AW1: Copper Resource Upgrade plus USA Critical Minerals… and some silver too.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 14,722,222 AW1 shares and 7,361,111 AW1 Options at the time of publishing this article. The Company has been engaged by AW1 to share our commentary on the progress of our Investment in AW1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Humans will need to mine more copper in the next 18 years than we have mined in our entire recorded history.

This is just to meet the forecast demand of AI data centres, grid upgrades, chips, weapons systems and electrification.

That's SIX new Tier 1 copper mines coming online every year, for the next 25 years.

(good luck with that).

Two weeks ago the copper price hit the highest it has been in its history.

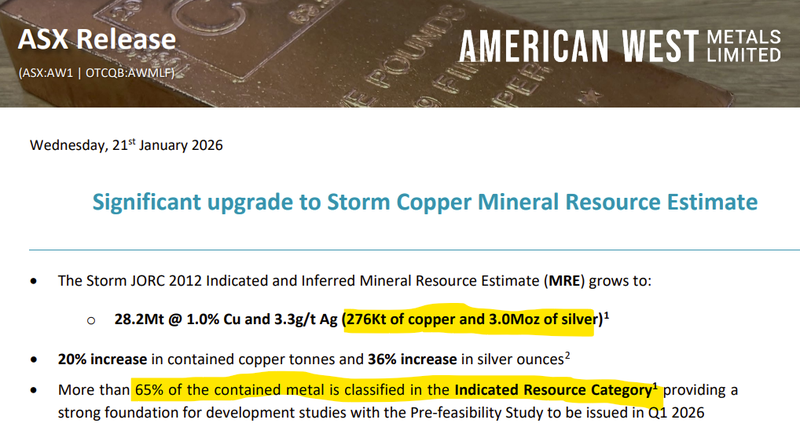

This company now has a resource of 28.2Mt @ 1.0% Cu and 3.3g/t Ag (276Kt of copper and 3.0Moz of silver).

It’s in an advanced stage, with a PFS due this quarter, and 80% of CAPEX for development already secured.

(Mining supermajors BHP and Antofagasta have both previously JV’d into this project, pulling out only after copper prices tanked - so it's potentially large enough for the mining big dogs to be interested)

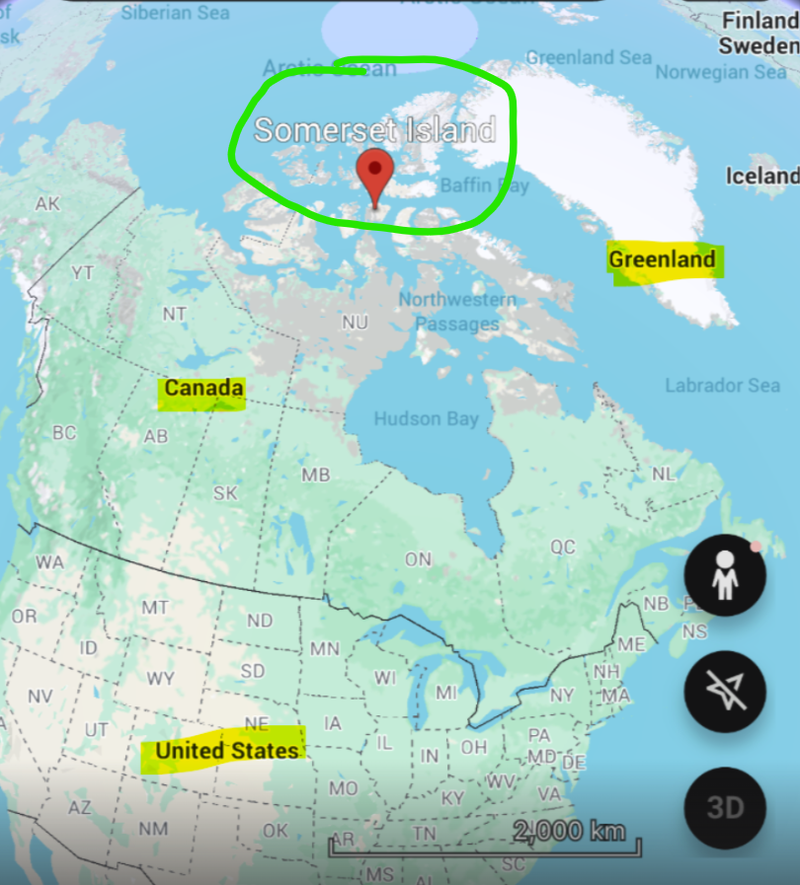

And it’s located right near the USA’s current favourite “region of strategic interest” - Greenland.

