ILA enters defence against bioweapons and virus terrorism with new acquisition.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,766,666 ILA shares at the time of publishing this article. The Company has been engaged by ILA to share our commentary on the progress of our Investment in ILA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The world feels pretty uncertain right now.

Countries are bulking up their military and defence capabilities - drones, shipbuilding and critical military metals are all well publicized in the media.

What about bioweapons defence - deploying weaponised viruses as part of war?

During the Cold War, anthrax played a major role in the secret biological weapons programs for both the US and the Soviet Union.

The threat of biological warfare has unfortunately never really gone away.

To combat this threat, countries stockpile drugs to defend against biological warfare.

Island Pharmaceuticals (ASX:ILA) has just finalised its acquisition of a drug with potential to defend against bioweapons.

ILA’s new drug has already had over US$70M in US government funding support for clinical development against viruses that could be deployed as bioweapons in war scenarios.

We think, as part of the broader defence build up we are seeing globally, countries will soon start to increase their sourcing and stockpiling of bioweapon treatments and vaccines - like we are seeing with critical military metals.

ILA’s new acquisition puts the company into our “global uncertainty and defence build up” thematic portfolio - which covers gold, silver, military metals sourcing and stockpiling and growth of defence industrial bases.

ILA’s new drug has already been shown to be effective against ~20 other viruses in lab tests - many of which sit in the “weaponisable” category.

For weaponisable viruses like Marburg, Ebola and Zika, ILA’s new drug has shown (in animal studies) survival rates of up to 100% versus 0% survival in placebo... (more on this later).

The virus which ILA’s new drug has been tested the most in a clinical setting is Marburg virus - which is what ILA will be targeting as an effective treatment first...

(Not so) Fun Fact: During the Cold War, the Soviet Union's bioweapons program actively weaponised Marburg virus, producing it in large quantities and favoring it over Ebola due to its stability in weaponized form (source, source ).

Could Russia be at it again...?

(Source)

We hope not... but better be prepared just in case, right?

Marburg disease is classified as a Category A bioterrorism threat (the highest level threat) by the US government. (source)

(for Category A bioterrorism threats, governments around the world will generally maintain a stockpile of vaccines or treatments to quickly deploy. So we would assume if ILA can demonstrate its drug is effective against Marburg, the US government will take an interest)

Marburg is a highly dangerous virus that causes severe hemorrhagic fever in humans, with a fatality rate up to 88%.

There is no current vaccine or cure for Marburg.

ILA’s new drug is called Galidesivir, and it has already shown 100% Marburg survival rate for animals injected with it 24 and 48 hours after infection:

That’s a promising early start, but there is more work still to do.

The next step for ILA’s new drug is to prove efficacy in a larger trial with non-human primates.

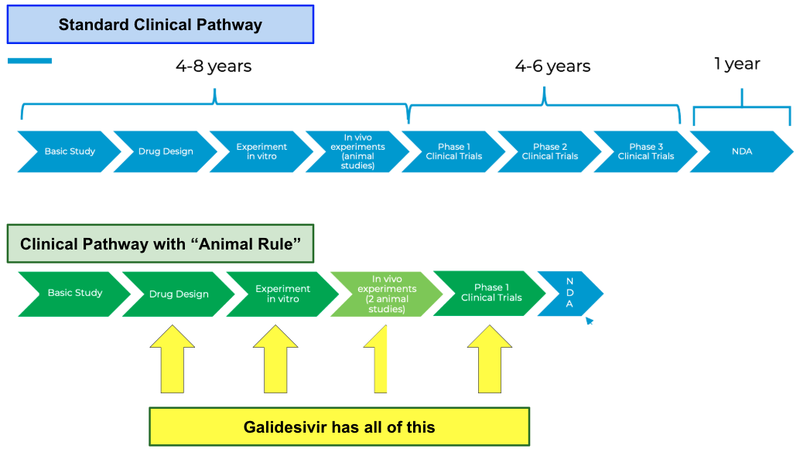

But before that, ILA will need the FDA’s blessing to use the “Animal Rule” regulatory pathway - which allows for drugs to be approved based on animal studies and human safety data alone.

