HVY: Transformational new deal just announced? Producing by end of this year?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,745,000 HVY Shares, 75,000 HVY options and $75,000 in the HVY Tranche 1 royalty agreement at the time of publishing this article. The Company has been engaged by HVY to share our commentary on the progress of our Investment in HVY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

We think 2026 is going to see an “every commodity” rally.

It’s our view that in this rally, attention and capital will start flowing into companies with advanced-stage mining projects.

Those with a line of sight to production and revenues...

(who can make the most of an “every commodity” rally).

We Invested in Heavy Minerals (ASX:HVY) in 2023 for its development stage Port Gregory garnet project in WA, right next door to the biggest garnet producer in the world.

Garnet is an important industrial material used in high-precision manufacturing, global shipbuilding, defence infrastructure, and heavy engineering.

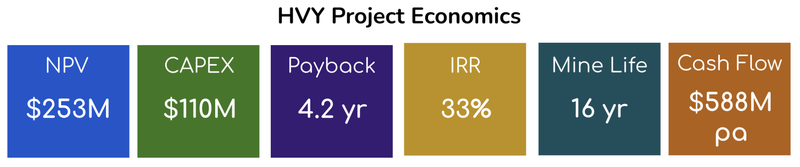

HVY’s original WA project’s scoping study returned a Net Present Value of $253M - a decent size project for a company currently capped at just $39M...

... but more on this in a second.

Today, $39M capped HVY just announced a deal that could make the company a revenue generating garnet producer before the end of this year.

Just in time for an “every commodity” bull run?

(We hope so... HVY is currently one of our largest holdings.)

HVY has just executed a binding agreement to:

- Take the garnet rich tailings (waste) from a producing copper-gold mine in South Australia (Hillgrove Resources)

- process the tailings,

- Extract valuable industrial use Hardrock Almandine Garnet, and;

- sell that garnet for cash.

And, HVY says it could be in production by the end of this year ...

By our VERY rough calcs (more detail + assumptions below) HVY could be generating up to ~$31.1M in gross revenue for the first 3 years.

Followed by up to ~$62.2M per year after that...

All for an estimated plant cost of $25M to $30M.

(plus operating costs and payments to the copper mine owner.)

Please note this is just our very rough calcs to demonstrate potential gross revenue and is by no means a forecast, more details on all of our assumptions and how we reached these numbers below - there could be the usual tailings processing challenges ahead and there’s no guarantee that HVY will generate any revenue.

HVY wants to start generating cash asap from this project, and use these proceeds to help fund the CAPEX of its original and much bigger Port Gregory Project.

Doing it this way minimises dilution for existing shareholders, which is a theme we have consistently seen from HVY since first Investing back in 2023.

HVY has raised most of their funds over the last 2 years via a non-dilutive royalty sale agreement.

(HVY does not like issuing new shares, which we believe has helped the HVY share price slowly grind upwards over the last two years, even with not much newsflow).

In today’s announcement, HVY said they will keep this non-dilutive funding culture going and will raise this $25M to $30M “via a combination of debt funding, pre-sales and Royalties”.

(HVY says it is already “advanced in its funding discussions with several interested parties” - with potential pre-sale funding out of the US or the EU...)

A significant amount of work has gone into this tailings re-processing deal already - over two years of negotiations, test work, flowsheet design work, plant designs, capital estimation, financial modelling, logistics, distribution and contract negotiations.

(and CAPEX financing discussions are happening right now...)

HVY has even locked in its plant design and has started planning where the plant would plug into Hillgrove's existing processing circuit:

(source - HVY announcement)

Why so much work already done BEFORE the deal got announced?

For a deal like this, you wouldn’t want to make a commitment until you knew a LOT about what it would take to build, how much revenue it could generate and how long it would take...

According to HVY it could be producing garnet by the end of 2026.

And we should get a better idea of the project’s economics in a few weeks - HVY said today that “The Company expects to release the modelling results in the coming weeks”

HVY also said that the long awaited PFS on their original and even bigger project is expected in the coming weeks too.

So a lot of news is coming soon from HVY.

