CND: 3 billion barrels of oil prospective resource. 1Tcf gas DISCOVERY. $13.6M market cap. Oil & gas back in 2026?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 31,060,455 CND Shares and 13,675,000 CND Options and the Company’s staff own 1,538,462 CND Shares at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

We think the oil & gas macro theme is going to make a comeback in 2026...

$13.6M Condor Energy (ASX:CND) has 3 billion barrels of prospective oil resources...

And an existing 1 trillion cubic feet gas discovery...

(yes, a Discovery - we’ve lost count of how many oil & gas explorers we have invested in over the last 20 years TRYING to make a discovery - CND already has a major one)

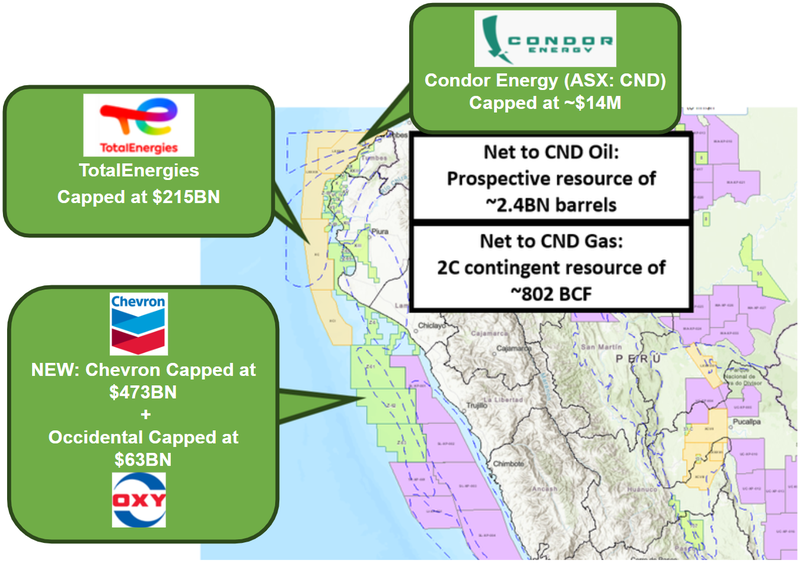

CND’s block in Peru is surrounded by $215BN TotalEnergies.

...and sits to the north of $473BN Chevron and $63BN Occidental’s blocks.

All three supermajors entered Peru... AFTER CND.

Yesterday, CND added an extension to one of its oil prospects - which could mean that 3BN barrel prospect inventory could get bigger (source) - more on this in a second.

And a few weeks before that CND signed an MoU to look at development options for its 1tcf gas discovery...

WITH the Peruvian division of Promigas - the gas distributor for 94% of the market in Peru and 38% in Columbia. (source)

We think CND’s $13.6M valuation is a function of the recent risk off sentiment from investors willing to fund offshore oil and gas.

But we have seen the juniors with assets like CND’s move on exploration success recently...

And we think that there is a precedent in the market for small caps like CND to re-rate off a “farm-in partnership”.

Basically where CND is able to attract a partner big enough and cashed up enough to fund drilling.

CND has previously said a “Farmout process commenced with multiple parties in data room”... (source)

Recently we have seen investors more willing to sit on the sidelines and wait for a farm-in partner to come in and de-risk funding before the valuation of a company really starts to run.

(would you want to stump up the estimated $20M to $30M for CND’s offshore well? We want to see a major farm in partner pay most of it and get a free(ish) ride on the result...)

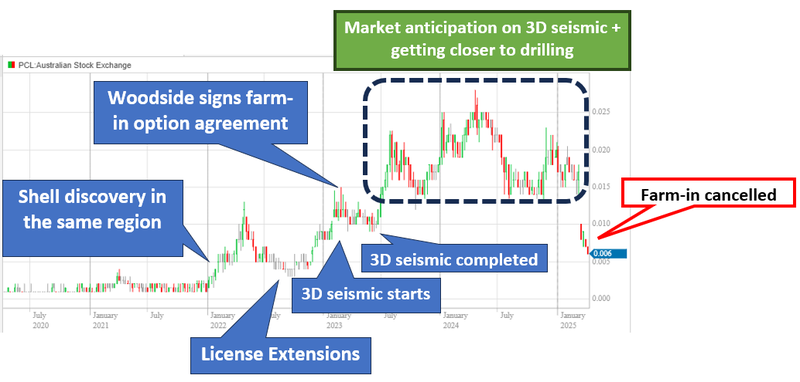

A farm-in with Woodside is what triggered another ASX listed offshore oil explorer’s (Pancontinental) share price to start a run from ~$7M to ~$230M market cap.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

