CAY starting mining operations in a few weeks…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY Shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our 2025 Wise Owl Pick of the Year Canyon Resources (ASX:CAY) is bringing into production the highest grade undeveloped bauxite projects on the planet.

Very soon.

Bauxite is the rock that is essential for the production of aluminium - which is a critical ingredient to transport, power grids, modern clean‐energy technologies and...

Military and defence.

A few months ago the biggest bauxite exporter, Guinea (~73% of global bauxite exports) put in export restrictions AND revoked licenses for some of the country's biggest mines. (source) (source)

Good thing CAY is only a month away from mining, and five months away from shipping out its first batch of bauxite in Cameroon...

A surface miner has just arrived in-country and will start operating next month.

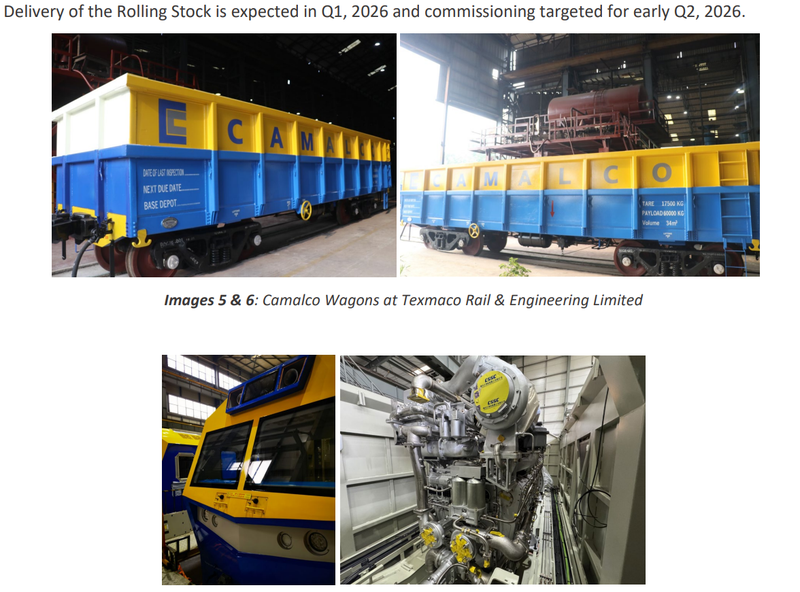

Delivery of rail locomotives and wagons is happening this quarter.

Ore haulage is set to begin next quarter.

CAY’s first bauxite shipment is planned for late June 2026 - and according to a recent CEO interview the company will be generating cash in Q3 (you can watch the full interview further down).

CAY’s bauxite project has an estimated 1 billion tonne plus JORC resource in Cameroon, Africa.

The resource is big enough for production to run for over fifty plus years.

It’s the type of asset that the big miners like to call ‘Tier 1’ assets - large, long life, and low cost.

(the ‘Tier 1’ adjective gets thrown around a lot in this industry, but we think CAY’s asset definitely fits this category).

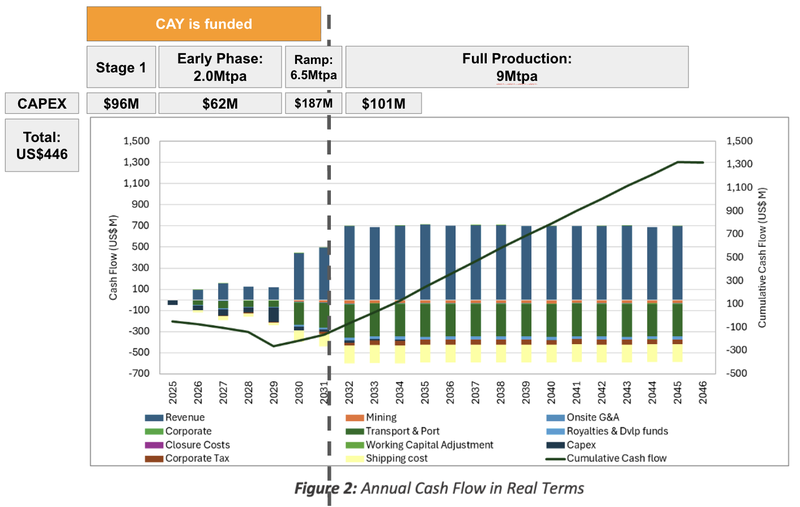

Once ramped up to full phase 3 production - the project will be producing 10M tonnes of bauxite per annum - and according to CAY’s CEO at US$81-2 per tonne with US$35 costs, CAY could produce ~US$200M in annual free cash flow at full capacity.

