GUE: Acquiring advanced Uranium development project in the USA, and a new NASDAQ listed 19.9% cornerstone investor…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,671,018 GUE shares and 500,000 GUE options and the Company’s staff own 35,000 GUE shares at the time of publishing this article. The Company has been engaged by GUE to share our commentary on the progress of our Investment in GUE over time.

The USA’s new hunt for metals, gold and energy within its own borders is currently one of our favourite investment thematics.

We are witnessing the new USA administration lead potentially some of the biggest changes to the world order since WW2.

As part of this, the US is now moving to secure critical metals and nuclear energy for AI within its own borders.

Nuclear energy needs uranium.

The USA needs a local supply of uranium.

We Invested in Global Uranium and Enrichment (ASX:GUE) because it has uranium in the USA...

And this week it just acquired even more...

GUE’s strategy is to build a high grade uranium portfolio, targeting a potential 100Mlbs of total resources.

We also like that GUE owns 21.9% of a “world leading” uranium enrichment technology.

Now, GUE has just announced a transformational transaction that is going to help it dramatically scale up its ‘pounds in the ground’ uranium resources.

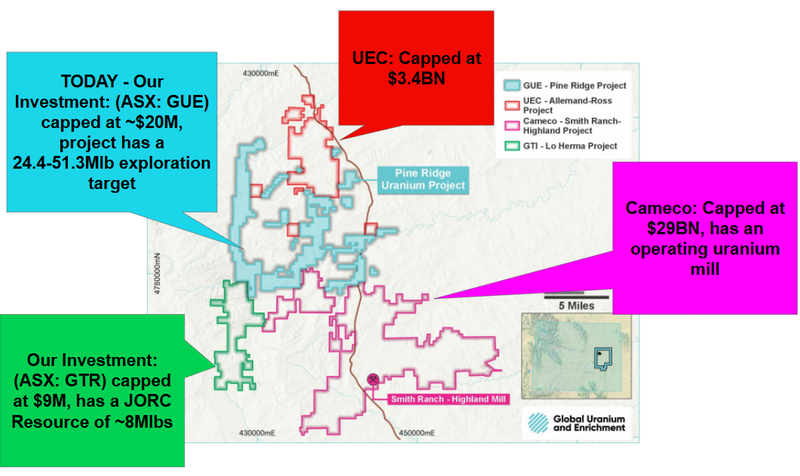

GUE is buying 50% of an advanced stage uranium development project in the USA that has an exploration target of 24.4 - 51.3M lbs.

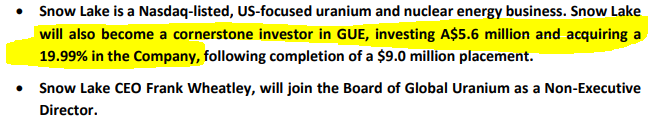

And it's getting a new NASDAQ listed cornerstone investor, Snow Lake Resources - a US based uranium and nuclear energy company.

Snow Lake is investing A$5.8M in GUE’s $10M Placement to hold a 19.9% stake in GUE, and will take a GUE board seat

(Snow Lake CEO Frank Wheatley will be joining the GUE board as a Non Exec Director.)

And by look through, Snow Lake effectively will own ~4% of the Ubaryon uranium enrichment tech.

(we are also putting cash into the GUE placement)

