GUE: Ubaryon uranium enrichment technology AND US based uranium…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,671,018 GUE shares and 500,000 GUE options and the Company’s staff own 35,000 GUE shares at the time of publishing this article. The Company has been engaged by GUE to share our commentary on the progress of our Investment in GUE over time.

The USA is talking a lot about how many data centres they need to build for their Artificial Intelligence ambitions.

(a couple of weeks ago Trump announced “Stargate” - the $500-Billion plan to build AI infrastructure and data centres in the US.)

And the domestic nuclear energy needed to power these data centres...

To make nuclear energy you need raw uranium mined out of the ground

AND

Access to advanced technology to “enrich” that raw uranium to be used in nuclear reactors.

The USA now also wants to bring home many of its mining, processing and energy generation industries.

(See the “Unleashing American Energy” executive order signed a few weeks ago)

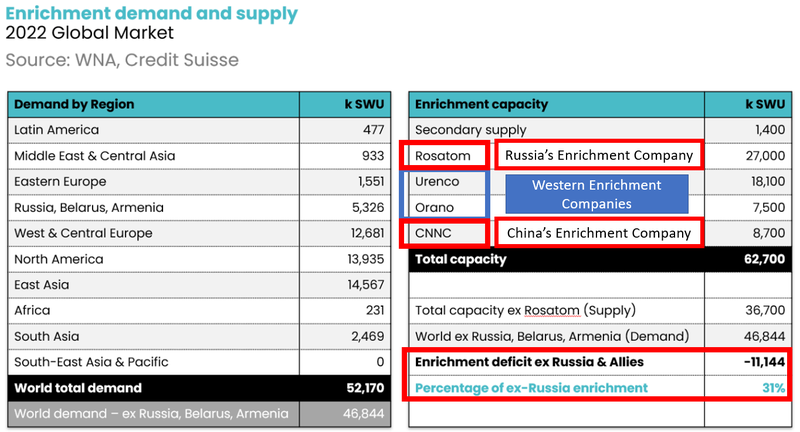

As of 2022, Russia and China dominate the global uranium enrichment market with a combined 63% of global capacity - and there’s a big squeeze going on in the West for enrichment capacity.

Our Investment Global Uranium and Enrichment (ASX:GUE) holds a number of promising US based uranium exploration and development assets.

GUE is also the largest holder (with a 21.9% stake) in a private uranium enrichment company - called Ubaryon.

(GUE’s material stake in this uranium enrichment tech is one of the main reasons we Invested in GUE)

Uranium enrichment is a technology process which brings uranium mined from the ground to a state where it is suitable as fuel for reactors.

GUE’s private enrichment company is developing a technology for enriching uranium that is potentially cheaper, safer and more environmentally friendly than others.

We were attracted to GUE as it is one of only two companies on the ASX with uranium enrichment exposure.

The only other company - Silex Systems - is capped at over $1.3BN and has seen its share price rise over 500% in the last two years.

Silex owns 51% of its enrichment tech and is partnered with uranium major $33BN Cameco.

GUE is currently capped at $25M, and has a 21.9% stake in its technology.

On Wednesday this week, GUE announced that the prospect of a strategic partner has emerged to take Ubaryon forward and invest in the technology.

GUE expects that strategic partnership inside the next 4 months...

GUE’s Ubaryon is targeting a transaction “with selected organisations involved in the Nuclear Fuel Cycle production industry” which have “expressed interest in reviewing technology and potentially investing”.

(Source)

Our take is that with additional funding by a strategic partner, things could really accelerate for it, and along with it, GUE’s valuation.

Check out the chart below for the ONLY other uranium enrichment technology company on the ASX... Silex Systems.

Silex increased over 3,000% in a 5-year timeframe and now has a market cap of over $1BN:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

With the nuclear power thematic heating up, and a greater focus on the security of supply, we think that the time is now for this technology to be carried forward.

Here are the key points from GUE’s Ubayron update:

- In the next four months: Ubaryon is targeting a transaction “with selected organisations involved in the Nuclear Fuel Cycle production industry” which have “expressed interest in reviewing technology and potentially investing”.

- From late February: site visits are planned for appropriate independent experts to review the details of its technology.

The Ubaryon shareholder update that GUE released on Wednesday says that Ubaryon is confident that the current strategic organisations engaging with Ubaryon can speed up and enable the commercialisation of the technology and a “commercial outcome”.

