Introducing our 2025 Tech Pick of the Year: Rocketboots (ASX: ROC)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,999,000 ROC Shares at the time of publishing this article. The Company has been engaged by ROC to share our commentary on the progress of our Investment in ROC over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

RocketBoots (ASX:ROC) is now our 2025 Tech Pick Of The Year.

Over the last six years, we have only ever announced three Tech “Picks of the Year”, so it's not something we do lightly.

We look at hundreds of stocks a year, and end up Investing in only about 8 to 12.

We then reserve our “Picks of the Year” for the stocks we think have the highest potential to deliver outsized, 1,000% returns over a mult-year period.

Our three previous Tech Picks of the Year were:

- 2024 Tech Pick of the Year - AML3D (ASX: AL3) - which at its peak was up 431% from our Initial Entry price, it is currently 158% above our Initial Entry Price.

- 2021 Tech Pick of the Year - Oneview Healthcare (ASX: ONE) - which at its peak was up 858% from our Initial Entry price, it is currently 284% above our Initial Entry Price.

- 2019 Tech Pick of the Year - Whitehawk (ASX: WHK) - which at its peak was up 364% from our Initial Entry price, it is currently 92% below our Initial Entry Price. Whilst WHK was travelling pretty well for a while it has more recently fallen out of favour with the market due to slow progress on new sales.

Other successful tech Investments we have made include EIQ (up as high as 147%, currently up 77%, ION (up as high as 379%, currently up 193%).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Why do we seem to be able to pick winners in tech? Aren’t we early stage resource investors?

We’ll explain in a second...

Our 2025 Tech Pick Of The Year is ROC.

ROC’s “Vision Artificial Intelligence” technology is used by giant companies (like major retailers and banks) to analyse and respond to in-store customer behaviours.

(basically this means using AI and advanced analytics on live in-store camera footage to analyse customer behaviours, allowing the giant company to improve operations across its sites).

It operates under a Software as a Service (SaaS) model.

Our Investment Thesis when we first Invested in ROC back in March was that ROC had already gone through the difficult “tinkering” stage of a tech company's lifecycle.

This revolves around years and years of building the product and getting it market ready, securing long term, renewing, big name customers and building a big sales pipeline....

We thought ROC was at the stage where it was ready to sign the big “transformational”, company making, recurring revenue deals.

The type of deal to kickstart the typical “surging growth” phase for a tech business.

(the kind of deals we want to see from all our tech Investments)

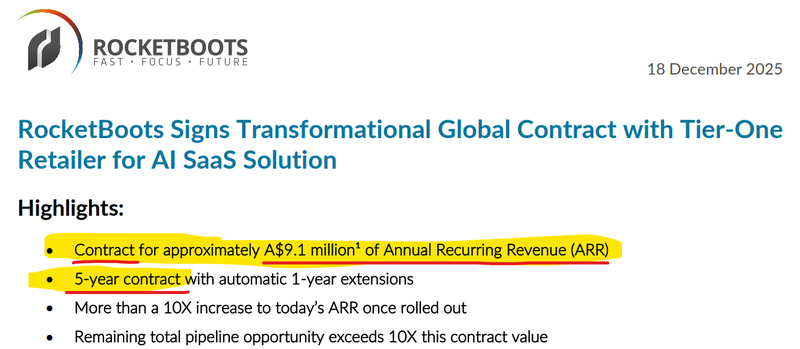

After holding for ~9 months, last week ROC delivered the transformational company making deal we had been waiting for.

