HAR: High grade gold, processing plant, permits to mine, in the USA. And now this...

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,383,780 HAR Shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Some gold projects are high grade.

Some have infrastructure.

Some are big but have neither of the above.

It’s hard to find a project with all three... especially in ASX small cap land.

(AND one located in the USA - which we think will suddenly become VERY interested in gold in the near term - regular readers will already know why.)

Our Investment Haranga Resources (ASX:HAR) has all three at its project in California’s Mother Lode gold belt.

(The centre of the original gold rush in the US back in the 1850s)

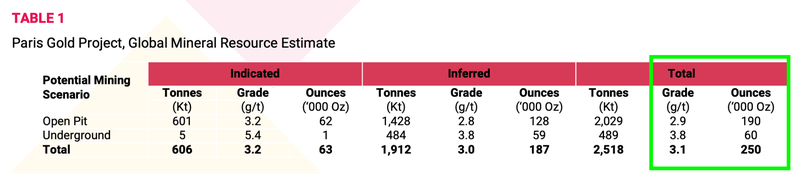

This morning HAR delivered a maiden JORC resource estimate of 402k ounces of gold at an average grade of 5.1g/t gold.

Making HAR’s project one of the highest grade undeveloped gold resources on the ASX.

This is just the start though - we think HAR can grow from here, building a “multi-million ounce” high grade gold asset.

And the thing that sets HAR apart from most sub $50M market cap juniors is that HAR owns a shiny, almost new, gold plant that was last operating in 2022.

A plant that can be restarted to process and sell gold, while gold prices continue at record highs (we went to site and checked it out for ourselves - pictures of it coming up).

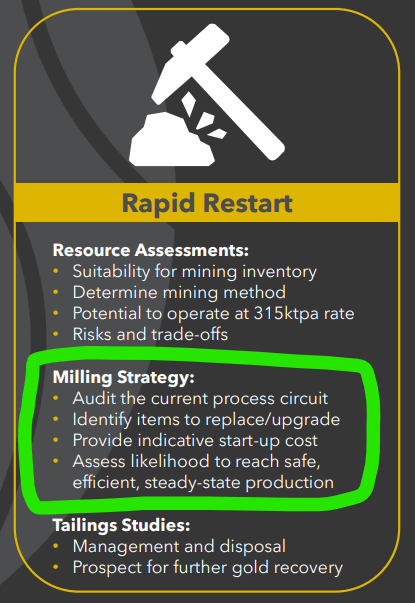

All up there was ~$90M of prior capital investment on the project, and today HAR said it will be commencing “Rapid Restart studies” on the plant.

High grade gold, plus a processing plant, plus now a new 402k oz gold at 5.1g/t gold JORC compliant resource.

Deeper drilling starts in July to grow the resource.

Plus HAR has 3x more exploration targets coming from some of the other historic “California gold rush” mines on its land package.

(more on that in a second)