That could be a valuable thing for GUE which is Ubaryon’s largest shareholder.

We also think that this update is incredibly timely given Trump’s new energy policy stance which has nuclear energy, along with oil as some of its cornerstones.

First though, what’s the “secret sauce” that helped GUE’s peer, Silex Systems achieve a +3000% re-rate?

The Silex Systems story - what would success look like for GUE?

With its 21.9% stake in Ubayron, GUE is looking to become the next “Silex Systems”.

Silex stands for Separation of Isotopes by Laser EXcitation - yes, they actually use lasers to enrich uranium.

GUE’s tech works slightly differently, it is a chemical process of enriching uranium - which if it works, could use less energy, be more environmentally friendly and simplify the enrichment process.

Silex was first listed in 1998, and it has been a long journey for the company to reach its current +$1BN valuation, mainly on the prospect that its laser can help revolutionise what is now a +$6BN uranium enrichment market.

Things started getting interesting in 2006 for Silex though when Silex signed a partnership deal with General Electric (GE)-Hitachi:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We did a deep dive into the history of Silex, and in the simplified timeline below, we’ve noted a few major moments for it:

- 2006: A partnership deal with GE-Hitachi partnership - helped take it from a share price of ~$1 to ~$12.50 in a year (deal terms noted below) (Source)

- 2008: Global Financial Crisis

- 2011: The Fukushima disaster in Japan (by this stage the Silex share price is close to ~$2)

- 2016: An attempt at a deal re-cut with GE-Hitachi - GE-Hitachi had different “business priorities” (Source)

- 2018: Silex moves to abandon the tech and partnership with GE-Hitachi (Source)

- 2019: Deal revived with Cameco where Silex retains a 51% ownership (deal terms noted below) (Source)

- 2022: Ukraine Russia war starts - share price back to ~$1.50

- 2023: Inflation Reduction Act allocates US$700M to enriched uranium - share price at ~$4.50

- 2024: US legislation moves to ban Russian enriched uranium imports - share price at ~$6.60

As you can see, getting uranium enrichment technology off the ground can take many years, but the macro tailwinds have never been stronger for these types of technologies.

We think a mix of investor and government interest will mean capital enters the sector fast enough to speed up the development of enrichment technologies...

And we are betting that GUE’s Ubaryon benefits from these tailwinds.

Why we think GUE’s enrichment technology is well placed

We’re hoping that GUE can move much quicker than Silex in achieving a major re-rate through a commercial outcome for a number of reasons:

- It’s a chemical process and doesn’t require “fancy lasers” (like Silex’s technology does)

- It isn’t encumbered with a commercial partner that has different business priorities (like the GE-Hitachi partnership was)

- Unlike Silex, GUE hasn’t had to navigate the GFC (2008) and Fukushima (2011), and as far as geopolitics go, the case for nuclear power and uranium is much stronger now than it has been in decades

Back in June 2024, GUE announced that its enrichment technology had achieved “a separation factor approximately three times higher than the enrichment factor.”

An “important measure for commercialisation.”

Read more about GUE’s stake in an enrichment technology partner in the article below:

GUE: Uranium enrichment technology achieves 3x “separation factor” in enrichment process

Enrichment tech is crucial to energy supply

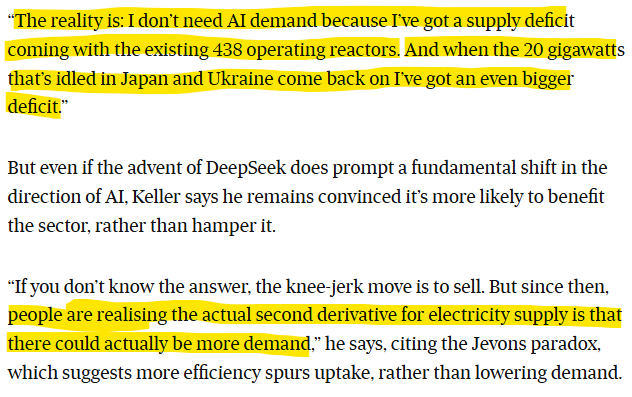

The markets interpreted that the recent kerfuffle around the new Chinese AI model “DeepSeek” would reduce forecast AI power demand (and thus nuclear demand and uranium demand).