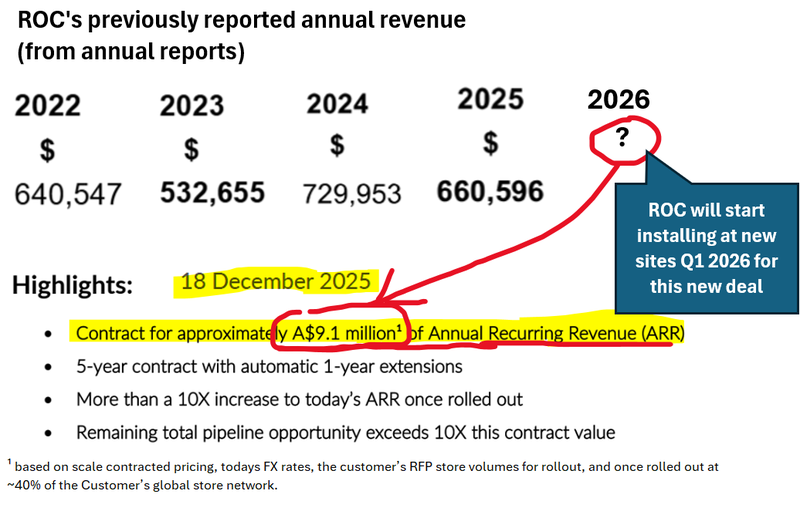

A ~$9.1M Annual Recurring Revenue (ARR) deal for an initial 5 year term...

14x’ing ROC’s FY25 revenues once fully rolled out.

This is only for 40% of the customer’s global sites.

(adding the remaining 60% of sites would equal ~$22.5M ARR to ROC....)

Plus sitting in ROC’s sales pipeline is another 10x this contract value...

In order to deliver on this new global contract (and more in its sales pipeline), ROC has just come out of a trading halt after raising $7M at 25c. This a solid foundation and cash runway for growth in 2026.

(source)

(we put cash in again to the 25c ROC raise... plus we got scaled back telling us there was strong demand)

With the transformational contract signed, and crucial capital now raised to execute, we have decided to make ROC our 2025 Tech Pick Of The Year.

(given its Christmas Day tomorrow, technically it’s sort of our 2026 Pick of the Year... but the capital raise was the final piece of the puzzle for us and it happened today, on Christmas Eve, so here we are in 2025)

We Increased our Investment in the capital raise today at 25c per share.

We think ROC’s deal, signed last week, was one of the best deals we have ever seen from any small cap ASX listed tech company...

... and also many private tech companies too...

How do we know this?

Before I became a silver nut, years ago I founded and ran a tech SaaS startup - it raised millions from Venture Capital funds in Australia and the USA and the pressure was on to grow our Annual Recurring Revenue as fast as possible...

(Sources)

Growing to $1M Annual Recurring Revenue (ARR) took us years - then the expectation and pressure to double ARR each year after that was immense.

In years where our ARR growth was fast, the Venture Capital money would come, at high valuations.

Having lived running an early stage tech company for many years (the company is still going and I am now on a non-exec the board) and experienced the difficulty in making large enterprise SaaS sales...

I can’t stress enough how significant and “company making” this new deal is from ROC.

Even doing a $100k ARR deal with a major global company is a significant achievement that takes a lot of hard work.

And being able to tell other major potential customers that one of their peers has committed to ROC’s product in such a big way will help accelerate closing their advanced stage pipeline in the near term.

So well done to the CEO Joel and the entire ROC team for getting this incredible deal signed - tens of thousands of public and private tech start ups would give anything to get a deal like the one ROC signed last week...

(I know I would have - I am legit extremely jealous of this deal)

Once rolled out, ROC’s deal is for approximately $9.1M Annual Recurring Revenue... (that’s $9.1M PER YEAR) for at least 5 years... and probably beyond.

With one transformational deal, they have increased their yearly revenue by ~1,400% (once fully rolled out)...

(Source: ROC announcement)

