BLK Will Start Mining Gold in 3 Weeks

Published 21-JUN-2016 11:36 A.M.

|

13 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Australia’s brightest gold junior is nearing its first gold pour – scheduled for September.

In just three weeks’ time it will start mining.

Blackham Resources (ASX:BLK) has been diligent in its gold exploration to now stand at the threshold of moving from explorer to gold producer.

An economic mine plan containing 873,000oz. has been defined, BLK is funded all the way to September production and has a plethora of positive caveats in its Matilda Gold Project economics.

Over the past year, BLK has gradually progressed its 4.8 million oz. Matilda Gold Project from initial exploration to now stand on the precipice of going into production.

BLK’s value has gone from around $0.15 per share when we first published our article, ‘ ASX Junior to Unleash 100koz pa Gold Machine: Funding Now Secured ’ in May 2015, to around $0.47 per share today. In between it’s been up as high as 300%, since our first article.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

BLK has recently upgraded its DFS and improved its project economics in several key areas which means 100,000oz per annum of gold production will commence later this year.

Helping this along will be its agreement with Interim Resources Ltd (ASX:IRC) to purchase their calcine tailings stockpile located next to the Wiluna Plant. The stockpile comprises a JORC Indicated Mineral Resource Estimate of 370,[email protected]/t Au for 59,5000oz.

BLK continues to beef up its longer-term mining inventory as well – with gravity and passive surveys firming up 25 new targets, 12 of which are high-priority .

And as BLK rushes toward first gold production at Matilda, it has also begun a program aimed at extending the amount of inventory available to mine.

BLK’s greenfields exploration programme is designed to build upon the current eight year mine life at Matilda through the discovery of additional free-milling ore close to the planned Matilda, Golden Age and Williamson mines.

The Matilda Gold Project has now gained all its approvals and funding commitment required to commence operations at the Matilda Mine and underground mining at the high grade Golden Age orebody .

Now, before we go too far, it should be reiterated, that like all speculative gold stocks, you should still take a cautious approach to your investment decision with regard to this stock.

The Golden Age initial mine plan consists of 206,[email protected]/t for 38,000oz of free milling ore which will be mined over the first two years. The underground reserve comprises 112,[email protected]/t for 21,000oz.

There are currently five drill rigs completing infill and extensional drill programmes and recent successful drilling, resource upgrades and open pit and underground mine design optimisations have added 43,000oz to the free milling reserves.

BLK has added [email protected]/t for 106,000oz in Mining Inventory since publishing its Definitive Feasibility Study in February.

What’s also putting the wind in BLK’s sails is the gold price continuing their advance – especially when measured in Australian dollars.

BLK is now on the cusp of becoming Australia’s next gold producer, and giving the commodity naysayers a counter-punch of exactly the right kind as it progresses towards ‘mid-tier producer’ status.

Assaying:

![]()

Blackham Resources (ASX:BLK) has achieved what most other junior gold explorers have failed to do in recent years...

...advance a gold project amidst recent price tilts as well as a broader pullback from all commodities. This has been a tough slog – but the good news is that BLK has managed to get its house in order and define one of the most significant new gold Resources in Australia.

BLK’s share price illustrates just how successful the company has been. BLK was the second best performing Aussie gold stock in 2015 and has doubled in price during 2016. We first shone the spotlight on BLK way back in May 2015, in the article ASX Junior to Unleash 100koz pa Gold Machine: Funding Now Secured – since then the stock has been up over 260%:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

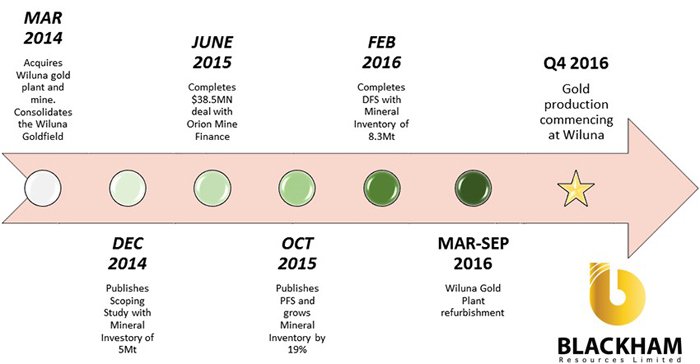

Here’s a timeline of BLK’s progress since acquiring its Matilda asset in 2014:

BLK’s rise has been a textbook story of strong project economics being progressed diligently and with ample institutional funding.