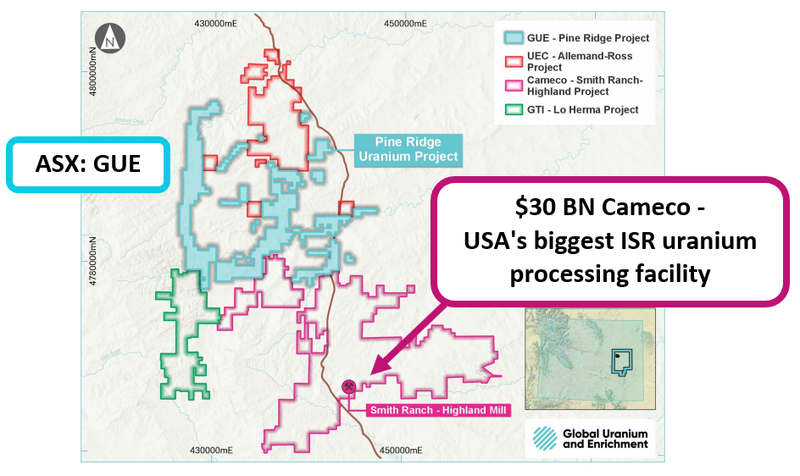

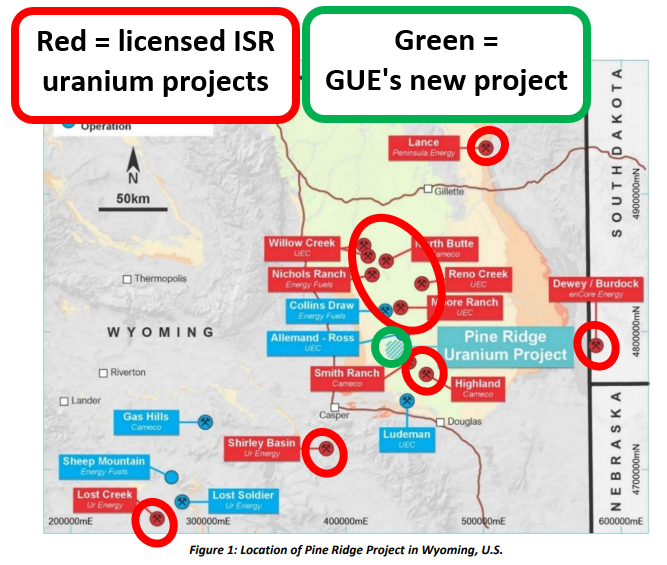

As part of this deal, Snow Lake and GUE have agreed to jointly acquire the Pine Ridge uranium asset in Wyoming, USA in a 50:50 joint venture.

Pine Ridge Uranium Project in Wyoming is an In-Situ Recovery (ISR) uranium project which has an initial exploration target of 24.4-51.3Mlbs.

And if GUE and Snow Lake can confirm that much uranium in upcoming drilling - it would be one of the largest uranium projects in Wyoming.

(By the way, ISR is a mining process where uranium is recovered on site, making it cheaper to put into production.)

The project is ~15km away from the USA’s biggest permitted ISR processing facility owned by $30BN Cameco:

The deal and placement completion is subject to shareholder approval in April, plus Snow Lake will need to complete due diligence on GUE.

Seeing a NASDAQ listed, US based company like Snow Lake take such a big stake in an ASX company with USA uranium assets and uranium enrichment tech got us thinking:

- Snow Lake could have stopped at just the 50% JV with GUE on the new Wyoming project, why buy 19.99% of GUE?

- Are they buying 19.9% of GUE for exposure to GUE’s Ubaryon uranium enrichment tech?

- GUE recently announced a new major strategic partner for Ubaryon is expected to be secured in the next few months

- This is a news event that could capture NASDAQ attention

- GUE, the ultimate owner of 21.9% of Ubaryon, could stand to benefit most from this attention.

Thats just our quick take speculation after having done some digging on Snow Lake and this new transaction with GUE.

Probably better to hear what the GUE CEO thinks...

GUE Managing Director Andrew Ferrier is providing an update on the new project and a Q&A session at 11am AEDT:

11AM AEDT TODAY

(Thursday 13th March)

Click here to register for the GUE investor conference call

Why is NASDAQ listed Snow Lake buying 19.99% of GUE?

A part of the deal that caught our attention was the fact that Snow Lake came into GUE via a direct investment.

Snow Lake put $5.8M into GUE in the placement and will end up being GUE’s biggest shareholder.

(19.99% is also the limit to which a company can buy, without triggering takeover rules on the ASX).

But why did Snow Lake not stop at the 50% Joint Venture on the Wyoming assets?