(the USA is keen on Greenland for its strategic location and natural resources /critical minerals - we expect a lot of energy and attention to be flowing to this general region over the coming years)

And this copper stock is... American West Metals (ASX:AW1).

We originally Invested in AW1 back in October 2025 because it has the biggest and only indium resource in the USA.

We also liked its development stage copper project in Northern Canada.

Today AW1 increased its resource to 28.2Mt @ 1.0% Cu and 3.3g/t Ag (276Kt of copper and 3.0Moz of silver).

(3Moz of silver too... well hello, hello)

(source)

Again, Back in October 2025 we Invested in AW1 because it has the biggest (and only) indium resource in the USA.

Indium is named by the USA as a critical mineral.

Indium is used in things like infrared detectors, night vision systems, missile guidance systems, Radar systems and F-35 fighter jets...

The USA has zero domestic indium production, relying 100% on imports to meet its demand.

(US based critical metals are back in 2026 - read our full commentary on AW1’s indium resource here)

When we first invested in AW1 one of our key reasons was we thought the valuation was underpinned by its other asset...

An advanced stage copper project in the Northern regions of Canada (close to Greenland).

(source - our AW1 launch note October 2025)

AW1 is steadily moving an advanced stage copper asset in Canada toward development.

Just as the copper price hits all time highs.

AW1 already has a funding pathway lined up for the CAPEX, it's proven the economics are robust - and a PFS is due this quarter.

Today AW1 increased its resource to 28.2Mt @ 1.0% Cu and 3.3g/t Ag (276Kt of copper and 3.0Moz of silver).

That’s a 20% increase in contained copper tonnes and 36% increase in silver ounces.

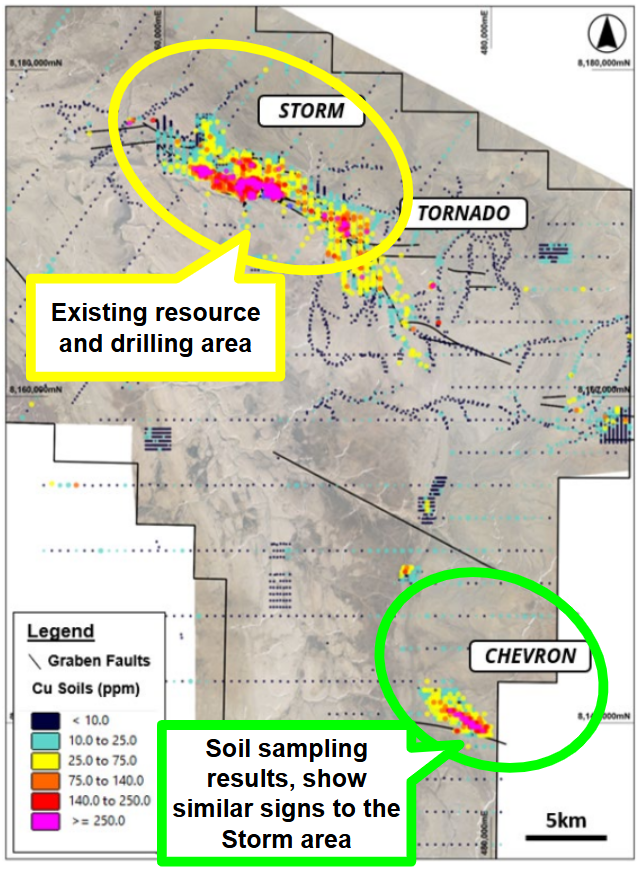

With some drilling we think that it can grow even further - there’s 8 high grade prospects ready for drilling, and less than 5% of the 110km copper bearing horizon has been adequately explored.