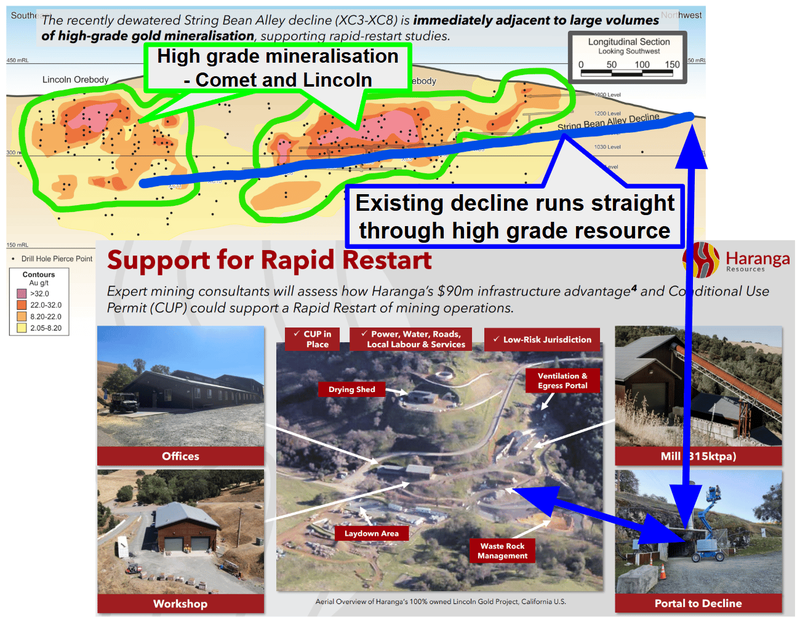

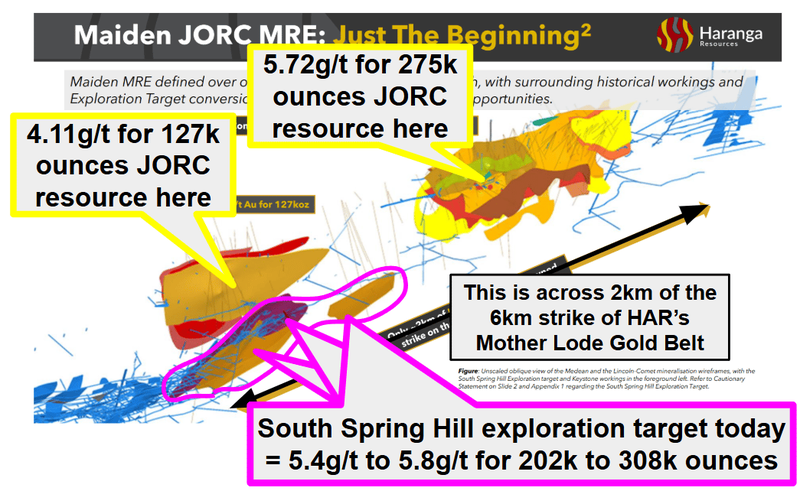

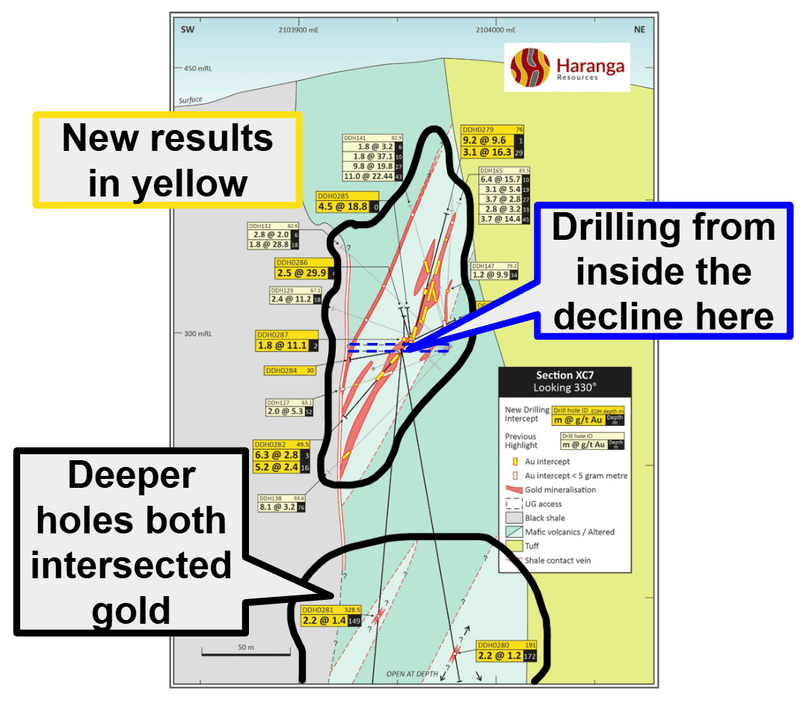

Most of that high grade maiden JORC resource estimate announced today (~275k ounces) is accessible from the project’s existing underground decline.

(a “decline” is a long underground tunnel used by trucks and drilling equipment to access deeper gold)

The same decline HAR spent the last ~12 months rehabilitating.

Which is only a few hundred metres away from HAR’s 100% owned processing plant.

This next image shows the existing decline running directly through the high grade pockets of today’s gold resource.

AND where it all sits relative to the existing plant:

(source)

So HAR is now in a position where it has:

- Gold ground in the famous “California gold rush” Mother Lode Gold Belt.

- ~A$90M of capital recently invested into infrastructure by previous owners, which includes:

- 100% owned 315,000tpa gold processing plant (last operated in 2022 ie NOT an old rustbucket)

- Offices, workshop, and laydown yard

- A “Conditional Use Permit” that allows production of gold.

- NEW TODAY - JORC resource estimate of 402k ounces at 5.1g/t gold.

- Capped at $49M with $9M cash in the bank (31 March 2026) - an enterprise value of ~$40M.

We are Invested in HAR not for today’s resource - but the future one - we think this could evolve into a multi-million ounce asset with time.