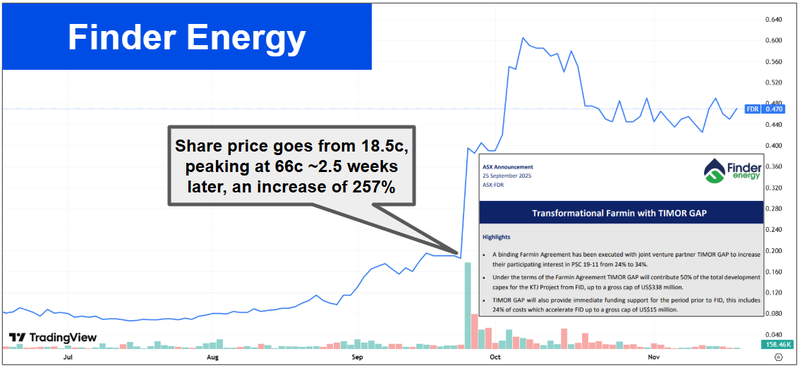

And more recently Finder Energy signed a farm-in deal and saw its share price go from 18.5c to a high of 66c:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

CND is currently capped at $13.6M.

And as mentioned earlier there are already some very deep pocketed majors sniffing around offshore in Peru... $212BN Total Energies - the French energy supermajor, almost completely surrounds CND’s acreage.

The $63BN Occidental Petroleum is hunting new discoveries nearby as well...

We also note there have been big deals happen in this part of the world before.

Back in 2009, KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND’s block.

(Source)

We think that a farm-in deal on the oil prospects and line of sight toward a first well could be what re-rates CND’s current valuation.

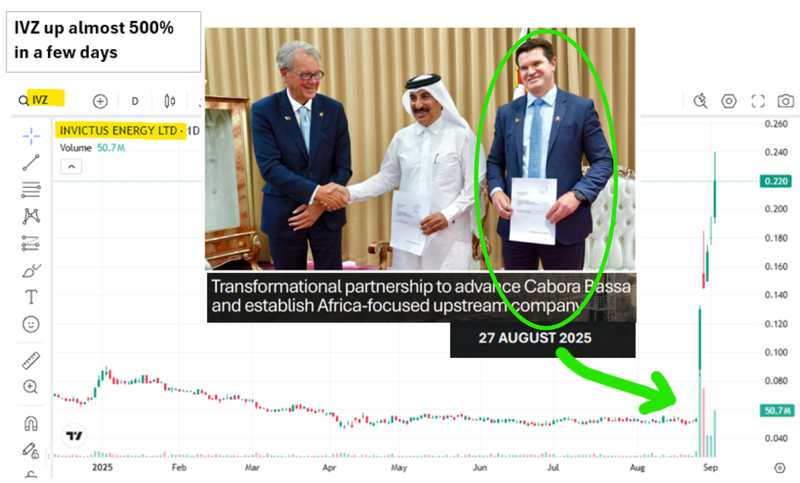

Hopefully CND’s director Scott Macmillan will open up his golden contact book to help out (after the enormous deal he signed with the Qatari’s at IVZ).

See our coverage of that news here: CND: Share price up on IVZ mega deal? CND director Scott Macmillan suddenly very well connected...

(source: our article september 3rd 2025)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Three ways we think CND could re-rate from here

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND does a deal on its gas asset - maybe some of the proceeds that come from this can go toward drilling an exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe? Now with Promigas looking at the asset, this is more in play...

- CND does a deal on its oil exploration assets - Maybe CND gets a free carried interest in a well that would be fully funded by a farm-in partner. This means less dilution going into a big drilling event for existing shareholders...

- Maybe a combination of the two? - CND could bring someone in that is interested in both...