The “Animal Rule” approvals process is reserved for viruses or diseases where running human clinical trials would be unethical or too risky...

Like Marburg where fatality rates are up to 88%...

IF ILA’s new drug is approved as eligible for approvals under the “animal rule” pathway - it could skip what is typically a 15+ year process of human clinical trials and get to FDA approvals in 12-18 months.

We should know if ILA’s new drug is eligible for the “Animal Rule” process fairly soon.

In a webinar yesterday, ILA’s management said that they could start engaging with the FDA as soon as the acquisition was completed.

(Source)

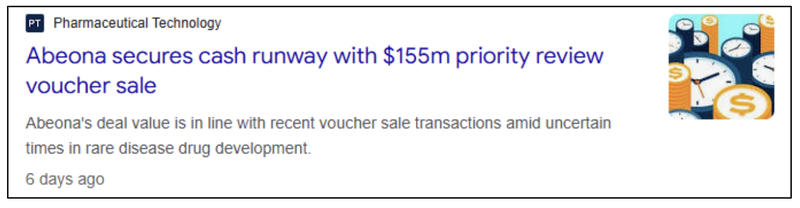

The big unlock of accelerated approvals for ILA’s new drug is that it would open the door for ILA being given a “Priority Review Voucher” (PRV).

(More on what a PRV is later in today’s note)

At a very high level, PRV’s are inherently valuable on their own because companies can sell them to other companies... on average, they are selling for US$100M (A$156M).

The most recent sale only a week ago was for US$155M (A$237M) - which is more than 6X ILA’s current market cap of $39M.

(Source)

Looks pretty good but of course ILA doesn't have one yet, and there is no guarantee they will be successful in getting one.

ILA’s new asset gives us a major catalyst to look forward to that is due before the end of the year (FDA’s decision on the Animal Rule), while we wait for ILA to complete the trial design for its dengue fever treatment.

ILA management ran a webinar yesterday to run through the new acquisition - where our key takeaways on what's next for ILA were:

- FIRST, Complete the Galidesivir acquisition (in the next 30 days)

- THEN, immediately look to set up a meeting with the FDA to identify ILA’s application of the “Animal Rule” to its Marburg studies

- WHILE, ILA is currently reviewing sites for the animal trials, looking to move into the clinic very quickly.

For those who missed it, here is the full webinar with ILA’s new chairman Jason Carroll and CEO David Foster:

Marburg disease is classified as a Category A bioterrorism threat by the US Government.

The fatality rate is up to 88% and there is no specific treatment or vaccine... yet.

ILA just executed an asset purchase agreement to acquire a drug with promising animal data on treating Marburg disease.

100% survival rate for animals injected with Galidesivir 24 and 48 hours after infection:

While this early data is promising, ILA will likely need to replicate it in a larger clinical trial in non-human primates in order to prove further efficacy.

This asset purchase follows ILA’s strategy of acquiring assets with existing clinical data and a potential for expedited approval path.

The US Government has spent over US$70M in developing this drug with the vendor, NASDAQ listed company BioCryst (NASDAQ:BCRX).

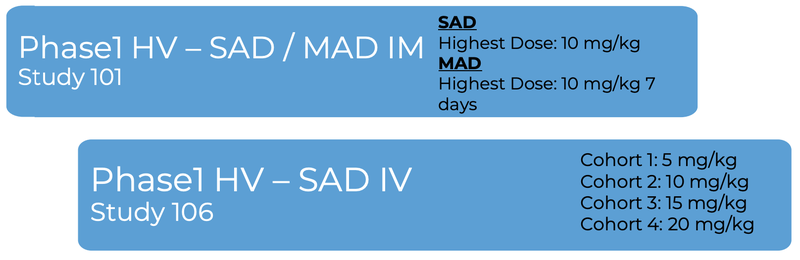

Also, the drug already has a bunch of Phase 1 safety data...

