DXB Actively Recruiting Patients Across the Globe, First Dosing Soon

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 2,825,000 DXB shares at the time of publication. S3 Consortium Pty Ltd has been engaged by DXB to share our commentary and opinion on the progress of our investment in DXB over time.

Our 2021 Biotech Pick of the Year, Dimerix (ASX:DXB), released a strong quarterly report yesterday, which showed solid progress towards proving its treatment for a rare kidney disease (FSGS) is both safe and effective.

DXB is a long-term position for us, and despite its share price performance over recent weeks, we’re quietly satisfied with its progress to date - especially on the FSGS front.

We Invested in DXB last year, with a view to seeing the share price re-rate significantly in the lead up to interim results of Phase III trials.

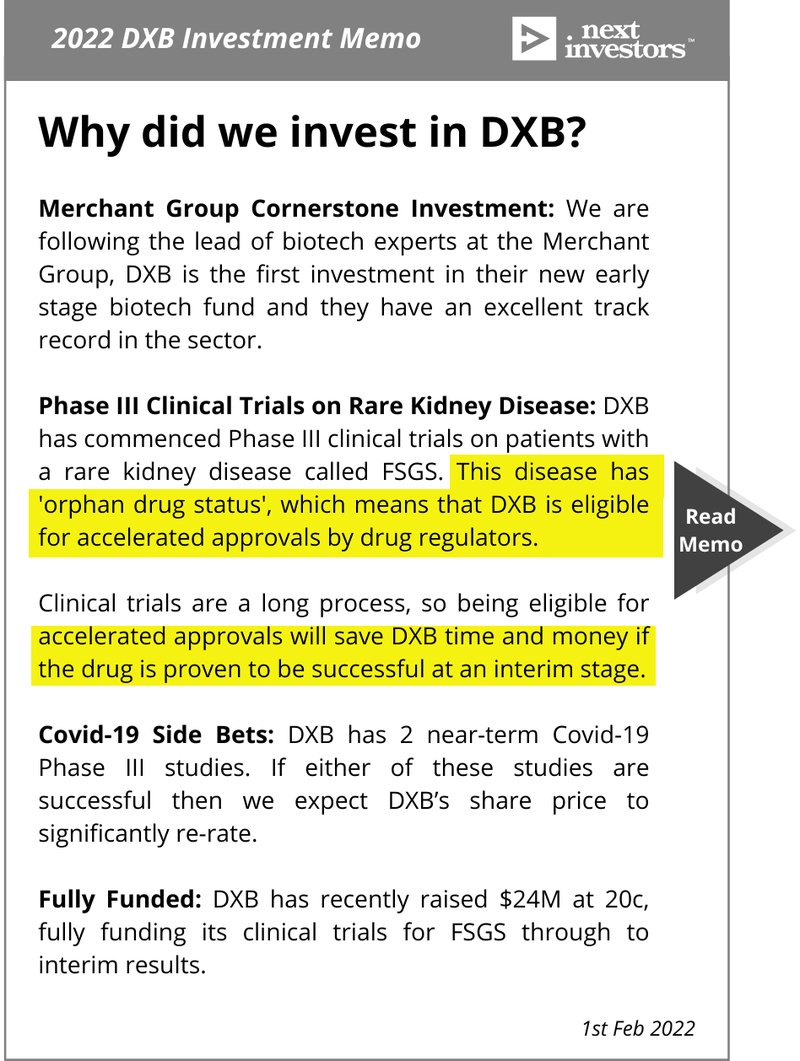

The outcome of these results are significant, because DXB’s FSGS treatment is eligible for accelerated approvals, and if successful, can fast track commercialisation of its drug.

Further below, we have analysed success and failure at the various Phases of clinical trials, and have formed an opinion that drugs that have advanced to Phase III (like DXB’s treatment) have an improved chance of success.

Of course, DXB is a small cap, high risk, investment, and there’s no guarantee that this will be a successful investment plan for us.

Focal segmental glomerulosclerosis - or more simply “FSGS”, is a nasty disease - it is characterised by a dysfunction in the part of the kidney that filters blood.

FSGS affects 210,000 people around the world, and there is no treatment currently in the market.

The disease can frequently lead to kidney failure and the need for a kidney transplant.

