GTR boosts its uranium resources in Wyoming, as USA seeks more uranium

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 41,043,000 GTR shares and 1,579,715 GTR options at the time of publication. The Company has been engaged by GTR to share our commentary on the progress of our Investment in GTR over time.

Russia supplies about 20% of the USA’s enriched uranium.

The two countries aren't exactly best of mates right now.

Enriched uranium is what powers the USA’s nuclear power fleet.

It is responsible for a fifth of the country's electricity generation capacity.

Uranium production is now a matter of energy security.

Consequently, the US is desperately looking to rebuild its domestic uranium supply chain.

Historically, the heartland of US uranium production has been the state of Wyoming - it has the infrastructure and resources to switch this supply on again quickly.

Wyoming is also home to uranium majors like the $19BN Cameco, $1.9BN Uranium Energy Corp, $1.5B Energy Fuels and $410M UR-Energy.

It's the same state where Bill Gates is aiming to build an advanced nuclear plant in Wyoming with Warren Buffet.

We are Invested in a $12M microcap stock in our portfolio that is actively developing a series of uranium projects in Wyoming - GTi Energy (ASX: GTR).

GTR already has uranium pounds in the ground in the USA, and this morning it just confirmed a much bigger total JORC resource inventory.

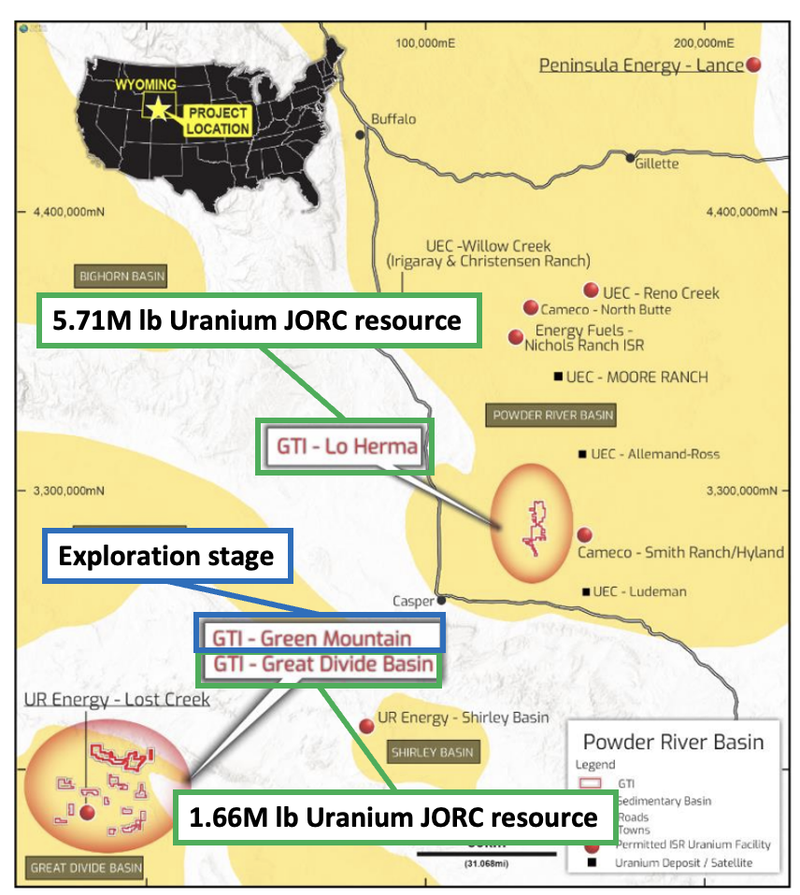

GTR today released a JORC resource at its La Herma project of 4.12mt at 630ppm for 5.71 million lbs of uranium.

This brings GTR’s total in-ground uranium resource to ~7.37 million lbs of uranium.

Remember, GTR is currently capped at just $12M.

We think that if the uranium price rips higher, GTR’s pounds in the ground will start to become much more valuable.

The question then turns to: is the uranium price setting up for a bigger run?

It might be...

Consider the following:

- The uranium spot price is threatening to break above US$60/lb

- There is growing knowledge of the US utilities coverage “cliff” (more on that later)

- Ramped up demand from new nuclear reactors

- US Department of Energy push to triple nuclear power generation

- Two new uranium and nuclear power focussed bills going through US Congress

With that in mind - back to GTR and its Wyoming uranium assets...

We think GTR might be devising a plan to attract the eye of those much bigger uranium companies in the neighbourhood.