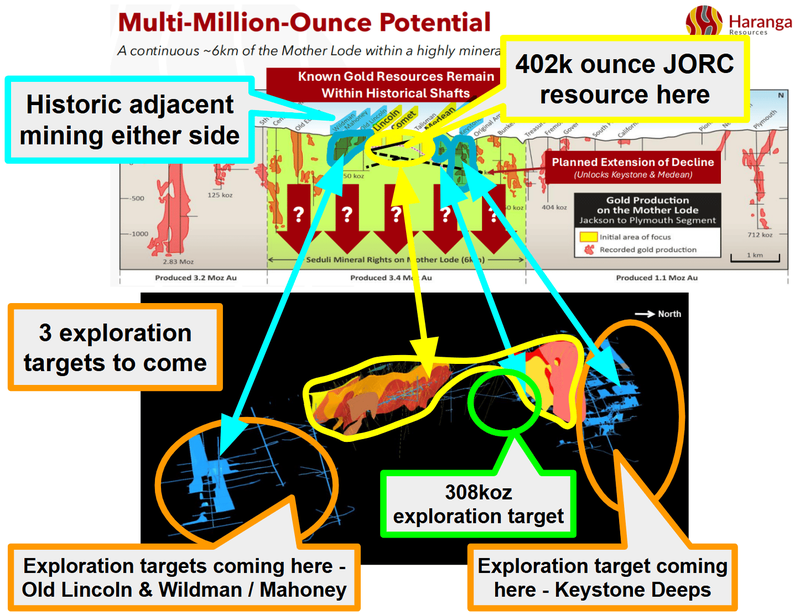

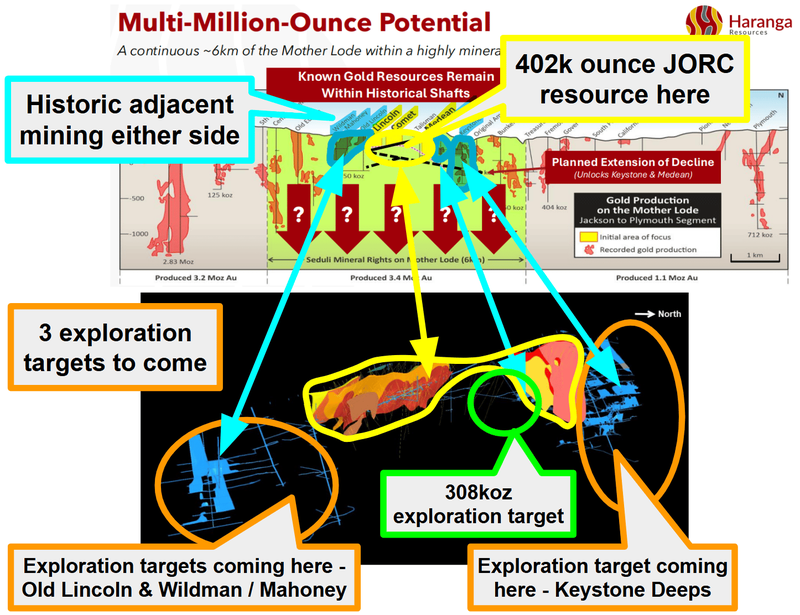

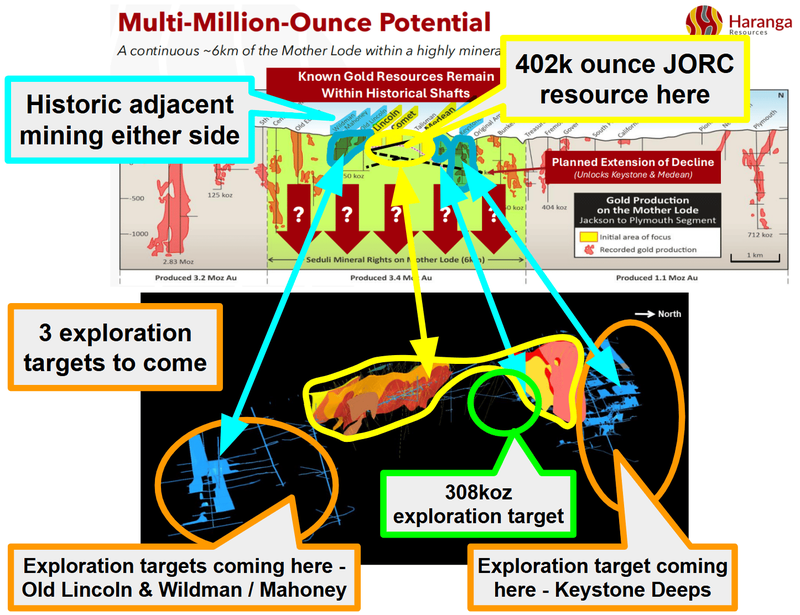

As it stands, HAR has only really focussed on ~2km of the 6km strike its project sits on and has:

- 402k ounce gold JORC resource estimate at Lincoln/Comet and Medean. A

- ~308k ounce exploration target at the "South Spring Hill" target, A

- Multiple exploration targets coming from the other old mines in the area

There are almost 700k ounces defined (JORC resource + a single exploration target).

How much bigger does the resource potential get when those other old mines come into play?

We should find out pretty soon.

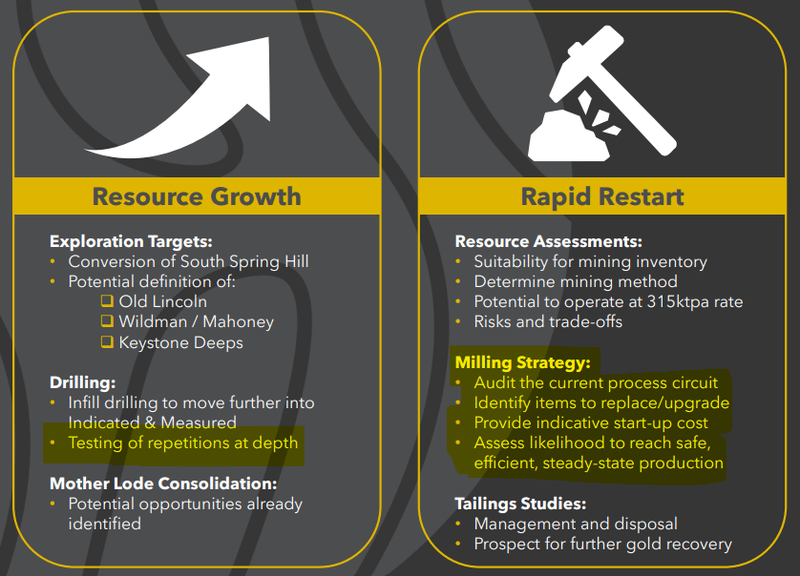

We think HAR has the pieces in place to do one of two things:

- Decide to bring back into production its existing resource - HAR confirmed today that it would look to identify replacement/upgrades that it can then use to provide “indicative costs to start-up” the project.