Ultimately we think some sort of farm-in deal that de-risks funding for a well or development plan will be the catalyst to re-rate CND toward our Big Bet which is as follows:

Our CND Big Bet:

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

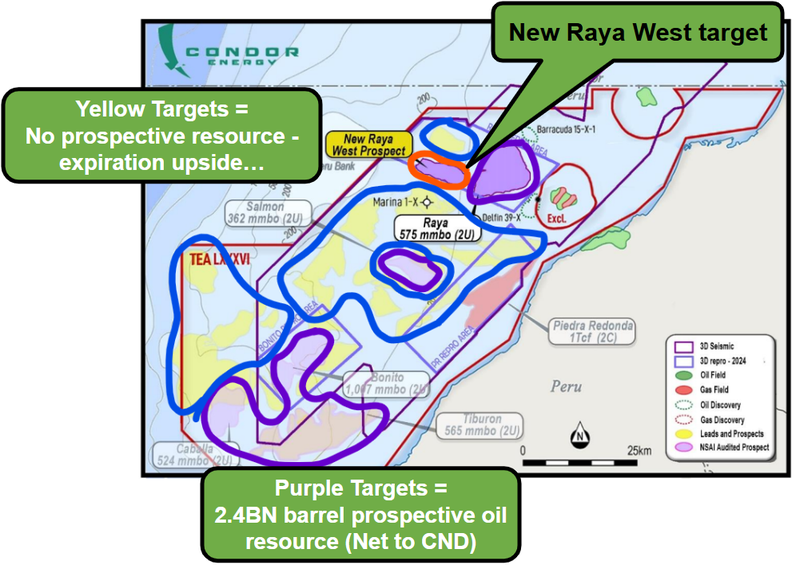

CND’s 3BN barrel oil prospective resource could be even bigger

At the moment CND’s asset has a 3BN barrel prospective resource split across five prospects.

We already knew there were a bunch of leads that did NOT have resource estimates yet...

(Source)

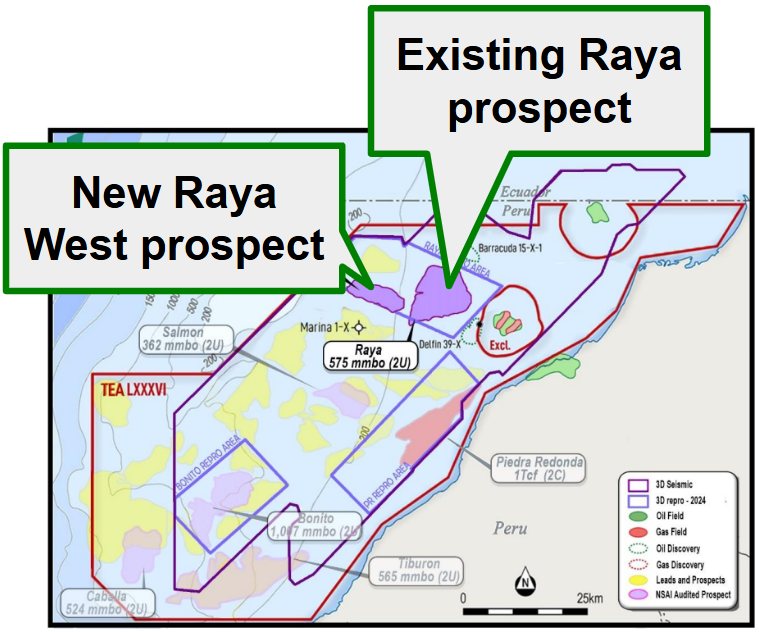

Yesterday CND added a whole new target right next to its 575M barrel prospective resource on Raya...

(Source)

The new structure with “AVO” anomalies (basically a good early stage indicator there might be hydrocarbons in a target) to the west could mean that the Raya structure is a lot bigger than we initially thought.

CND confirmed a prospective resource for that new target was now in the works...

The key takeaway for us was that the whole Raya structure could become one giant target where one well de-risks each target...

IF Raya comes in then Raya Weet is de-risked and vice versa.

(Source)

We think that sort of double-sided exploration exposure is important when marketing the asset to potential farm-in partners.

Those groups looking at CND would want something like Raya where an offshore well can de-risk more than just one target, but also set the base for follow up wells...