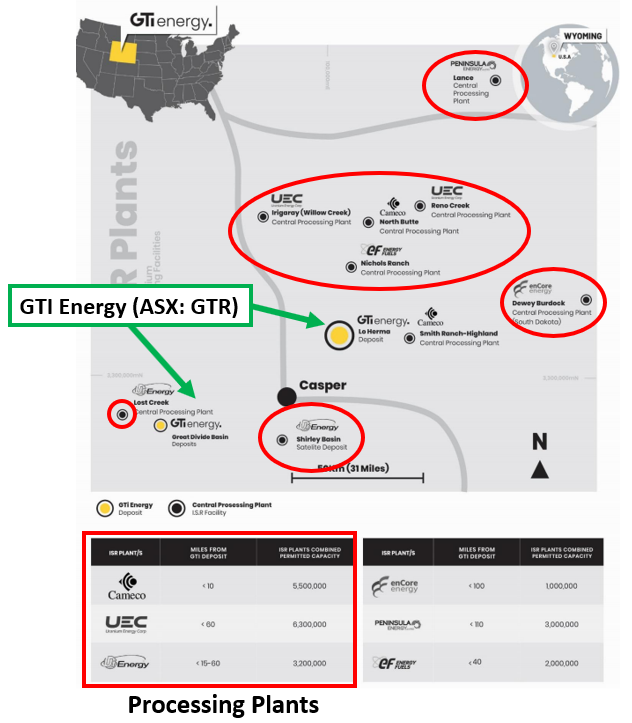

Within ~80km of GTR’s Lo Herma uranium project sit five permitted ISR production facilities (more on ISR uranium and what that is, further down).

We think if GTR can demonstrate a big enough resource size - it could start to turn up on the radars of the much bigger uranium producers in the area, who need to fill idle capacity at their mills.

Deals have been done before - GTR’s neighbour Uranium Energy Corporation (UEC) has been the most active neighbour on the Merger and Acquisitions (M&A) front with its acquisition of neighbour Uranium One.

In that deal UEC paid ~US$134M for ~100m lbs of uranium resource - ~US$1.34 per lb of uranium resource...

GTR has three projects inside Wyoming, two of which now have an in-ground JORC resource estimate attached to them.

- Great Divide Basin - 1.3mt at 570ppm for 1.66 million lbs of uranium.

- Lo Herma (announced today) - 4.12mt at 630ppm for 5.71 million lbs of uranium.

- Green Mountain - exploration stage

Across two of the three projects GTR has an in ground JORC resource of ~7.37 million lbs of uranium.

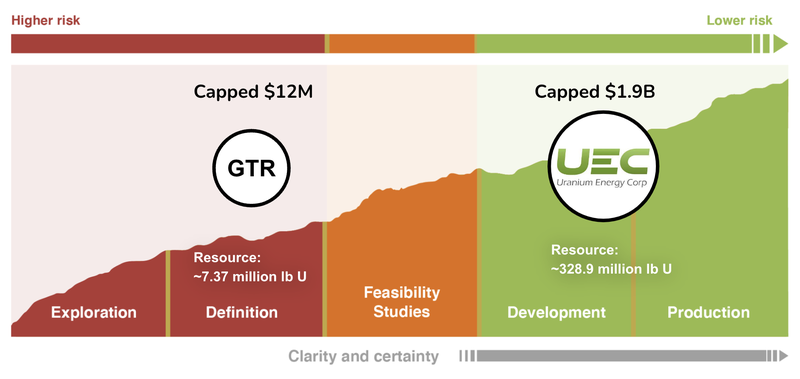

For context - Uranium Energy Corp (UEC) has ~328.9 million lb uranium resource (of which ~100 million lb is in Wyoming) and is valued at $1.95BN.

On a very basic “resource to market cap” basis:

- GTR is valued at $1.58/ lb of uranium resource.

- UEC is valued at $5.92/ lb of uranium resource.

And despite its resources, GTR is capped at less than $12M. GTR recently raised over $1.3M from a rights issue, and had $3.42M in the bank at the end of last quarter.

We participated in the GTR rights issue at $0.09, increasing our position in the company.

Of course, UEC is much more advanced than GTR in its development. Investing in early stage companies like GTR is much riskier. We have a diversified portfolio and are comfortable with the risk profile of our GTR Investment. This may not be appropriate for you.

Obviously, GTR’s projects are at an earlier stage, but the comparison to UEC provides good context on what GTR is trying to build.