We think it has a lot to do with GUE’s 21.9% owned enrichment investment (Ubaryon).

Uranium enrichment technology exposures across any exchanges are extremely hard to find.

On the ASX, GUE is just one of two companies...

The other one is Silex Systems which owns 51% of its tech, partnered with Cameco.

Post the recent Russian export restrictions on enriched uranium, Silex’s market cap hit close to $1.5BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Enrichment tech is usually exclusive to the biggest names in the sector and the only way to get exposure would be to own something like Cameco.

By picking up 19.99% of GUE, Snow Lake puts its foot on ~4% of the Ubaryon uranium enrichment tech.

AND now, GUE’s enrichment tech gets exposure to the biggest capital markets in the world.

With that comes a much bigger pool of investors, with much deeper pockets than we are used to on the ASX, especially when it comes to tech.

In the US, seed rounds for this type of tech could see $100M+ cheques being thrown around.

For the Melbournians out there, think of the NASDAQ like the MCG and the ASX like Rod Laver Arena...

We think Snow Lake is buying into GUE for exposure to its enrichment tech JUST BEFORE a big catalyst is due for that enrichment tech.

GUE in an update last month said it was targeting a transaction “with selected organisations involved in the Nuclear Fuel Cycle production industry” which have “expressed interest in reviewing technology and potentially investing”.

AND that “a potential transaction is expected to be completed in the first half of 2025”.

So inside the next 3 months we could see GUE announce a catalyst that we have been waiting for ever since we first Invested in GUE back in February 2023.

(Source)

We think that a major catalyst, from tech that is hard to find exposure to, AND which is now able to be invested into on the NASDAQ and the ASX... could be a trigger for a re-rate for GUE.

Potentially even, a bit like the crowd reaction when a last minute AFL Grand Final goal sails through at the MCG.

Ultimately our Big Bet for GUE is centred around seeing the company’s valuation re-rate off the back of developing or dealing on its enrichment investment:

Our GUE Big Bet:

“GUE re-rates to a +$250M market cap by achieving a major technological breakthrough with its uranium enrichment technology and/or is acquired at multiples of our Entry Price by a US focussed uranium major looking to gain access to its assets and technology”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our GUE Investment Memo.

8 reasons why we like GUE’s new project

Wyoming is a region we are quite familiar with from our Investment in another uranium company, GTI Resources (ASX: GTR).

GTR owns the project immediately to the south of GUE’s new asset.

As soon as we saw the announcement from GUE yesterday, we had a pretty good idea of why GUE would be putting its foot on an asset in this part of the world.

We think Wyoming and the type of project GUE has (ISR uranium - read our 8 reasons below for more) will be the ones to make it into production first in the US.

Here are the 8 reasons why we like GUE’s new project:

1. Located in the uranium capital of the US

GUE’s new project is in the old capital for uranium production in the USA - Wyoming was once producing most of the world’s uranium.

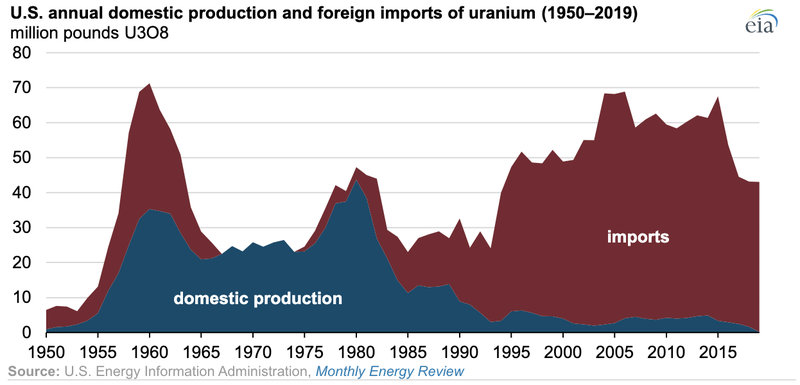

2. Domestic uranium is crucial for the US

~20% of US electricity generation relies on nuclear power. The USA is also home to the world’s largest fleet of nuclear reactors. Despite this, the country is reliant on imports for ~95% of its nuclear fuel consumption, much of which still comes from Russia and Kazakhstan... We think the US will need to bring domestic supply back online - which is good for GUE.