(source)

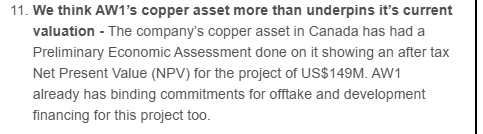

AW1’s next major catalyst for the asset will be drill results and that upcoming PFS...

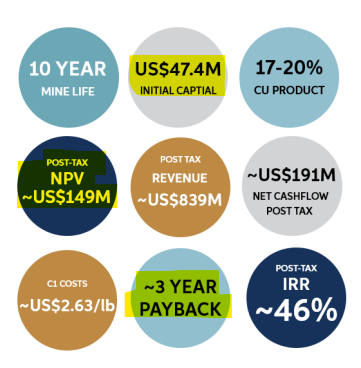

The last time a study was done on the project, it returned US$149M NPV from US$47.4M CAPEX.

This is a pretty modest capex number, and the economics of the asset are way above the 2:1 NPV/CAPEX ratio we normally like to see.

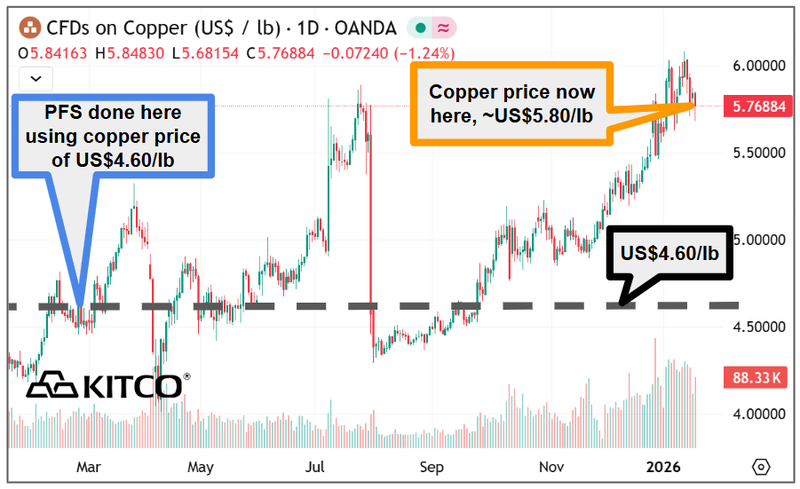

That study was based on a copper price of US$4.60/lb - the copper price is currently ~ US$5.80/lb.

(Source)

AW1’s market cap at A$70M is below the NPV of its copper project... and as mentioned earlier, the “biggest indium deposit in the USA” is also 100% owned by AW1.

Permitting is underway, and there are two funding deals in place for up to 80% of the project's CAPEX to get into production...

It’s entirely possible that this project actually makes it into production in the current bull market for base metals...

Copper is usually seen as the most “boring” of the critical minerals because of the maturity of its market. Copper has been used and traded for thousands of years - and the market is massive and liquid.

But copper prices are now running... and the US tech capital rotation into metals and mining might be going into copper first...

Silicon Valley billionaire tech venture capitalist Chamath Palihapitiya singled copper out as his “best trade idea for 2026” and said “the material manifests in everything from our data centres, to chips to our weapons systems”.

(source)

There’s plenty more copper bulls out there, but what makes Chamath’s call interesting is that it comes from outside of traditional mining investors.

This is a smart guy that made his billions by investing in software companies, and he has decided his best trade idea in 2026 is... copper.

To get a better idea of the macro trend for copper, check out this presentation titled “Dawn of the copper age given by Founder and Chair of Ivanhoe Mines, Robert Friedland.

(This preso was delivered at the Saudi Arabia Future Minerals Forum a few days ago)

Coming back to AW1’s advanced stage copper asset...