Most Investment capital is currently focused on the major uranium developers/producers BUT eventually, we think capital will start flowing down to the junior explorers.

We think that once capital flows start into the uranium explorers, GTR’s low valuation will mean it has plenty of room to re-rate to the upside.

Over the last three months, the $12M capped GTR has announced two JORC resource estimates and now has:

- Projects with an in ground JORC resource of 7.37 million lbs of uranium, in the capital of uranium production inside the USA.

- Uranium projects amenable to ISR mining - the lowest cost (both CAPEX and OPEX) style of uranium mining; and

- Is surrounded by some of the world’s biggest uranium producers/developers.

Now, the focus for GTR will be on trying to grow the size of its JORC resources to a level where the project becomes of interest to GTR’s regional peers.

But before we go further, a quick history lesson is required.

The history of uranium production in Wyoming

Here’s why we think Wyoming is a good place for GTR to be defining uranium resources in.

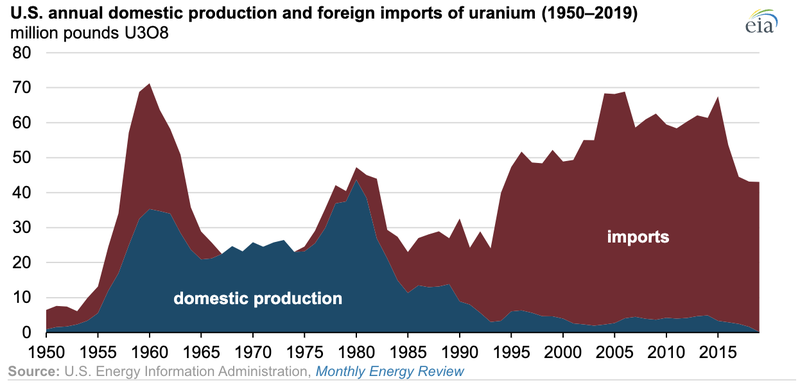

Up until the 1980s, the US - and Wyoming specifically - was the world’s biggest uranium producer.

(Source)

Over the last four decades, it lost that position as an industry leader.

Production in Wyoming, and the US, is now almost non-existent - the US now produces less than 0.5% of the world's uranium.

At the moment, ~43% of the world's uranium is produced in Kazakhstan, and ~20% of the enriched uranium used to power nuclear power stations in the US comes from Russia.

The US is now in a position where it has the world's largest nuclear reactor fleet but is almost fully reliant on imports for its nuclear fuel (uranium).

The US government quickly recognised after the start of the Russia/Ukraine war that nuclear fuel supply chains could be at risk and started making legislative moves.

The US government is considering passing two pieces of legislation:

- Bill #1: Ban Russian uranium - A potential ban on Russian uranium 90 days after its enactment.

- Bill #2 - Invest in domestic supply chains - Look to onshore nuclear fuel production through ~US$3.5BN in funding.

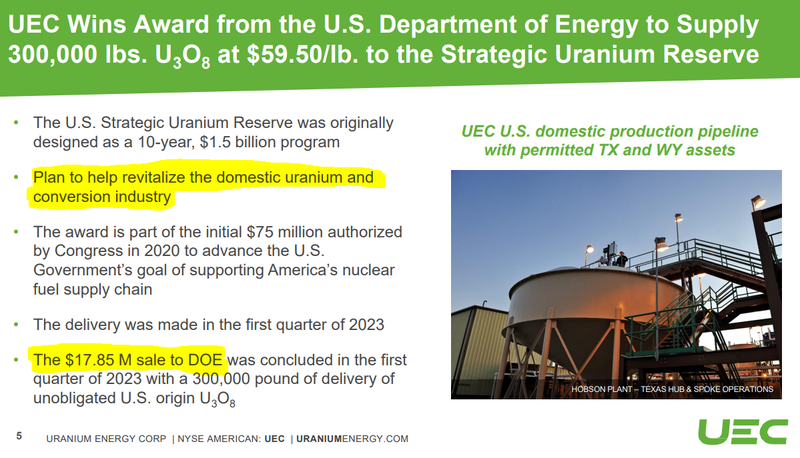

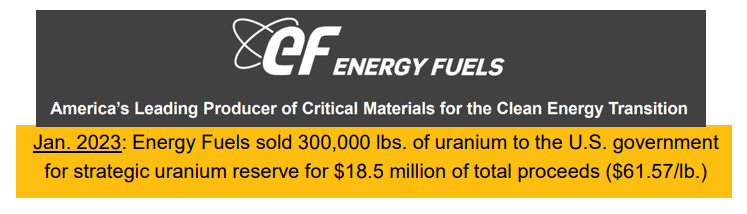

The US Department Of Energy (DOE) also signed supply contracts with the majors close to or in production:

(Source)

(Source)

(Source)

The legislative push has definitely had an impact on the appetite of the US uranium players. Companies in proximity to GTR are now readying to put their projects back into production.

