China bans rare earth exports. SGQ has one of the largest and highest grade hard rock, rare earths resources in the world

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 29,000,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time.

You’ve probably heard “rare earths” mentioned in the news a lot lately.

(especially last night)

China dominates the rare earths market.

It controls 87% of the global refined rare earths supply.

China just announced it is restricting the export of a range of rare earths elements, sending shockwaves through global supply chains.

The USA’s largest rare earths producer’s share price promptly surged up 21% overnight in response.

Rare earths are used in the permanent magnets that are critical in the aerospace and defence industries.

They are also key inputs into making electric vehicles and wind turbines.

(All hot button industries in today’s turbulent geopolitical environment)

A rare earths export ban is China’s latest salvo in the tit for tat trade war with the USA.

Critical industries in the US rely on imports from China for rare earths and all of their downstream applications, including permanent magnets.

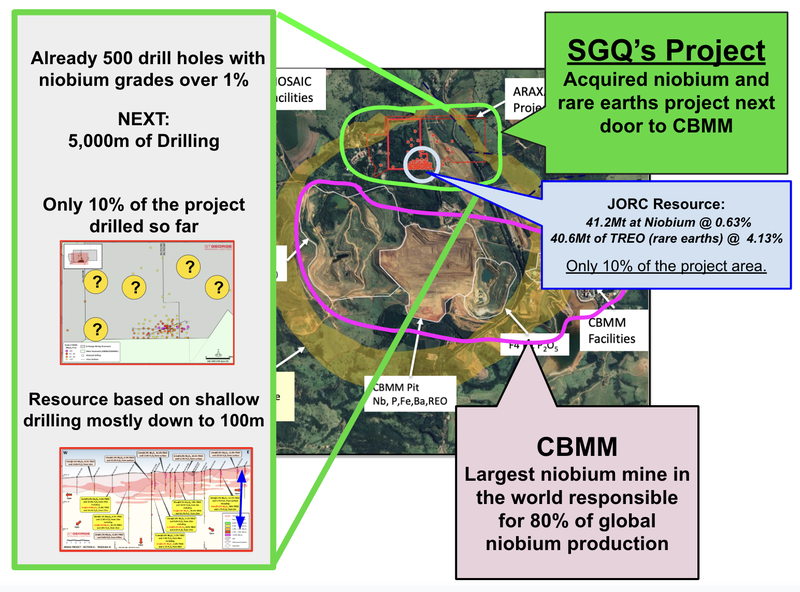

Our Investment St George Mining (ASX:SGQ) already has one of the largest and highest grade hard-rock rare earths deposits in the world.

Prior to market open today, SGQ was capped at $48M, still a fraction of its more advanced peers.

Today, SGQ released a peer comparison table which shows just how the company’s existing JORC resource stacks up in what is now a red hot macro environment for rare earths - which we cover below.

Following the release of its JORC resource a few weeks ago, SGQ’s project development studies are already underway. Plus drilling is scheduled to “commence in the coming weeks” to improve the resource, which is good timing.

(Source)

