CND: TEA to full license conversion in coming weeks to rerate $12M CND?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 48,634,867 CND Shares and 13,675,000 CND Options at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Why is this oil & gas explorer capped at just $12M?

And what key event is about to happen in the coming weeks that could change that?

(The answer is below - and no, it’s NOT drilling...yet)

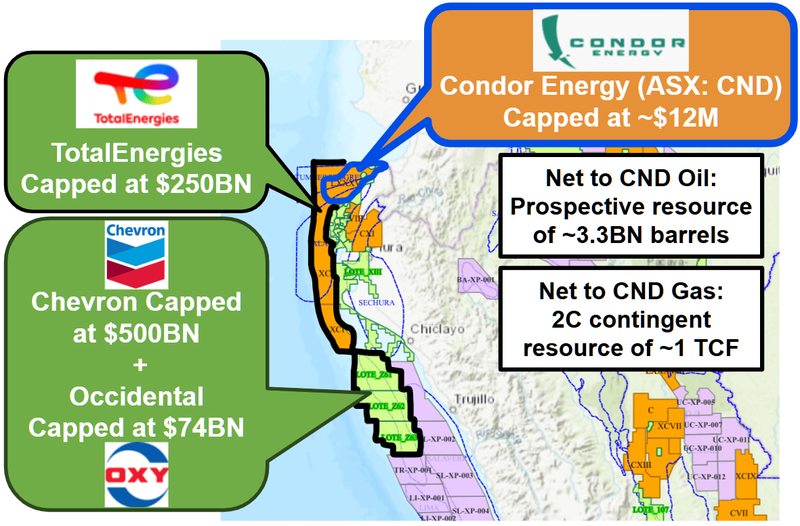

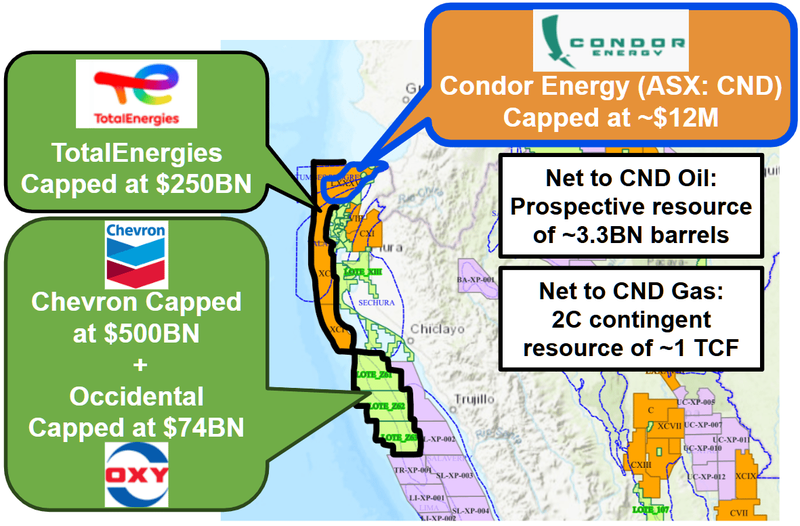

Our microcap Investment $12M capped Condor Energy (ASX:CND) has a Technical Evaluation Agreement (TEA) on 100% of an offshore exploration block in Peru, with:

- 3.3 billion barrels of unrisked prospective oil resources (2U), AND

- An existing 1 trillion cubic feet gas DISCOVERY (contingent resource, 2C).

In the coming weeks we are hoping for the Peruvian government to convert this TEA agreement to a full Exploration License, which will allow CND to drill test its oil prospects (more on this imminent share price catalyst below).

The gas is an existing discovery that has previously been flow tested.

The oil is the “swing for the fences” exploration, with billions of barrels of exploration upside, right next to producing fields. CND has identified over 20 leads and prospects so far.

CND’s block sits inside Peru’s Tumbes and Talara basins which are responsible for ~1.7BN barrels of oil production historically.

Tiny CND is surrounded by ~US$180BN energy supermajor TotalEnergies:

(source)

CND last traded at 1.5c. We put cash into the most recent CND placement at 1.7c a few weeks ago.

So why is CND capped at just $12M?

For the last 3 years, CND has held something called a Technical Evaluation Agreement (TEA).

It's basically a “look before you buy” agreement with the Peruvian government, for both parties.

A TEA lets a company study an offshore area's seismic and geological data for a couple of years, with no obligation to drill.

If the company likes what it sees, it gets first crack at converting the area into a full exploration licence - it's the cheap option ticket before committing serious capital.

Peru will also want to know that whoever is granted a license is going to explore and progress the project.

Currently TotalEnergies ALSO has TEAs over its blocks that surround CND.

During this “TEA time” (last ~3 years), CND has been reprocessing seismic data, new geological modelling and updating the resource estimates over the project. (source)

Everything is looking really good, but we think the market is waiting for CND to get the full license and officially own the blocks.