The uranium price did soften a little bit BUT is still at 14 year highs.

Longer term, this is about geopolitics and competition by great powers for control of energy supply in the uranium and uranium enrichment market, as well as the long term demand for nuclear power and uranium as a way of decarbonising as more reactors come on line.

Guy Keller of Tribeca Investment Partners recently noted that the AI debate may not be material to the longer term picture for nuclear power and uranium:

(Source)

We think that’s an excellent point.

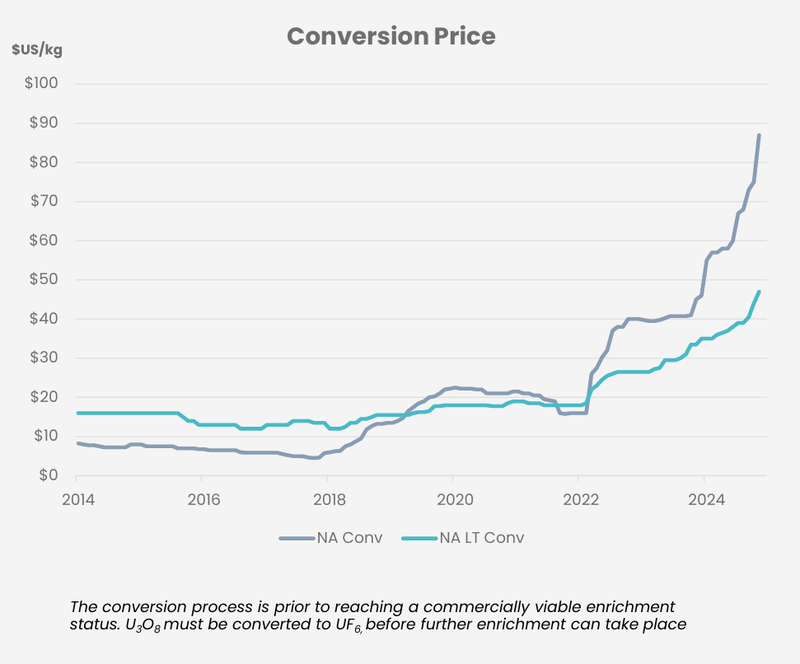

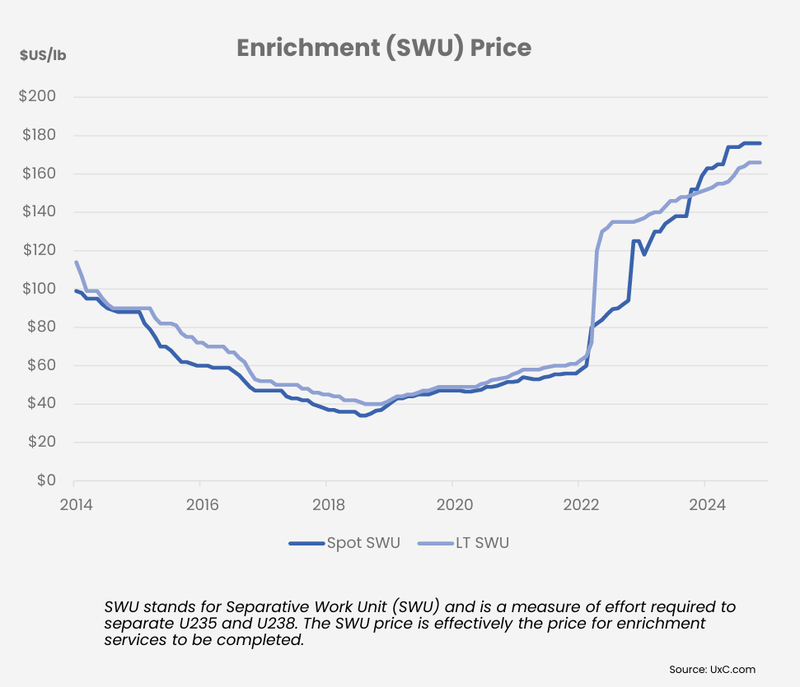

And then of course, there are the current uranium enrichment market fundamentals which we think could drive any potential negotiations that GUE’s Ubaryon enters into.

Have a look at the costs of conversion (where yellowcake is converted into a gas) and enrichment prices from a recent GUE presentation:

(Source)

That looks like the start of a pretty aggressive trajectory.