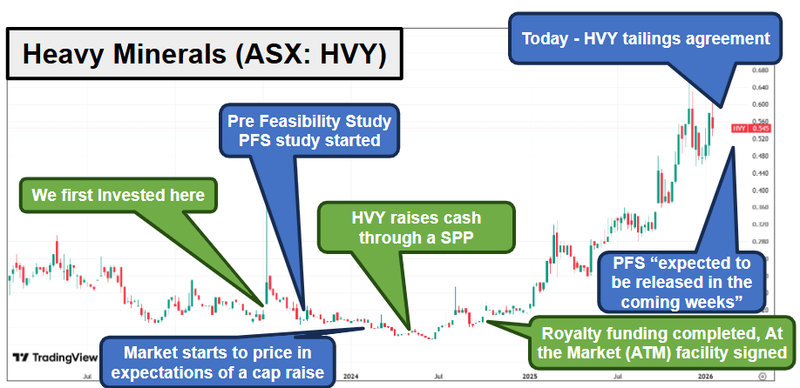

HVY has been relatively quiet (but busy it seems) over the last 18 months, but if there was ever a time to deliver a flurry of announcements, HVY has timed it well into a very buoyant commodities market.

(and even while HVY is quiet, the share price still likes to go up, helped along by HVY keeping their capital structure very tight with non-dilutive fundraisings instead of share placements)

Why we like HVY’s new deal

- HVY is partnering with an established copper producer capped at ~$174M - this producing company is letting HVY onto their mine site and to plug into their processing plant - a strong show of confidence in HVY’s ability to execute.

- HVY has already done most of the technical work - Bulk Sampling, Metallurgy and flowsheet work is all done. The process plant is designed. End-product testwork is complete and distribution, financing discussions are underway.

- HVY could produce $31.1M to $62.2M per year gross revenue from just $25M to $30M CAPEX (our rough gross revenue calcs, full details below)

- Simple, predictable permitting process - HVY is plugging into Hillgrove’s existing processing circuit, so there shouldn’t be any major permitting issues getting HVY’s plant built.

- Quick timeline to production subject to funding - HVY expects to be in production ~8-10 months after making a Final Investment Decision on the project.

- HVY’s board is incentivised for “commercial production” before 31 December. (source)

- HVY can scale up to meet demand - HVY is planning to produce up to ~50ktpa of waterjet garnet (~10% of global demand) and eventually aim to increase capacity to 100ktpa. This means, HVY can scale up/scale down based on market demand for its product.

- More newsflow (and hopefully revenue) while we wait for progress on HVY’s Port Gregory Project.

How does today’s deal make HVY a near term garnet producer?

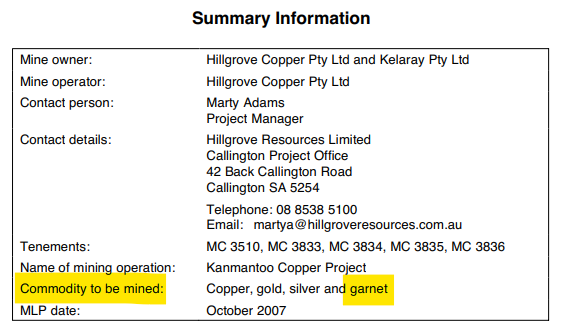

HVY has done a deal with $177M capped Hillgrove Resources, who produces 12,000 tonnes of copper per year in South Australia.

It turns out the tailings (waste material) from Hillgrove's copper mine plan is full of... garnet.

Garnet is an important industrial material used in high-precision manufacturing, global shipbuilding, defence infrastructure, and heavy engineering.

According to the South Australian government, some of the Hillgrove’s host rock had >12% garnet grades (source).

(Source)

Hillgrove even had garnet as one of the commodities that would be mined in their mining lease proposals from back in 2007. (source)

(source)

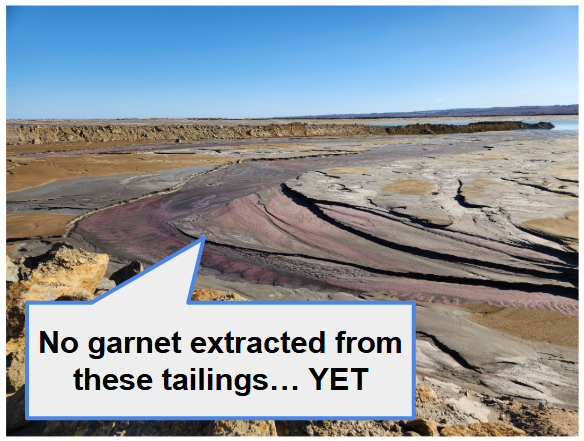

Since then, though, no one has had a crack at recovering the garnet...