(for example, you wouldn't buy a car from somebody who tells you they are currently just taking it for a test drive and don't own it yet - investors and supermajors probably think the same thing about CND)

We think the market will rerate CND IF they convert their “look before you buy” TEA into a full license.

Meaning they own the project, can deal on the project (ie: do a farm out), and can also drill.

(We Invested in CND well before the “TEA to license” conversion event, to try and capture the upside if the full license is granted, and accepted the risk if the license is not granted)

CND’s TEA status hasn't stopped interested parties taking a closer look however. Back in April 2025 CND said it had “multiple parties in the dataroom” and that a “farm out process had commenced”. (source)

So hopefully a lot of the warm up work for anyone interested has already been done, and IF/when the license is granted, things can start to happen quickly...

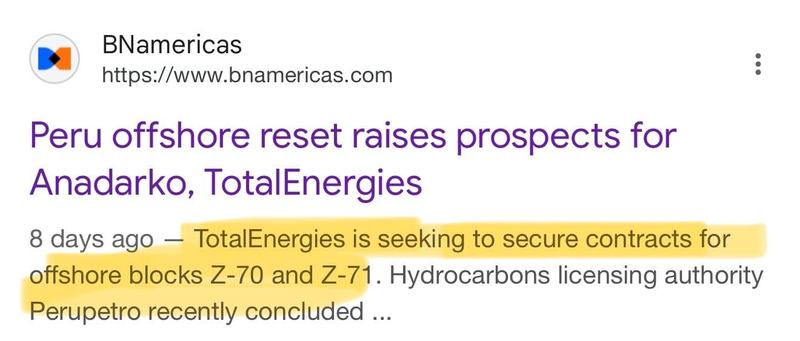

Eight days ago we saw reports that TotalEnergies applied to have its TEAs converted to a full license.

(source)

So it looks like US$180BN TotalEnergies is getting serious about Peru.