- UR Energy is currently ramping up production at its Lost Creek project which sits right next to GTR’s projects.

- $230M capped ASX listed Peninsula Energy expects to have its project in Wyoming back in production in the second half of this year.

GTR is our higher risk/higher reward exposure to a resurgence in the Wyoming uranium industry.

While the market’s focus is on the producers for now, we prefer to Invest in earlier stage explorers like GTR, where we can build a position at much lower valuations, and be leveraged to future growth. However - this investment strategy is riskier, there is no guarantee we will be successful in our Investment.

Remember, GTR currently has a market cap of just $11.7M and should have ~$4.7M in cash ($3.4M at 30 March 2023 + $1.3M from a rights issue during the June quarter).

Before accounting for the June quarter spending, GTR’s Enterprise Value (EV) is ~$7M. We will get an updated June 30th cash balance at the end of this month.

We think that eventually capital will start flowing down from the producers to the explorers/developers and GTR has a low enough valuation to re-rate to the upside.

Of course - we could be wrong - there is no guarantee that our Investment in GTR will be successful.

What's happening with the U price?

We think GTR's valuation stands to gain from an upswing in the uranium price - so let's take a look at what's happening with the spot price.

After briefly cracking above the US$60/lb mark in April of last year, the uranium spot price threatened to have another go at the psychologically important threshold two weeks ago:

(Source)

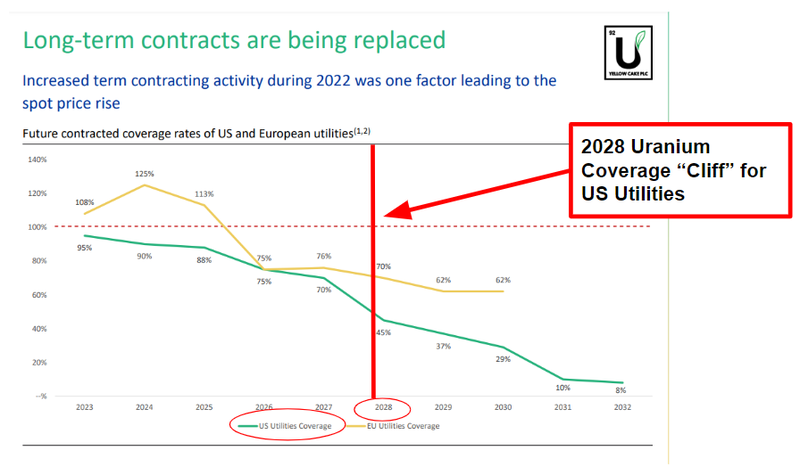

In the next chart, we can see “coverage rates” of US and European nuclear energy utilities companies.

Coverage rates are roughly how much of these utilities’ uranium needs have been contracted.

We can see that they remain relatively high among US utilities (green line) - however this is anticipated to drop off sharply in 2028:

(Source)

2028 may seem like a long way away.

But in recent testimony before the US Senate Committee on Energy and Natural Resources, Joseph Dominguez, who is president of a 21 reactor nuclear company, said that his company had enough inventory and contracts to meet the needs of its fleet of 21 reactors until 2028.

Crucially though, Dominguez added that, “in the world of nuclear fuel, 2028 is tomorrow.”

As we noted higher up, consider the following:

- Uranium spot price is threatening to break above US$60/lb

- Growing knowledge of the US utilities coverage “cliff”

- Ramped up demand from new nuclear reactors

- US Department of Energy push to 3x nuclear power generation

- Two new uranium and nuclear power focussed bills going through US Congress

To us it seems clear that there is a confluence of factors creating major macro tailwinds for GTR as it seeks to deliver value from its Wyoming uranium assets.

More on ISR uranium - what exactly is it?

At a very high level, we like the type of project GTR is looking to define and develop - ISR uranium.

