW1 achieve

- Why we are Invested in AW1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.