- Grow the resources (going after the multi-million ounce potential) - HAR confirmed today that the next drill program would start in July going after the moonshot ‘at depth’ exploration targets.

Or do both?

(source)

In the rest of today’s note, we will cover:

- Why grade + infrastructure + permitting + a JORC resource estimate matters

- How HAR's resource stacks up against ASX peers

- Why we think HAR’s resource could grow from here

- What we saw on our site visit to HAR’s US project

- Why we like HAR’s other project in Senegal (where HAR is drilling right now)

- What we want to see next from HAR

HAR has high grade, infrastructure, permitting and now a JORC resource too

Having all of the existing infrastructure in place and ready to go PLUS having a 5.1g/t average grade should theoretically mean HAR can produce gold at a far lower cost than if the project was completely greenfields.

In most underground gold projects, just getting access to an orebody deep underground can cost tens of millions of $$.

And that is just getting to the starting line for production.

HAR's access way is already built, already dewatered, and already next to the gold.

No need to build the tunnel to access the ore from scratch - or the plant.

(as we said above, we’ve been there and seen it with our own eyes - more on this in later)

As for the grade - that means that for every tonne of rock HAR mines - there are more grams of gold (5.1 grams per tonne).

For context - ASX listed, $2.27BN capped Bellevue Gold’s underground gold mine in WA averaged 4.6g/t grade for the March quarter and the gold produced was at an all-in sustaining cost of ~A$2,578 per ounce. (source)

The gold price is currently at A$6,389 per ounce.

(Of course, Bellevue’s project is a lot bigger than HAR’s (for now...?) so there are economies of scale at play for that mine too - that comparison for us it's just a good way of getting a bearing on how grades impact costs).

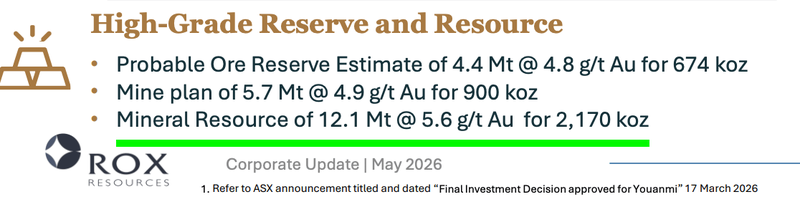

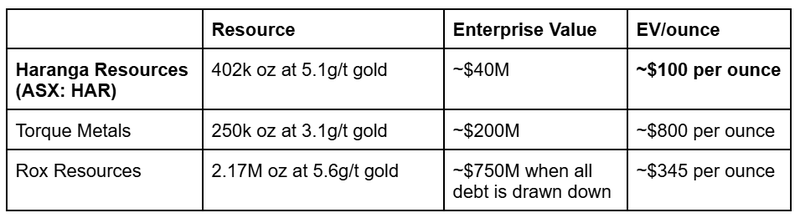

How HAR’s JORC resource stacks up against its ASX peers

We think today’s JORC resource now means the market can finally start to value HAR against its ASX peers.

One comparison the market could draw is Rox Resources’ whose project has a 2.17M ounce gold JORC resource estimate with an average grade of 5.6g/t gold.

(source)

Rox’s market cap right now is ~$600M. The company has a $350M debt facility in place to build all of the infrastructure needed to produce gold on its project and ~$200M in cash.

So Rox’s enterprise value is somewhere around ~$750M assuming a full debt drawn down (EV = market cap plus debt).

ASX listed Torque Metals has a 250k ounce gold resource estimate with an average gold grade of ~3.1g/t gold. (source)

(source)

Torque is currently capped at $215M and had ~$12M cash in the bank at 31st March 2026.

So Torque’s enterprise value is ~$200M.

HAR’s current market cap is $49M with $9.3M cash in the bank at 31 March 2026.

That gives HAR an enterprise value of ~A$40M.

Here is how HAR compares to those two other companies on an EV/ounce basis:

Note these are very rough calculations - Rox could end up needing more cash, or finish building their mine below budget, in which case the debt won't be needed.

A big part of Torque’s resource is open-pittable which could mean lower costs relative to HAR.

Let's not forget - HAR’s project also comes with:

- ~A$90M of historical capital infrastructure investment built by previous owners

- A 100% owned and permitted 315,000tpa gold processing plant (last operated in 2022)

- An 880m underground decline

- Offices, workshop, and laydown yard

- AND a Conditional Use Permit that allows production of gold

Of course, HAR will have to spend some cash getting its processing plant and infrastructure back into good standing too - that’s what those ‘Rapid Restart studies’ starting now are all about.