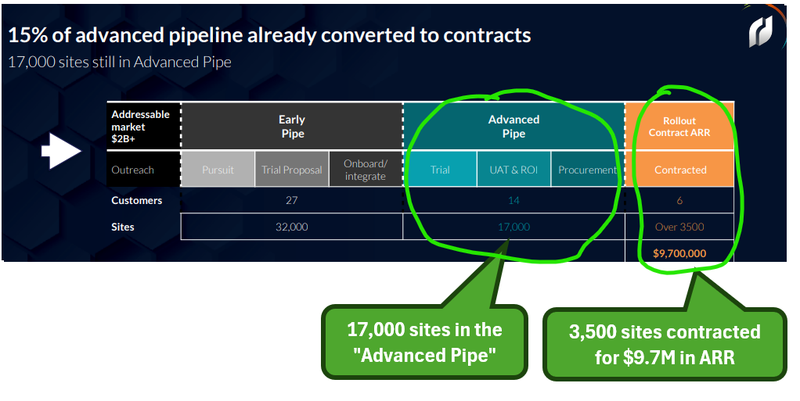

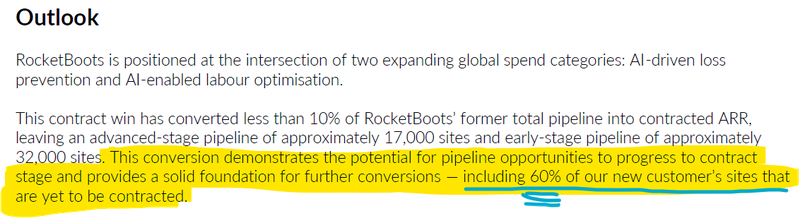

With this deal now closed, by our calcs ROC still has about ~$61M of potential revenue in its “advanced stage pipeline” across 14 global companies (more on this in a second).

There aren’t many ways of getting genuine AI exposure in the small cap ASX space at the moment.

(especially AI companies that actually make revenue...)

We think ROC is one of very few ways to get genuine exposure to AI being applied in a small cap tech stock on the ASX...

ROC’s “Vision Artificial Intelligence” technology is used by giant companies (like major retailers and banks) to analyse and respond to in-store customer behaviours.

(basically this means using AI on live in-store camera footage to analyse customer behaviours, allowing the giant company to improve operations across its sites)

Below is a look at ROC’s historical revenue over recent years - along with the step change in revenue that is now possible from last week’s deal.

Yes 14x... once fully rolled out - from just one deal:

Revenue from this deal will be received as and when the tech is activated at different customer sites, on an annual upfront basis, pro-rated to December 31st after activation.

So the ARR will build up to $9.1M until all the sites are rolled out...

But the revenue from this global Tier 1 retail customer could end up being much larger in the future.

At this point in time the deal only covers ~40% of this one new customer's “global store network”.

If this one customer decides to roll out ROC’s tech across the other 60% of its global stores, we can extrapolate to bring the total to $22.5M Annual Recurring Revenue to ROC.

(no guarantees of course - that number is complete speculation on our part, not a guarantee and not a forecast)

(Source)

And then there is the rest of ROC’s sales pipeline...

We estimate that ROC’s advanced stage sales pipeline currently sits at ~17,000 sites (after last week’s deal shifted some of the sites in the pipeline into paying sites).

So based on the assumption that ROC charges ~$3,500 per year, per site for its tech (source, ROC investor deck slide 10)...

ROC’s advanced stage pipeline now works out to be ~$60M in Annual Recurring Revenue...

So there still could be a lot more deals to come...

Of course like any sales pipeline, there’s no guarantee it all converts, and timing is always uncertain, plus these are just our very rough calcs.

ROC has now repeatedly shown it can convert the advanced stage opportunities in its pipeline into signed, paying deals...

As well as the Tier 1 global retailer signed up last week, ROC also counts Bunnings, Suncorp, a major Mexican retail bank and a major unnamed Australian bank as paying customers.

IF any more advanced stage opportunities come in then we can start to see ROC moving up the stage 4 (surging growth) of the “hockey stick growth chart” very quickly.

(‘hockey stick growth’ can describe a business’s rapid, exponential increase in revenue after a long period of slow, flat, or linear growth - forming a curve that resembles a hockey stick... )

No guarantees ROC will keep climbing into surging growth of course - this is still an early stage tech company and things can and do go wrong.

So how does the ASX value Annual Recurring Revenue like this?

Annual Recurring Revenue is a tech industry term for the yearly repeatable fee a customer pays to use a software or technology.

Tech investors like this metric as it provides a clear basis for assessing a company’s future financial performance.