And a potential fast track pathway for ILA is through the “Animal Rule”.

If the FDA allows ILA to use the “Animal Rule” to fasttrack the approval of Galidesivir, it means that the company can effectively skip expensive Phase 2 and Phase 3 clinical trials in humans.

Why would the FDA do this?

Some conditions are considered so severe that it would not be ethical to undertake human efficacy studies, giving people the disease to test for efficacy would kill them.

(examples include smallpox and anthrax).

The Animal Rule could significantly shorten the time frame that ILA brings its drug to market, and realising value for shareholders.

If ILA’s drug is approved there are two ways it can derive value:

- Priority Review Voucher - these are “thank yous” that the US government grants to companies developing drugs of national importance. It speeds up the final FDA regulatory approval from 10 months to 6 months (which can be very valuable to big pharma companies with millions in sales on the line). They are transferable and can be sold for between US$100M - US$150M.

- Government Stockpiling - for Category A bioterrorism threats governments around the world will generally maintain a stockpile of vaccines or treatments to quickly deploy. These stockpiling contracts can be very lucrative. One example is Emergent BioSolutions Inc. (NYSE:EBS) securing a US$911M contract for the US National Stockpile (source).

As ILA Investors, we are still interested in the potential for ILA’s dengue fever drug ISLA-101, with the company recently publishing results from its Phase 2a/b trial.

You can read our full take on the results here ILA clinical trial achieves anti-dengue activity in humans

While ILA sets up for a larger clinical trial on dengue fever, the company can focus on developing Galidesivir in parallel...

Giving it one more shot on goal to achieve the coveted Priority Review Voucher.

Key takeaways from ILA’s webinar yesterday on the acquisition

Yesterday, new ILA Chairman Jason Carroll and CEO David Foster spoke to shareholders in a webinar.

At the start of the webinar Jason Carroll expressed that with every single new biotech investment there are some key first principle questions to ask:

- Does the drug work?

Answer: The drug has shown a great amount of efficacy in animal trials. 100% survival rate for non-human primates infected with the Marburg disease. Also, a significant reduction in the virus as well. (Also shown efficacy for Zika and Ebola) - Is the drug safe?

Answer: Yes, the drug has robust safety data from two phase 1 clinical trials testing the drug at different dosing levels - What does it cost to bring it to market?

Answer: If the “Animal Rule” is applied by the FDA, ILA could take the drug to market in a much quicker way compared to the standard drug development pathway. This is conditional on the FDA approval of the use of the Animal Rule (which is not guaranteed). - What’s the value of the product once it's there?

Answer: If ILA’s drug is approved for Marburg disease it could be eligible for a Priority Review Voucher (again this is not guaranteed). These sell for US$100M - US$150M. Also, ILA could sell the product to government stockpiles, where Anthrax vaccines have sold for US$1BN.

Other takeaways:

- Acquisition to close in the next 30 days.

- ILA is currently reviewing sites for the animal trials, looking to move into the clinic very quickly.

- As soon as ILA closes the acquisition, it will look to set up a meeting with the FDA to pursue the “Animal Rule”.

Our take: this is a key risk point for the company, if the FDA allows the Animal Rule AND allows ILA to use the existing animal and safety data, this would be a big de-risking factor. - On PRVs: PRVs are very valuable for large pharma companies looking to bring drugs to market and they will pay up to get them. ILA Chairman Jason Carroll mentioned that they are becoming less and less available, pushing their price up.

- Why did BioCryst sell the product? ILA’stake was that because the government funding dried up around COVID time BioCryst pivoted towards another indication (orphan drugs). BioCryst trials were successful for its rare disease drug and so it shelved the Galidesivir product.

History of Galidesivir and data

ILA will purchase Galidesivir from NASDAQ listed company BioCryst.

BioCryst first developed Galidesivir to combat Hepatitis C in the early 2010s, but quickly realised that the drug had a broad-spectrum effectiveness against a range of viral infections.