Kidney transplants are not cheap - in 2020, the average cost of a kidney transplant in the US was US$442,500.

In this context, DXB is aiming to provide a much needed treatment for this rare, debilitating and costly disease.

DXB intends to do so via an Orphan Drug Designation, which confers special benefits to fast track its path to market in the US and Europe.

DXB had a market cap of $46.5M at last close, and held $16.8M in cash at March 31st - which gives an Enterprise Value of ~ $30M.

DXB is at an advanced stage (Phase III trials) compared to other small cap biotech stocks that are similarly valued around these levels.

As of today, DXB has 75 sites contracted across 12 countries to conduct the trials, and the company is actively recruiting patients right now.

DXB’s strong cash balance of $16.8M stood out to us in yesterday’s quarterly report. In fact, DXB’s cash balance actually increased last quarter by $500k - due to government grants, tax incentives, and a low cash burn.

We think this cash position allows plenty of runway for DXB to deliver major share price catalysts, hopefully taking it all the way to Phase III clinical trial interim results, without needing to tap the market for cash anytime soon.

Since we announced DXB as our 2021 Biotech Pick of the Year, we’ve seen the company deliver a number of milestones, including ethics approvals, trial design, site initiations and commencing patient recruitment.

Despite hitting all of these milestones and continuing to advance its Phase III clinical trials, the DXB share price has taken a hit in recent weeks, with DXB shares now trading around 14.5c. This is well below our initial entry point of 20c, which is also the same price as the most recent funding round.

We view biotech investing as a game of patience, as clinical trials can take time to set up and deliver, and our strategy is to make long term investments which we hold for a number of years.

The recent downward share price movements may have been due to impatient investors exiting the stock, a hiccup in one of our two DXB COVID-19 “Side Bets”, and broader market softness - or a combination of all.

If you are new to DXB, it’s worth checking out DXB’s March 2022 Investor Presentation for a complete look at each of DXB’s therapies and the progress made on each.

The Phase III clinical trial for FSGS is our “Main Bet”, and the key reason for our investment in DXB, and to that end, we consider DXB’s progress to be on track.

Patient recruitment is now underway with 75 sites contracted across Australia, Asia and Europe, and US regulatory approval imminent.

With interim results slated for H1-2023, and a 6 week timeframe from recruitment to first dose, we expect DXB to have its first patient dosed soon.

In order to announce interim results by mid-2023, the company will need to complete its recruitment of the first batch of patients by the end of the year.

This is a key milestone we are looking out for.

With sites contracted and ethics approval granted in 11 of the 12 countries, we think DXB is on track to meet the anticipated time frame.

Here’s how we’ll approach the rest of this note:

- Key points from yesterday's DXB Quarterly

- Why we think DXB’s chances of success are solid

- “Side Bet” Update

- Investigator-led studies pros and cons

- Peer comparison - DXB’s potential for a re-rate

- What’s next for DXB?

- Risks, our Investment Plan for DXB and our DXB Investment Memo

Below is why we invested in DXB, drawn from our DXB Investment Memo:

More on DXB’s Quarterly:

Here’s what is new in the DXB quarterly:

- For 11 of the 12 countries planned for trials, DXB has received ethics and/or regulatory approval to conduct the FSGS study, with USA approval pending.

- Dr Ash Soman appointed as Chief Medical Officer.

- A new DMX-200 patent application submitted globally, adding patent protection through to 2041, if granted.

- Net operating cash flow for the March quarter was $500K, after a $3.7M R&D tax incentive rebate and the Australian government’s BTB program’s $300K grant

- Cash balance of $16.8M.

As we covered above, DXB is trading at an Enterprise Value (EV) of ~$30M, which we think is particularly low, given the advanced stage of its clinical trials for FSGS (Phase III).

This trial officially started in October 2021, when its first ethics approval was granted.

DXB anticipates the first interim data to be ready by H1-2023.