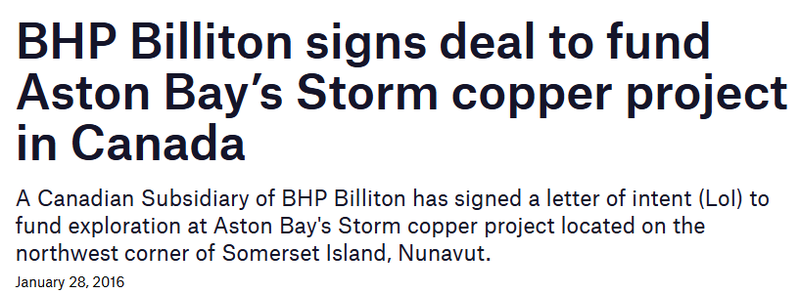

Over the years, the AW1’s projects actually had both $248BN BHP and $70BN Antofagasta sign Joint Ventures to earn into the asset.

(They wouldn't be sniffing around if the asset didn't meet their size/scale criteria)

Both walked away because the copper price was too low in the mid-2010s and instead focused on large porphyries in South America.

Yep, this copper asset once attracted mining supermajor BHP to it... and we think the market is missing just how big the project could get for AW1.

It’s also attracted some high quality people to study its geology and the potential for a large discovery.

David Broughton has been a technical advisor to AW1’s partner Aston Bay Holdings on this project.

David previously worked for Robert Friedland (yep the same Robert Friedland from the video earlier), and is co-credited with the discovery of some of the world’s largest copper discoveries.

You can watch him talking technical about AW1’s asset here.

We originally Invested in AW1 late last year because we thought the copper asset more than justified AW1’s valuation, which gave us a “free kick” at the indium asset...

That was three months ago when copper was trading at ~US$4.9/lb.

Now copper is at an all-time high and is climbing quickly...

(source)

One of AW1’s Directors is John Prineas who is the Exec Chairman of one of our best performers from 2025 - St George Mining (ASX: SGQ).

(SGQ was briefly up by over 1,000% in 2025 and is already up 26% in the first weeks of 2026).

Interestingly, we initially went into SGQ for the niobium (and saw the rare earths as the free kick upside) - but we think the rare earths aspect to SGQ was what took the company’s share price from a low of 1.5c in April to a high of 18c in October last year.

Maybe the same thing happens for AW1?

(Past performance of SGQ is not and should not be taken as an indication of future performance of AW1)

As mentioned earlier, AW1 has already delivered a Preliminary Economic Assessment (PEA) for its project that showed the project had a post-tax Net Present Value (NPV) of US$149M based on CAPEX of US$47.4M. (source)

That study was done using a copper price of US$4.60/lb and US$25 per ounce for silver.

The copper price is now closer to US$5.80/lb, and silver is at US$95/oz.

Hopefully the bigger resource from today and the higher commodity prices translates to improved project economics...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

AW1’s market cap today at ~$70M is below the NPV of its copper project...

(so we think we are still getting a pretty good “free kick” at the indium asset mentioned earlier)

AW1’s copper asset previously attracted BHP to farm in

We think AW1’s 80% owned copper project underpins the company’s current $70M valuation.

AW1’s copper project has just had a resource upgrade to a 28.2Mt resource with average grades of 1% copper and 3.3g/t silver - for a total 276Kt of copper and 3.0Moz of silver.

Back in 2016 the same asset attracted BHP to them via an earn-in deal that would have seen BHP spend US$50M on the asset.

Clearly BHP saw potential for size/scale that was worth their time here - a good sign for AW1 attracting future partners.

(Source)

The deal fell through in 2018 - walking away because the copper price was too low at the time and they preferred to focus on large porphyries in South America.

Then, in 2021 AW1 signed an earn-in deal to acquire 80% of the asset (from the now 20% owners Canadian Aston Bay) by spending a minimum of CAD$10 million on exploration expenditure.

Interestingly, AW1’s Managing Director Dave O’Neill is also ex-BHP (though from a few years before that deal for AW1’s copper asset was done).