Recently BLK reported that as a result of receiving vegetation clearing permits over the entire main plan by the Department of Mining and Petroleum (DMP), Orion Mine Finance confirmed a $23 million Project Facility is now available under the revised funding agreement. The expiry term has been extended until 28 February 2019, with payments being marched to gold price and cash flow.

Furthermore BLK lodged a drawdown notice for $15M which it expects to receive in June.

With strong finances and a DFS to match, BLK is in a strong position.

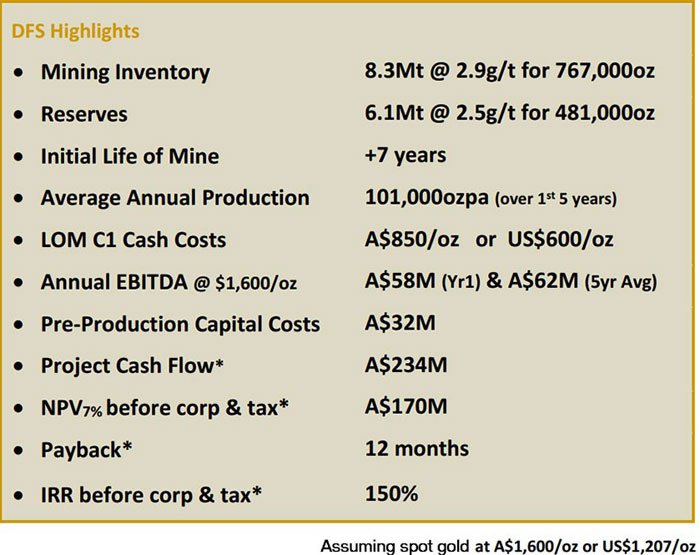

Take a look at BLK’s Definitive Feasibility Study (DFS) results published back in February.

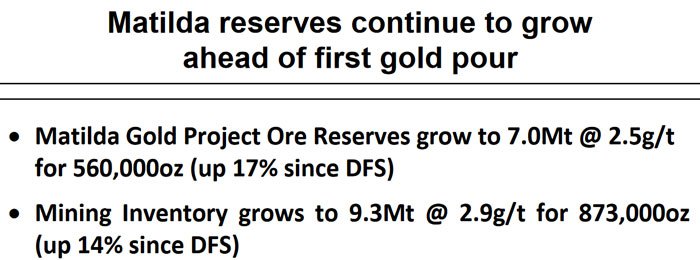

Not only did BLK deliver a rather bulky 8.3Mt Mining Inventory and estimated Reserves of around 480,000oz – BLK then went one better and further upgraded these figures just recently.

Here’s the current resource status for BLK, and as you can see it’s grown since BLK’s DFS to 560,000oz – up 17%.

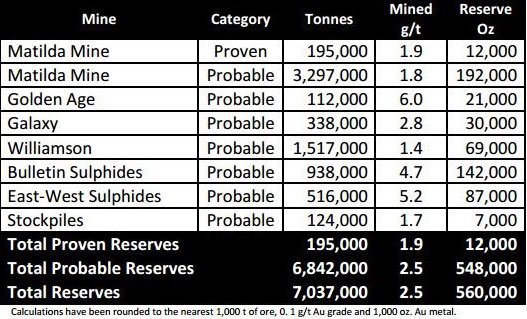

And here’s the full breakdown of where BLK’s gold is located across the Matilda Gold Project:

As you can, there is much going on and BLK is moving quickly into production with its mines already hinting at successful resource production.

