ION: Signs binding agreement for rare earths recycling in the USA

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 24,360,000 ION Shares at the time of publishing this article. The Company has been engaged by ION to share our commentary on the progress of our Investment in ION over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The USA is urgently trying to secure a domestic rare earths supply.

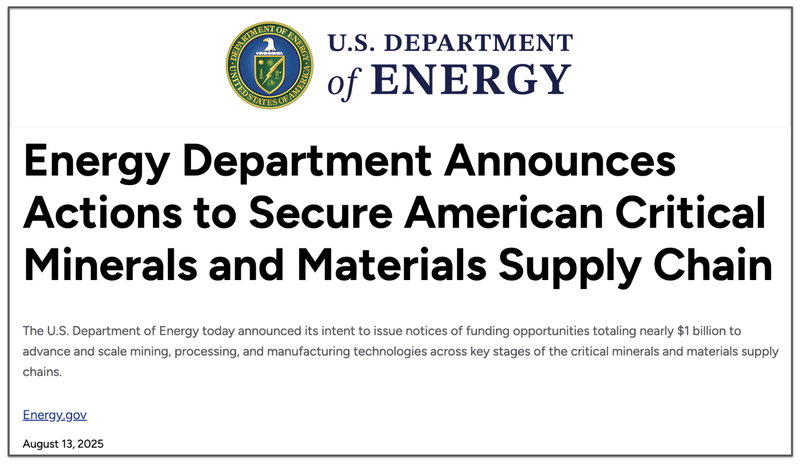

Including from recycling - where the US Dept of Energy last week allocated hundreds of millions of dollars to accelerate US rare earths recycling capabilities...

IonDrive (ASX:ION) just announced a BINDING agreement for rare earths recycling in the USA.

(a proper “binding” contract where stuff will actually happen, as opposed to a fluffy “non-binding MoU” that we often see at the small end of the ASX market)

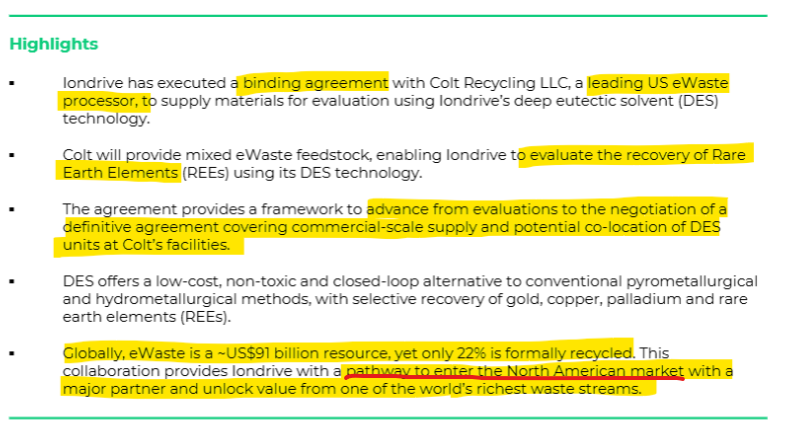

The binding agreement is with Colt Recycling, a part of the Elemental Holding Group that has advanced recycling operations in more than 20 countries across four continents...

Colt is one of the USA’s largest and most advanced eWaste recycling companies...

In the US alone, Colt processes ~40 million lbs (18 million kilograms) of eWaste every year.

The agreement is to test if ION’s tech can successfully recover rare earths from Colt’s eWaste...

Inside US borders.

IF ION can successfully show its tech can recover rare earths commercially, Colt could push ION’s tech into its metals recycling facilities across the US.

ION was actually given a grant to test its tech on e-waste specifically for rare earths back in June so they will probably already know what they can deliver to Colt...

And Colt signing a binding agreement with ION means they must be happy with what they are seeing from ION so far...

(there was no guidance in the announcement on when the market should expect results to be announced)

If the trial is successful it could mean ION’s tech plugs straight into a business processing ~40M lbs of e-waste every year...

Inside the USA...