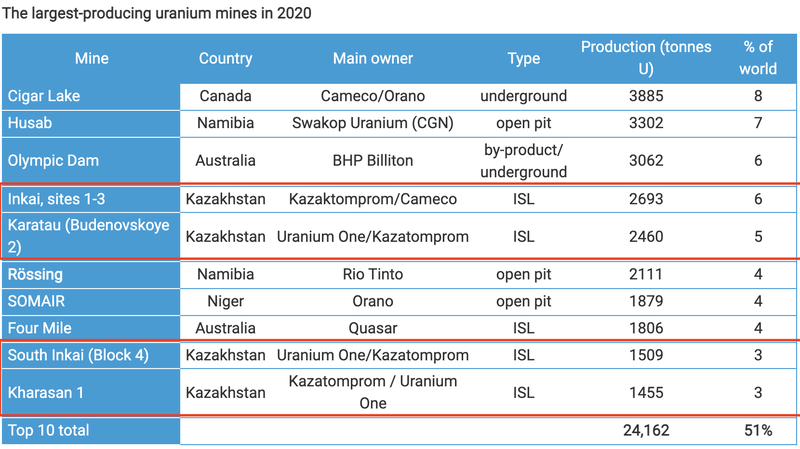

All of the major projects that are leading the restart of the US uranium industry in Wyoming are ISR uranium deposits.

ISR stands for In Situ Recoverable... uranium.

Also called Insitu Leach (ISL) mining, ISR projects are:

- among the lowest cost from both a CAPEX and OPEX perspective, AND;

- have a far lower environmental impact versus conventional hard rock mining.

ISR projects are very different to the standard method of mining which is to dig a large hole in the ground and extract minerals/metals.

Instead ISR projects are more similar to oil & gas projects - they involve pumping acid solution into the ground where the uranium resource is, dissolving the resource and then pumping it back up to surface to be processed.

(Source)

Below is a visual representation of the differences (left is a conventional hard rock uranium mine and on the right an ISR mine).

The visual differences between the two types of mining are enough to understand where these cost advantages come from.

Particularly with regards to the cost of extracting the waste rock material from conventional uranium mining before the miner can get to the valuable uranium.

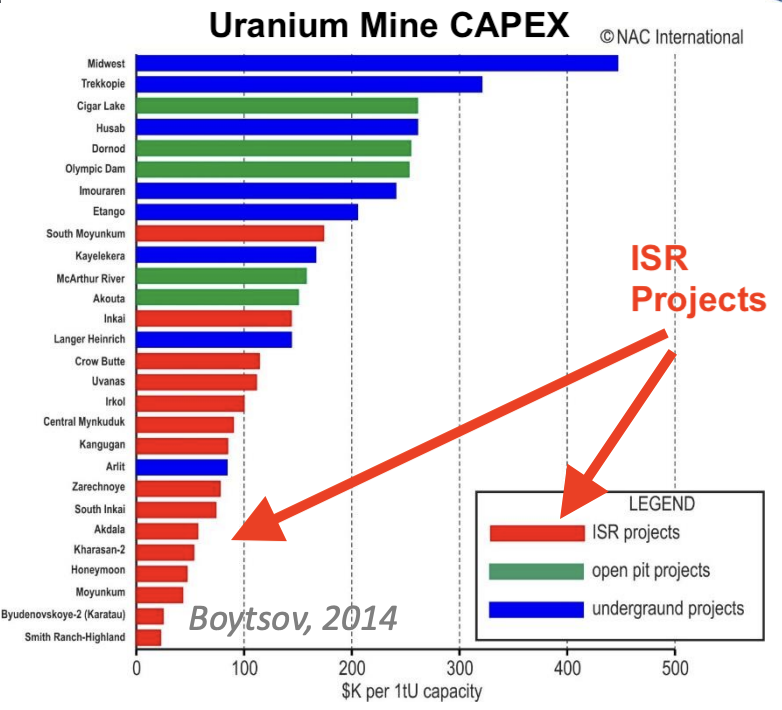

Below is a chart showing the CAPEX differences between ISR and conventional mines:

(Source)

It's also no surprise to us that the world’s biggest producer of uranium (Kazakhstan) is also operating mostly ISR mines.

(Source)

Kazakhstan accounts for ~41% of Global Uranium supply and is the lowest-cost producer in the world.

Summing up - the $12M capped GTR has

- Projects with an in ground JORC resource of 7.37 million lbs of uranium, in the capital of uranium production inside the USA.

- Uranium projects amenable to ISR mining - the lowest cost (both CAPEX and OPEX) style of uranium mining; and

- Is surrounded by some of the world’s biggest uranium producers/developers.

We think GTR is looking to develop the right type of projects in the right place at the right time.