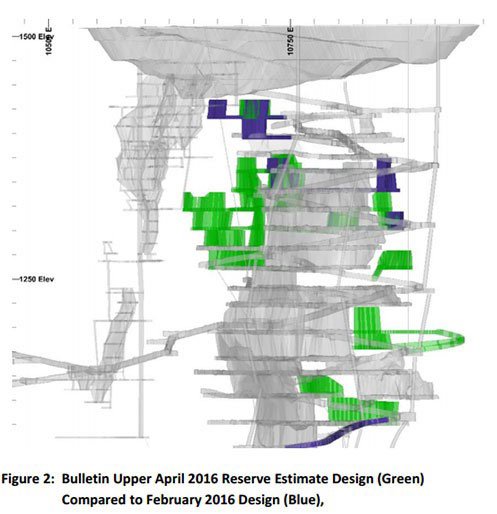

This Bulletin expands BLK’s Resource to 46Mt

BLK also released an updated resource for its Bulletin underground orebody.

Bulletin is likely to be the first of the sulphide underground mines to come on line at around Year 3 of its planned Matilda Project, benefitting substantially from extensive existing infrastructure.

The new resource of 1.6Mt at 4.8g/t for 247koz (50% Indicated) increases BLK’s total resource for the Matilda project to 46Mt at 3.3g/t for 4.8Moz. It’s Measured and Indicated resources now total 21Mt @ 3.4g/t for 2.4Moz.

What’s really important about BLK’s entry strategy is that it is aiming for low-risk shallow (<500 metres) mining first and foremost. This greatly de-risks BLK’s overall operations and reduces the chances of unforeseen costs entering the picture.

The Bulletin Reserve now stands at 938,000 tonnes @ 4.7g/t for 142,000 ounces.

Take a look at this illustration showing BLK’s progress at its Bulletin prospect with blue areas showing February’s estimates, and green areas showing what’s been added in April.

BLK is now in top gear and racing towards production with as much in the tank as possible.

BLK’s DFS and subsequent Resource upgrades show that BLK is the most capital efficient and economically viable gold producer compared to any other in Western Australia

From a Resource perspective BLK isn’t done yet and wants to add to its Resource.

But already its Matilda project economics are standing out rather well. BLK already owns 100% of the Matilda Gold Project including the Wiluna gold plant, gas power station, camp, bore-fields and all underground infrastructure needed for production.

And it recently entered into an agreement with Interim Resources (ASX:IRC) to purchase 100% of their calcine tailings stockpile located next to the Wiluna Plant, adding a JORC 2004 Indicated Mineral Resource Estimate of 370,[email protected]/t for 59,500oz.

The acquisition, for which BLK will pay a total of $1.5 million for the tailings, which are the residual product from cyanidation of roasted sulphide concentrates produced prior to WW2 from Wiluna gold ores, will give BLK greater flexibility over the placement of tailings within the direct vicinity of the plant.

The project economics has helped BLK to establish a Payback time of just 12 months on its planned investment and development of Matilda.

BLK’s cash, liquid investments, together, with a recent $20MN financing boost means BLK is fully-funded to production.

BLK completed a A$20.3MN Placement to institutional investors in March. The Placement shares were snapped up with “strong support” which is yet another sign that the institutional smart money likes this stock.

However, this is still a junior resources company and a speculative stock – it’s always a good idea to seek professional advice before choosing to invest in stocks like BLK.

The additional funds allow for an immediate acceleration of development at Matilda.

First on the list is the refurbishment of the Wiluna gold plant which is on track for completion by September 2016.

Next, BLK wants to fast-track reserve and resource drilling across its Matilda gold project and provide adequate working capital as it transitions into production.

The additional drilling is important because it could potentially allow BLK to expand its mine life from 7 to 10 years and possibly beyond. If all goes to plan, this could be expanded even further subject to more exploration drilling and Resource upgrades.