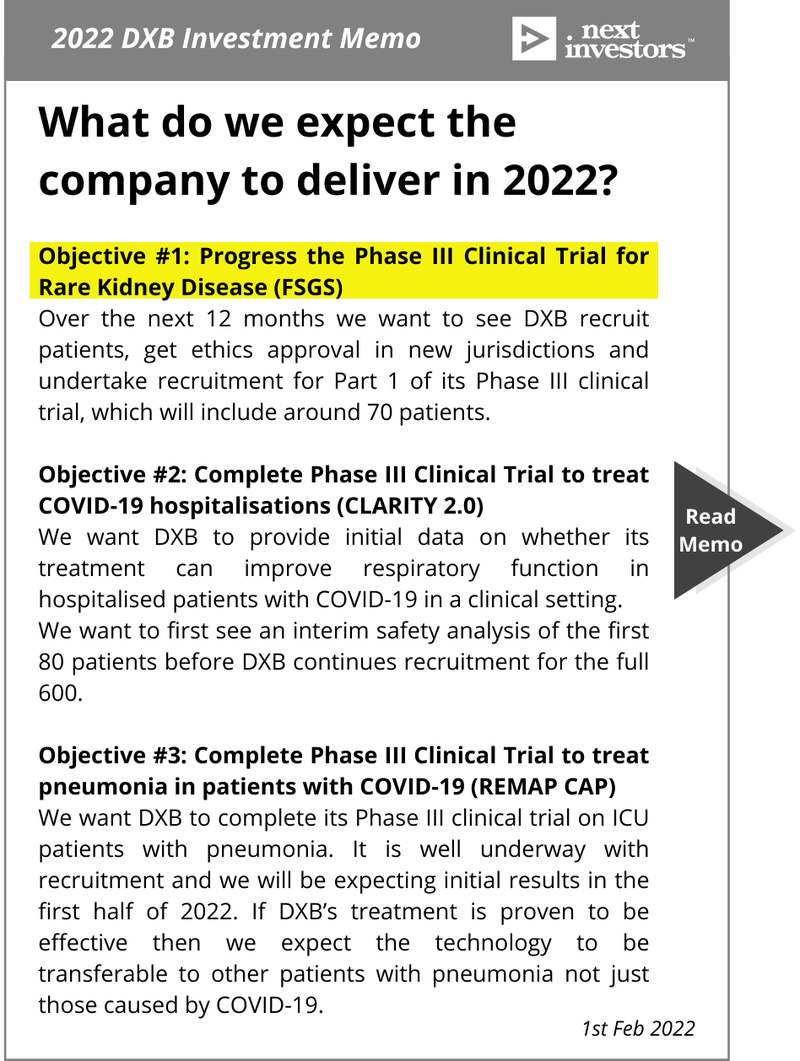

With more regulatory approvals in hand and active recruitment happening, we think DXB is making good progress on our Objective #1 that we wanted to see from the company:

Aiding DXB moving forward will be Dr Ash Soman, who was appointed as Chief Medical Officer at DXB.

Dr Soman is a highly experienced operator in the clinical trial field. Notably, Dr Soman was previously the Medical Director for the global Contract Research Organisation (CRO), IQVIA.

IQVIA (market cap ~US$39B) is a clinical research behemoth - the largest Contract Research Organisation in the world. Importantly, IQVIA is the company that DXB has contracted to run their FSGS trial.

Because of this, we think if there’s one person who can get this trial over the line, it would be Dr Soman.

Why we think DXB’s chances of success are solid

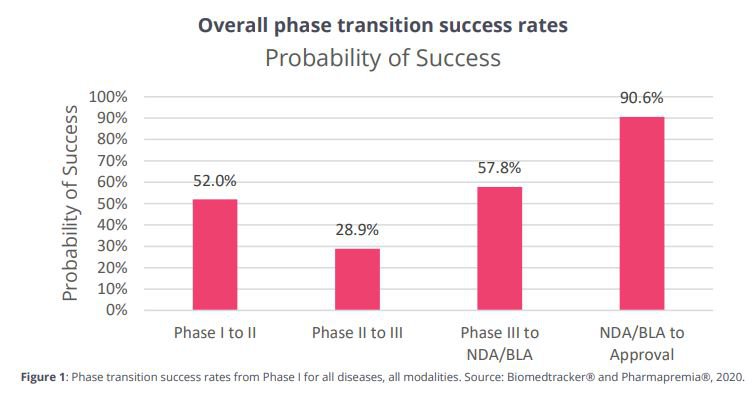

We’re going to present a chart which we think shows how remarkable it is that DXB has arrived at three Phase III clinical trials for its treatment.