Enter HVY...

While Hillgrove is focused on copper, HVY as a company is fully focused on garnet, has garnet knowledge and would know the industry inside and out having worked on its garnet asset for years.

HVY is a natural partner to extract and sell the valuable garnet from Hillgrove’s mine tailings.

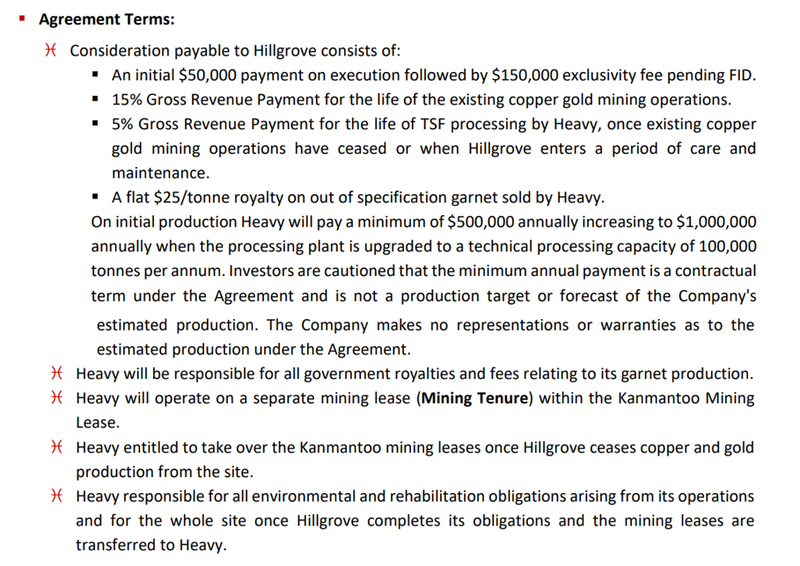

HVY’s deal with Hillgrove means HVY pays ~$200k to Hillgrove, plus 15% of gross revenue (from garnet sales) made while the copper mine is still operating, then 5% of revenue (from garnet sales) after the mine shuts down.

(Once HVY gets into production, these 5% and 15% payments to Hillgrove have a minimum floor of $500k annually increasing to minimum $1M annually once HVY’s processing plan is upgraded to a technical processing capacity of 100,000 tonnes per annum.)

How does HVY continue producing garnet after the copper mine has shut down?

From all of the already processed material sitting in Hillgrove’s tailings storage facility.

(Who knows, maybe there are decades of production potential in those tailings)

(source)

It's a win-win for both companies...

HVY becomes a revenue generating garnet producer without all of the CAPEX and mining operating costs associated with building a resources project completely from scratch.

Hillgrove gets to monetise a resource that was going untouched until HVY entered the picture.

(Source - read the HVY deal announcement)

Speaking of production targets... below is our very rough calculation of total gross revenue HVY could generate...

Caution - before you go on to read these numbers, we are operating with limited information and are completely speculating here.

HVY is still at a very early stage and has not generated any revenue yet. There’s no guarantee HVY will get anywhere near the below numbers.

How HVY could generate $31.1m to $62.2M in revenues per annum

OK lets try and figure out what kind of cash HVY could spin off with this new project.

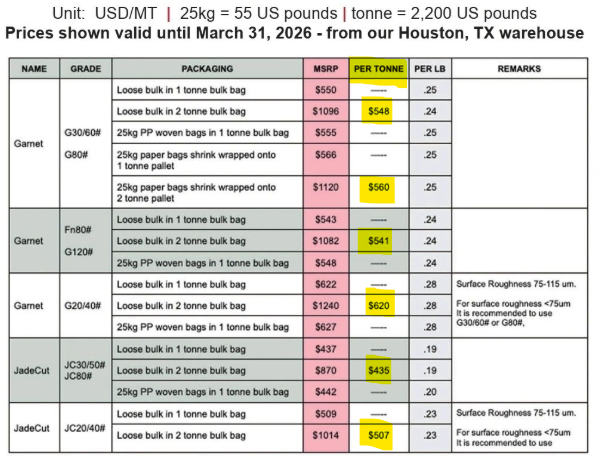

According to this post, garnet prices range between US$435 to US$620 per tonne:

(source)

Even taking the LOWEST price per tonne of US$435 = ~$630 AUD per tonne.

