Catalysts Imminent as NIC Eyes Full Scale Nickel Production

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Recently we introduced you to ASX newcomer Nickel Mines Limited (ASX:NIC) and posed the question: is this company the next big thing in nickel?

Well, NIC is certainly moving quickly to live up to the moniker.

Just last week the company announced that a first batch of Nickel Pig Iron (NPI) had been produced from one of the two rotary kilns at its 60% owned Hengjaya Nickel Project in a maiden production run leading into the Chinese New Year holiday season.

So now with full scale production coming into view, combined with low costs and a bullish nickel price outlook, NIC could be well on its way to answering the ‘next big thing’ in global nickel markets question.

What initially piqued our interest in NIC was the financial, operational and strategic partnership it had struck with Tsingshan Group, the world’s largest stainless steel producers.

Under the terms of two separate Collaboration Agreements with Shanghai Decent, a Tsingshan group company, NIC will own and operate RKEF processing facilities within the Indonesia Morowali Industrial Park (IMIP), the world’s largest vertically integrated stainless steel facility with a current stainless steel production capacity of 3.0 million tonnes per annum.

In addition to these downstream processing assets NIC also holds an 80% interest in the Hengjaya Nickel Mine, a large tonnage, high-grade nickel laterite deposit is located just 12 kilometres from the IMIP.

In our introductory article, The Next Big Thing in Nickel? ASX Newcomer Partners Up with World’s Biggest Stainless Steelmaker, we also suggested there would be a string of upcoming share price catalysts for investors to look forward to in the months ahead.

Last week’s announcement of first NPI production was the first of these and came a little sooner than expected.

This milestone event came as NIC’s share price recovered to its IPO listing price of 35c (for a market cap of $486 million), a level that clearly ignores the six months of solid progress since – although it has been in a solid uptrend since early January.

With so much going on, and so much upside to report, let’s get the full story on...

Maiden NPI production complete at Hengjaya Nickel Project

As Nickel Mines (ASX:NIC) reported last week, a first batch of Nickel Pig Iron (NPI) was produced in a maiden production run from one of Hengjaya Nickel’s two rotary kilns.

With first production over the line, Hengjaya Nickel’s first kiln is expected to reach at least 80% of nameplate capacity by early April 2019.

Here's an article from Finfeed.com covering the news...

The second kiln is anticipated to commence commissioning in early March and is expected to reach at least 80% of capacity in early May 2019.

Ramp-up to full scale production will be achieved shortly thereafter.

This commissioning process and ramp-up is consistent with that previously implemented across the 20 existing RKEF lines currently in operation within the Indonesia Morowali Industrial Park (IMIP), which you can see below:

Progress at the Henjaya Nickel Mine complements the work NIC is doing at its...

Ranger Nickel Project

Shanghai Decent has advised that an expedited schedule will now see the first kiln of the company’s 17% owned Ranger Nickel Project ready to commence commissioning in April 2019, with the second kiln to commence commissioning in May — well ahead of previous guidance of ‘the September quarter’.

Under the terms of its Collaboration Agreement with Shanghai Decent, a second acquisition option, will permit NIC to increase its interest in Ranger Nickel to between 51% and 60% before 31 December 2019. A third acquisition option will then allow NIC to increase its interest to up to 80% in the Ranger Nickel within 18 months of the first batch of NPI being produced.

Potential tier-1 nickel investment exposure

The Hengjaya Nickel and Ranger Nickel Projects considered together give NIC a potential nickel production profile of approximately 30kt of nickel per annum.

This would make it one of the largest listed pure play nickel companies anywhere in the world, and well on the way to achieving its objective of becoming a tier-1 nickel investment exposure.

We can expect significant upside for Nickel Mines due to the project having very low capital intensity. And since it can boast being among the lowest cost nickel producers in the industry, NIC anticipate that it will generate strong operational cash flows.