We think HAR’s resource can grow from here

As it stands, HAR has:

- 402k ounce gold JORC resource estimate at Lincoln/Comet and Medean. A

- ~308k ounce exploration target at the "South Spring Hill" target, A

- Multiple exploration targets pending

There are almost 700k ounces there already in non-JORC resources and one single exploration target.

So the quick easy win is getting South Spring Hill converted into a JORC resource:

(source)

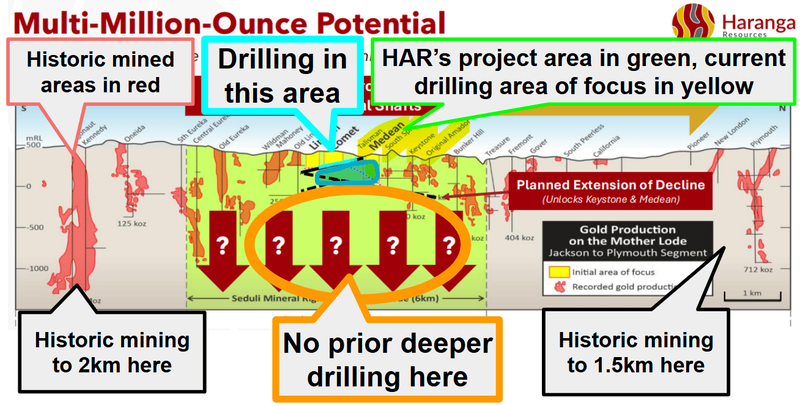

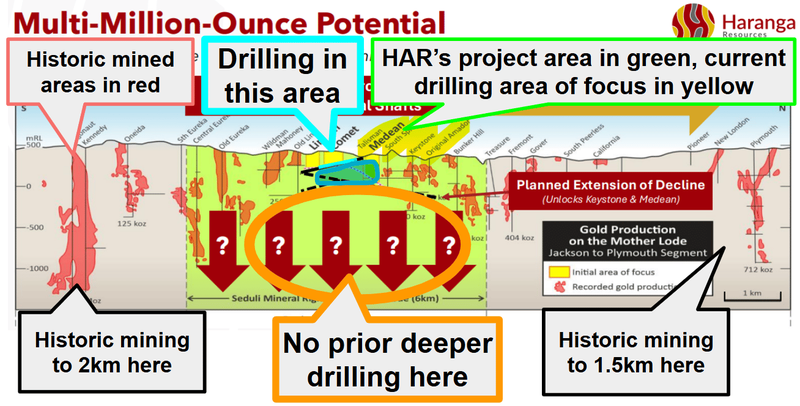

The thing with the HAR’s US project is that there is still so much of the project left to drill test.

Some mines in the area were operated down to ~2km depths before they shut down.

The reason they shut down had nothing to do with running out of gold.

They shut down in the 1940s when the US government redirected mining manpower to the WW2 war effort.

On top of that, the gold price collapsed after the war, the mines never restarted, and the area had essentially been forgotten.

So the mining didn't stop because the gold ran out...

HAR’s resource today is defined across ~2km of strike and only down to depths of ~150m.

HAR still has over 6km of strike to test and over 1,000m at depth (if those old mines are anything to go by).

This slide gives a sense of the exploration upside on the project:

(source)

We think the big moonshot exploration upside will come by drilling at depth.

HAR's most recent drilling program had two “Hail Mary” holes that went looking for those at depth repetitions and both holes hit gold.

(Source: HAR announcement)

Importantly, the alteration package intersected at the base of DDH0280 has been interpreted as indicative of a potential repetition of the mineralised package above.

The Lincoln-Comet system is mineralised at depth, and it remains entirely open.

The deeper drilling that's about to follow these first two scout holes is what could unlock the second, third and fourth lodes of high-grade gold beneath the current 402koz resource.

On top of that, HAR has flagged three more Exploration Targets in its pipeline for definition over H2 CY26:

- Old Lincoln

- Wildman / Mahoney

- Keystone Deeps

All three sit on the same 6km strike, all three have historical workings on them, and all three have historical drilling and sampling data.

So inside the second half of this year we could see HAR make new discoveries OR convert those old structures into exploration targets which spell out how HAR gets to that “multi-million ounce” potential it keeps talking about.

HAR expects to be drilling the deeper targets on the project in July and have the exploration targets out in the second half of 2026.

We think once a few of those exploration targets drop - the market can start to visualise how HAR’s project gets scaled quickly.

Especially after today’s maiden JORC resource...

We have been to site - here is what we saw:

We were on site with HAR’s team back in June last year (check the full note here) - here is a quick overview of everything we saw:

- HAR’s fully built and operational site office

- HAR’s fully built, stocked and staffed workshop

- HAR’s built and permitted 315,000 tpa gold processing plant

- HAR’s 880m decline (the tunnel to the gold)

- The laydown yard, and our meeting with locals that know the project well

- The historic mines in the area (that have produced ~7.7 million ounces of gold in the past)

- The old mining town that surrounds HAR’s project

(source - our full write up and pics from a site visit last year, see that here)

How about in Senegal - can HAR repeat the $4.5BN Predictive Discovery playbook?