CAY is fully funded for Stage 1 production (up to 2M tonnes of bauxite per annum) through a mix of debt and equity - including the backing of major partners - Eagle Eye Asset Management.

Eagle Eye is investing a further $100M in a second tranche of last year’s placement at 26c per share.

An additional ~$70M is coming from a subsidiary of Afriland First Bank, a major Cameroonian bank.

CAY is currently trading at 22c per share - below that previous funding round price.

CAY’s CEO also flagged a move downstream into alumina refining in a recent interview (and again in today’s announcement), to capture even more of the value chain

(more on what he said on the downstream plan later in today’s note)

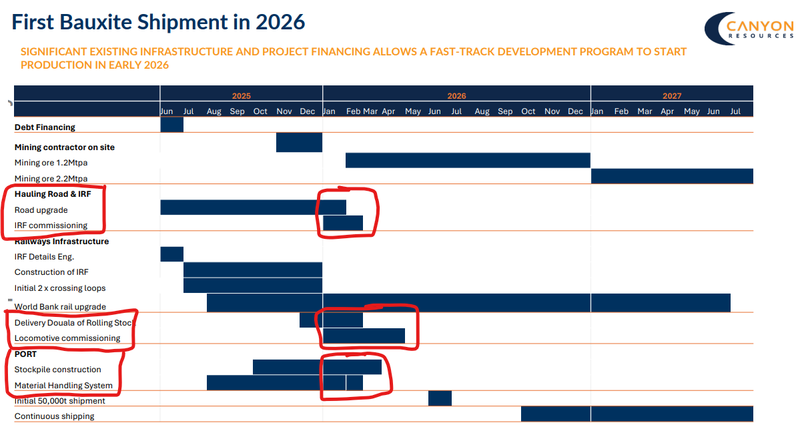

Today we got a Development Update from CAY, which gave some pretty firm timeframes for us to follow into the company’s first production revenues:

- CAY expects to be mining in February 2026 (next month).

- CAY expects to be hauling material to its Inland Rail Facility (IRF) in Q2 2026 (in ~2 months)

- CAY expects to be shipping bauxite in June 2026 (in ~5 months).

So we are likely a few weeks away from mining starting... and ~6 months from potential first revenues...

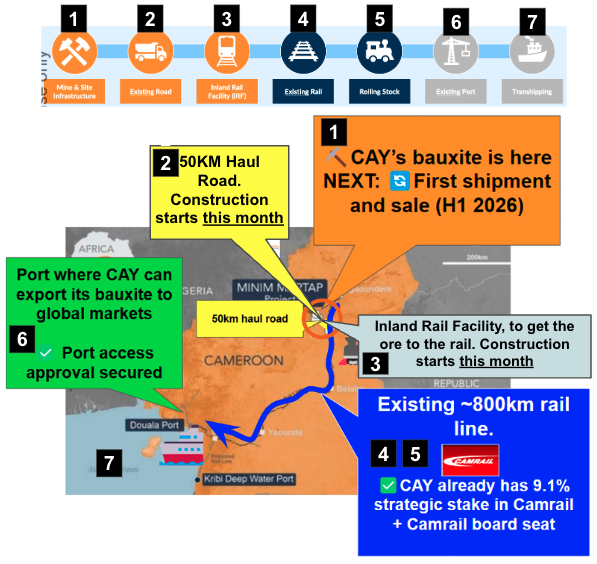

CAY is building the project infrastructure right now.

Here is the haul road being built:

(source)

And here is the surface miner that just got delivered to Cameroon - on its way to CAY’s site to start mining in February:

(source)

Here are the trains that were ordered last year - scheduled to be shipped to Cameroon next month:

(source)

As we mentioned above, CAY has already secured funding to get to that first shipment to customers - and the equity component was done at a premium to the current market share price.

Late last year, CAY secured ~$215M in funding to get its projects into production - the raise was done at 26c per share.

CAY is currently trading at 22c per share.

Once the second tranche of the placement settles (next quarter), CAY should be in a position where it roughly has:

- A market cap of ~A$597M (assuming the share price hovers around where it is right now)

- ~A$266M in cash

- ~A$175M in undrawn debt facilities

- Enterprise value of ~A$330M (again assuming the share price doesn't move too much and our cash balance estimate is close)

- An increase in CAY’s ownership of Camrail from 9.1% to 35% (Camrail is Cameroon’s state-owned rail operator) - more on this later.