On the ASX, SaaS or tech companies are generally valued at between 6x to 15x their Annual Recurring Revenue (ARR).

(some market darlings that keep delivering and growing even get a 100x multiple - like Pro Medicus - more on that one in a second)

So rough calculations on 6x to 15x ARR after last week’s deal would put ROC in a range somewhere between ~$54M to $135M market cap...

After today’s capital raise that’s a share price somewhere in the range of 28c and 70c.

This is not a price target though, it's just our rough “back of the napkin” calcs. There’s plenty of reasons ASX listed tech companies trade at different ARR multiples, there are also risks involved in small cap tech stocks.

Where that ARR multiple lands will likely depend on how much of that ~$60M advanced stage pipeline the market thinks ROC can convert, and how quickly customers roll out ROC’s technology across their sites.

All it takes is for a few investors to start running their own numbers, landing on a $20-30M ARR target and then applying a 10X multiple, and we could see ROC’s valuation move a lot higher than where it is today.

(again we are just throwing some numbers out here, it’s almost impossible to forecast with any surety how ROC will perform over coming months and years.)

That’s what we are seeing happen for AI imaging software company Pro Medicus.

Pro Medicus reported Annual Recurring revenues for FY25 of ~A$213M...

... and its market cap is $23BN.

That is an ARR multiple of ~100X...

The first big deal Pro Medicus signed was back in April 2016 with Mercy Health - a 7 year, A$21M deal. (source)

Not too dissimilar to the type of deal ROC’s signed last week.

Though we fully acknowledge that the two companies operate in different sectors, so we do not expect the market to value them on the same multiples.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

ASX market darling Pro Medicus is definitely an outlier (a great business with an even greater valuation) but it is a datapoint that demonstrates that valuations can go anywhere with these high growth, highly scalable tech companies...

How ROC’s technology works, and the Total Addressable Market

ROC developed its “Vision Artificial Intelligence” technology for giant companies to analyse and respond to in-store customer behaviours.

Basically this means using AI on live in-store camera footage to analyse customer behaviours, allowing the giant company to improve operations.

Or in a supermarket setting for “loss prevention”, providing a solution to a big problem the supermarket giants face at their self checkouts - theft.

(this is called ‘shrinkage’ in the retail industry - all up its estimated to cause a US$100BN plus annual loss to retailers - this impact on the bottom line is why retailers are so interested in ROC’s technology)

ROC’s tech is currently in use by TWO major, Australian household name companies - Suncorp in the banking sector and Bunnings in retail shopping.

And in the last ~4 months ROC signed a deal with a major Mexican retail bank AND

a new “Major Australian Retail Bank”.

Most of those deals are small relative to the monster deal ROC signed last week.

So ROC is already established and operating in two markets that we think are big enough to drive a substantial re-rate higher in ROC’s valuations:

(especially after last week’s news)

1. AI-driven loss prevention - The market ROC is targeting for here are retailers that have implemented self-checkout systems. ROC estimates these losses to be a ~$100BN per annum problem. ROC’s solution can help reduce this problem. (This is the part of the business last week’s deal relates to.)

AND

2. AI-enabled labour optimisation - ROC also sells workforce management tech. The global workforce management market is estimated to be US$8.38BN in 2025, growing to US$13.03BN by 2030.

After last week’s mega deal - see our note on that here, and then today’s $7M capital raise at 25c, we think now is the right time to refresh our ROC Investment Memo, as we expect the trajectory of the business to look a lot different now compared to when we first Invested in March 2025.

Below is our new ROC Investment Memo where we detail:

- What ROC does

- The macro theme for ROC

- Our ROC Big Bet

- What we want to see ROC achieve

- Why we are Invested in ROC

- The key risks to our Investment Thesis,

- Our Investment Plan

Investment Memo 2: RocketBoots (ASX:ROC)

Memo Opened: 24th December 2025

Shares Held: 6,999,000

What does ROC do?

RocketBoots (ASX:ROC) has developed “Vision Artificial Intelligence” technology for giant companies to analyse and respond to in-store customer behaviours.