Once GTR has defined a resource large enough in size it could make for a good bolt-on acquisition for one of the majors in the region.

GTR’s neighbour Uranium Energy Corporation (UEC) has been the most active neighbour on the Merger and Acquisitions (M&A) front with its acquisition of neighbour Uranium One.

In that deal UEC paid ~US$134M for ~100m lbs of uranium resource - ~US$1.34 per lb of uranium resource.

All we need now is for GTR to increase the size and scale of its projects which forms the basis for our GTR Big Bet which is as follows:

Our GTR Big Bet:

“Prove out a large resource base in the “uranium capital” of the USA and generate offtake or acquisition interest as the USA moves to secure local uranium supply”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our GTR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

For our summary of GTR’s progress over time and how today’s announcement contributes to our Big Bet see our GTR Progress Tracker.

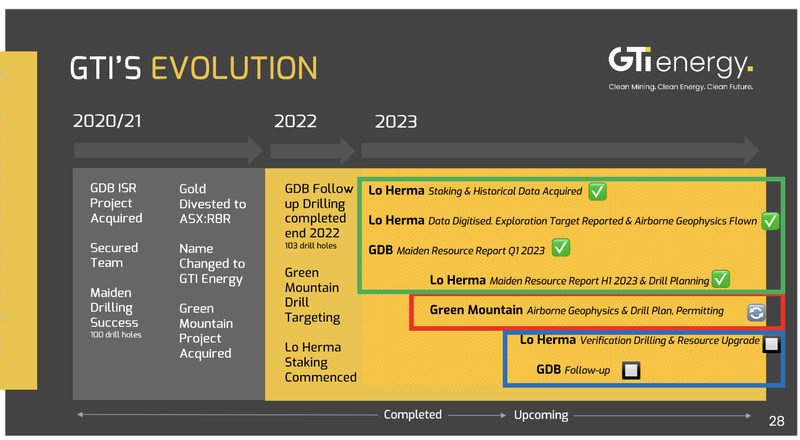

What’s next for GTR?

(Source)

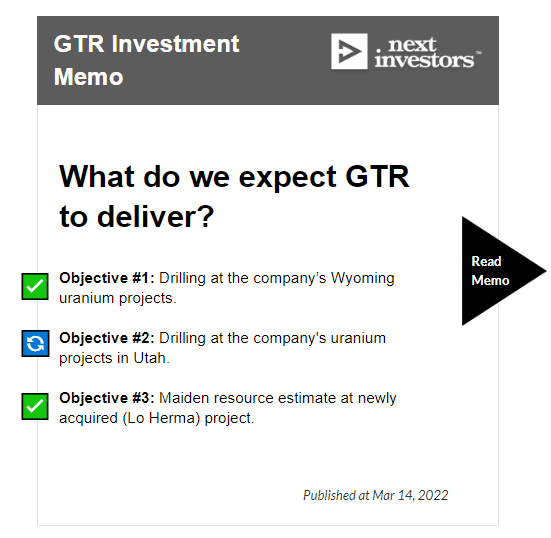

Permitting for drilling at Lo Herma (late 2023/H2 2024) 🔄

Target generation works at its Wyoming Green Mountain project 🔄

GTR is currently running an airborne geophysical survey to firm up drill targets across the Green Mountain project.

GTR expects to be drilling at Green Mountain toward the end of 2023.

The Green Mountain project shares a border with Rio Tinto and is next to Energy Fuels’ 30 million-pound Sheep Mountain uranium deposit.

GTR risks

In recent months GTR has raised ~$3.6M in capital, and while the dilution to existing holders is painful, the company has mitigated short-term funding risk, and has enough cash in the bank to build value into its projects.

As a micro cap pre-revenue explorer, over the long term, funding risk will remain, given the company isn't producing cash and will be investing its cash on exploration and development.

The bet (like all small cap companies), is that GTR can build enough value in its projects to raise capital at continually higher prices.

Even though there is no short-mid term risk, for completeness, today we still include funding risk as part of our GTR Investment Memo:

Our GTR Investment Memo

After today’s news, GTR has ticked off two of the major objectives we had set for the company as part of our initial GTR Investment Memo.

In the coming weeks, we will look to release a NEW GTR Investment Memo where we will re-establish:

- The Key objectives for GTR for the coming year

- Why we are Invested in GTR

- What the key risks to our Investment thesis are

- Our Investment plan.

Be on the lookout for our new GTR Investment Memo in the coming weeks.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.