(Source)

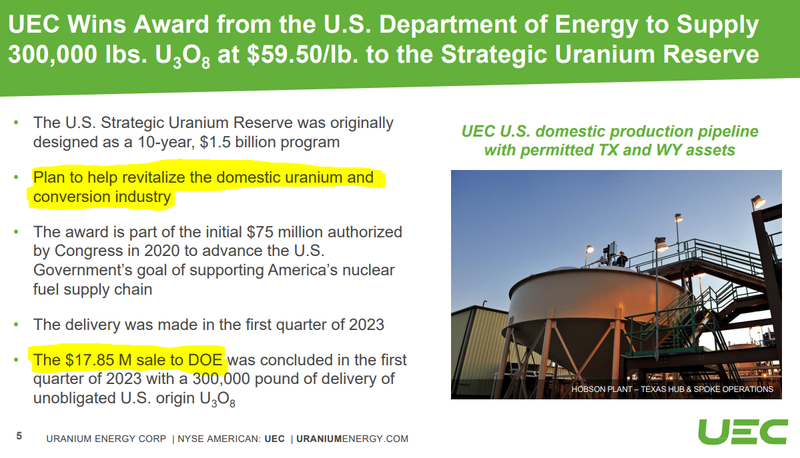

3. US Government is already allocating significant funding for the domestic uranium industry

The US government has committed upwards of US$10BN in funding to encourage new supply to come to market. More specifically, the US Department Of Energy started signing purchase orders with Wyoming based companies...

(Source)

(Source)

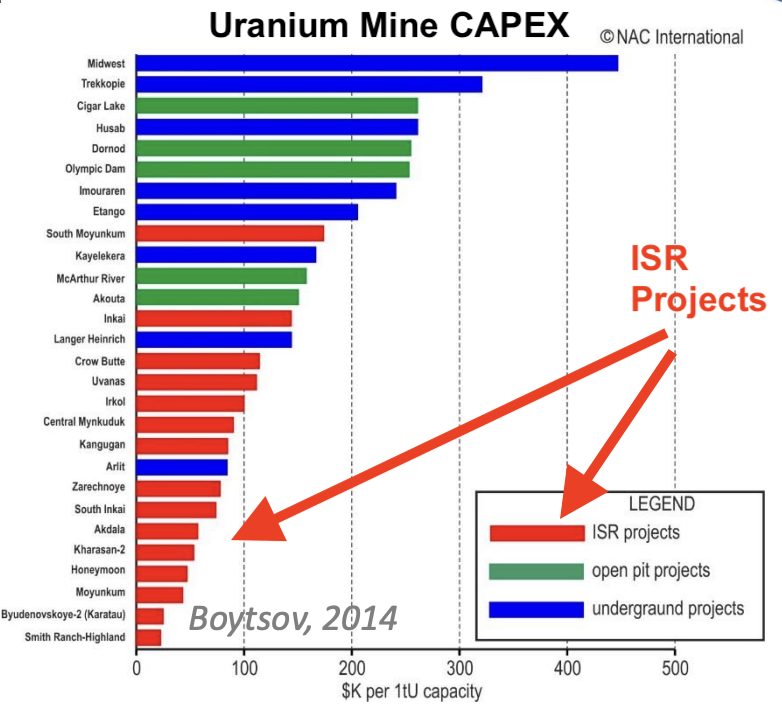

4. GUE’s new project is the lowest cost style of uranium

ISR uranium has the lowest opex, lowest CAPEX and is the easiest type of uranium to get into production. Most of the world’s uranium supply comes from ISR deposits in Kazakhstan.

(Source)

5. GUE’s project is right next to Cameco’s fully permitted ISR processing facility

GUE’s new project sits within ~80km of 5 permitted ISR uranium facilities, including Cameco’s Smith Ranch-Highland plant (the USA’s biggest ISR uranium production facility). Plants are owned by the likes of $30BN Cameco & $3.4BN Uranium Energy Corp.