(for the simplicity of this basic calc just to show simple total gross revenue, let’s assume full capacity to 50,000tpa from day 1, in reality it will likely take time to get the plant humming smoothly and up to this capacity)

50,000 tonnes per annum x $630 per tonne = $31.1M gross revenue for the first 3 years.

Then after 3 years, 100,000 tonnes per annum x $630 = $62.2M gross revenue per year after that for the life of mine.

Even taking out Hillgrove’s 5% to 15% cut (get it? Garnet is used for water jet cutting? never mind), the rough numbers look very good for a $39M capped company like HVY.

Caution - this is a VERY rough calc, net revenue to HVY will be either 15% or 5% gross revenue payment to Hillgrove, the cost to produce, plus any fees paid to distributors - also garnet prices may go up OR down over life of mine - this rough calculation is for illustration purposes of the general scale of the project and should not be relied on.

The big variable will be the “cost to produce” which should be minimal given HVY doesn't have to actually mine anything...

However processing tailings can be notoriously tricky - so it's not completely without risk.

Garnet is an industrial use product that must meet end user specifications and requirements (which is why HVY spent a lot of time doing sample testing), and meeting those needs consistently might be challenging - we won’t know until HVY tries.

HVY explicitly said in today’s announcement the “Company expects to release the modelling results in the coming weeks.”

So we should have firmer, more robust calculations than our rough, back of the napkin calculation very soon...

The next big thing for HVY to do is find the A$25M to A$30M to build its plant...

In today’s announcement HVY said they will raise this $25M to $30M “via a combination of debt funding, pre-sales and royalties”.

We like HVY’s commitment to non-dilutive funding, as we saw with their chosen funding pathway for the last 2 years using a non-dilutive royalty agreement versus equity raises - which is why we think the HVY share price generally moves upwards - more on this in a second.

HVY says it is already “advanced in its funding discussions with several interested parties”.

So we are hoping to see some updates on this soon too, in HVY’s “2026 year of newsflow".

Four catalysts we want to see HVY deliver in 2026

HVY has been a bit sparse with newsflow over the last 12 months, but the share price keeps going up so investors are happy.

The newsflow should start to increase now, as we now have four bits of major news to look forward to:

- Funding deals for the $25-30M CAPEX needed for the tailings processing plant.

- Offtakes/distribution deals for the industrial garnet end product.

- Economic modelling on the tailings processing deal with Hillgrove Resources, and

- Of course, the Pre Feasibility Study (PFS) for the bigger Port Gregory garnet project.

Two of those are expected “in the coming weeks”.

On that Pre Feasibility Study (PFS) for HVY’s much larger project

The next news we (and the market) were actually expecting from HVY was the long-awaited Pre-Feasibility Study on the economics of its original Port Gregory garnet project.

HVY’s initial scoping study for Port Gregory indicated a low CAPEX of $110M against an after tax Net Present Value (NPV) of $253M, a payback period of 4.2 years, an after tax Internal Rate of Return (IRR) of 33% and Free Cash Flow of $588M across a 16 mine life.

HVY now says the PFS is to be released in the coming weeks, and management is incentivised to get CAPEX down and NPV up - see AGM resolution 6 here.

(Source)

How about funding for the A$25-30M tailings plant - HVY to pull off another non-dilutive raise?

So HVY could be about to become a revenue generating Waterjet Almandine Garnet Producer...

... After an ~8-10 month lead time to get everything up and running, and as we said above HVY wants to get into production by the end of the year, and the board is incentivised to make that happen.

(“Show me the incentive and I'll show you the outcome”: Charlie Munger)

The next major catalyst for HVY will be to raise $25M to $30M, build its 50ktpa plant and plug it into Hillgrove’s processing circuit.

If there is one thing HVY’s managed to do well is raise funds without diluting HVY’s cap structure.