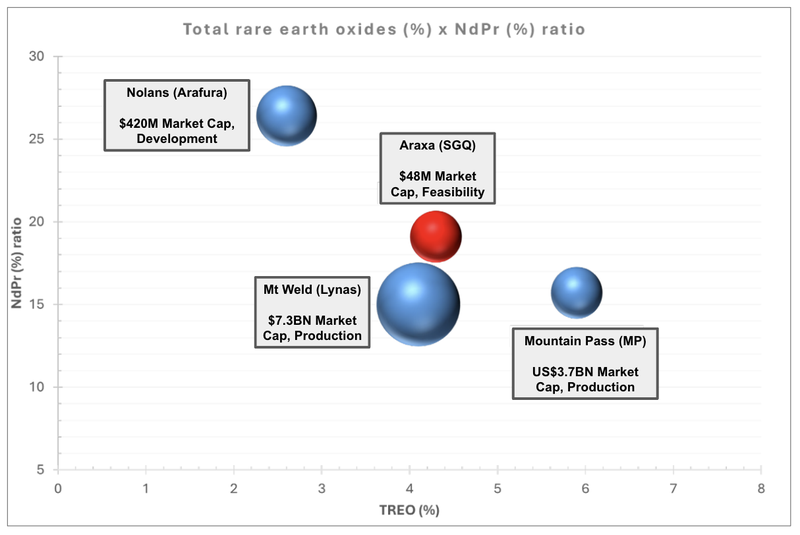

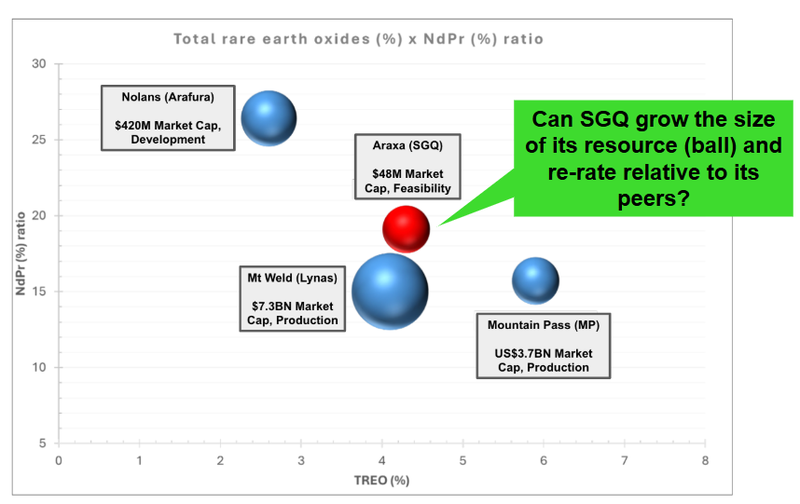

Below you can see a chart of SGQ’s current resource and how it compares to its peers.

Without any drilling of its own, SGQ’s resource already rivals its multi-billion capped peers.

The chart above can be tricky to get your head around, so let us explain.

SGQ is the red ball, and its peers are blue balls, where:

- Size of ball: indicates the size of the resource.

- Y (vertical) axis: % NdPr (the valuable stuff)

- X (horizontal) axis: the total rare earth oxide of the deposit.

The closer to the top right part of the chart the ball sits, and the bigger it is, the better.

Then the final step in digesting that chart above is to look at each company’s market cap and stage of development and determine (for yourself) which is undervalued.

For just one example of the sudden surge in interest around rare earths in the last 12 hours...

Last night (off the back of the China rare earths export ban news), USA’s largest rare earths producer MP Materials surged up 21%.

(MP Materials is the bottom right blue ball in the image above - similar size to SGQ)

That overnight move added US$1BN to MP Material’s market cap which is now ~US$4.5BN...

(and it’s looking like it will gap up again another few hundred million in market cap overnight)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

MP Materials already has a supply deal with the US Department of Defense - so you can see how these materials are very important to the US national interest.

But with this new China ban in place (including physically halting shipments of rare earths at ports: source), the US will be scrambling for additional new avenues of supply...

We expect many countries will be suddenly realising the strategic importance of rare earths supply and processing.

(not to mention the other critical metals used in defence, aerospace and artificial intelligence)

So as of last night, if they weren’t already, rare earths are now firmly on the global radar...

In today’s note we will breakdown:

- How SGQ’s current rare earths resource stacks up

- The exploration upside on SGQ’s project - how SGQ’s project can get bigger

- SGQ’s niobium resource (another one that is on critical minerals lists all over the world)

- The US China Trade war for Rare Earths and what it means for SGQ

- What we want to see next from SGQ

You can also check out our deep dive note from a few weeks ago on SGQ where we covered its maiden JORC resource (including the niobium) in detail.

Our take on SGQ’s maiden resource. It’s shallow and from surface... more drilling to come

How does SGQ’s rare earths asset stack up?

SGQ has one of the largest and highest grade hard-rock rare earth deposits in the world.