So that's the price to consider - but there’s also geography involved as well.

That is, which countries hold the largest share of the uranium enrichment market.

In our initiation note (read it here, note: at the time GUE was called OKR), we mention that the enrichment market is dominated by Russia and China.

Below is a quick summary of the companies that have enrichment capacity in the world matched up against sources of demand:

Quick takeaway: As of 2022, Russia and China dominate the global uranium enrichment market with a combined 63% of global capacity - and there’s a big squeeze going on in the West for enrichment capacity.

We think Silex’s current +$1BN valuation is based on the fact that its technology has the potential to revolutionise or dominate a growing +$6BN uranium enrichment market.

Deal terms are important here for Silex, as we anticipate they will be for Ubaryon (of which GUE is the largest shareholder with a 21.9% stake).

Silex has a 51% stake in a JV with Cameco, and importantly the agreement that Silex struck in 2019 with Cameco sees it retain a perpetual 7% royalty.

(Source 2019 Silex-Cameco JV Announcement)

The Silex-Cameco JV also includes access to a large ~300,000 metric ton uranium tailings facility in Kentucky, USA, which assuming the Silex technology works at scale, is equivalent to a Tier-1 uranium deposit with a ~40 year mine life according to previous Silex announcements. (Source)

All of this, we think points to potential valuation upside for GUE based on its current market cap of $25M and its 21.9% stake in Ubayron (not to mention its existing ~52Mlbs of uranium resources and its ambition to grow that to +100Mlbs).

While the technology is a black box, as it remains heavily regulated and subject to the most stringent government controls, the Silex story gives us some good clues as to how much the market values enrichment technologies.

In other words, we just can’t know exactly how “good” it might be.

So the site visits conducted in late February (this month) will further confirm to independent experts just how good it is.

Then we hope that Ubaryon, as part of its strategic partnership planning, can secure a good commercial outcome for themselves (and by extension, their largest shareholder in GUE) with any negotiations.

The proof will be in the pudding, as they say.

US processing tech and capital markets expert joins GUE board

There’s a new director at GUE with experience bringing commodity processing tech to market in the US... and he is familiar to us and our Portfolio

Last week Hugo Schumann was appointed as non-executive director of GUE.

This is the same Hugo Schumann that sits on the board of one of our other Portfolio companies IonDrive (ASX:ION).

Hugo is the former CFO of Jetti Resources, a copper extraction technology.

Jetti was backed by top industry investors like Freeport, BHP, Mitsubishi and Blackrock.

Hugo was instrumental in delivering the Series C ($50M) and Series D ($160M) rounds for the company which was last valued at $2.5BN in 2022.

Hugo also established the London office of the Apollo Group, a natural resources VC firm.

We think that Schumann’s track record of raising significant amounts of capital for minerals processing technology companies is of big benefit to GUE.

GUE is not just a uranium exploration company... its stake in uranium enrichment company Ubyron means that Schumann is a perfect fit.

Our GUE Big Bet:

“GUE re-rates to a +$250M market cap by achieving a major technological breakthrough with its uranium enrichment technology and/or is acquired at multiples of our Entry Price by a US focussed uranium major looking to gain access to its assets and technology”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our GUE Investment Memo.

More nuclear energy is coming to America under Trump

GUE holds a number of promising US based uranium exploration and development assets and a 21.9% stake in a uranium enrichment technology.

In the first few weeks of his presidency Donald Trump announced the “Unleashing American Energy” executive order.

The goal is to reduce red tape and unnecessary regulations to “unlock” the domestic energy potential within America.

In the Executive Order, Trump also directs the US Geological Survey to update the list of critical minerals.

Highlighting uranium specifically for consideration:

The strategy is to make it easier for domestic nuclear resources to emerge.

Two days later Trump announced “Stargate” the $500-Billion plan to build AI infrastructure and data centres in the US.

With investments from SoftBank, Open AI and Oracle - the race is on to turn the US into an AI superhub.

These data centres are going to need reliable energy... and a lot of it.

Nuclear power is emerging as the preferred energy source for AI data centres for two key reasons.

It’s reliable and local.

Nuclear power can provide a consistent, reliable, and large amount of energy with minimal carbon emissions to these data centers

Also, small modular reactors could minimise the infrastructure build out needed to link data centres up to the grid.