ROC’s main customers are retail supermarkets and commercial banks to help optimise workforce management and alleviate loss prevention.

What is the macro theme behind ROC?

In-store shopping behaviours are moving to “autonomous”.

With self-checkout and self-ordering systems stores are putting the control back into the customers’ hands.

The challenge is that this has led to an increased amount of loss and theft for the retailers, and requires highly advanced monitoring software to sustain.

Our ROC Big Bet

“ROC re-rates to a $500M market cap by securing multiple large recurring contracts with retail clients and scaling up its business”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our ROC Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 9 Reasons We Invested in ROC and made it our Tech Pick of the Year

1. ROC has long term, paying enterprise customers.

Both Bunnings (large DIY goods retailer owned by Wesfarmers) and Suncorp (a bank owned by ANZ) are paying customers of ROC.

They have been customers since before ROC’s December 2021 IPO and continue to renew and expand their licence contracts 7+ years later.

More recently ROC added one of Mexico’s biggest retail banks to its customer list, a major unnamed Australian bank...

And then the big one - an unnamed “Tier-1 global retailer” - see next reason.

2. ROC signed the big “transformational deal” tech companies can take years to land

ROC signed a deal with a global Tier 1 retailer that once fully rolled out would 14x ROC’s current revenues.

The contract is for ~$9.1M in Annual Recurring Revenues per annum for five years once fully rolled out (and potentially longer).

The deal is for only 40% of that single customer's store network - so revenue from that one customer alone could get a lot bigger.

We think this single deal is a sort of “anchor” deal that marks an inflection point for ROC.

3. ROC has a ~$60M in potential Annual Recurring Revenues in its “advanced stage deal pipeline”

ROC recently confirmed that it has an advanced stage pipeline of 17,000 sites across grocery, retail and banking verticals from 14 customers.

At $3,500 per site per year, by our rough, basic calcs this represents over $60M in potential annual recurring revenue if ROC is able to convert into sales. (source, ROC investor deck slide 10)

(using a basic $3,500 per site per year times number of sites calc, ignoring bulk discounts and setup fees)

Of course, there is no guarantee these pipeline deals turn into revenues for ROC.

4. One large deal could multiply ROC’s current revenue

At a price point of ~$3,500 per store, one deal could be in the millions of dollars in recurring free cash flow.

We have already seen ROC land one of these with the ~$9.1M ARR deal - and we know there is the big advanced stage sales pipeline. One big additional deal could multiply ROC’s revenues.

These deals take a very long time to secure (as do most enterprise software deals).

ROC has shown that its enterprise customers tend to be incredibly “sticky” (stay on for a long time).

5. Partnership with Europe’s largest Point of Sale company: Gebit Solutions

Gebit Solutions sells self checkouts to supermarkets and retailers.

Gebit is the point of sale system for some of the largest supermarket retailers in Europe and Gebit supports an “out of the box integration” with ROC’s software.

High-synergy partners like Gebit help improve ROC’s reputation to enter the conversation with big retailers, despite ROC being a smaller player in the space.

6. Original founding team still in place, with experienced tech chairman at the helm

The original team that developed ROC’s technology in the early 2010s are still running the company (including the CEO and CTO).

This is a positive sign for tech startups when a long term founding team has been working on the product for 10+ years.

ROC also has a Chairman with experience in both private equity and tech enterprise sales.

ROC’s chairman Roy McKelvie is also the chairman of an education technology company called Pathify that he helped to scale and raise US$25M at a A$180M valuation.

7. Genuine AI and deep knowledge of how to apply AI to a specific problem

ROC’s AI and machine learning technology has been developed since 2010.

(well before AI became a big Investment theme)

Companies developing genuine AI with over a decade of development efforts AND internal knowledge on how to apply AI to solve a specific and real world problem are rare on the ASX.

And in our view are the best positioned to leverage and apply the rapid recent advances in AI technology and tools to their specific sector of expertise.

8. Vision capture technology valued in the US$250M-$500M range

In late 2022 a company called Trigo raised US$100M off the back of its grocery vision software.