As mentioned earlier, we also like HAR’s Senegal asset where the company is currently drilling.

We didn't use to like it - it was more of a legacy “side salad” project we pushed to the side of the plate and tried our best to ignore...

But HAR committed to some cheap, shallow drilling...

And delivered a massive gold hit on hole #8 back in October 2025 which hit 20m at 6.54g/t gold and quickly captured the market's attention... and ours.

That first batch of results were strong enough for HAR to go straight into a second shallow round of drilling.

And now we know there is ~800m of strike to test with a fair few holes that ended in mineralisation.

All of the drilling so far has been holes down to ~20-85m depths.

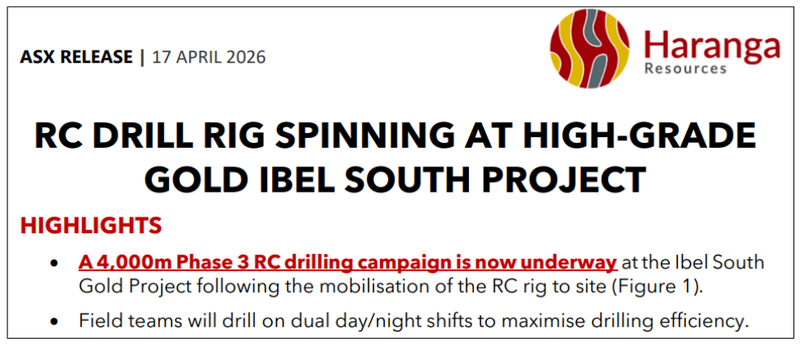

Right now, HAR is running the first RC drill program with holes planned down to depths of ~260-300m.

With this program we should find out if HAR accidentally made a big new gold discovery, OR if the results from back in October were isolated pockets of high grade gold.

(source)

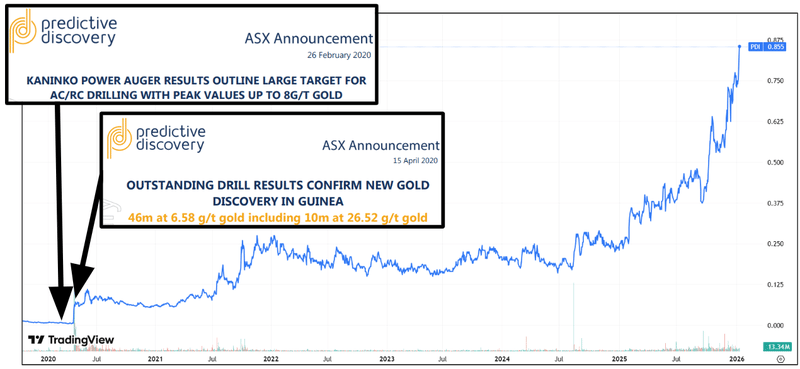

We think HAR is now in a similar position to where $4.5BN Predictive Discovery was when it made its discovery back in February 2020.

Predictive’s asset ended up as a 4.9M ounce discovery and took the company’s share price from 0.6c per share to a high of ~$1 per share.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The ultimate win for HAR in Senegal would be a “Predictive Discovery style” major gold discovery.

Here is how the Predictive story went and where we see similarities with what HAR has...

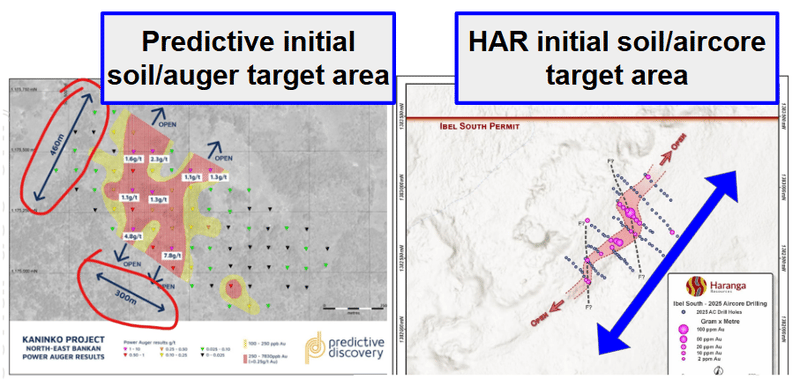

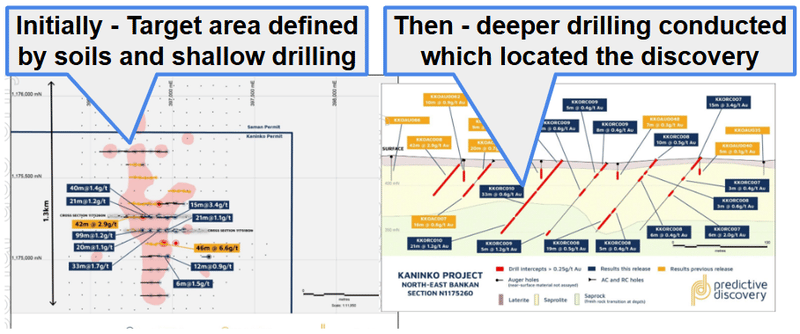

The Predictive announcement from 26 February 2020 was when we got a first look at the extent of gold structures (from shallow auger drilling) - similar to what HAR has defined so far.