By our back of the napkin calculations and making some reasonable assumptions, it means CAY should be funded for the CAPEX of phase one and two of its project:

(CAY explicitly says it is fully funded for phase 1 - up to 2mtpa of production)

(source)

Here are the key things CAY has already done to get to first revenues:

- Ordered locomotives (train carriages) - CAY confirmed today that the locomotives and wagons would be delivered to site this quarter. (source)

- Appointed a contractor to start construction on the Inland Rail Facility - this is where the ore loading onto the trains happens. CAY confirmed today that ore haulage from the Inland Rail Facility would begin next quarter. (source)

- Appointed a contractor to start road construction - road construction is happening right now. CAY confirmed that the upgrade works were on track for completion by the end of this quarter. (source)

- The surface miner (what CAY will use to mine its bauxite) has arrived in Cameroon and will be ready for mining in February 2026. (source)

- Official opening ceremony with government officials on site. (source)

And here are the big ticket items that CAY has left to complete before we see those first shipments out of Cameroon (and subsequently CAY’s first revenues):

(source)

Basically now it's just a case of getting the trains in country, commissioning that inland rail facility and starting mining.

CAY owns a piece of its rail infrastructure too - soon to be 35% of the national rail company

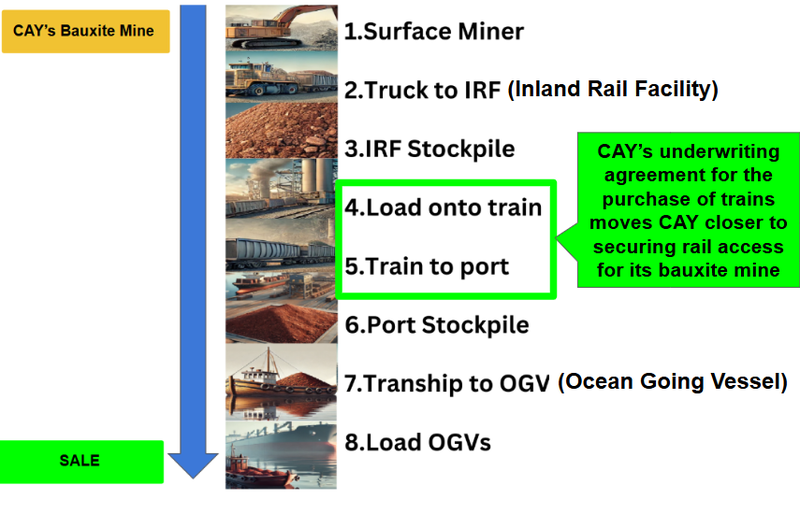

CAY’s deposit starts from the surface, and is high enough grade that CAY will be mining DSO (direct shipping ore).

That means the mining process is as simple as digging up the ground and putting it on a truck to load onto a train.

Simple mining process means that the biggest bottleneck for CAY’s project was always going to be logistical - rail, haulage routes and shipping to get the product from mine to customers around the world.

After all, bulk commodity projects like this one are more of a logistics challenge than a mining challenge.

CAY has de-risked that to a certain extent by taking an ownership stake in Cameroon’s state owned rail operator - CAMRAIL.

CAY after its last capital raise, committed to increasing its stake in CAMRAIL to 35%. (Source)

Today, CAY said discussions around finalising that deal were ongoing and “expected to be completed in Q1-2026”.

Which should mean CAY has enough of a say to dictate how the rail infrastructure is developed in country and how much space is allocated to CAY’s project...

More control over this piece of key infrastructure is crucial.

It also means CAY doesn’t just own a big mining asset - but also a piece of pretty important infrastructure in the country (which we think isn't really being built into CAY’s valuation).

We did a deep dive on why the rail matters so much in a previous note here: Bauxite developer CAY to acquire 9.1% of Cameroon rail company, plus board seat

This is how we see CAY’s project working:

Over the next few months we think the main market moving share price catalysts for CAY will be:

- An offtake deal that locks in a sale price for CAY’s product (keeping in mind that CAY’s bauxite is a premium product and could fetch US$11 higher than market bauxite prices)

- Mining fleet mobilising to site (now expected in February)

- Locomotives arriving in country (expected to be happening this quarter)

- Road/rail infrastructure completion (expected to be ready for use by June).

Ultimately we want to see CAY bring its project into production thus achieving our Big Bet which we set out when we first Invested:

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our CAY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Latest from CAY’s new CEO

For anyone catching up on the CAY story here is a good interview with CAY’s CEO Peter Secker:

(source)

Our key takeaways from the interview

On the importance of product quality in the bauxite market

Peter talks about how the operating costs for CAY’s project will be ~$35 per tonne.

He then says “The key thing about Minim Martap is 51% alumina, less than 2% silica. This is premium bauxite”.

Usually bauxite with lower impurities like CAY’s project demand a premium price (CAY expects that to be ~US$10 premium on Guinean bauxite which sells for ~US$70-72 per tonne).