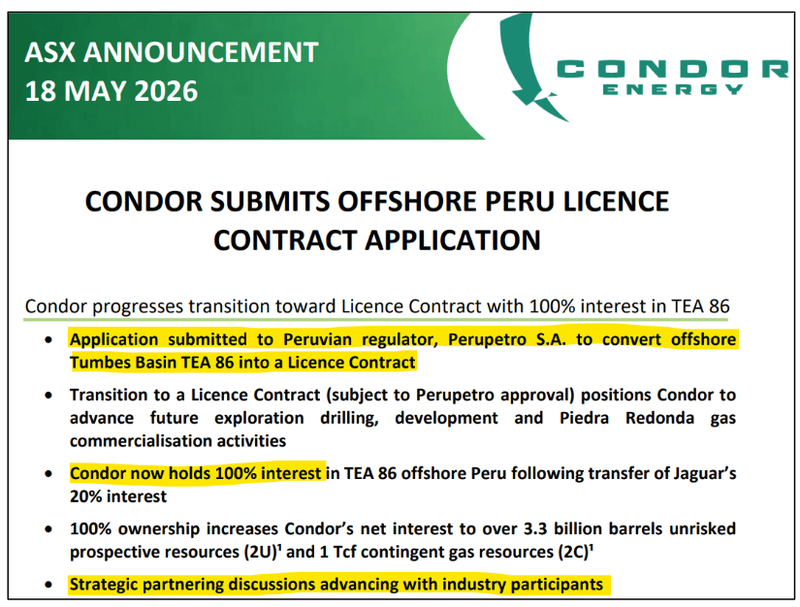

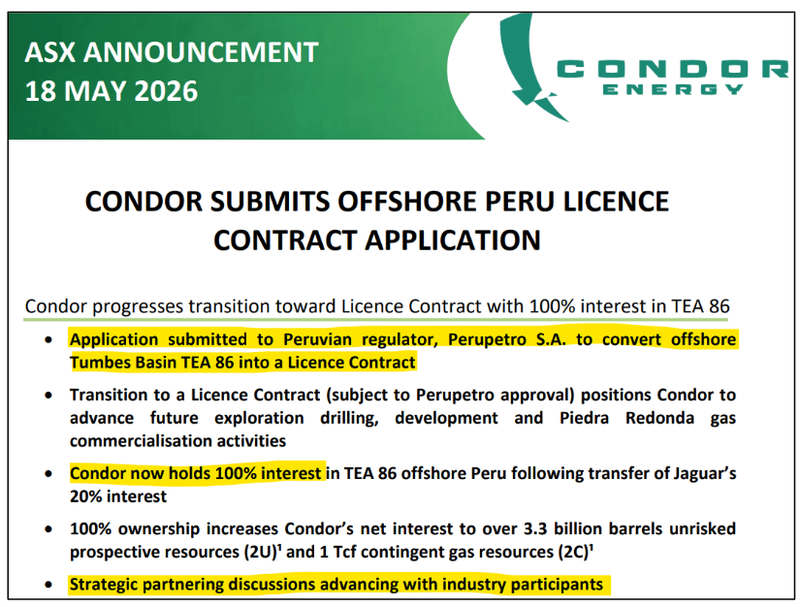

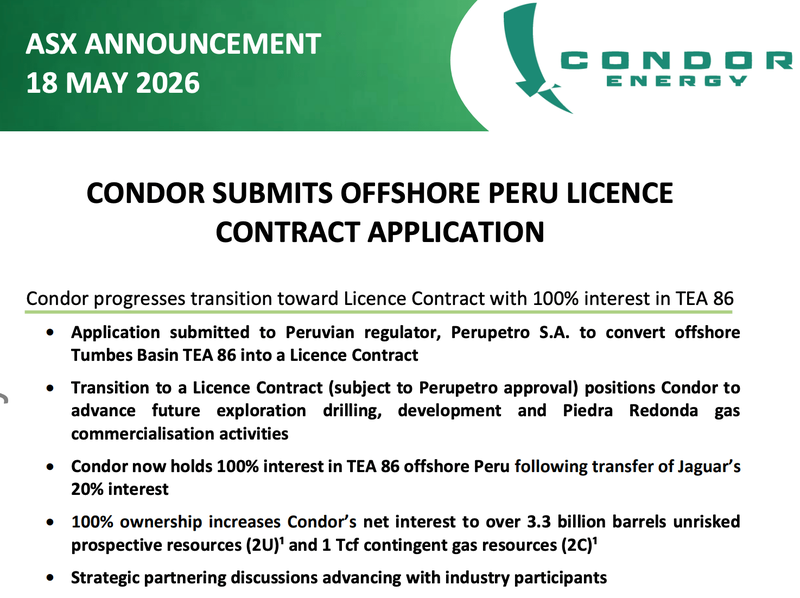

And in May CND announced it had made its submission to convert its own TEA into a license too.

(source)

We think IF CND license is granted, the market and super majors will instantly move from seeing CND as test driving a car, to being the owner of the car - now in a position to make things happen with said car.

CND has not guided on how long the government response could take - so it could be weeks, or months, we don't actually know for sure.

But we are watching closely because we think a successful conversion of CND’s TEA into a full license will re-rate CND.

Plus we are also watching for TotalEnergies TEA applications to be converted to a license.

Oh and by the way... oil prices popped last night on new Iran attacks - we certainly don't think that rollercoaster is finished just yet.

Now we wait for news on the CND license application result.

We wonder if CND’s offshore Peru neighbours Chevron, Total and Occidental are watching too?

CND was the earliest entrant into Peru - supermajors have come in since then

CND came into Peru back in 2023, since then we have seen:

- US$180BN supermajor TotalEnergies come into Peru - surrounding CND’s block and now going for a full licence contract over the blocks.

- US$500BN Chevron come into Peru, AND

- US$74BN Occidental come into Peru - They have already shot a big 3D marine seismic survey and in 2025 brought in a partner (Westlawn) to help fund drilling. (source)

- The most recent entrant is $40BN Spanish major Repsol which signed agreements with the regulators only a few weeks ago.

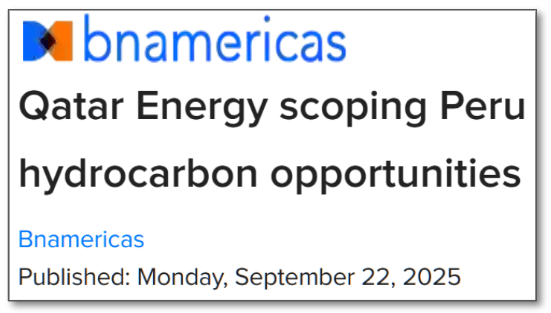

There were even rumours back in September 2025 that the Qatari’s were scoping opportunities in Peru.

(source)

All of the supermajors that have come into Peru - did so AFTER CND.

(source)

We think the majors coming into Peru is a precursor for the opening up of the offshore oil and gas industry.

And somehow $12M capped CND has managed to wedge itself in and amongst the big boys.

On a block that we think is extremely “dealable”.

By that we mean IF any other supermajor wanted to come into Peru they could just partner with CND on either:

- The 3.3BN oil unrisked prospective resources - big enough to warrant drilling AND if a discovery is made - plenty of follow up targets to drill.

(source)

- A 1.1TCF gas discovery (contingent resource) that has seen a development scenario considered for it back in 2006.

Someone could hypothetically come in for the gas alone OR come in for the oil alone.

The big appeal will be for someone big enough to come in and develop the gas while going for moonshot exploration on the oil.

We also like that there is a precedent for big deals being done offshore in Peru too.