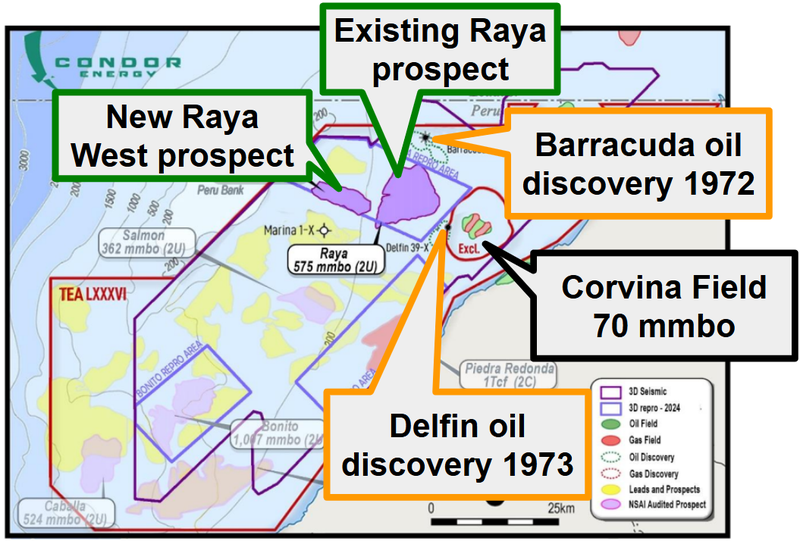

Another reason we think CND’s block just became more interesting to a potential farm-in partner is because the prospects sit in the middle of a PROVEN hydrocarbon system.

There is the Barracuda oil discovery that was made in 1972 and the Delfin oil discovery made in 1973 (both of which sit inside CND’s acreage)...

AND there is the Corvina Field (excluded from CND’s block) which is currently producing oil.

CND’s most recent reports suggested it was producing ~3,000 barrels of oil per day...

The two wider basins that CND’s block sits within have produced ~1.7BN Barrels of oil historically.

So CND’s 3BN barrel in prospects are in a part of the world where discoveries have been made and projects have been brought into production...

(Source)

Now we wait to see if the news yesterday changes the way any of the parties in CND’s data room view the project...

CND also signed a big MoU for its existing 1 Tcf gas discovery

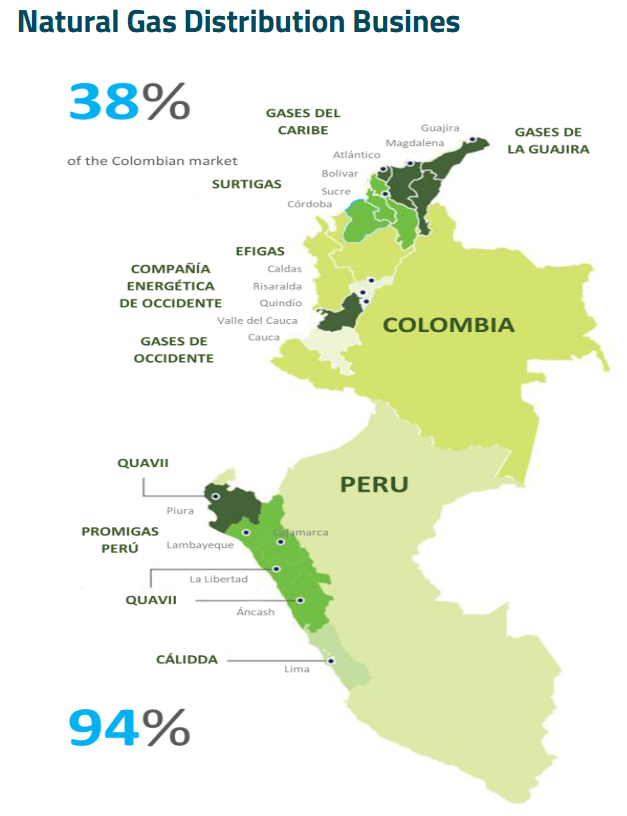

14 days ago, CND also signed what we think is an important MoU (Memorandum Of Understanding) with Promigas Peru.

Promigas manage, maintain and build gas infrastructure across northern Peru, supplying gas to homes, businesses and industrial facilities.