There is a broad spectrum of around 20 different RNA viruses that Galidesivir has shown efficacy against in lab studies:

Over the following ten years, BioCryst company conducted multiple animal trials to evaluate effectiveness against various viruses:

- Marburg Virus - 100% survival at initial dose 2dpi, 0% survival from the control

- Zika Virus - Viral load suppression initial dose 3dpi, 0% survival control.

- Ebola Virus - 100% survival initial dose 2dpi, 67% survival initial does 3dpi, 0% survival from control

BioCryst also conducted multiple Phase 1 safety trials in humans which demonstrated safety and that the drug was well tolerated across different doses.

While BioCryst ran the trials, they were predominantly funded by the US Government:

- US$47M contract with the National Institute of Allergy and Infectious Diseases (NIAID) and

- Up to US$39.1M from Biomedical Advanced Research and Development Authority (BARDA)

So there has already been nearly US$100M sunk into R&D costs to develop this drug, and ILA is picking it up for just US$500,000.

So what happened?

In 2020, in the midst of the COVID-19 pandemic, all infectious disease research was allocated to finding a COVID-19 cure (BioCryst even got $3M in funding to see if Galidesivir would work).

Around this time, BioCryst was getting very promising results from another clinical trial and dedicated all resources to developing rare disease therapeutics.

This left Galidesivir on the shelf, ready for a smaller, more nimble company like ILA to develop.

Over the 10+ years that BioCryst developed Galidesivir the drug has shown:

- A very strong safety profile

- Efficacy in vitro against 20 different RNA viruses

- Efficacy against Malburg, Zika and Ebola virus in animals

It is effectively a “de-risked” acquisition by ILA, that gives the company a second ‘shot on goal’ to develop an antiviral drug alongside its ISLA-101 product for dengue fever.

If either Galidesivir or ISLA-101 is approved by the FDA for use against highly infectious disease it could be eligible for a Priority Review Voucher.

These PRVs are like a “thank you” from the FDA for bringing a drug to market and are transferrable - generally selling between US$100M to US$150M each.

There is still a long way for ILA to get there, and a lot of risks to be aware of, including regulatory risks (will the FDA approve the animal pathway?) and efficacy risk (can ILA repeat its results in a larger clinical trial?).

How can ILA fast track approvals through the “Animal Rule”?

As we’ve noted above, for deadly infectious diseases, the FDA will allow companies to prove the efficacy of their drug in animal trials, using the “Animal Rule”.

This drastically reduces the approval timelines because no clinical efficacy data on humans is needed.

Before any drug is approved by the FDA there are two key things that any company will need to first prove:

- Efficacy - Does it work?

- Safety - Is it safe for human consumption?

Generally, the company will undertake rigorous trials in order to gather clinical data that supports whether their drug is safe and effective.

However, there are some conditions that are so severe that ‘it would not be ethical’ to undertake human efficacy studies.

These are incredibly deadly infectious diseases like smallpox or anthrax.

This is where the “Animal Rule” comes in.

For the Animal Rule to take effect there generally needs to be “more than one” clinical trial on non-human primates.

Because the original owners BioCryst have conducted animal trials for Marburg disease, and collected a bunch of human safety data, we think that it is likely that the FDA will factor in this data when ILA looks to implement the “Animal Rule” for fast track approvals.

ILA will next consult with the FDA to see how it can use the Animal Rule to fast track the approval of this drug.

(there is no guarantee that ILA is able to use the BioCryst data for the Animal Rule however)

With more strong data on Galidesivir in non-human primates, the FDA may grant it a direct pathway to a New Drug Application without doing human trials.

This would be a big cost saving for ILA - particularly because a lot of the safety data has been provided by BioCryst in multiple Phase 1 trials already.

(but again, not guaranteed)

Marburg is a severe disease with a fatality rate of up to 88% - it also has no specific treatment or vaccine.

The Animal Rule has been used to approve drugs for infectious diseases as “countermeasures” against bioterrorism, including drugs like Levaquin, Raxibacumab, CIPRO, Avelox, Anthim, TPOXX, Tembexa.