Back in 2009, KNOC (the South Korean National Oil Corporation) and Ecopetrol (the Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND's block. (source)

Then there was the farm-out the previous owners of CND’s block ($960M Karoon Energy) did a deal with Tullow Oil back in 2019.

And the most recent one is the one that Occidental did with Westlawn...

A quick side note - CND just a few weeks ago appointed the ex- CEO/MD Dr Julian Fowles as its non-exec director.

(surely he will have a rolodex of companies he knows might be interested in the asset from his time at Karoon)

We think there is a very good chance CND is able to attract a farm-in partner for the project again.

Knowing all of this... why is CND capped at just ~$12M?

It doesn't really make sense for an existing 1 TCF gas discovery + 3.3BN barrels of oil prospects trades at a ~$12M market cap...

We think the reason it does comes down to the permitting status of CND’s block.

Up until now, CND hasn't actually "owned" the right to drill and develop its block.

It held something called a Technical Evaluation Agreement (TEA).

The TEA was basically a “look before you buy” agreement.

It allows a company to study an offshore area's seismic and geological data for a couple of years, with no obligation to drill.

CND spent the last ~2.5 years Reprocessing seismic data, new geological modelling and updating the resource estimates over the project. (source)

And then in May CND made its submission to convert the TEA into a license contract:

(source)

Ultimately, the licence contract is what gives CND the right to drill and develop the block.

And we think IF successful - that grant alone could be a major catalyst for a re-rate in CND’s share price...

(No guarantees of course - Perupetro approval is not guaranteed, and timing can slip. More on that in the risks section.)

We also think the licence contract opens the door to deals being done on CND’s block.

(understandably, anyone committing to a farm-in would have wanted to see CND have tenure over the block)

In April 2025 CND said it had “multiple parties in the dataroom” and that a farm out process had commenced. (source)

So hopefully a lot of the warming up of interested parties has already been done And IF/when the license is granted things can start to happen quickly...

IF CND secures the licence contract we think CND could:

1. Do a deal on its 1.1TCF existing gas discovery - Maybe CND gets a free-carried interest in an asset that could generate revenues in a reasonable timeframe? We note Promigas - the gas distributor for 94% of Peru's market - is already studying the asset under an MoU. (source),

OR

2. Do a deal on its 3.3BN barrel oil exploration assets - Maybe CND lands a free-carried interest in a well that's fully funded by a farm-in partner.

OR maybe it's a combination, a partner that wants BOTH the oil and the gas.

Ultimately we think that IF CND lands that licence contract it will have big enough targets and an existing discovery large enough, to farm-down to bigger parties BUT retain something company making... especially from the current $12M market cap.

We have also seen how farm-ins have triggered re-rates in other offshore explorers before.

A farm-in with Woodside is what triggered offshore explorer Pancontinental to run from a ~$7M market cap to ~$230M.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Another example is Finder Energy signed a farm-in deal and saw its share price run from 18.5c to a high of 66c.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We look at CND in two ways right now

Scenario A:

- We have exposure to an EXISTING 1.1 Tcf gas discovery - one that's flowed gas before and got close to development in the past.

In that scenario we get the 3.3 BN barrels of oil exploration upside as a “free option”.

Scenario B:

- Exposure to 3.3 billion barrels of oil exploration targets offshore Peru

In that scenario we get the 1.1TCF existing gas discovery as a “free option”.

Either way we think the current $12M market cap is highly leveraged to a re-rate (IF that licence contract lands).

