Cybersecurity as a Service

Overview: WhiteHawk Limited ("Whitehawk", "the Company") is an ASX-listed Arlington, Virginia, USA-based cybersecurity company, providing a range of cyber risk products, services, and solutions. WhiteHawk developed and operates the first online cybersecurity exchange enabling businesses of all sizes to manage cybersecurity threats. The Company is evolving its portfolio of cybersecurity systems and services and has secured contracts with key US federal government departments, along with Fortune 500 companies, top US financial institutions, major insurers, manufacturers, utility providers and a top Defence Industrial Base (DIB) company.

![]()

Catalysts: New and extended contract announcements and partnerships have proven to be share price catalysts for WhiteHawk. This was demonstrated with the recent growth in customer contracts through its expanded product line and new SaaS product via its partnership with a major global consulting firm. WhiteHawk’s product lines and services continue to be sold and executed via cloud based online platforms, SaaS services and virtual consultations. Management has confirmed it is well-positioned to continue to support its customers and to engage with future customers seamlessly and effectively throughout the current global pandemic. Additional working capital facilities totalling A$1.9m subject to shareholder approval, provide additional funding capabilities. New contracts will boost the Company's recurring revenue base and have the potential to be value drivers.

Hurdles: While the Company announced sufficient cash reserves through 2021, additional external capital may be required to ensure the long-term sustainability of the business. There is no guarantee that capital can be procured at favourable terms to shareholders. Despite implementing a range of mitigation initiatives, the greater impact of COVID-19 on the global economy and WhiteHawk remain somewhat uncertain and there is no guarantee that ongoing growth can be achieved. The Company may be subject to increasing competition in a growing market.

Investment View: WhiteHawk offers exposure to the growing global cybersecurity market via its cybersecurity exchange. We are attracted to management’s industry connections, the Company’s existing contracts with U.S. federal government departments & Fortune 500 companies, its partnerships and sales pipeline. WhiteHawk has a firm financial position and while the Company remains reliant on external capital, recent funding supply should provide management with near-term resources to pursue growth opportunities. The Company’s existing revenue-generating contracts are supported by a deep sales pipeline in the US across diverse sectors including the federal government, financial sector, Defense and Industrial Base as well as manufacturing and utility sectors. As the market for cybersecurity continues to grow, WhiteHawk is in a unique position to take advantage of increased cybersecurity spend through its Cybersecurity Exchange and solutions. While the long-term growth potential of the business remains to be validated, we believe that a series of favourable quarterly updates along with any new contract or partnership announcements could drive significant interest towards the stock and we, therefore, initiate coverage with a view to providing further updates in the future.

COMPANY & ASSET OVERVIEW

Launched in 2016, WhiteHawk commenced operations as a cybersecurity advisory service and has since expanded its offering to cloud-based SaaS solutions, simplifying how companies purchase cybersecurity solutions.

Today, WhiteHawk enables companies to identify and mitigate their priority cyber risks on an ongoing basis with demonstrated cost and time savings. Leveraging the online Cybersecurity Exchange platform and SaaS partners WhiteHawk works to identify, prioritise, and mitigate cyber risks that impact client revenue and reputation. It partners with top commercial technologies and SaaS services that leverage AI techniques and open data sources.

WhiteHawk’s expanded product line now includes the Cyber Risk Program, a software as a service (SaaS) product for mid-sized and large enterprises to defend against cyberattacks by monitoring, identifying, prioritising, and mitigating cyber risks. The company’s Cyber Risk Radar is an annual SaaS subscription that manages the business and cyber risks of an enterprise’s partners and supply chain companies. WhiteHawk’s annual Cyber Risk Scorecard subscription consists of quarterly updates combined with cyber consultant sessions in tandem with the delivery of each scorecard. The Cyber Marketplace is an online resource, offering hundreds of best-of-breed, affordable products and services catering to cyber risk mitigation needs of small to midsized businesses and organisations.

Founder and CEO, Terry Roberts, is a former deputy director of US Naval Intelligence and brings over 30 years of experience as a US national security and cyber intelligence professional. This includes time as a US Naval Intelligence Officer, a Department of Defence Senior Executive and as a Cyber Engineering, Architecture and Analytics industry executive.