6. Neighbours with plants have been doing M&A over the years

Wyoming neighbours Uranium Energy Corp have been talking about “Hub and Spoke” operating models for years now and have always said they are open to bringing new projects into their portfolio. $3.4BN Uranium Energy Corp has also been trigger happy on deals paying US$134M for a junior back in 2021 when the uranium price was only US$42/lb.

(Source)

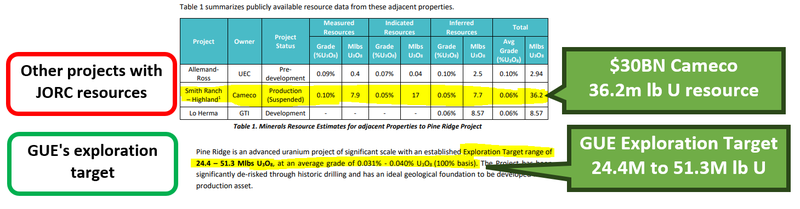

7. GUE’s project could host more uranium than $30BN Cameco’s project next door

The project has a 24.4-51.3Mlbs exploration target. IF GUE is able to define a JORC resource at the upper end of that target it could become comparable to $30BN Cameco’s project next door. So far the project has had ~1,200 holes drilled so the target is estimated with a pretty big data set of drillholes.

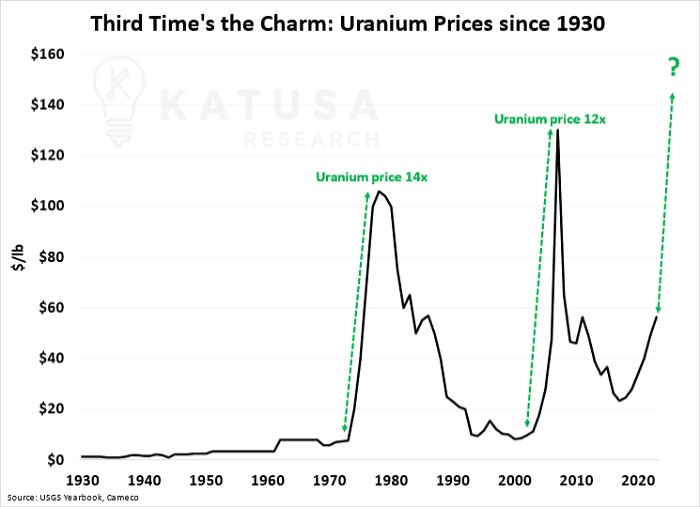

8. We really like the uranium macro thematic

Once they get moving, the uranium price tends to rip. It’s happened twice since 1970. This time we think the structural demand & forecast supply issues from decades of stalled new projects could come together to trigger a big run in uranium prices.

NASDAQ listed partner to hold 19.99% of GUE - more details

Another reason we like GUE’s new deal has a lot to do with the incoming project partner.

Upon completion of today’s deal, GUE’s biggest shareholder will be Snow Lake Resources.

Snow Lake will end up being 50-50 shareholders in the Wyoming asset along with GUE - but the interesting part of the deal was that they also decided to take a 19.99% stake in GUE.

They did that by investing $5.8M into GUE at 6.5c. They also got 14M options exercisable at 13c expiring 3 years from date of issue.

Snow Lake’s CEO Frank Wheatley will join GUE as a Non Exec Director.

We think this part of the deal could be a game changer for GUE in the long run.

We also think Snow Lake did this for multiple reasons:

1. Leveraged domestic uranium exposure for NASDAQ investors

For all the reasons we mentioned earlier, domestic uranium stories will start to resonate more and more with US investors as the government pushes to re-start its domestic uranium industry.

These US investors will look to get exposure to this thematic, and more specifically exposure with a lot of leverage to the upside.

Instead of buying $30BN Cameco or $3.4BN Uranium Energy Corp, there will be the option of picking up ~$53M Snow Lake.