(which is why we think HVY’s share price performs so well, even with not much news)

Over recent years (since we Invested) HVY hasn’t offered the market any discounted capital raises with oppies like most other companies do (especially during the bear market)...

HVY has taken a much harder route of a non-dilutive ~$2M “royalty sale agreement”

(which they completed in August 2024, a second $2M is currently in progress)

A “royalty agreement” is a non-dilutive funding method for early stage resource companies.

In HVY’s case, it means the company sells down a tiny percentage of the future mine revenue (1.05%) in return for a non-dilutive cash injection now.

HVY pulled off what was actually the “the First Syndicated Non-Dilutive Pre-Paid Royalty to be done in Australia”.

It took many hard months but it helped HVY avoid a big dilutive capital raise.

We think HVY’s bobbing, weaving and avoiding a “bear market cap raise sucker punch” is why the company’s share price is trading up where it is today.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now with the market roaring... HVY could find it a lot easier to raise capital...

Especially now with news to come from its Port Gregory project AND the new deal announced today.

IF HVY can pull off non dilutive funding to get the tailings reprocessing deal up and running...

Then use the cash generated from the tailings processing deal to fund Port Gregory CAPEX...

We could see HVY complete one of the most epic “threading of the needle” to advance a mining project without blowing up a company’s capital structure...

It’s still very early days but with HVY being one of our biggest positions we are hoping it all comes off.

Reminder: 13 Reasons why we are Invested in HVY:

It’s been a while since we wrote about our Investment in HVY - here is a reminder and update on the reasons we Invested:

These reasons were first published on 14th July 2023. We have put in a small update on some of the reasons we think have evolved since then:

1. Tiny market cap after lots of progress - When we initially Invested in HVY it was capped at just $6M with a scoping study already completed for its project.

Update: HVY is now capped at ~$39M and as mentioned earlier there are a fair few catalysts brewing for HVY right now.

2. Tight structure low shares on issue (SOI) - When we initially Invested HVY had ~55 million shares and ~18 million options on issue. Prior to our Investment, the top 5 shareholders held ~75% of these shares

Update: HVY has managed to protect its capital structure extremely well during this time. HVY still has only ~69M shares on issue.

3. Management skin in game - Before our Investment, HVY directors held ~11.6% of the company, with chairman Adam Schofield holding 7.7% himself.

Update: HVY directors now hold ~10% of the company, with CEO Adam Schofield holding ~6.0% himself. Management are also incentivised with performance rights vesting based on market cap milestones and “commercial production” hurdles.

4. Garnet is an important niche material - Garnet is leveraged to big industries like the maritime and aerospace industries to allow for rust removal, industrial cutting and anti-corrosive paint to be applied to surfaces. It cannot be easily replaced.

5. Favourable long-term pricing environment for garnet - Supply side is decreasing with Indian garnet production being banned. On the demand side bans are being considered for garnet alternatives (copper slag/silica) due to ESG concerns. We expect to see demand outstrip supply in the coming years leading to higher prices.

Update: We have seen a significant uplift in the garnet price since our last note, with pricing in the US now around US$431 to US$620 per tonne.'

6. US is spending ~US$40BN on upgrading old rusty bridges - The US has budgeted US$40BN of new funding for bridge repair, replacement, and rehabilitation. We expect this to increase demand for garnet as a sandblasting product.

Update: This reason strengthened last year with the US Trump Administration having singled out rusting old US navy ships as being a big problem... (we mentioned this in our prior note).

7. Quick, viable pathway to becoming key garnet supplier - HVY’s project has an established JORC resource, a completed scoping study and is just about to start a pre-feasibility study. HVY is targeting first production in 2026.

Update: Well its 2026 now - while Port Gregory timelines have slipped, HVY is still targeting first production this year, now from its tailings reprocessing project.

8. Close proximity to two producing garnet projects - HVY’s projects sits next door to the GMA mine which supplies ~35% of the world’s almandine Garnet and Resource and Development Group’s newly constructed mine.

9. Neighbour RDG trading at a ~$220M enterprise value - Resource and Development Group next door is capped at ~$150M and has an enterprise value close to ~$220M. RDG is also ~65% owned by $13BN Mineral Resources.

Update: RDG entered voluntary administration in July 2025. MinRes then bought the garnet mine 100%. So HVY’s neighbour is now $12.3BN MinRes.