Promigas supply natural gas to 38% of the Columbian market and 94% of the Peru market. (source)

(Source)

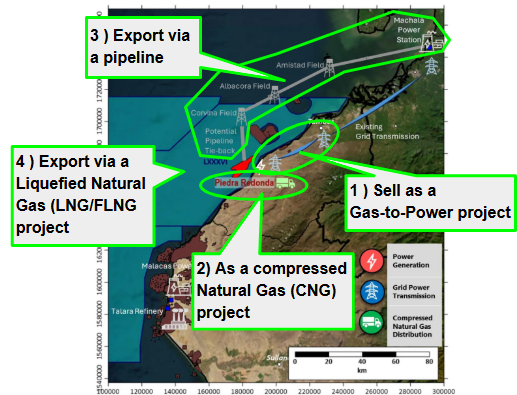

The deal with CND is around a potential offtake from CND’s existing gas discovery at Piedra Redonda.

CND’s project has a 1 Trillion Cubic Feet (Tcf) discovered gas field and together with Promigas will do studies on:

- Evaluating gas production potential

- Assessing infrastructure and delivery options

- Defining integration and commercial pathways

Basically, CND’s MoU with Promigas is to work out how best to take gas from its existing gas field and bring it to market.

One thing that stood out to us was CND’s comment on “Promigas’ efforts to expand access to natural gas in Peru’s northern regions”.

This region is key, because not only is the northern regions expanding rapidly, it opens up access to Columbia where Promigas already supplies gas and it borders Ecuador, which has had significant energy supply issues of late (source).

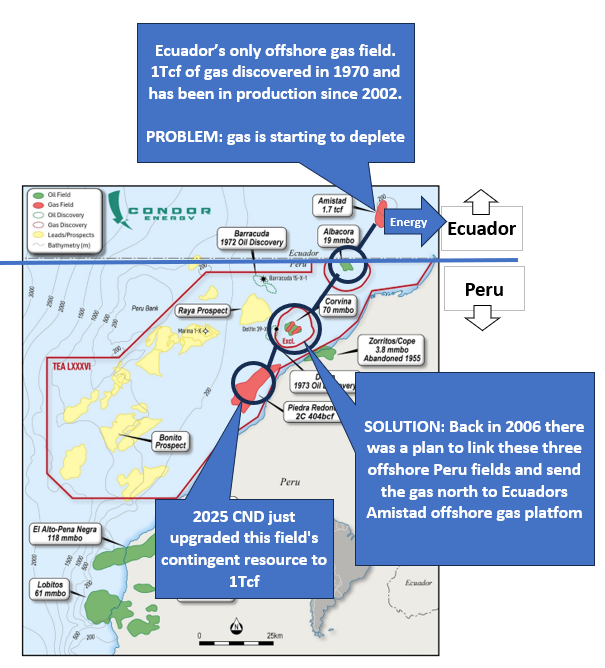

Ecuador only has one offshore gas field (Amistad) which has 1Tcf of gas and has been in production since 2002 - its right near the maritime border with Peru (and CND’s Peruvian acreage).

But the gas from Ecuador's field is starting to deplete and the Ecuadorian industrial sector is in need of more...

(Source)

We think energy from Peru could be a part of the solution here (not to mention the benefits to Peru itself)...

Less than three months ago the Ecuadorian Minister for Energy & Mines approved the import of 7.3 billion cubic feet of Liquefied Natural Gas (LNG) from Peru.

And the European Investment Bank said it would contribute US$125M to the construction of a power interconnector between Peru and Ecuador:

(Source)

All of that activity is happening in and around CND’s block... and where a possible development option would be tabled for its gas discovery.

The really interesting takeaway for us from the MoU is that supplying gas from CND’s block, north into Ecuador has been explored in the past...

Back in 2006 CND’s project was almost developed as part of a plan to help solve Ecuador’s energy shortages.