(you can find a full list of drugs approved under the Animal Rule here).

ILA could also become a biodefense “stockpiling” play

The big upside is that Galidesivir could make ILA a “stockpiling play”.

This is where the drug is of such interest and importance to public health that governments have a strong interest in stockpiling a reserve “in case of emergency”.

The best way to think about it is if we could have foreseen a big COVID outbreak in 2020 and the vaccine already existed, governments could have used their stockpile to prevent the spread of the outbreak.

This would have avoided all of the disruptions caused by the lockdowns and vaccine rollout.

OR even worse, in the event a bioweapon is used in war...

Governments wouldn’t be scrambling for a defensive vaccine/treatment.

Here are some government stockpiling deals that have been awarded in the last few years:

- Emergent BioSolutions up to $911 million through 2021 for BioThrax (the only FDA anthrax vaccine). BARDA also awarded Emergent $100 million for BioThrax.

- Bavarian Nordic- $120million for JYNNEOS (smallpox and mpox vaccine) in 2023

- Bavarian Nordic- $140million for JYNNEOS in 2024; BARDA also awarded them $63 million

- Bavarian Nordic- $140million for JYNNEOS in 2025

More on Priority Review Vouchers

A priority review voucher is a “reward” for biotech companies that develop drugs that the FDA are targeting... in particular:

- Neglected tropical diseases

- Rare pediatric diseases

- Medical countermeasures (e.g. for bioterrorism or pandemics)

FDA Priority Review Vouchers can either be used for the specific drug that the company is seeking to be approved OR be used on the next drug that the company is looking to develop (like a bonus ‘thank you’ for getting approved).

The priority review reduces the review time frame from 10 months down to 6 months.

The reason PRVs are so valuable is because:

- A drug can get put into market a lot quicker than the traditional commercialisation strategy. Time is money.

- Once a company is granted PRV status for a drug, that status can be transferred to another product of choice without having to qualify for a priority review.

That time saving is obviously valuable for companies who can get into market ~4 months earlier (versus going through the priority review process).

Particularly to big pharma, where new drugs can sell for billions a year and there is a 7-year exclusivity timeframe before generics hit the market.

PRVs have sold for as high as US$350M (source).

ILA is hoping to fast track approvals and secure a PRV for Galidesivir because of:

- The existing safety and pharmacogenetic data conducted in two Phase 1 clinical trials by BioCryst

- The “Animal Rule” which allows effective drugs to be approved just from animal trials.

These two factors may significantly shorten the timeframe for ILA to secure FDA approval and the coveted PRV.

A couple of weeks ago the FDA Commissioner highlighted the potential for new Priority Vouchers to be granted to “companies supporting the US National Interest”.

(Source)

There were four broad categories that were identified by the FDA as “US National Interest”:

- Addressing a health crisis in the U.S.

- Delivering more innovative cures for the American people.

- Addressing unmet public health needs.

- Increasing domestic drug manufacturing as a national security issue.

While these categories don’t necessarily give a specific direction to the market as to which types of drugs will be eligible, the prize is big.

However, the possibility that ILA is eligible for two different Priority Vouchers is a big prize worth chasing.

So, what did ILA pay for Galidesivir?

Terms of the deal

In July last year, ILA signed an option agreement to purchase Galidesivir.

Now ILA is moving forward with the acquisition.

The key terms include:

- Payment of US$50,000 for the option to acquire

- Payment upfront of US$500,000 upon exercising the option to acquire all rights, title, and interest in the Galidesivir program

- US$500,000 upon completion of Phase 2 clinical trial

- US$1M upon approval of New Drug Application in the US or equivalent

- US$1.5M upon Animal Rule approval where no Phase 2 is required

- Tiered royalties of 5–10% of Net Sales

- 25% of proceeds from sale of any Priority Review Voucher awarded due to FDA approval of the acquired program

So the only upfront cost for ILA is US$500,000 and then milestone payments as the company develops the asset through FDA approvals.

And then a 25% cut of any potential PRV transaction at a later date.