10. Project economics stack up, plenty of room for upside - HVY’s scoping study showed an after-tax project Net Present Value (NPV) of $253M, a payback period of 4.2 years, and an after tax Internal Rate of Return (IRR) of 33%. The project CAPEX is also relatively modest at $110M.

Update: We should get updated project economics in the coming weeks from HVY when the Pre Feasibility Study (PFS) drops.

11. Upside to increase garnet resource - HVY could double its existing JORC resource with more drilling to the north/south of its existing JORC resource and at its Red Hill project where it has a 90-150Mt (4.1 to 5.4% THM) exploration target.

12. Project financing support from Dutch Export Credit Agency - HVY recently received a “Letter of Support” for project funding from Atradius - the Dutch Export Credit Agency.

13. ESG focus and Australian project attractive to European/US garnet buyers - Western companies are seeking sustainably produced materials, which will increase interest in sustainable produced garnet, especially given the cloud surrounding garnet that was previously produced in India

Ultimately, we hope that the above reasons combine to deliver our Big Bet which is as follows:

Our “Big Bet” for HVY

“We want to see 20x return as HVY moves into production by 2026 and become a profitable garnet mine”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done and many risks involved - some of which we list below. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

HVY’s WA project is next door to the world’s biggest garnet mine

HVY’s Port Gregory Project in WA sits right next to two operating garnet mines.

Including the world’s biggest, previously owned by a private group - GMA Garnet (the world’s largest garnet producer).

For that company The Australian reported that the previous owners wanted around $500M when it was up for sale in November 2023 (source).

GMA Garnet Group was later sold to Jebsen & Jessen Group in April 2024, for an amount that was not publicly disclosed. GMA’s net assets were reported at $280 million as of December 2024, following adjustments after the ownership change.

The second is the Lucky Bay Garnet Mine now owned by the $12.3BN Mineral Resources (ASX: MIN).

HVY’s current Enterprise Value is ~$39M.

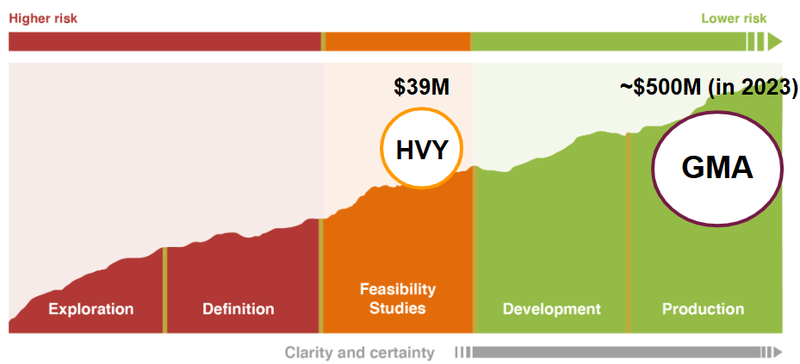

Here is where HVY sits relative to GMA on the “mining lifecycle” chart:

As HVY moves out of the feasibility stage and into development/production we are hoping the valuation gap between the company and the bigger players in the area can close.

Especially considering the A$253M NPV HVY’s project has.

What’s next for HVY?

🔄 Tailings Reprocessing deal with Hillgrove Resources

After today’s announcement, we are looking forward to HVY delivering these four milestones:

- Secure CAPEX funding for the project (A$25-30M)

- Distribution/offtake deals for the end product

- Final Investment Decision

- Start production

- Cash flow generation

🔄 Complete Pre Feasibility Study (PFS) for Port Gregory

In today’s update, HVY said that the PFS “is expected to be released in the coming weeks”.

We are looking forward to the PFS coming out, mainly because it will give potential offtake partners and project financiers more certainty around the cost estimates/timelines of HVY’s project.

We also think it gives HVY a chance to show the market its project economics are strong based on studies with a higher level of detail.

HVY’s 2022 scoping study demonstrated:

- An after-tax project Net Present Value (NPV) of $253M

- A payback period of 4.2 years,

- An after tax Internal Rate of Return (IRR) of 33%

- And a relatively modest project CAPEX of $110M

Since then, HVY has mentioned there is potential for a “significant reduction” in its project’s CAPEX by using an alternate mineral processing plant.