Here is what Predictive had in February of 2020, and what HAR has now side by side:

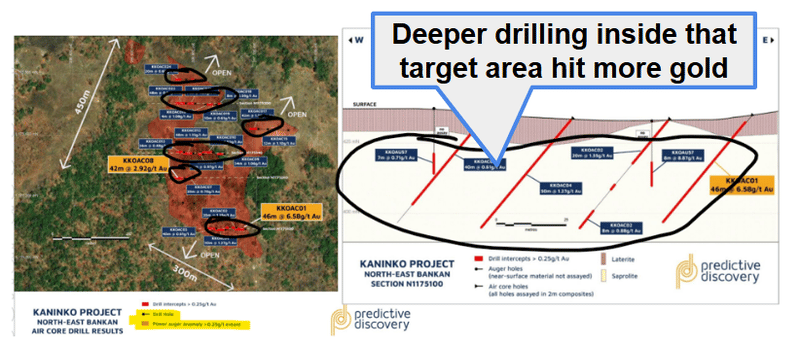

Then a few months later, Predictive followed up with deeper holes along that area that the shallow drilling had defined (they literally drilled below those shallow gold targets):

(source)

HAR is currently at this stage - running the first round of deeper drilling where it hit gold with shallow auger drillholes.

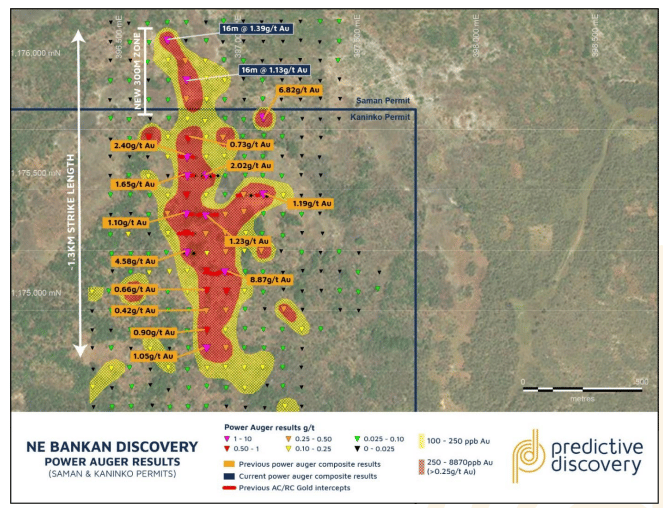

That first round of deeper drilling was what opened the door to a big capital raise for Predictive and by July 2020, a ~1,300m structure had been defined on the project:

(source)

After that larger structure was drilled the market started to really take the discovery seriously.

(source)

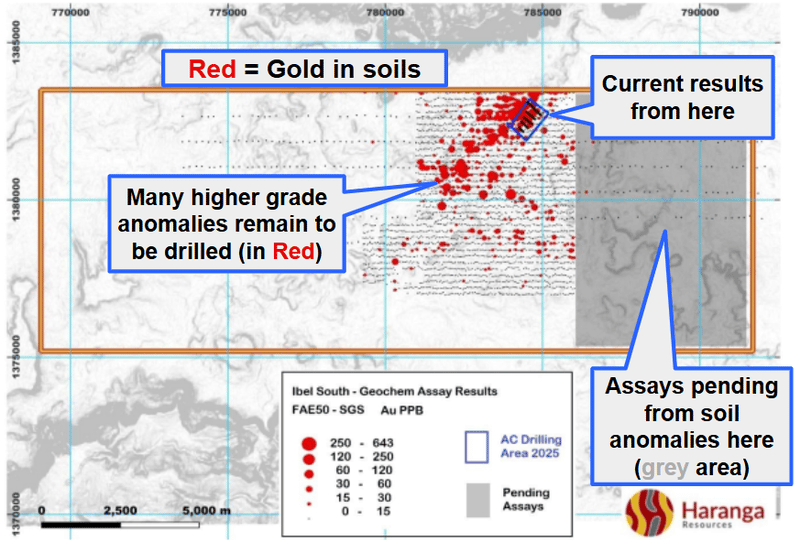

Right now, HAR’s got its 800m gold in termite mound soil anomalies - confirmed by shallow aircore drilling.

And the area that’s been drilled so far only makes up a small fraction of the ~5km area with gold in soils across the project:

(source)

These early results could be the makings of a big discovery - or it could go nowhere.

What we do know is that often big discoveries are made when no one expects anything to happen (that’s exploration for you 🤷♂️).

The deeper drilling (IF it comes in - no guarantees of course) just like Predictive’s did between February & April 2020 could be what sets up HAR to go off and test the rest of the project.