And especially, how close DXB could be to delivering on our “Main Bet”, FSGS trial success.

This is the chance of success of overall “phase transition success” (in the US) for biotechs from 2011-2020:

Using expected probability here, the chance of making it from Phase I to Approval in this data would be 7.8%.

Not great - and investors know biotech investing is particularly risky.

The chance of ‘phase transition success’ from Phase II to Phase III is a mighty low 28.9% - this is the hardest leap to make for a biotech.

The good news for DXB here, is that they’ve passed that hurdle and are on Phase III.

The chance for ‘phase transition success’ is a much improved 57.8% once Phase III is reached.

While this in no way guarantees that DXB’s individual treatment for FSGS will be successful in moving past Phase III, we think that as a probabilistic exercise, the statistics from the data on biotechs in the US from 2011-2020 gives us reason to be optimistic here.

In short, we think that DXB’s chances of success here are solid.

“Side Bet” update:

There are two other near-term ‘Side Bets’ for DXB that we’re also paying attention to.

“Side Bet #1,” or CLARITY 2.0 is an investigator-led study for COVID-19 treatment that is ongoing - we think that the results from this study could be a welcome bonus for DXB investors.

“Side Bet #2” or REMAP-CAP is a second investigator-led study that was paused for severely ill patients due to a safety signal unrelated to DXB’s drug - efficacy results are still pending for patients with mild COVID-19.

Investigator-led studies have a certain set of pros and cons - with the main tradeoff being reduced cash burn vs operational oversight, something we’ll explain more below.

With COVID-19 waning in the public’s consciousness, the emphasis placed on DXB’s two investigator-led COVID trials may be diminished and consequently, this may be impacting market sentiment towards DXB.

Investigator-led studies: pros and cons

DXB’s two COVID trials were investigator-led, which means the trials happen at arms length.

Investigator-led trials generally use the investigator’s infrastructure and as a result, have reduced cost.

But while an investigator-led trial may be more practical, it also means that a certain amount of quality control is lost.

This includes control over the timeframe of the study.

So we think DXB’s decision to pursue investigator-led trials for their COVID treatment makes sense - they aren’t as central to DXB’s success as the FSGS trial.

Their FSGS trial, however, will be operating within parameters that DXB has greater control over.

The tradeoff for DXB, as we understand it, is largely between cash burn and operational oversight.

There’s a great summary of this distinction:

“Some trials are initiated by industry sponsors, such as pharmaceutical companies or clinical research organisations (CROs), whereas others, investigator-led trials, originate within research sites... Industry-sponsored trials investigate experimental drugs with largely unknown effects and typically have an explanatory approach. They tend to be suitable for the development of novel agents or combinations. Whereas, investigator-led studies are more pragmatic; they usually investigate the benefits and harms of treatments in routine clinical practice.”

Which is why we’re pleased that the FSGS “Main Bet” will be “in-house” or an industry-sponsored trial. More certainty, better data control and improved experimental conditions.

All resulting in, ideally, regulatory approval and subsequent commercialisation for DXB’s FSGS treatment.

Peer comparison - DXB’s potential for a re-rate

Regulatory approval for its treatment is the ultimate goal for DXB and we’ll place DXB’s treatment within the context of another company operating under an Orphan Drug Designation.

There are some 210,000 people around the world who have FSGS.

Each year, 1000 people each receive kidney transplants for FSGS (source), and up to 60% of patients will have recurrent FSGS after a kidney transplant (source).

Although the cost of treatment for orphan drugs is expensive (roughly $84K per year), it is often paid for by the insurance companies and much cheaper and more reliable than a kidney transplant.

The company we’ll compare DXB to today is called Neuren Pharmaceuticals.

While it's not an exact like for like comparison, as Neuren is focussed on rare neurological/developmental disorders, we think it's a good point of reference for DXB.

Like DXB, Neuren is pursuing Phase III trials for its treatment under the Orphan Drug Designation.

You can see the estimated number of patients across various geographies below:

That would be a total of 60,000 patients available for its most advanced trial.