In 2023 one of the largest companies in this space Everseen raised US$70M to advance a very similar technology.

Those large raises are evidence of the size of the opportunity in this space that investors are seeing.

If ROC is able to deliver more sales and capture market share, it could grow to the size of these larger competitors in the space.

9. ROC has a good capital structure and has protected it well.

We think ROC’s capital structure has been managed well - running the company lean, often with a low cash balance but buying enough time to get a mega deal signed (like the $9.1M ARR one).

ROC’s also managed to resist offering options in capital raises which means there will be very few shares on issue (199,313,384 shares after the December 2025 raise is completed).

The major shareholders are the original vendors of the technology and have proven to be sticky since the IPO.

The board and senior management represent ~44% of the shares on issue prior to this recent capital raise, which means they are very aligned to shareholders interests.

10. Institutional backing (which is rare to see in the small cap ASX tech space)

We like that ROC has attracted deep pocketed institutional investors to its register including the Bombora Special Investments Growth Fund, who is a substantial holder of ROC (over 5%).

Bombora has had a previous win with ROC’s chairman.

We also like that the most recent capital raise had “4 new institutions” come into the company.

The institutional ownership means ROC is de-risked from a future funding perspective because as long as ROC can deliver contract wins, these shareholders will be willing to bankroll the company’s future cap raises.

For us, it's an implicit de-risking of “funding risk” which is usually a very big risk for early stage tech companies on the ASX.

What do we want to see ROC do next?

Objective #1: Successfully rollout the $9.1M ARR deal

We want to see ROC roll out the $9.1M ARR deal that was recently signed.

Milestones

🔲 Rollout commenced

🔲 Rollout completed

🔲 First payment from deal received

Objective #2: New Sales from the advanced stage pipeline

We want to see ROC convert some of its ~17,000 site advanced-stage sales pipeline into new signed deals.

Milestones

🔲 New deal signed #1

🔲 New deal signed #2

🔲 New deal signed #3

Objective #3: Existing customer resigns OR expands current deal

We want to see ROC’s existing customers expand their current deals with ROC OR at the very least resign and continue with their current deals.

Milestones

🔲 Existing customer re-signs OR expands #1

🔲 Existing customer re-signs OR expands #2

What are the risks?

Sales and Delay Risk

ROC could lose key clients or not seal as many deals, hurting their revenue and share price.

Large organisations like the one’s ROC works with don’t tend to adopt new technology very often and the sales cycle can be long.

This feature of ROC’s customer base can cause delays in sales that drag out over a long time.

Marco factors in the market including a recession can cause a reduction in spending on new technology, affecting ROC’s ability to make sales.

Technology / Competition Risk

Technology is a competitive market. If ROC’s technology is deemed to be less valuable than other competitors, then it may fail to win sales.

Market risk

The tech part of the small cap market isn’t very well understood by ASX investors and so there is always a risk that the market fails to reward ROC regardless of any progress made.

Even if ROC does everything right from an operational standpoint, the market could always sell off or favour different sectors that it understands a lot better.

Funding Risk

ROC is still a small cap company that will require more capital to grow.

There is always a risk that that capital needs to come through capital raises - IF there are any delays in rolling out contracts OR in securing new deals ROC may need to tap the market for cash.

Other risks

ROC operates in a rapidly evolving AI vision market. Larger, better-funded competitors could emerge and challenge ROC’s position or put pressure on pricing.

The technology depends on in-store video and behavioural analytics. Changes in privacy regulations or public attitudes could increase compliance costs or limit deployment opportunities.

Currently, ROC’s revenue comes from a small number of key clients. Losing any one of these could have a significant financial impact.

Scaling from initial trials to broader rollouts will test ROC’s operational capabilities. Delays, integration challenges, or customer service issues could slow growth.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

We plan to hold a position in ROC for the next 3 to 5 years (and beyond) as it scales up its technology business.

We eventually may look to take some profits by selling up to ~20% of our holding (in line with our holding policy and escrow conditions) if the share price materially re-rates on the company successfully delivering on the key objectives listed above.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.