We think $53M market caps on the NASDAQ are a bit like the $2M market cap companies we see on the ASX.

In fact, even a $500M market cap isn't that big on the ASX...

IF Snow Lake (and GUE) are able to make something of their asset (starting with a successful drill campaign) it could be like a $2M market cap shell on the ASX picking up and developing a project.

In which case the market cap would be multiples higher than that initial entry...

So we think there is plenty of room for a story like Snow Lake’s to resonate with US investors and re-rate off the back of that.

Ultimately, if Snow Lake’s valuation goes up, then we would expect it to trickle down into GUE.

(Which by the way, also has an OTC listing in the US)

That brings us to our second major point...

2. It’s rare to find enrichment exposure in small cap listed companies... in the US and the rest of the world.

IF Snow Lake were just going after the domestic uranium story then the 50% project ownership would have been enough.

We think the 19.99% direct investment into GUE is also a big part of the deal’s make up.

In other words, we think Snow Lake is also looking to get exposure to GUE’s enrichment tech...

Enriched uranium wasn't talked about all that much over the last few years, but prices of enriched uranium ran much harder than the raw material...

Primarily because Russia controls almost ~50% of the world’s supply...

Enrichment exposures across any exchanges are extremely hard to find.

On the ASX there are just two - Silex Systems, capped at ~$1BN which owns 51% of their enrichment tech and GUE which owns 21.9% of its tech.

Enrichment tech is usually exclusive to the biggest names in the sector and the only way to get exposure would be to own something like Cameco.

By picking up 19.99% of GUE, Snow Lake gets an ownership stake in GUE’s 21.9% owned enrichment investment (Ubaryon).

Again, the thing to note here is that Snow Lake is bringing the world’s biggest capital market’s attention to an exposure that is very hard to find in the small cap space.

In the US, seed rounds for this type of tech could value projects in the hundreds of millions of $.

If the US market (NASDAQ) investors start to show some interest in what Snow Lake is doing then we think that set of eyeballs will eventually flow through to GUE.

Remember, GUE is the ultimate owner of that 21.9% in Ubaryon.

So if the US markets want a bigger exposure to the enrichment tech, they will need to get it through GUE.

Ultimately, we think the deal is a win-win for GUE, first because of the style and location of the asset AND second because of the attention it brings to a company like GUE.

GUE getting closer to a strategic partner for its enrichment tech

Speaking of GUE’s enrichment tech.

We are expecting a big catalyst on that front over the next 3 months as well.

In February of last month GUE put out an update on its investment and said that:

GUE’s Ubaryon is targeting a transaction “with selected organisations involved in the Nuclear Fuel Cycle production industry” which have “expressed interest in reviewing technology and potentially investing”.

GUE also said that the process to identify a strategic partner was “well advanced”.

Site visits from those interested parties were planned for late February so it could be even closer now...

(Source)

GUE also said that “a potential transaction is expected to be completed in the first half of 2025”.

So inside the next 3 months we could see GUE announce a catalyst that we have been waiting for ever since we first Invested in GUE back in February 2023.

(Source)