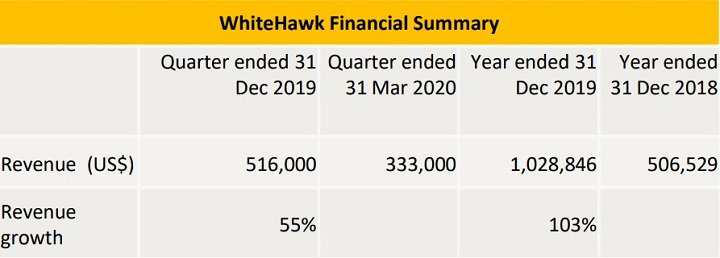

Whitehawk generated revenues of US$1.03 million (A$1.5M) during financial year 2019, a 100% gain in the prior year, of which US$867k (A$1.32M) were with two key customers in the US and US$161k (A$245k) in government contracting. Issued capital stands at US$11.2 million (A$17M) as of 31 December 2019.

The first quarter 2020 revenues of US$516k (A$787k), were up 55% from US$333k (A$508K) in Q419 and up 282% on pcp. WhiteHawk has taken a lean approach to expenses, reducing its cash burn during the quarter while increasing gross margins. It finished the first quarter with a strong cash position of US$1.5 million (A$2.3M) and a solid pipeline of sales contracts. The Company has additional Working Capital facilities available from RiverFort Global, comprising a A$400k loan and a A$1.5m combined placement and equity (subject to shareholder approval at the May 2020 AGM).

Following a period of accelerated investment in product and sales channel development, WhiteHawk is on track to again deliver growth in 2020. A recent partnership with a major global consulting firm has delivered an additional sales channel that has generated annual 2020 SaaS subscriptions of greater than US$400k, as of 15 April. The table below is a summary of WhiteHawk’s recent financial performance and highlights the growth achieved over the prior corresponding period.

OUTLOOK

WhiteHawk has made great advancements in the evolution of its business over the past year and is positioned for strong scalable growth. The Company has existing revenue generating contracts and a strong sales pipeline in the US. These span diverse sectors including US federal government, US financial sector, US Defense and Industrial Base (DIB) and the US manufacturing sector.

The Cyber Risk focused business model enables WhiteHawk to remain agile, to partner with the best open data and AI enabled platforms, and to continually evolve to align with customer needs and appetites. The Company now has optimal positioning in the cyber risk market, across companies and organisations of all sizes in the US and is seeking to increase business internationally.

WhiteHawk is on track to again deliver strong revenue growth in 2020. It has completed the online integration and automation of its product lines and added a major global consulting firm as a sales partner. Its partnership with Sontiq/EZShield provides a scalable business model and seamless access to thousands of businesses needing to address their digital risks. Plus, the new rules around cybersecurity of US government supply chain and contractor companies should generate new business.

THE BULLS SAY

- Following a period of accelerated investment in 2018 and 2019, the business is well-positioned to take advantage of growth opportunities in the cybersecurity market.

- Rising revenues, including recurring SaaS annual revenues and US government contracts that can become annuities.

- Has multiple US federal government contracts that are very difficult to secure, plus large private sector counterparties, reflecting the quality of the product and the reach of the management team.

- The need for effective cybersecurity remains amid the global coronavirus pandemic. WhiteHawk products and services continue to be sold and executed via cloud-based online platforms, SaaS services, and virtual consultations.

- And while automated services and products and that Cyber Security is more essential than ever

- Any additional contract announcements that will improve the company's recurring revenue base have the potential to be a major value driver.

- Successful execution of Whitehawk's growth strategy could drive significant interest toward the stock.

THE BEARS SAY

- While the Company announced sufficient cash reserves through 2021, additional external capital may be required to ensure the long-term sustainability of the business.

- There is no guarantee that capital can be procured at favourable terms to shareholders.

- Despite a range of mitigation measures implemented by management and while automated services and products make cybersecurity more essential than ever, the greater impact of COVID19 on the global economy and Whitehawk remains uncertain and there is no guarantee that ongoing growth can be achieved.

- Some contracts, particularly with key U.S. federal government departments have been slow to finalise and execute.

- The Company may be subject to increasing competition in a growing market.

- The Company's financial position could deteriorate if operational targets are not achieved.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.