Just as China is trying to exert even more control on the rare earths market:

(Source)

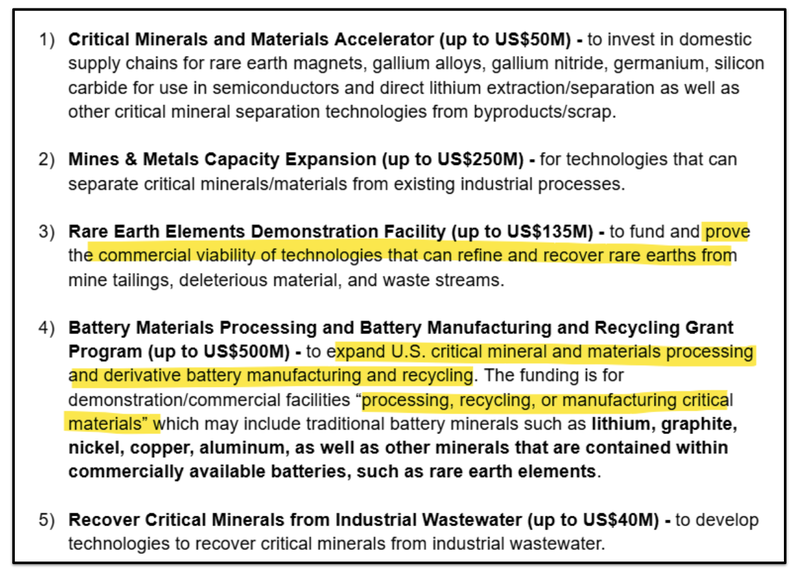

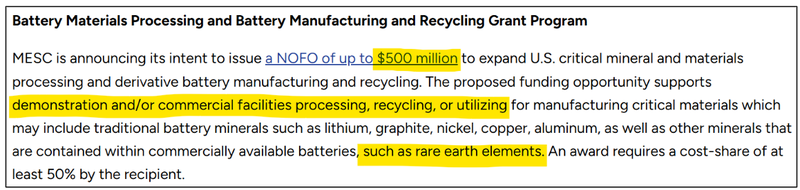

And just as the US government, through the Department Of Energy (DOE), is looking to put to work ~US$1BN in grant funding for:

“demonstration/commercial facilities”, “processing, recycling, or manufacturing critical materials”, “that are contained within commercially available batteries, such as rare earth elements”.

(Source, US Department of Energy)

The US DoE funding was split into five separate pools of cash.

We think ION’s tech fits into pool #3 and pool #4 of the two DoE grant areas (totalling ~US$635M of the US$1BN in DOE funding pool).

In a weekend note a few weeks back we said “We think that ION could be a big winner from this news because a lot of the DoE funding is earmarked for recycling and reprocessing technology”

Not just because ION at the time had explicitly said it was in the US looking at rare earths partnerships...