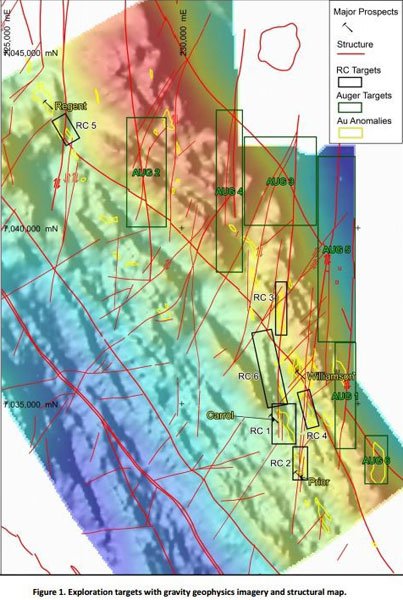

Exploration at Lake Way

In a recent announcement, BLK informed the market of exploration targets defined from detailed gravity and passive seismic geophysical surveys completed at the Matilda Gold Project.

BLK’s greenfields exploration programme has been set up to extend the current eight year mine life at Matilda through the discovery of additional free-milling ore close to Matilda and the Williamson mine.

The programme is aimed at extending the amount of inventory available to mine and BLK has identified an area close to its existing Williamson and Regent deposits known as the Lake Way district which contains a salt lake.

The Salt lakes proved difficult to delineate a gold resource in the past as the salt cover obscured previous surveys.

Previous drilling conducted was broad based with limited multi-element analysis completed, so by conducting gravity and passive seismic surveys, BLK thinks it may have found a solution to this problem and could discover blind deposits under the lake cover.

BLK has now firmed up 25 target areas – including 12 areas it has labelled as targets for high-priority drilling.

Below are the targets...

Here at The Next Mining Boom , we think BLK’s development prowess will continue as it has since 2014, with BLK soon to kick-start production and moving confidently towards becoming a mid-tier producer over the mid-long term.

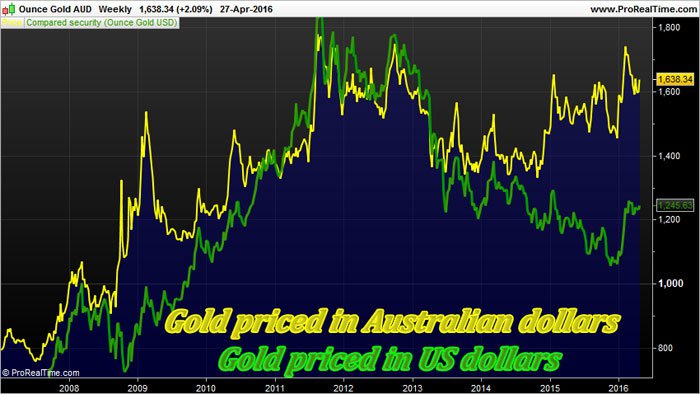

One factor that has recently been in BLK’s favour is the parallel improvement in BLK’s terms of trade courtesy of the Aussie dollar.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Gold priced in Aussie dollars continues to climb while in US dollars, it is still sagging at around US$1,100-1,200 per oz.

The mean-weighted average gold price for the past 5 years has been A$1,520/oz. which adds further confidence that Matilda’s gold will generate strong profit margins once fully operational.

This macro factor is a great boon for BLK – and here’s why...

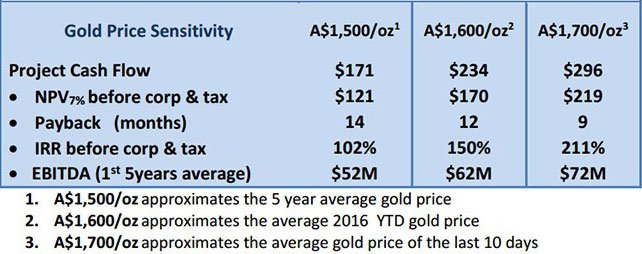

Every $100/oz. increase in the gold price adds roughly $73 million to BLK’s cash flow.

Matilda’s C1 cash costs and cash operating costs (AISC-all in sustaining costs) are forecast to be $850/oz. and $1,160/oz. with an underlying gold price of $1,600/oz.