Lower CAPEX should mean better overall economics... which we hope makes HVY’s project more financeable...

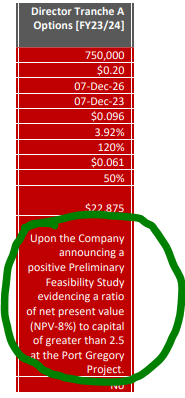

We note that one of the director performance options vesting conditions is to see the NPV/CAPEX ratio go above 2.5x when the PFS comes out.

Based on the scoping study numbers, the ratio is currently at ~2.3x.

We are hoping the alternate processing plant designs are enough to get that ratio above 2.5x, which again will highlight the strength of HVY’s project economics.

Higher NPV for less CAPEX is a big win when it comes to study results... it means far less upfront investment is required to make a larger return in the long run.

(Source)

🔄 Mining Lease Application

HVY also mentioned in the previous quarterly (September 2025), that its mining lease application was expected to be lodged in Q1 (this quarter).

Heavy Minerals

ASX:HVY

What are the risks?

After today’s announcement, the main risk for HVY is “financing risk”.

As at 30 September 2025 HVY had ~$111K cash in the bank.

We should get HVY’s quarterly cash balance at some point this week.

At the moment the company is mostly being funded by an At-the-Market facility that was put into place back in August 2024 (source), and royalty agreements with investors.

The “At-The-Market” (ATM) facility means HVY can raise small amounts of capital at its discretion, giving it breathing room to get a bigger funding deal tucked away.

HVY needs to find $25-30M to get its tailings processing deal up and running & multiples of that to develop its garnet project in WA.

HVY wants to fund this $25-30M CAPEX via a combination of debt funding, pre-sales and Royalties, and says it’s in advanced discussions with several interested parties.

There is no guarantee these funds are secured, and if they are, the terms could dictate how much dilution there will be for existing shareholders.

Funding Risk

The small cap funding environment is particularly difficult, and it is possible that HVY cannot secure the funding it needs through royalty agreements or otherwise to continue its operations.

Small caps need money to grow, and capital raises are often needed, which can cause dilution to shareholders and these raises can be conducted at a discount to market prices.

Source: HVY Investment Memo, June 2023. What could go wrong?

The other major risk in the short term is “development/delay risk”.

While HVY is making substantial progress with its PFS and Mining Lease application, delays in these processes can push back the project's timeline.

The same could also happen with the tailings processing deal - a few months delay could push back the timelines for the deal past the Q4 2026 production date HVY mentioned in today’s announcement. (source)

Development delay risk

Development studies such as pre feasibility studies and bankable feasibility studies can take longer than expected and any delay here could hurt the pace of HVY’s newsflow and sentiment around the company.

Source: HVY Investment Memo, June 2023. What could go wrong?

To see all the relevant risks to HVY read our HVY Investment Memo.

Other risks

Like any small cap exploration and development company, HVY carries significant risk, we aim to identify a few more risks here.

The company’s newly announced tailings project is heavily reliant on its partnership with Hillgrove Resources. There is no guarantee that the integration with the Kanmantoo mine will proceed smoothly, or that Hillgrove’s own operations will continue as planned, which could impact HVY’s access to the garnet-rich tailings.

HVY’s valuation is now more sensitive to the successful financing and execution of this new project. If the company fails to secure the targeted non-dilutive funding, or if CAPEX costs blow out beyond the estimated $25-30M, the market could re-rate the stock lower.

HVY has exposure to a niche industrial mineral - garnet. While recent pricing is strong (~US$500/t), any fluctuation in global demand, particularly from the abrasive or waterjet cutting sectors, could affect project economics and investor sentiment.

Commissioning a new processing plant involves technical and execution risks. There is no guarantee that the plant will achieve economically viable recovery rates or production volumes, which could impact the feasibility of the tailings processing deal.

Finally, broader market sentiment and small cap liquidity could impact HVY’s valuation either positively, if the "every commodity rally" eventuates, or negatively, if investor attention consolidates elsewhere.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our HVY Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our HVY Investment Memo where you will find:

- What does HVY do?

- The macro theme for HVY

- Our HVY Big Bet

- What we want to see HVY achieve

- Why we are Invested in HVY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.