What is the plan for ILA’s dengue fever treatment?

ILA is also developing a drug to use as a preventative against dengue fever.

Since our last note, ILA has published more data on the ISLA-101 clinical trial for dengue fever.

Our key takeaways were that:

ILA reported “meaningful reduction in both viremia (viral load) and symptoms in preventative cohort”

(meaning good for a pill that you take if you are in a high risk dengue location, so IN THE EVENT THAT you get dengue fever it reduces the symptoms - a huge market)

And that “Treatment cohort demonstrated signals of drug effect”

(meaning good early signs for a pill you would take if you have ALREADY CONTRACTED dengue fever, to reduce the symptoms)

You can read our full take on the results here ILA clinical trial achieves anti-dengue activity in humans

Now that the trial is complete ILA will need to decide how it proceeds with advancing the asset.

It is likely that over the next few months the company will have several meetings with the FDA to decide on the size and protocol for its next trial.

For the next trial we are hoping to see whether ILA’s dengue fever drug is effective “in the wild”.

What’s next for ILA?

Animal trial for Marburg Disease

Now that ILA has completed the acquisition of Galidesivir, we want to see the company work with the FDA to develop an animal trial to determine efficacy on Marburg Disease.

🔲 FDA meetings to determine the application of the Animal Rule.

🔲 Clinical trial design completed

🔲 Funding

🔲 Clinical trial starts

🔲 Clinical trial completed

🔲 Clinical trial results

We think this should be a fairly quick process assuming ILA gets a favourable FDA Animal Rule outcome and it doesn't need to run trials in humans.

Phase 2/3 clinical trial design and completion for dengue fever

Now that the phase 2a/2b results are unblinded, we want to see ILA start designing its next trial for dengue fever.

The next stage will be a meeting with the FDA (these generally take about 4-6 months) and then a clinical trial design for the next phase of trials.

Here are the milestones we will be tracking:

🔲 FDA meetings to determine endpoints for the trial

🔲 Clinical trial design completed

🔲 Clinical trial starts

🔲 Clinical trial completed

🔲 Clinical trial results

What are the risks?

Galidesivir (Marburg Disease)

The primary risk for ILA is regulatory uncertainty.

While the FDA’s Animal Rule provides a potential fast-track pathway for Galidesivir, it is not guaranteed.

ILA must meet with the FDA to determine if the existing non-human primate efficacy data and Phase 1 human safety data from BioCryst are sufficient to proceed.

If not, the company may be required to conduct new studies, increasing both costs and timelines.

The second risk for ILA is efficacy risk, although there is some good early stage data, ILA will need to prove in a larger clinical trial that Galidesivir is effective.

The third risk is commercialisation risk, even with approval, there is no certainty that ILA will receive a Priority Review Voucher or secure government stockpiling contracts.

The fourth risk is competition risk, there are other drugs being developed for Marburg, and if they make it to market first, it may affect the commercial potential of Galidesivir.

ISLA-101 (dengue fever)

While the initial data from ILA’s Phase 2a clinical trial showed that ISLA-101 was effective as a preventative, ILA will still need to conduct a larger clinical trial to get the drug approved by the FDA.

The first risk is regulatory risk, the FDA may say to ILA that it will need to conduct a Phase 2 (rather than a Phase 3) trial in order to develop more data for approvals.

The second risk is financing risk, the next clinical trial may be expensive, in particular because ILA will likely need to prove that its drug works on dengue fever “in the wild”.

Setting up clinical trials for dengue fever may be challenging as dengue fever often occurs in tropical locations.

The third risk is efficacy risk, there is no guarantee that even with a clinical trial that ILA is able to prove that its drug is effective at preventing dengue fever - although there have been promising results from the Phase 2a - these will need to be repeated in a bigger trial and in the wild.

Our ILA Investment Memo:

You can read our ILA Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our ILA Investment Memo covers:

- What does ILA do?

- The macro theme for ILA

- Our ILA Big Bet

- What we want to see ILA achieve

- Why we are Invested in ILA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.