Of course this is a commodity price we are talking about, and it’s going to fluctuate – so economic figures are no guarantee to eventuate, and keep that in mind if considering making an investment here.

With gold prices now starting to get some support in tandem with BLK’s strong progress on exploration, Australia’s next producer is walking into a favourable market landscape that is geared for efficient gold producers with low-cost production.

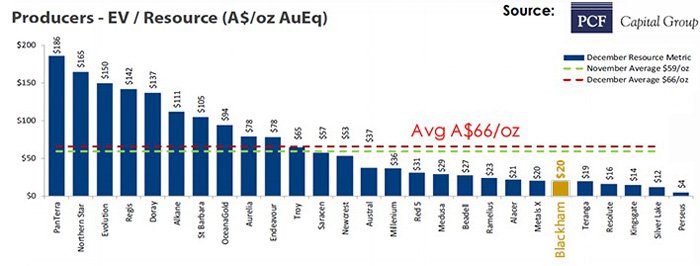

From an EV/Resource perspective BLK is currently sitting around $20/oz.

BLK is still therefore significantly undervalued when considering the above metric.

With strong production efficiency confirmed in its DFS, here’s how that translates for BLK on the front line of production in a few months’ time:

Currently, spot gold prices are at around $1650/oz. and could potentially add more cheer to BLK’s project economics if they continue advancing like they have been recently (and trending higher since 2008).

Analyst research

In our last update article BLK is Australia’s Next Gold Producer we looked into what various research analysts were saying about BLK to see if it matched our own conclusions.

The same analysts are still positive with revised estimates backing BLK’s business plans.

Take a look at this research note from The Sophisticated Investor analyst Adam Kiley who has placed a 99c price target on BLK, which is an 98% premium on today’s price of A$0.50:

At the same time, analyst price targets are no guarantee to come true – so don’t only consider this price target if considering an investment in BLK – please do your own research and consider your own personal circumstances before making an investment decision.

Last but not least, there is one more additional factor that could give BLK a serious boost...

When it comes to exploring for any Resource or progressing multifaceted mining projects, it helps to have a guru in your corner.

BLK has brought in 2012 AMEC Prospector of the Year, Bruce Kendall into the fold – and it’s a human acquisition that could have a major impact.

Mr. Kendall has over 20 years’ experience in managing near mine gold exploration (exactly what BLK is currently busy doing). He’s had previous spells at BHP, Jabiru Metals, Independence Group and AngloGold Ashanti, a US$6BN-capped mature gold miner.

At all his engagements he has proven his mettle by adding 1Moz at the Sunrise Dam Gold Mine, and a further 1Mt at the Stockman VMS project. It was his Tropicana gold discovery in Western Australia (a new gold province) which earnt him the AMEC Prospector award alongside Brett Keillor.

Mr. Kendall knows exactly how to thread the eye of the gold production needle, and how to weave a mid-tier gold tapestry for BLK. That’s exactly what he’s been recruited for as Chief Geological Officer.

With him on board, BLK hopes it can raise the mine life at Matilda still further and expand its operational capacity across all its gold prospects.

On the cusp of production, BLK is a standout junior

With its operations, project economics, funding and personnel all neatly aligned, BLK is making excellent progress with market traction also growing.

BLK is growing its value as resources are upgraded while production approaches later this year in September.

BLK offers investors an opportunity to back a junior gold explorer gradually transforming into a mid-tier producer.

Seeing its Matilda Project approaching first gold pour with 9.3Mt @ 2.9g/t for 873,000oz in the mine plan is a feat that trumps the activities of any other junior gold explorer currently listed on the ASX.

When you throw in the caveat of BLK’s superior project economics in comparison to its peers, BLK offers a compelling case as an early-stage investment that could bear significant returns for investors in the coming years.

Remember however that this is a speculative mining stock, and any investment decision made with regard to this stock, should be done with the utmost caution.

Fully-funded to production and plans to expand activities over the coming years, we think this junior is going places.

Stay tuned to this one.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.