The alternative is linking these data centres up to the grid... which costs money and time in lobbying local communities to build more powerlines.

Major tech companies have gravitated to nuclear power as the perfect type of energy to run AI data centres.

Last year Microsoft signed a 20-year power supply agreement with nuclear power providers in Pennsylvania.

(Source)

Given Trump's fondness for nuclear energy and interest in growing the US’s AI infrastructure, we think that US-based uranium companies could see significant benefits.

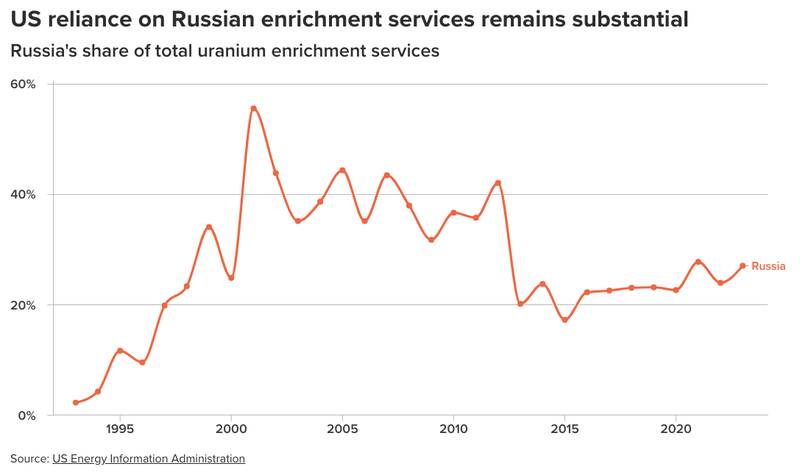

The challenge is that 27% of the US’s “enriched uranium” supply is coming from Russia... and is growing marginally.

(Source)

We don’t see Trump happy for Russia to control such a large part of the future energy mix for the United States.

So we expect uranium (and potentially enriched uranium) to be placed on the critical minerals list - which will support domestic production and help GUE in the process.

How does yesterday’s news impact our GUE Investment Memo?

Yesterday’s update advances our number 1 objective for GUE:

Objective #1: Advance enrichment technology

We want to see GUE advance its enrichment technology with its partner to make it attractive and viable in the eyes of uranium majors and the US government and/or other friendly countries.

GUE Investment Memo - FEB 2023

If Ubyron is able to secure a strategic partner and further funding for its uranium enrichment technology it could more quickly validate its technology.

What’s next for GUE?

Enrichment Technology

At the fundamental level, we want to see Ubaryon de-risk its enrichment technology both operationally and from a regulatory perspective:

🔄 Secure strategic/commercial partner for uranium enrichment technology

🔄 Further validation and extend the enrichment performance (show how well it works)

🔲 Achieve continuous operation at bench scale (scale up process)

🔲 Regulatory approvals

GUE’s Mining Projects

GUE has a number of North American uranium exploration & development assets, here is what we are looking out for across these projects:

🔄 Project 1:~52Mlb Resource Scoping study (coming months)

A Scoping Study is due shortly at GUE’s advanced ~52Mlb JORC resource in Colorado.

GUE indicated in September that the scoping study is due in the “coming months”

🔄 Project 2: Maybell JORC Resource (coming months)

GUE completed its drill program in October last year, now it is preparing a maiden mineral resource estimate for Maybell in another part of Colorado.

Depending on the resource size and economics, next steps could potentially include additional drilling in 2025 and a scoping study to evaluate development options.

What could go wrong?

We see the main risks for GUE to be “Development Risk” and “Technology Risk”.

While development risk was not included in our GUE Investment Memo, it is increasingly relevant to GUE as the company is on the cusp of delivering a scoping study at its ~52Mlb resource in Colorado.

Noting the currently sliding uranium price, the economics could be lower than market expectations, or the project could prove more difficult to develop further in the future.

On GUE’s enrichment technology, GUE could fail to secure regulatory approvals, the technology could struggle to scale up, or the technology partner fails to validate the efficiency improvements it brings at scale.

Our GUE Investment Memo:

Click this link to see our GUE Investment Memo where you can find a short, high level summary of our reasons for Investing.

In our GUE Investment Memo, you can find the following:

- What does GUE do?

- The macro theme for GUE

- Our GUE Big Bet

- What we want to see GUE achieve

- Why we are Invested in GUE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.