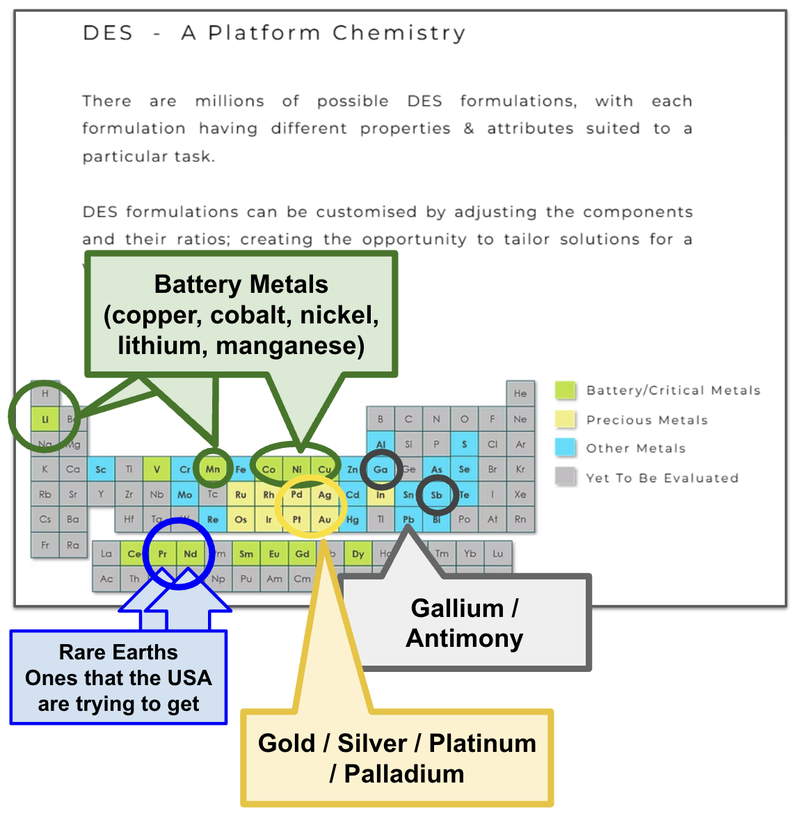

But because ION’s Deep Eutectic Solvents (the chemical process used in ION’s tech) can be applied across a whole range of other critical minerals, including copper, cobalt, gallium, antimony, silver and gold to name a few.

Here is a chart showing which minerals Deep Eutectic Solvents have been tested on:

We think that today’s deal with Colt could be the precursor for similar deals across other critical minerals, again inside the US.

The current ‘in focus’ minerals in the US right now are antimony and rare earths.

ION hasn’t done so yet, but it could try its technology at recovering antimony from different feedstocks.

And then whatever becomes the next urgent critical mineral is in the US - ION could again move quickly to testing its tech on feedstock to recover that particular mineral.

Giving ION multiple shots at inserting itself into the middle of one of our favourite macro thematics right now - US critical minerals.

(which we think is just getting started...)

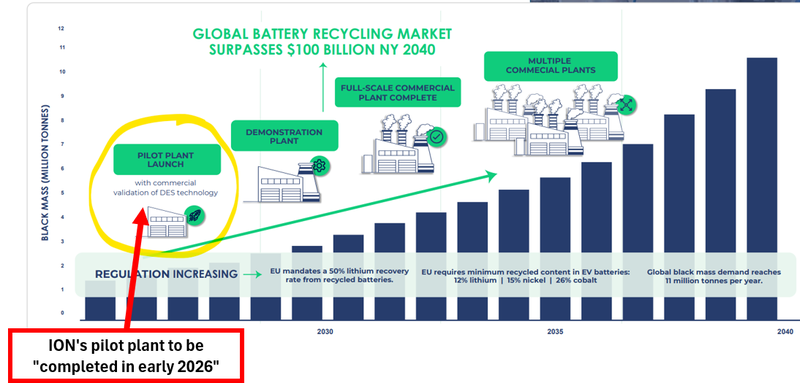

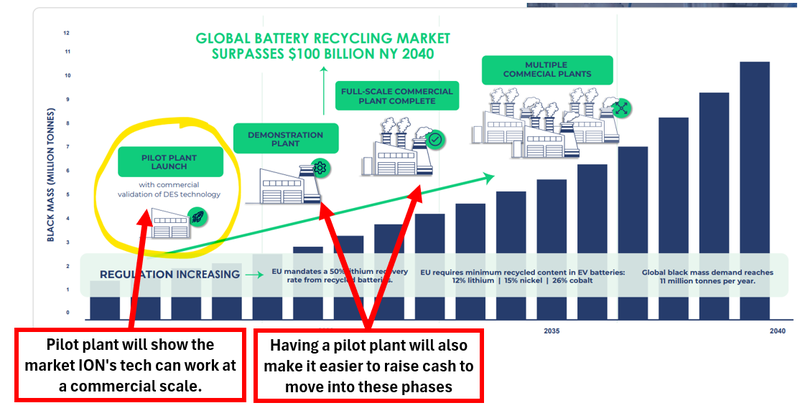

And all of this is happening as ION quietly announced a Final Investment Decision (FID) on a battery recycling pilot plant...

ION will have its battery recycling pilot plant ready by “early 2026”

Only a few weeks ago, ION received ~A$3.9M in non-dilutive grant funding from the Australian government to build a metals recycling pilot plant.

And on the same day ION’s board approved the construction of a Pilot Plant, with construction to start in December 2025 and be completed in early 2026.