Our CND Big Bet

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

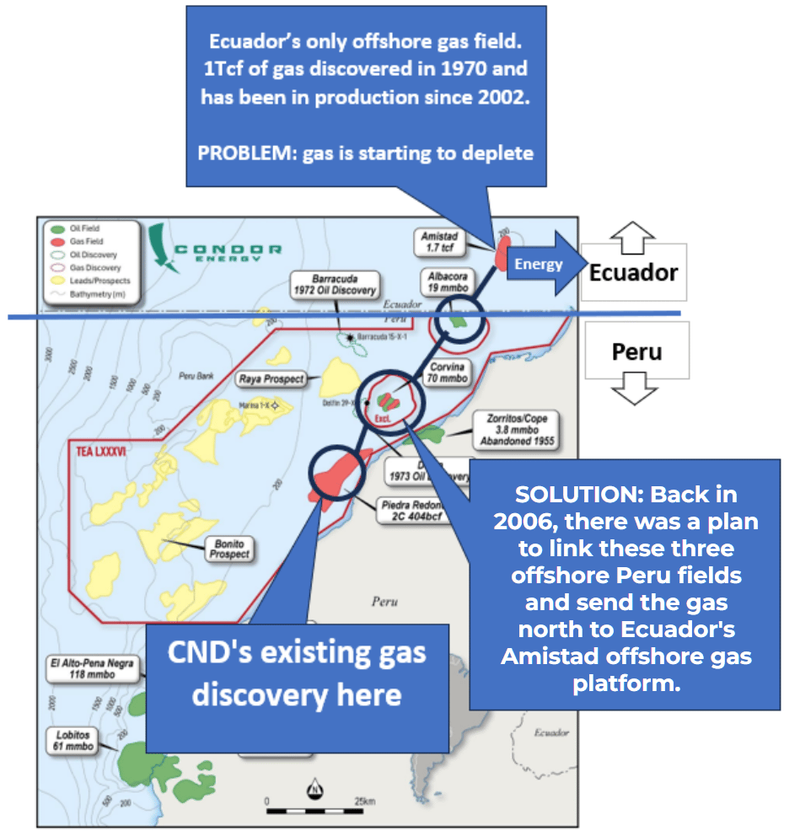

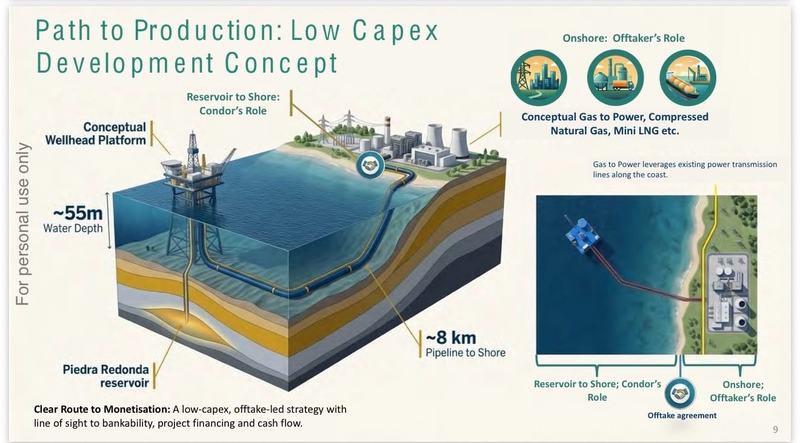

Deep dive into CND’s existing 1.1TCF gas discovery

This is the "advanced-stage" half CND’s block.

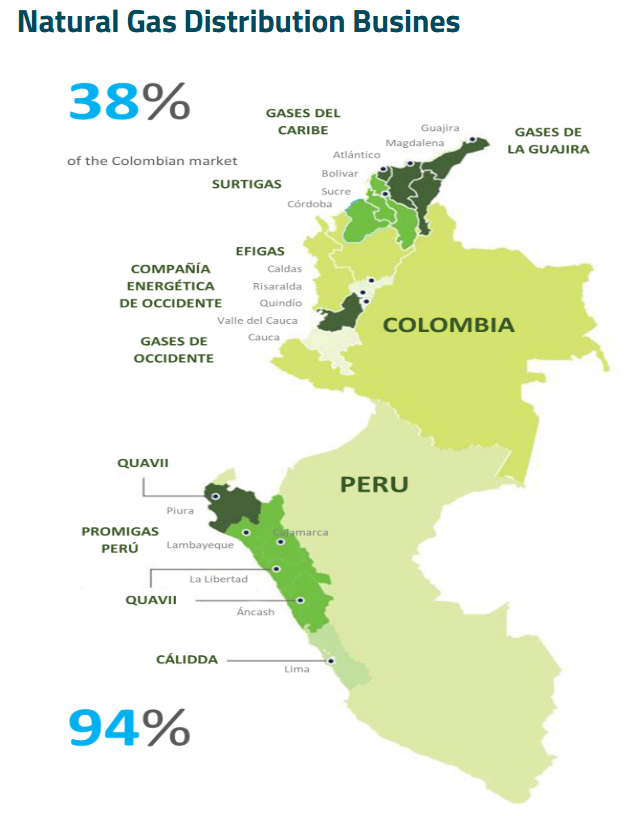

CND's Piedra Redonda gas field is a 1 Tcf discovery and CND has an MoU signed with Peru’s biggest gas distributor - Promigas Peru on the asset.

Promigas manages, maintains and builds gas infrastructure across northern Peru - supplying gas to homes, businesses and industrial facilities.

They supply natural gas to 94% of the Peruvian market and 38% of the Colombian market. (source)

(Source)

The deal with CND is around a potential offtake from CND’s existing gas discovery at Piedra Redonda.

CND’s project has a 1 Trillion Cubic Feet (Tcf) discovered gas field and together with Promigas will do studies on:

- Evaluating gas production potential

- Assessing infrastructure and delivery options

- Defining integration and commercial pathways

Basically, CND’s MoU with Promigas is to work out how best to take gas from its existing gas field and bring it to market.

One thing that stood out to us was CND’s comment on “Promigas’ efforts to expand access to natural gas in Peru’s northern regions”.