SGQ’s resource is carbonatite hosted (hard rock) which is well understood. It has similar geology to the rocks the US$4.5BN MP Materials and $7.6BN Lynas are producing rare earths from.

It IS NOT hosted in clays or some other project type that requires complex met work and processing tech...

And it's in Brazil, a country easy to do business with, in a Tier 1 mining jurisdiction, the state of Minas Gerais, in a region with a long history of commercial mines.

SGQ’s rare earths resource is of similar size to MP Materials (however, MP has more “indicated” resources at a higher confidence classification, and is already a producer).

SGQ has barely scratched the surface of its resource - so there could be much more to this story.

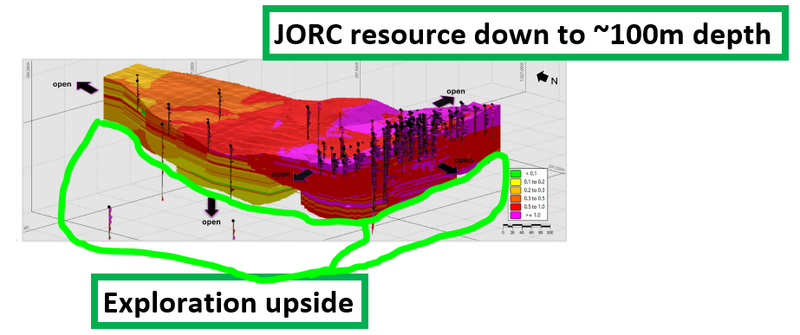

SGQ’s deposit has only been calculated from drilling down to shallow depths of up to 100m...

... and SGQ is about to start drilling in the coming weeks to potentially grow the resource by an order of magnitude.

Drilling could quickly expand the size of SGQ’s resource (i.e. the size of the red ball in the chart below).

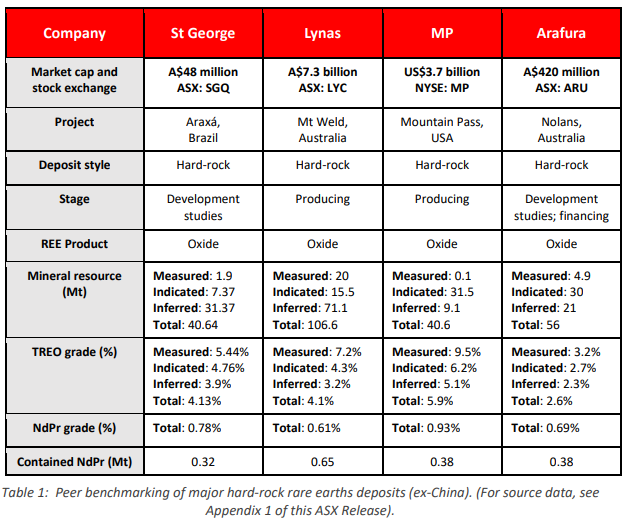

As it sits today, SGQ’s project has a 40.6Mt JORC resource with rare earths at grades of 4.13% TREO (total rare earths oxide).

Remember, the above chart shows how much of that TREO has valuable grades of NdPr on the X and Y axes.

“NdPr", which is a combination of Neodymium (Nd) and Praseodymium (Pr), are the two most sought after rare earths elements in most rare earth deposits as these are what are most useful in high tech defence applications, EVs and wind turbines.

SGQ’s resource has similar grades to A$6.5BN capped Lynas Rare Earths, who owns the producing Mount Weld project in WA.

And in terms of size, SGQ has the same tonnages as US$4.5BN MP Materials which is producing from its project in the USA.

Comparing it to a developer - SGQ has a higher grade relative to A$420M Arafura.

Here is how SGQ ranks side by side against Lynas, Arafura and MP Materials:

So what could SGQ’s asset be really worth?

Well, back in 2012, a Preliminary Economic Assessment (PEA) was completed for the project.