So at US$81-2 per tonne with US$35 costs, CAY could produce ~US$200M in annual free cash flow at full capacity (10M tonnes per annum).

Peters commentary on the premium pricing and potential cashflows starts at 5:00 here.

On the production ramp up strategy

CAY expects to be in production at 2M tonnes per annum (phase 1 production target) based on existing rail capacity.

Expansions to phase 2 & 3 are dependent on rail upgrades which are being financed by the World Bank (~US$820M for the PQ2 rail corridor upgrade).

(Source)

(Source)

We covered those rail upgrades in our last note here: CAY’s ownership in rail infrastructure is also increasing...

Peter confirmed that the target was to be at 5M tonnes per annum in 2029 and then 10M tonnes per annum in 2031 with a potential expansion to 15M tonnes per annum a possibility.

On the importance of infrastructure control

As we mentioned earlier, infrastructure control is a big part of CAY’s story.

Peter also talked about this and explicitly said: “We believe that the rail is key to this project”.

He also confirmed that with an increased 35% stake, CAY “would have a couple of board seats” and we'd have “some operational input” into the rail infrastructure development/upgrade works.

On the downstream value-add strategy

Producing bauxite for a profit is very good.

However on top of that CAY can capture more of the value chain, and that is by refining the bauxite into aluminium.

We have written about the potential for a move downstream into alumina refining inside Cameroon here.

Back in February 2025 there was media speculation that CAY’s biggest shareholder Eagle Eye was in talks to buy a stake in Cameroon’s state aluminium company which owns the country's only aluminium smelter...

(Eagle Eye will maintain its ownership at 56.5% of CAY after the T2 placement, source)

(Source)

At the same time, CAY was talking about doing a Definitive Feasibility Study (DFS) on a move downstream.

In the interview above, Peter confirmed that CAY is currently "doing a feasibility for an in-country refinery to produce alumina. That will be finished middle of the year”.

And today, CAY reiterated the progress on this study, confirming that the feasibility study was now 45% complete.

So we could start to see some newsflow on this just as CAY is about to make its first bauxite shipments in June...

The “alumina refining” angle to CAY is something that could add additional upside in future years.

What’s next for CAY?

As mentioned earlier, the key catalysts we will be looking out for over the coming months are:

- An offtake deal that locks in a sale price for CAY’s product (keeping in mind that CAY’s bauxite is a premium product and could fetch US$11 higher than market bauxite prices)

- Mining fleet mobilising to site (now expected in February)

- Locomotives arriving in country (now expected to be shipped to site next month)

- Road/rail infrastructure completion (now expected to be ready for use by May).

We want to see CAY execute its development plan as they have outlined below:

(source)

What are the risks?

CAY’s is funded through to first production now, so the two key risks for CAY in the medium term are “delay risk” and “commodity price risk”.

Delay risk, because there is always the possibility that the first production target is pushed back and the infrastructure build out/locomotive deliveries are finalised well after those production forecast dates.

Development/delay risk

Should any or all of the above risks materialise, CAY could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price.

Source: “What could go wrong” - CAY Investment Memo 20 Jan 2025

Commodity price risk because the bauxite price could fall between now and when CAY is selling it, impacting the returns on investment early into the project's life - which is typically where the market is looking for a fast capital payback on any mining asset.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: “What could go wrong” - CAY Investment Memo 20 Jan 2025

For the other reasons we list as part of our Investment Thesis, check out our Investment Memo here.

Other risks

Like any stock market investment, investing in CAY carries a multitude of risks which may affect the value of the company, some of which may not be foreseeable (this is the nature of risks).

Here we aim to identify a few more risks.

CAY is still a pre-production company, and while now fully funded to build its mine, there is always a chance that construction or commissioning issues lead to delays, cost overruns, or operational setbacks.

The company is also highly sensitive to movements in the bauxite price. A sustained downturn in the commodity could materially impact project economics, offtake discussions, and investor sentiment.

While Cameroon has a long history of mining, it is still considered a higher risk jurisdiction compared to more established markets. Political, fiscal, or regulatory changes could affect project timelines or economics.

Despite its recent capital raise, CAY may still require additional funding for future expansion or unforeseen costs. Any further capital raises could dilute existing shareholders.

As CAY is transitioning from explorer/developer to producer, execution risk remains high.

Successfully managing logistics, infrastructure, and ramp-up to steady-state production will be critical and failure to deliver may weigh heavily on the share price.

Finally, the current valuation may already factor in future upside. Any negative surprises whether from delays, commodity markets, or permitting could result in sharp volatility.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.