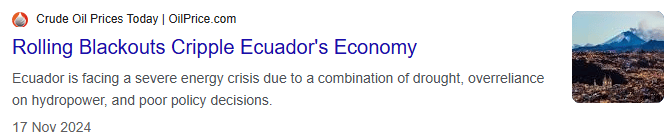

This region is key, because not only is the northern regions expanding rapidly, it opens up access to Colombia where Promigas already supplies gas and it borders Ecuador, which has had significant energy supply issues of late (source).

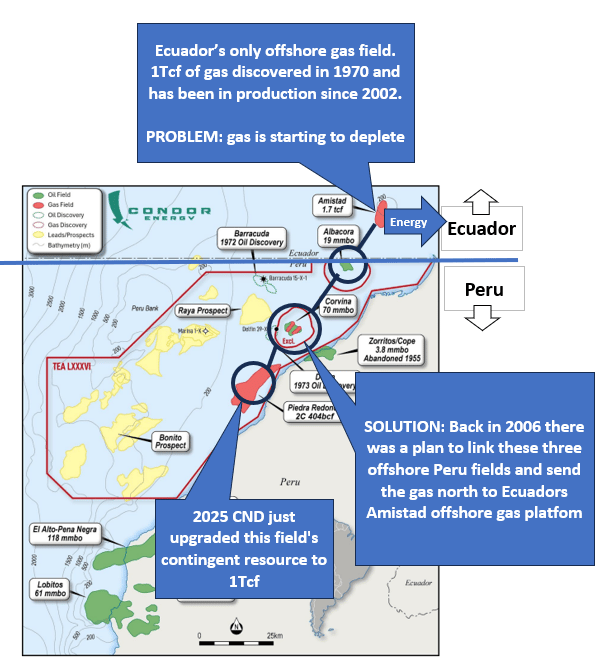

Ecuador only has one offshore gas field (Amistad) which has 1Tcf of gas and has been in production since 2002 - it’s right near the maritime border with Peru (and CND’s Peruvian acreage).

But the gas from Ecuador's field is starting to deplete and the Ecuadorian industrial sector is in need of more...

(Source)

We think energy from Peru could be a part of the solution here.

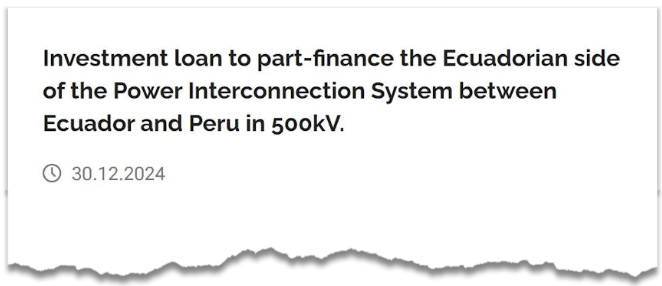

Back in November 2024 the Ecuadorian Minister for Energy & Mines approved the import of 7.3 billion cubic feet of Liquefied Natural Gas (LNG) from Peru.

And the European Investment Bank said it would contribute US$125M to the construction of a power interconnector between Peru and Ecuador:

(Source)

All of that activity is happening in and around CND’s block.

The really interesting takeaway for us from the MoU is that supplying gas from CND’s block, north into Ecuador has been explored in the past...

Back in 2006 CND’s project was almost developed as part of a plan to help solve Ecuador’s energy shortages.

The plan was to tie in CND’s gas discovery to the Amistad project to the north just over the border in Ecuador:

(source)

The project even had backing from the World Bank International Finance Corporation who was going to partially fund it.

(Source)

THEN...

The previous owners at the time (a US company called BPZ) decided to also focus on oil and took on a huge amount of debt to develop their oil projects...

However a 2015 oil price crash eventually caused BPZ to declare bankruptcy - which led to a fire sale of their offshore Peru assets.

(Source)

And now the block sits 100% controlled through a TEA by $12M capped CND.

We also note there is a commercialisation study that CND has completed recently which could be something Promigas take and run with too.

We covered the work from that in a recent Quick Take here: CND completes commercialisation study for 1 trillion cubic feet gas discovery

Here is a nice summary image from CND’s recent presentation showing how its gas project could be developed:

(source)