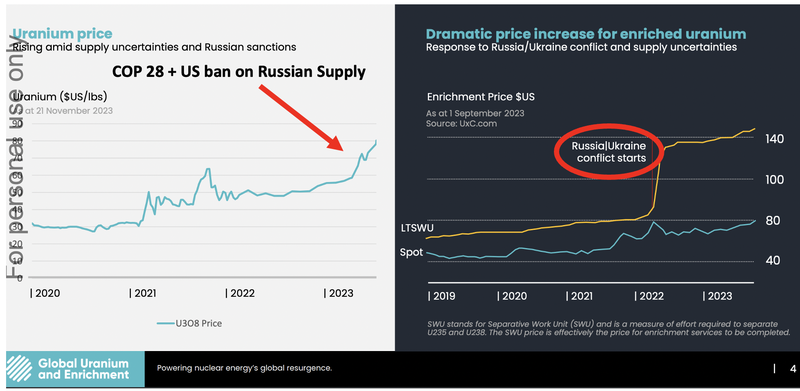

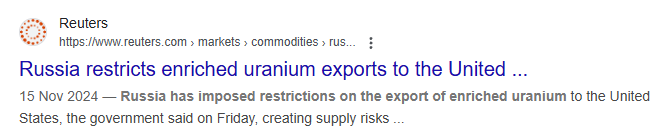

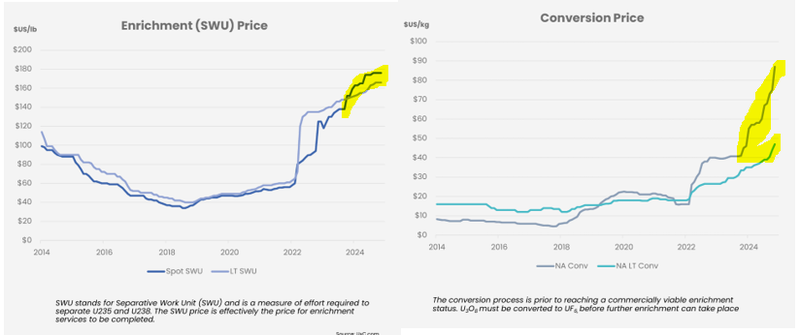

We think the sudden movement on this has a lot to do with the recent export restrictions Russia put on enriched uranium...

(Source)

(Remember - Russia controls ~50% of the global enrichment capacity, Russia and China combined control ~63%)

Those restrictions have also pushed conversion & enrichment pricing higher exponentially:

More details on GUE’s new project in Wyoming...

In the near term, we can expect an extensive drill program as GUE and its new JV partner chase down an initial exploration target of 24.4-51.3Mlbs of uranium.

Should upcoming drilling confirm mineralisation of this extent - it would make the project one of the most significant in Wyoming by size.

This project has over 1200 historical holes on it in the project in the premier US uranium jurisdiction (Wyoming).

So GUE has a lot to work with at this project together with its JV partner Snow Lake.

This is the heartland of US uranium production.

In the immediate vicinity of GUE’s new project are a number of players, including another of our US uranium investments, GTi Energy:

Just 15km away from GUE’s project, is uranium giant Cameco which has a currently operating uranium mill at Smith Ranch with a licensed capacity of 5.5M lbs.

To the north of GUE’s project is the $3.4BN capped UEC, which has the Allemand-Ross project.

Which means this is a very good part of the world to be operating in - big neighbours, existing infrastructure for production and strong jurisdictional support.

While this drilling approaches, we’ve also got a major catalyst in the offing for GUE too.

And it comes down to GUE’s investment in a uranium enrichment company...

What’s next for GUE?

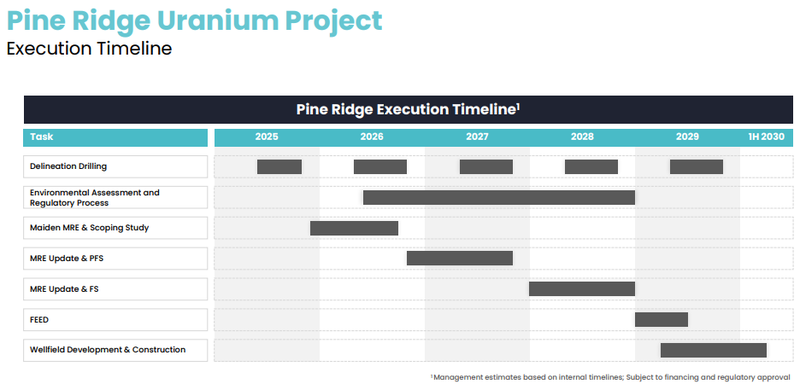

🔄 NEW Project: Drilling at new project in Wyoming to confirm and expand the initial exploration target.

Below is a slide from GUE’s latest investor deck which outlines next steps at its new project in Wyoming:

We can expect definition drilling to commence very quickly upon deal completion according to this timeline.