DXB on the other hand has 210,000 patients available around the world.

This is what happened to the Neuren share price when it announced positive results from its Phase III trial:

While Neuren has the advantage of commercial arrangements with Acadia Pharmaceuticals (market cap ~US$3B), DXB may pursue a similar path to market for their treatment down the track. Particularly after DXB edges towards regulatory approval for their FSGS trial in the US and their first patient is dosed.

What’s next for DXB?

As at the start of this note, we’re looking for the first patient being dosed for their FSGS trial in the near-term.

After that, an important step would be US regulatory and/or ethics approval for their FSGS trial which would be the last of the 12 countries they’ve targeted for trials:

From there, DXB will likely reach the “execution phase” for the clinical trial, providing recruitment updates in investor presentations and quarterly reports.

The key milestone that we want to see from DXB is that it has recruited and dosed 72 patients by the end of the year - which would keep it on track for the interim Phase III study results by mid 2023.

We are also awaiting results from the two investigator-led COVID 19 “Side Bets”.

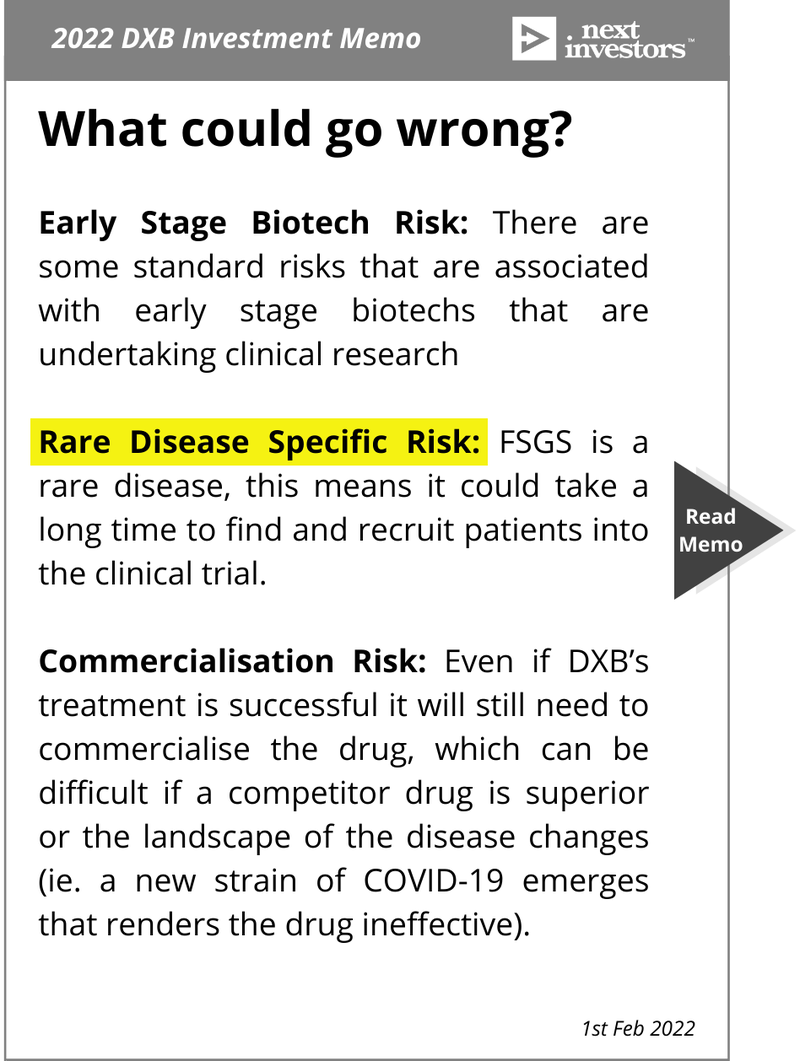

Risks, our Investment Plan for DXB and DXB Investment Memo

With the regulatory approvals for the trials in hand, DXB is addressing what we call “Rare Disease Specific Risk” as we laid out in our DXB Investment Memo:

And as per our Investment Plan for DXB, we intend to hold the majority of our DXB shares as we await the FSGS results:

In our DXB Investment Memo you’ll find:

- Key objectives for DXB in 2022

- Why we invested in DXB

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.