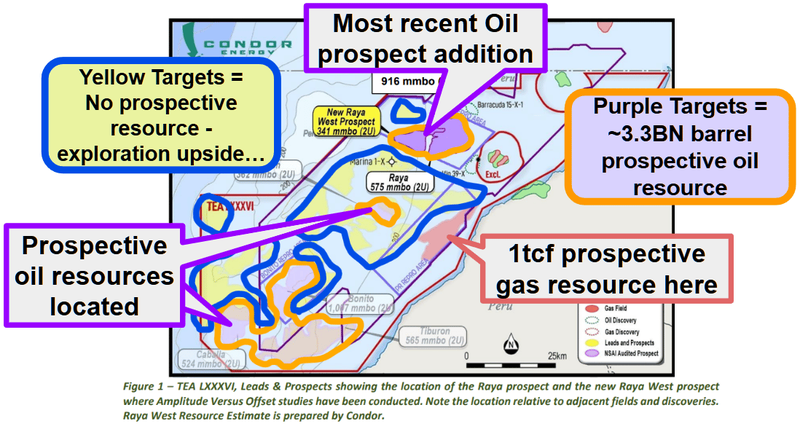

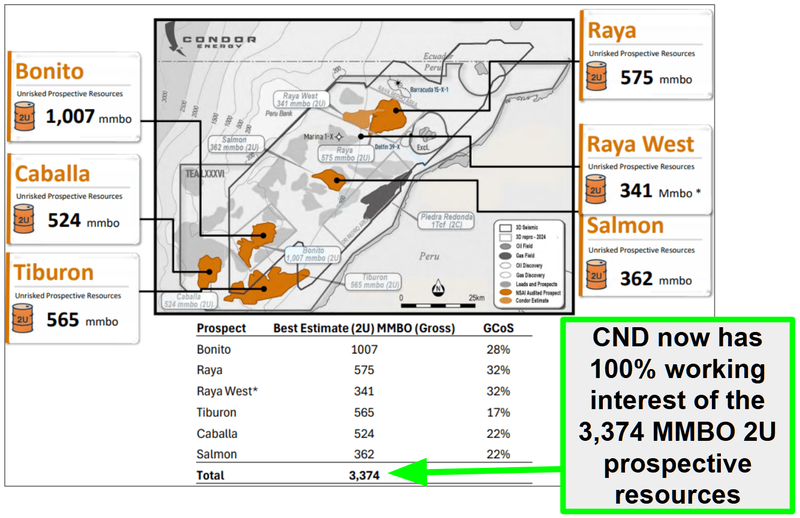

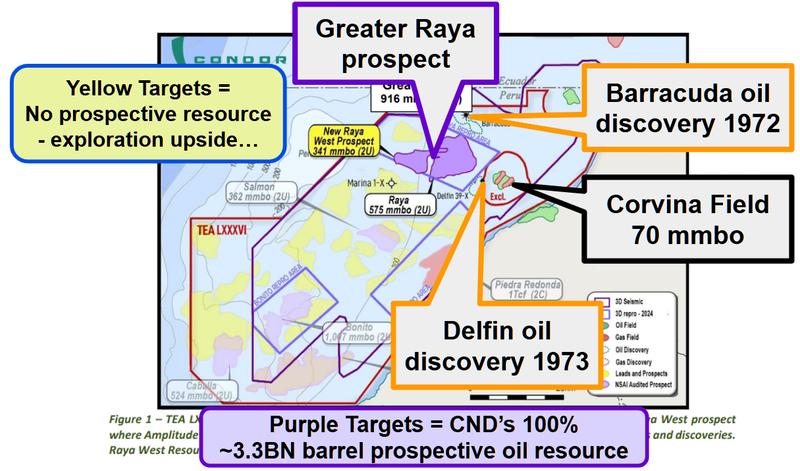

Deep dive into CND’s 3.3BN barrel oil exploration prospects

At the moment CND’s asset has a 3.3BN barrel prospective resource split across six main prospects:

(source)

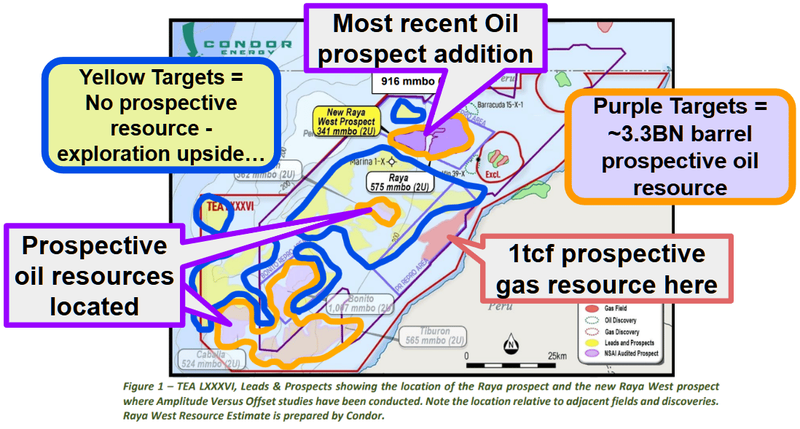

And there are a bunch of other leads that DO NOT have a resource estimate defined on them yet... so the exact upside could be a lot bigger than 3.3BN barrels:

(source)

A big part of why we like these prospects is because CND’s single biggest target is the ~1BN barrel Bonito prospect - more than big enough to be an interesting single well exploration roll of the dice.