The study was done using an old foreign resource (which is smaller than SGQ’s current resource estimate - SGQ’s JORC resource is now almost TWICE that size).

The PEA showed Net Present Value for SGQ’s project of US$967M...

So SGQ is capped at less than $50M, has previously been modelled to have an NPV of almost a billion dollars (at a resource that was half the size) and is on par with some of the best rare earths assets in the world...

It’s almost double the grade of Arafura’s project, just as big as MP Materials and there is scope to make the resource even bigger.

SGQ’s resource is all based on drilling down to ~100m depths, whereas Arafura’s for example is based on drilling down to ~215m depths.

SGQ’s current resource is based on historic drilling which covers only ~10% of the project area...

SGQ is due to start drilling any day now to grow the resource...

We think that any upgrade to its already very strong resource could be well received by the market.

Again, SGQ was capped at ~ $48M prior to market open today, with a share price of 1.9c. .

SGQ is still digesting a $20M cap raise completed at 2c back in January - but we hope the sudden interest in rare earths and upcoming news flow should help SGQ finally break through the current 2c wall.

We think successful drilling could see it at least close the gap with developer Arafura, and then eventually get closer to the bigger rare earths players once the project is closer to being developed.

Bear in mind that closing the gap to Arafura would be a ~8x move on SGQ’s current market cap...

Of course, anything can and will happen - SGQ is a high risk development stage mining stock, and success is no guarantee.

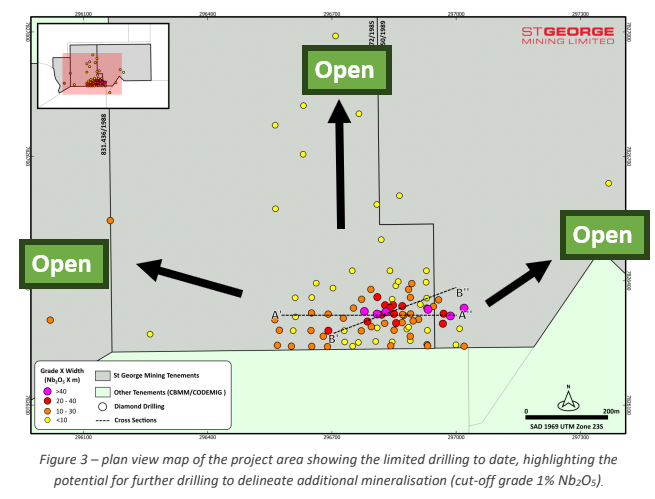

SGQ’s project can get a lot bigger, what’s the exploration upside?

SGQ’s project is serially underdrilled.

The project was previously held by a phosphate producer on the TSX called Itafos (who now hold ~10% SGQ).

Itafos’ focus has always been on eking out as much profit as possible from its phosphate mines and so this rare earth / niobium project saw barely any capital get invested into it.

The reality is that SGQ’s project hasn't been drilled for years and has had almost no work done on it during the current positive market sentiment for niobium.

Which is why we think SGQ can add a lot of value to the project with the drill bit.

At the moment, almost all of the JORC resource is limited to depths of ~100m and drilling has been on only ~10% of the project area:

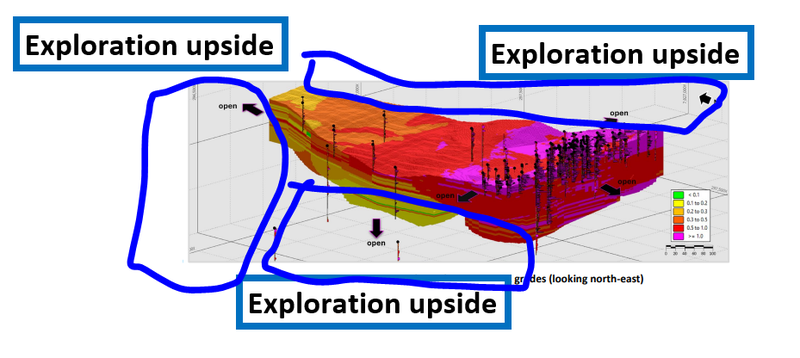

For SGQ’s upcoming drill program we want to see SGQ do two things:

- Extend the JORC resource below 100m.