The plan was to tie in CND’s gas discovery to the Amistad project to the north just over the border in Ecuador:

(source)

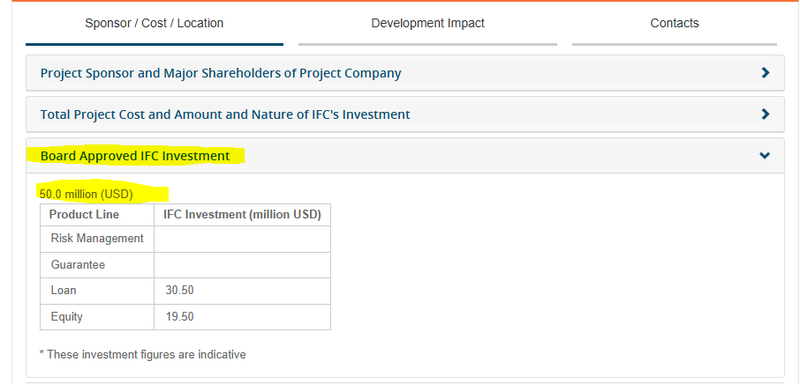

The project even had backing from the World Bank International Finance Corporation who was going to partially fund it.

(Source)

THEN...

The previous owners at the time (a US company called BPZ) decided to also focus on oil and took on a huge amount of debt to develop their oil projects...

However a 2015 oil price crash eventually caused BPZ to declare bankruptcy - which led to a fire sale of their offshore Peru assets.

(Source)

These events eventually led to ~$13.6M capped CND now owning 80% of the 1 TCF contingent resource.

Demand for gas globally has changed in a big way since 2006...

And now we will get to see a big distributor dust off those old development plans and look at it with fresh eyes.

Hopefully the studies end up in some sort of binding offtake/development deal.

No guarantees of course, there is always a chance nothing comes of the MoU.

We also note there is a commercialisation study that CND has completed recently which could be something Promigas take and run with too.

We covered the work from that in a recent Quick Take here: CND completes commercialisation study for 1 trillion cubic feet gas discovery

(Source)

What are the risks?

In the short term, the key risks for CND are “funding risk” and “commodity risk”.

Funding risk because CND have completed most of the desktop studies on their project.

Drilling an offshore target will cost a lot of money which CND’s current market cap wouldn't be able to support.

CND will therefore need to raise capital to fund drilling OR sign a deal with a funding partner to pay for the drill program.

A deal is never a guarantee and any delays could mean CND’s share price drifts lower as the market starts to price in a deal not being completed.

Funding risk

CND does not generate any revenues and so is reliant on raising capital to fund its exploration programs. If the markets are unwilling to finance CND’s exploration programs the company may need to go slow on its operations or offer large discounts to its share price when raising capital.

Source: “What could go wrong?” - CND Investment Memo 5 December 2023

“Commodity risk” because appetite for CND’s shares are loosely correlated to global oil/gas prices..

Usually for offshore exploration to be considered attractive we would need to see oil prices above ~US$60-70 per barrel.

With oil prices now trading sub US$60 barrel, it could mean market appetite to finance a drill program OR major partners to farm-in will be diminished.

Commodity risk

CND’s project is leveraged to the price and demand for oil & gas. As the world looks to move away from fossil fuels, hydrocarbon projects may be phased out.

Source: “What could go wrong?” - CND Investment Memo 5 December 2023

To see more risks read our CND Investment Memo here.

Other risks for CND

Like any small cap O&G explorer, investing in CND carries a high degree of risk.

CND operates in an offshore jurisdiction, which brings regulatory and permitting uncertainties. Timelines for approvals can shift with changes in government priorities, potentially slowing progress or altering development paths.

There is also execution risk. Even with good seismic indicators and proven discoveries in the region, offshore drilling is technically complex and expensive. A well can miss or deliver smaller-than-expected results, which would likely impact market sentiment and future funding options.

Partner risk is another factor. CND is actively seeking a farm-in or development partner, but until a binding agreement is finalised, there is no certainty a deal will be completed. Potential partners can change strategy, delay negotiations, or walk away, which could weigh on CND’s valuation.

CND is also exposed to country and geopolitical risks. Peru has a history of supporting energy development, but policy shifts, regulatory updates, or broader political instability could affect permitting, commercial terms, or project economics.

Rising industry costs may also affect outcomes. Offshore rigs, vessels, and specialised personnel are influenced by global demand cycles, and cost inflation could impact drilling budgets or reduce the attractiveness of development plans for potential partners.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our CND Investment Memo

In our CND Investment Memo, you can find:

- CND’s macro thematic

- Why we Invested in CND

- Our CND “Big Bet” - what we think the upside Investment case for CND is

- The key objectives we want to see CND achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.