This grant would fund 50% of the cost of ION’s pilot plant up to a maximum of A$3.9M.. ION expects the plant to cost $4.38M,, which means ION should comfortably have 50% of the plant’s costs funded with today’s grant, even if there are cost overruns.

The plant would be built in Australia but ION’s CEO did say in a recent interview that it will be a “mobile unit” that can be moved anywhere in the world if needed...

The pilot plant is the first time ION is proving up its technology at a scale larger then bench scale testing.

Now that ION is funded to completion of its pilot plant, we think it sets up the company for bigger funding deal discussions on scaling up even further.

And we note that US$500M of that US Department Of Energy funding deal that we mentioned earlier today is reserved for demo/commercial scale plants like the one ION would be looking to build next...

(Source)

What is ION working on now? Six catalysts that could re-rate ION inside the next 6 months

Over the next 6-9 months, we think one (or multiple) of the below catalysts could trigger a sustained re-rate in ION’s market cap:

- [New] US rare earths partnership - ION will now test its tech on e-waste feedstock to see if it can commercially recover rare earths. IF successful, ION’s tech could be rolled out across recycling facilities processing ~40M lbs of e-waste feedstocks annually.

- Pilot plant build for battery recycling tech - as mentioned earlier, we think this will be a big inflection point for ION. ION expects to have the plant built and commercially producing by “early 2026”.

- EU grant decision - ION has also applied for a €3.1M EU grant with a consortium that includes “carmakers, battery manufacturers, material processors, and recyclers”. We expect an update within the next 3 months.

- ION’s mineral processing tech gets de-risked - ION is currently testing its technology on “US sourced feedstock”. Any big feedstock supply deal, partnership deal or any strong recovery results could be a big unexpected catalyst for ION.

- Application into new markets - Here, ION is looking at recovering copper, gold, silver, osmium and rare earth elements from e-waste (Printed Circuit Boards). Results from these tests could come at arbitrary times. We could see the market re-rate ION if the results are positive.

- Graphite upgrade results - updates on this front came from a recent ION’s announcement. If ION can produce anode-grade graphite from recycled black mass, it could add to the economics of its pilot plant and strengthen the commercial case for a bigger plant. See our Quick Take on that news here.

Ultimately, a combination of the above catalysts AND ION switching its pilot plant on and commercialising its tech is what we want to see.

Commercialisation is central to our Big Bet which is as follows:

Our ION Big Bet:

“ION re-rates to a +$150M market cap on successful large-scale production of commercial quantities of battery materials through its recycling process and/or by securing important partnerships in the recycling industry.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including technology risk, scale up risk, regulatory risk and development risk - just some of which we list in our ION Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

ASX:ION

How does ION’s tech work and how does it compare to other ASX listed players?

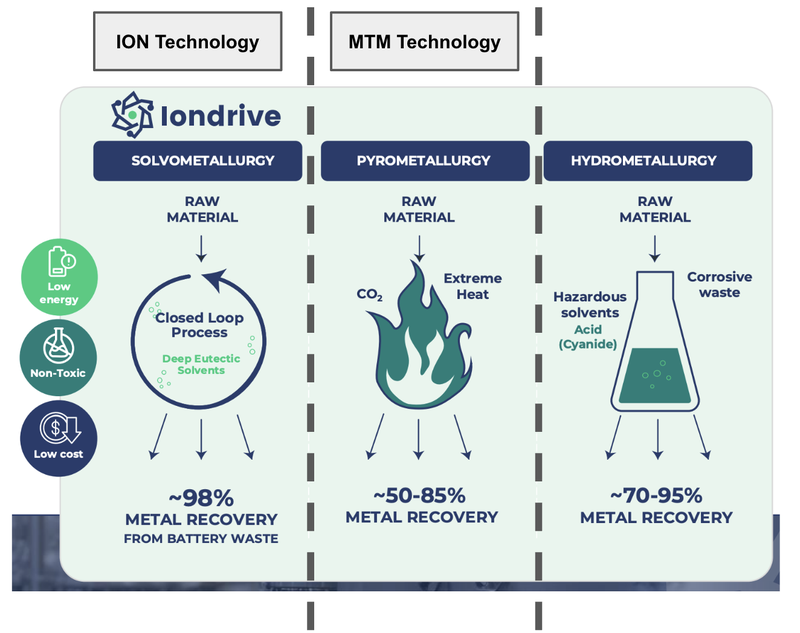

One of the key reasons we Invested in ION was because its technology is different to other recycling technologies in the market.