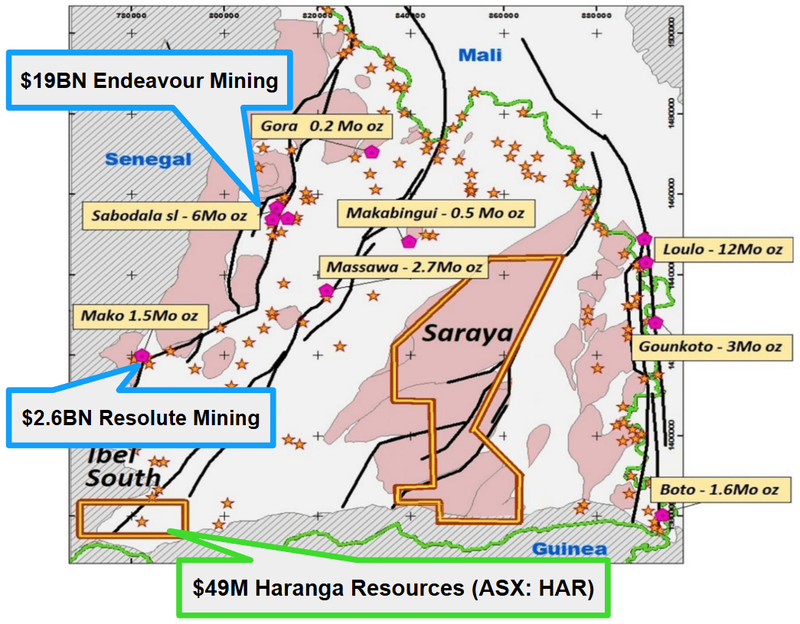

IF HAR can find anything remotely valuable, then it is also in a part of the world where it could attract attention from much larger-cap peers too.

HAR’s project sits in an area with some big operating mines including projects owned by $22BN Endeavour Mining and $3.1BN Resolute Mining.

(The region has a few other gold discoveries too, so it's not in the middle of nowhere).

So a big discovery from HAR here could very easily bring with it corporate attention (if the early results haven’t already).

(source)

Ultimately, success at either of HAR’s projects could be what helps the company achieve our Big Bet as follows.

Our HAR Big Bet:

“HAR re-rates to a market cap greater than $200M by making new gold discoveries in California and progressing towards production or is acquired at a multiple of our initial entry price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our HAR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's Next for HAR?

🔄 Phase 2 underground drilling at US asset (mid-2026)

HAR has flagged that a phase 2 drilling program would start on the project in July.

We are especially looking forward to the deeper drilling below the current resource.

We have already seen hole #280 and #281 from the last round of drilling hit gold well below the existing decline - with the next round we should know if those were isolated OR part of bigger structures at depth.

Remember there have been mines running down to ~2km in this part of California:

(source - HAR presentation November 2025)

🔄 3x more exploration targets (H2 CY26)

HAR also mentioned in today’s announcement that it was working on an exploration target across three of its other targets:

- Old Lincoln

- Wildman / Mahoney

- Keystone Deeps

All three sit on the same 6km strike as the current resource.

All three have historical workings, historical drilling, and historical sampling data.

🔄 Scoping study for a ~315 ktpa mining operation

HAR’s presentation today said it would start identifying items to replace/upgrade and the big one “provide an indicative start-up cost”:

(source)

This will be the first time we get a look at any capital costs required to bring the processing plant (and associated project infrastructure back online).

🔄 Senegal drilling results

HAR is now drilling its asset in Senegal with a deeper RC rig.

As mentioned earlier, here we are hoping that previous hit (20m @ 6.54 g/t gold from just 12m depth) can be followed up and proven as part of a larger gold system.

Here are the milestones we are tracking for the Senegal asset:

- ✅ Drilling started

- 🔄 Assay results

- 🔲 Decision to come back and do more drilling

What Could Go Wrong?

The near-term risk for HAR is around “exploration risk”

HAR has a drilling program planned to start in July chasing the deeper extensions to its current resource.

There is no guarantee HAR finds anything economic with that drilling - IF results are below market expectations then HAR’s share price could suffer negatively.

Exploration risk

There is no guarantee that HAR's upcoming drill programs are successful and HAR may fail to find economic gold deposits.

Source: "What could go wrong" - HAR Investment Memo 25 June 2025.

Other risks

Like any early-stage gold exploration and development company, HAR carries significant risk, here we aim to identify a few more risks.

While HAR benefits from an existing processing plant and underground decline, this infrastructure has been idle since 2022.

There is a risk that the upcoming scoping study reveals much higher-than-expected restart costs to bring these assets back into good standing.

Furthermore, executing simultaneous drilling programs in both California and Senegal alongside engineering studies will deplete the company's $9.3 million cash buffer.

This high cash burn rate means HAR will likely require future capital raises, resulting in potential shareholder dilution.

Finally, the company remains highly exposed to broader commodity price fluctuations.

Although gold prices are currently strong, any sharp decline would immediately threaten the commercial viability of HAR's underlying resources.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our HAR Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our HAR Investment Memo where you will find:

- What does HAR do?

- The macro theme for HAR

- Our HAR Big Bet

- What we want to see HAR achieve

- Why we are Invested in HAR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.