And more than big enough to get a few interested parties into a data room and signed up to a farm-in deal.

Another big reason we like these prospects is because they sit in the middle of a PROVEN hydrocarbon system.

There is the Barracuda oil discovery that was made in 1972 and the Delfin oil discovery made in 1973 (both of which sit inside CND’s acreage)...

AND there is the Corvina Field (excluded from CND’s block) which is currently producing oil.

As mentioned earlier, the two wider basins that CND’s block sits within have produced ~1.7BN Barrels of oil historically.

So CND’s 3BN barrel in prospects are in a part of the world where discoveries have been made and projects have been brought into production...

(source)

We think the oil exploration part of CND’s block is exactly what you want to see in an offshore up and coming basin.

BIG targets - with plenty of running room (follow up targets) IF discoveries get made which can help build scale to justify developing a new oil field...

(the big kicker is that its a proven hydrocarbon system with all of that historical production - so it's technically de-risked to some extent).

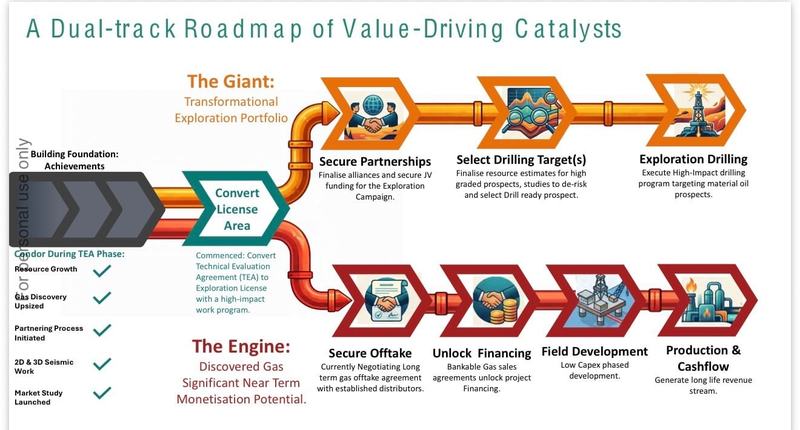

What’s next for CND?

License application outcome

The single biggest catalyst for CND right now is the outcome of the licence contract application.

Up until now, CND operated the project under a Technical Evaluation Agreement (TEA).

Reprocessing seismic data, new geological modelling and updating the resource estimates over the project. (source)

Back in May CND made its submission to convert the TEA into a license contract:

Ultimately, the licence contract is what gives CND the right to drill and develop the block.

And we think IF successful - that grant alone could be a major catalyst for a re-rate in CND’s share price...

We think it will also put CND’s block in play and allow for deals to be done over the asset:

(source)

What are the risks?

The single biggest risk right now is, without a doubt, licensing / regulatory risk.

CND has APPLIED to convert its TEA into a Licence Contract - but there is no guarantee the licence is granted.

If the market starts to price in a "no" or a long delay, CND's share price could drift lower.

Permitting risk

CND’s project is currently permitted under a Technical Evaluation Agreement (TEA) for a period of two years. Eventually before any drilling work can happen CND will have to convert it into an exploration licence. There is always a risk that the licence doesn't get granted and CND is left with no claim over the asset.

Source: “What could go wrong” - CND Investment Memo 05 December 2023

The other key near-term risks is commodity price risk.

Appetite for offshore explorers like CND is loosely tied to the oil price.

Offshore exploration usually needs oil comfortably above ~US$60–70/bbl to look attractive to partners.

If oil sits below that, appetite to fund a drill program - or to farm in - can dry up.

Commodity risk

CND’s project is leveraged to the price and demand for oil & gas. As the world looks to move away from fossil fuels, hydrocarbon projects may be phased out.

Source: “What could go wrong” - CND Investment Memo 05 December 2023

Other risks for CND

Like any small cap O&G explorer, investing in CND carries a high degree of risk.

Even with good seismic indicators and proven discoveries in the region, offshore drilling is technically complex and expensive.

A well can miss or deliver smaller-than-expected results, which would likely hit market sentiment and future funding options.

CND is also exposed to country and geopolitical risk. Peru has a history of supporting energy development, but policy shifts, regulatory changes or political instability could affect permitting, commercial terms or project economics.

And while a tense global oil backdrop (like the current Strait of Hormuz situation) can lift sentiment toward oil & gas explorers, it can just as easily reverse - sentiment-driven moves can be short-lived, and a sudden easing in oil prices could remove a tailwind just as quickly as it appeared.

Rising industry costs can also bite. Offshore rigs, vessels and specialised crews move with global demand cycles, and cost inflation could blow out drilling budgets or make a development less attractive to a partner.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our CND Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Our CND Investment Memo covers:

- What does CND do?

- The macro theme for CND

- Our CND Big Bet

- What we want to see CND achieve

- Why we are Invested in CND

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.