Most battery metals recycling technologies are some form of a pyrometallurgical process OR a hydrometallurgical process:

- Pyromet - where things are heated to extremely high temperatures using heaps of energy. Energy that can be expensive and depending on the location of the plant, not very environmentally friendly.

- Hydromet - where acids/solvents are applied to treat waste. Sometimes these acids/solvents can be environmentally damaging/toxic.

ION’s tech is a different form of hydromet which uses “Deep Eutectic Solvents (DES)” together with “benign organic solvents”.

The combination means ION’s approach uses solvents that are non-toxic and oftentimes biodegradable.

This chemical approach should be a lot more cost effective and have lower energy requirements compared to existing recycling methods.

The biggest runner in the recycling tech small cap space this year has by far been ASX listed Metallium - which is up over 25x in 16 months...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Metallium’s tech fits into the pyromet category, using huge amounts of energy to burn and incinerate everything except for the metals that need to be extracted.

That means Metallium’s technology can be a lot more energy intensive relative to ION’s tech.

Our bet is that ION can recover metals with a lower carbon footprint, with biodegradable solvents and no expensive energy requirements.

Another key reason why we Invested in ION was because we thought its tech could eventually be applied to different critical minerals.

Remember that image from earlier in today’s note:

A big part of the run in Metallium’s share price has come from almost weekly announcements applying Metallium’s tech to different feedstocks, recovering everything from gold to gallium...

We think that when the market starts to see ION’s tech being applied to recover different critical minerals ION’s valuation could start to bridge the gap to peers like Metallium.

Metallium is currently capped at ~$471M.

ION is capped at ~$53M.

We think there’s a valuation gap here that could see ION start to catch up to Metallium over the coming months.

(No guarantees of course)

What are the key risks?

The main risk for ION in the short term is “Scale up / Technology risk”.

Now that ION is moving into new markets, there is no guarantee ION’s tech is able to produce the recovery rates needed for its tech to be deemed ‘commercially viable’.

There is also no guarantee that ION is able to replicate its bench scale performance in a larger pilot plant setting.

IF the market starts to price in expectations of positive results and ION is unable to deliver it could impact the company’s share price in a negative way.

Scale up / technology risk

There is no guarantee that the Pilot Plant is able to replicate the results from the large lab study. Also “feedstock reliability” both in terms of supply and consistency of material is a big risk for ION to scale up its operations.

Source: “What could go wrong” - ION Investment Memo 03 December 2024

Source: “What could go wrong” - ION Investment Memo 03 December 2024

We list more risks to our ION Investment in our ION Investment Memo here.

Other risks

Like any stock market investment, investing in ION carries multiple risks which may affect the value of the company.

The company's Deep Eutectic Solvent (DES) technology remains unproven at a commercial scale. While laboratory/bench scale results show promising recovery rates, there is no guarantee that ION will successfully scale this technology to profitable commercial operations or that it will prove economically viable against other more established recycling tech.

ION could face significant technical challenges, cost overruns, or delays in achieving commercial production.

The battery recycling market, while projected to grow significantly, is still emerging and highly competitive. ION faces competition from established players with proven technologies and may struggle to secure sufficient feedstock or offtake agreements at economically viable terms.

ION’s business model is also highly sensitive to fluctuations in critical metal prices (lithium, nickel, cobalt, manganese) and the economics of its recycling operations depend heavily on maintaining favorable price differentials between black mass feedstock and recovered metals.

Regulatory risk and government support also impacts ION. Any delays or changes to battery recycling mandates, export restrictions, or environmental requirements could materially impact ION's business model and market opportunity.

The company's European consortium strategy introduces partnership risks. Failure to formalise agreements, partner withdrawals, or disputes could delay or prevent ION's European market entry.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ION Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our ION Investment Memo where you will find:

- What does ION do?

- The macro theme for ION

- Our ION Big Bet

- What we want to see ION achieve

- Why we are Invested in ION

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.