- Extend the JORC resource ot the east/west and north of the current resource

Here is a very basic 3D view of where we want to see SGQ drill (excuse us, we are not artists):

SGQ expects all of the drilling to be completed, reported, and the resource upgraded before the end of the year.

US-China trade war heats up. Rare earths are at the heart of it all

Over the last few days the trade tensions between the US and China have... escalated.

(and that’s putting it lightly)

Here is a quick rundown of events - with the daily changes it can be hard to keep up:

- Two weeks ago, Trump announced “Liberation Day” with a swathe of tariffs on all countries.

- The next day, China retaliates with a 34% tariff on the US.

- By the following Wednesday, Trump paused tariffs on every country bar one... China.

- The next day, Trump announces a 145% tariff on China.

- China responds with a tariff increase to 84% and again to 125% on Friday.

- In the last few days, China paused rare earth shipments and announced new measures to ensure rare earths (and subsequent products) don’t make it into the US.

It is not new for rare earths to be at the heart of a trade war.

The phrase "Critical Minerals” was invented by the Japanese in 2010 due to a trade dispute with rare earths at the centre.

In 2010 there was an incident involving a Chinese fishing boat encroaching on Japanese waters.

Tensions escalated and as a retaliation the Chinese placed an embargo on rare earth exports to Japan.

This caused havoc in certain key Japanese materials industries (despite the government at the time waving off the embargo initially).

From there Japan created the first ever “Critical Minerals” strategy, to protect itself from China’s dominance over the rare earth markets.

You can read the full story here: How Japan solved its rare earth minerals dependency issue

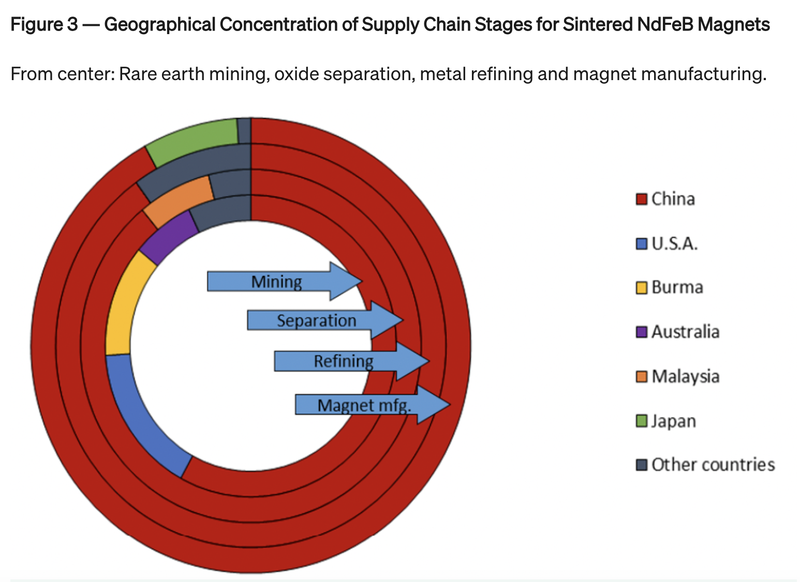

For Trump and his administration, “rare earths” have been a critical part of his strategy.

Because to this day, China still dominates all aspects of the rare earths supply chain:

(Source)

Trump has made some bold statements about “acquiring” Greenland and Canada for its critical minerals resources...

He even made “critical rare earths” a core part of any deal with Ukraine for continued support in its conflict with Russia.

He understands the leverage that China has over key industries in the US for national security, and wants to find other ways to protect its supply chain.

Our take is that rare earths, and in particular later-stage rare earth projects that could be alternative sources of supply - like SGQ’s - could become more valuable given the focus of the resource in this trade war.

SGQ also has niobium - another mineral on global critical minerals lists

SGQ is not just a rare earths story.