After that, GUE is targeting a maiden Mineral Resource Estimate (MRE) and scoping study by late this year through to next year, and then intends to go straight into an MRE update and Pre-Feasibility Study (PFS) towards the end of next year.

GUE’s other mining Projects

GUE has a number of other North American uranium exploration & development assets, here is what we are looking out for across these projects:

🔄 Project 1: ~52Mlb Resource Scoping study (coming months)

A Scoping Study is due shortly at GUE’s advanced ~52Mlb JORC resource in Colorado.

GUE indicated in September that the scoping study is due in the “coming months”

🔄 Project 2: Maybell JORC Resource (coming months)

GUE completed its drill program in October last year, now it is preparing a maiden mineral resource estimate for Maybell in another part of Colorado.

Depending on the resource size and economics, next steps could potentially include additional drilling in 2025 and a scoping study to evaluate development options.

Enrichment Technology

At the fundamental level, we want to see Ubaryon de-risk its enrichment technology both operationally and from a regulatory perspective:

🔄 Secure strategic/commercial partner for uranium enrichment technology

🔄 Further validation and extend the enrichment performance (show how well it works)

🔲 Achieve continuous operation at bench scale (scale up process)

🔲 Regulatory approvals

What could go wrong?

Due to the dynamics of the GUE JV, we now see “Funding/Dilution Risk” as well as “Exploration Risk” as two of the main risks for the company.

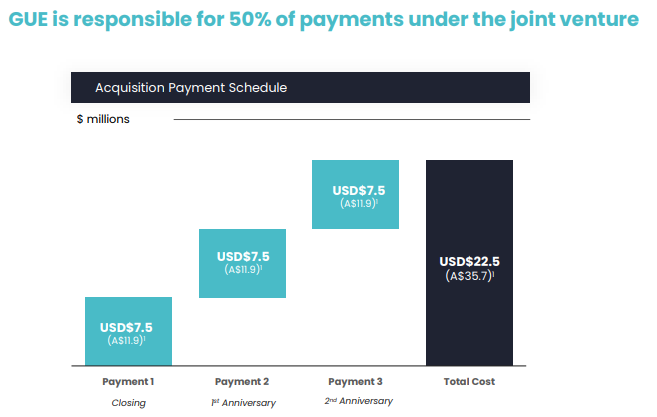

Post raise, GUE will have ~$11.5M, and be responsible for ongoing payments to the asset vendors as part of the JV agreement with its partner Snow Lake:

(Source)

GUE is also responsible for funding its portion of exploration at the project too - the above payments exclude this exploration funding.

Together, GUE and Snow Lake must spend a minimum of US$10M in exploration and development costs by the 3rd anniversary of the closing of the deal. (Source)

This means that GUE will need to raise additional capital, ideally at higher share prices in order to fund its ongoing commitments as part of the JV agreement with Snow Lake.

These capital raises may take place at a discount and incur dilution to shareholders - there is also no guarantee that these capital raises take place at higher share prices.

There is also “Deal Completion Risk” to consider as the placement requires shareholder approval and Snow Lake must also complete its due diligence on GUE and its assets on or before 2 April 2025.

Snow Lake is also reliant on capital markets to fund its share of the costs, if Snow Lake struggles to raise capital it will impact the progress GUE can make (given 50/50 project ownership).

Deals such as the one we covered today can fail to complete, and this can negatively impact share prices.

Furthermore, despite there being over pre-existing 1200 historical drillholes on GUE’s project, “Exploration Risk” shapes as another key risk for GUE.

If GUE and its JV partner are unable to confirm widespread economic mineralisation at the new project in Wyoming, this would negatively affect the share price of GUE.

Our GUE Investment Memo:

Click this link to see our GUE Investment Memo where you can find a short, high level summary of our reasons for Investing.

In our GUE Investment Memo you’ll find:

- What does GUE do?

- The macro theme for GUE

- Our GUE Big Bet

- What we want to see GUE achieve

- Why we are Invested in GUE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.