As Nickel Mines approaches the sixth month anniversary of its ASX listing, it’s worth revisiting what the company has achieved in that time:

- Increased its stake in the Hengjaya Nickel Project from 25% to 60% for US$70 million;

- Secured material corporate income tax concessions for the Hengjaya Nickel Project from the Indonesian Government that will see it pay no corporate income tax for seven years with an additional two years at a 50% discount on the normal 25% corporate tax rate;

- Converted an MOU to acquire an additional two line RKEF Plant (Ranger Nickel Project) into a definitive Collaboration Agreement, and secured an initial 17% equity interest in Ranger Nickel for US$50 million;

- Signed an MOU to supply limonite ore to the new HPAL plant recently announced for construction within the IMIP; and

- Announced the Hengjaya Nickel Project is now commissioning and has produced its first NPI, having commenced construction in early 2018.

Nickel Mines a ‘Buy’

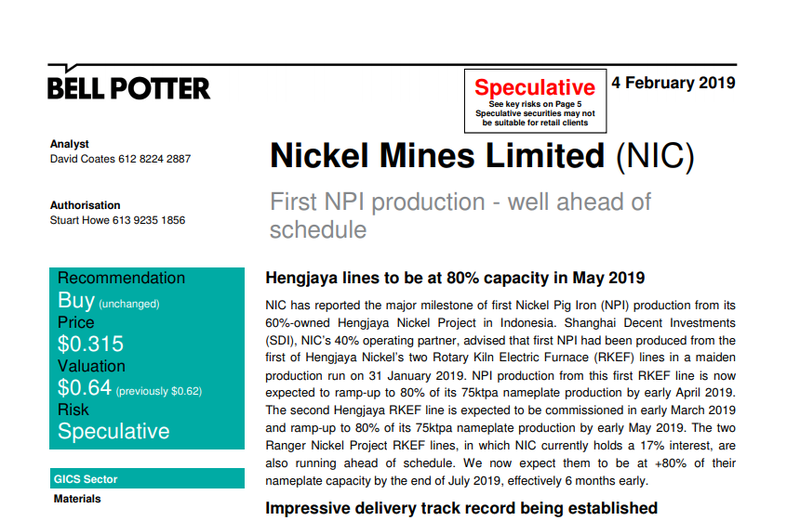

Following last week’s news of first production, Bell Potter analyst David Coates reaffirmed his ‘buy’ recommendation on the stock. He upgraded his forward earnings estimates and lifted his price target from 62 cents to 64 cents, implying share price upside of nearly 100% from the current 35 cent price.

“NIC remains one of our top picks in the sector on excellent value, strong production growth profile and the quality of its assets.”

The broker noted that other than the clear positive of earlier production and cash flow for NIC, the news will boost sentiment around the stock as it continues to build a strong track record of delivery. Of course broker predictions are speculative and there's no guarantee they'll eventuate.

The report notes that hard catalysts that could drive a re-rating of the stock in 2019 are advancing rapidly. As nameplate production is achieved, the market will have to take a fresh look at NIC’s production and cash flows and value it accordingly. NIC does plan to fund its growth via increased ownership of the Hengjaya and Ranger RKEF lines.

With long-life, low cost assets, Bell Potter recognises that NIC has a wide range of funding options available to it, in addition to its partnership with Shanghai Decent.

Value remains on offer

Having broken ground in early 2018, and now having already commenced production, Hengjaya Nickel

is further evidence of Tsingshan’s industry-leading ability to deliver a project in record time.

Benefitting from very low capital intensity and being among the lowest cost nickel producers in the industry, NIC expect to generate strong operational cash flows going forward, supported by a buoyant nickel price environment in the years ahead.

And as pointed out by Bell Potter a re-rating will likely be on the cards, “as nameplate production is achieved the market will have to take a fresh look at NIC’s production and cash flows and value it accordingly”.

Despite Nickel Mines having achieved so much in just six months, it’s hard to believe the company is now just getting back to its 35c IPO price.

But herein lies the opportunity for investors.

With the nickel price having recovered more than US$1/lb over the last month to current levels of around US$5.70/lb, and general sentiment toward the resources sector beginning to improve after a brutal last quarter of 2018, it can be expected that this positive news flow may soon be reflected in NIC’s share price.

If it does, NIC might just prove itself the next big thing in nickel, establishing itself as a tier-1 investment among listed nickel producers.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.