The same project also has a large niobium resource - of 41.2Mt at niobium grades of 0.63%.

Niobium is on the top of every critical minerals list all over the world.

Niobium has traditionally been used to make steel stronger and lighter - this use case is 88% of niobium demand.

However, niobium is also used in a range of speciality applications including aerospace, defence, semiconductors, optical lenses, and MRI equipment - about 12% of demand.

And it turns out niobium can also be used in battery technologies to improve battery performance and life - this is a high growth emerging market for niobium.

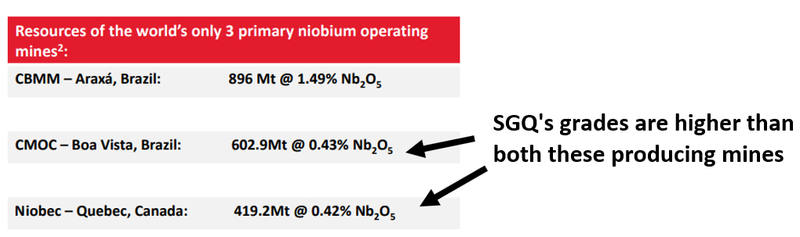

At the moment, ~80% of world supply comes from the mine next door to SGQ, and there are only three major mines in operation all over the world.

Because of that supply concentration, governments around the world are looking to secure their supply chains.

Just like we are seeing with rare earths in the last few days, the same could happen to niobium.

And if the US (or other countries) decided to start up strategic reserves then there will be very few places the world can go to get new niobium supply...

At the moment almost all of the world’s niobium supply comes from three mines:

- CBMM’s mine, next door to SGQ (biggest producer globally) - valued at ~US$12.5BN back in 2011 based on a deal to sell down 30% of the project for US$3.75BN.

- CMOC mine (2nd biggest producer)

- The Niobec mine in Quebec, Canada (3rd biggest producer) - acquired by a private group in 2015 for US$530M.

While the resources for all three of those assets are multiples the size of SGQ’s.

SGQ’s grades are higher than the 2nd and 3rd biggest mines in the world...

From a size perspective, SGQ’s resource is just under 1⁄4 of the size of Australia’s biggest niobium name, WA1.

WA1 is currently capped at ~$830M with an inferred resource of 200Mt at 1% niobium compared to SGQ’s ~41Mt resource.

(and all of that is before the exploration upside we just wrote about)

What we want to see next from SGQ

In the short term we want to see SGQ kick off its drilling.

Beyond that, over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

- Progress on strategic investors/offtake partners -hopefully SGQ can follow up the $8M cornerstone investment it managed to get from Xinhai Group - a global mining services provider - as part of its last raise.

- Finalise the remaining vendor payments - US$6M is due in ~9 months and then another US$5M in ~18 months.

- Start working on development studies -SGQ has mentioned some of these workstreams are already underway.

- Updates on downstream processing processing venture -SGQ is also working on a downstream processing process for niobium/rare earths products. This could be an additional upside if SGQ manages to make any material progress on this front.

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker. SGQ is participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Permitting - SGQ is working with the same consultants that worked on Sigma Lithium and Latin Resources projects (two large lithium players in the same region of Brazil, Minas Gerias). Permitting targeted for full completion by Q4, 2026.

Ultimately, as SGQ progresses its project, we are hoping it achieves our Big Bet which is as follows:

Our SGQ Big Bet:

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

What are the risks?

In the short term, the key risk for SGQ is “exploration risk”.

SGQ’s plan is to start drilling out its project in the short term.

There is no guarantee that drilling will successfully grow SGQ’s resource.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Beyond the drill program and SGQ’s resource upgrades, the main corporate risk is that SGQ will need to make the deferred payments due for the acquisition of its project.

SGQ has already paid the first US$10M of the acquisition costs.

Inside the next 9 months, the next US$6M is due, and in 18 months, the final US$5M.

IF SGQ struggles raising these funds it would likely have a negative impact on SGQ’s share price.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.