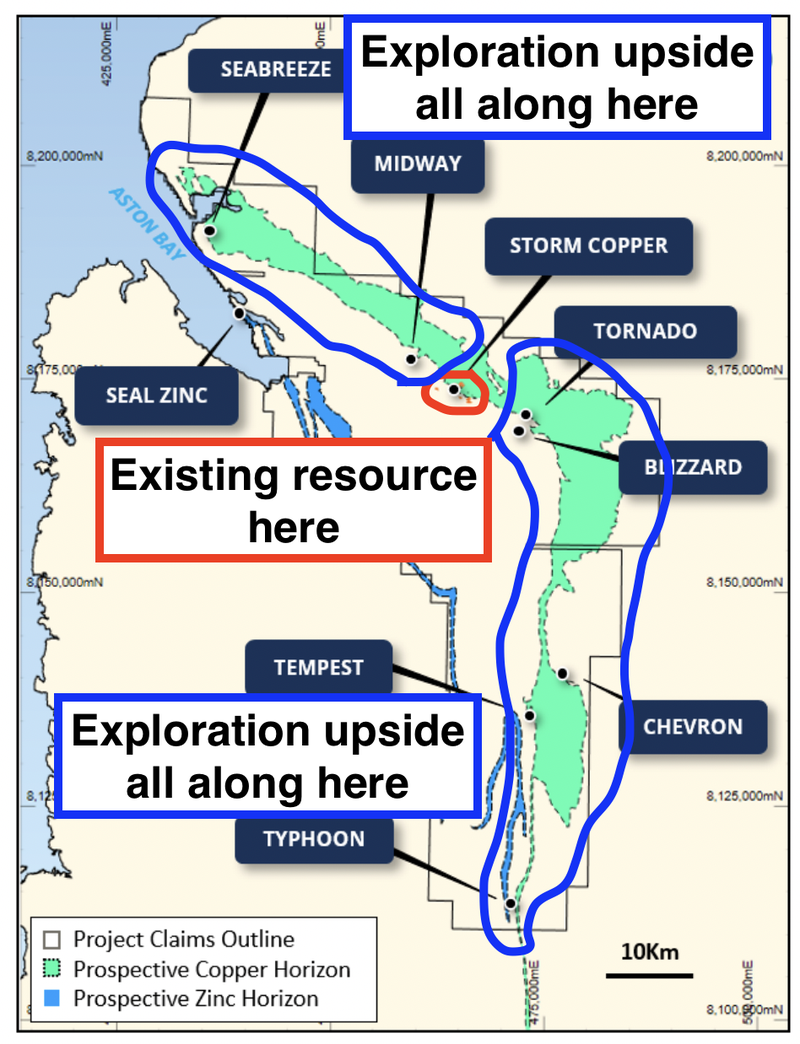

We think AW1’s copper project has big exploration upside

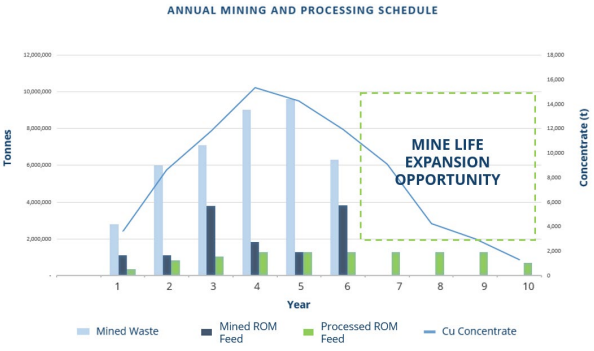

At the moment, the project modelling is based on ~6-year mine life and 10 years of processing.

So exploration upside here matters, to extend the mine life beyond years 7 and beyond:

(Source)

AW1’s project is largely undrilled at the moment. Drilling is ongoing right now across the multiple regional targets on the project.

For context, below is where the resource sits relative to that “prospective copper horizon” AW1 has referred to in announcements - marked in green:

(source)

We think that (with some exploration luck), AW1 could add to its resources in a big way.

For some context, below is just one of the targets AW1 is yet to drill... a 4.1km by 0.7km undrilled soil anomaly - here is that target area relative to AW1’s current JORC resource:

(Source)

IF AW1 found something there, it could multiply its current resource very quickly.

AW1 already has a fairly clear pathway to a big chunk of CAPEX financing

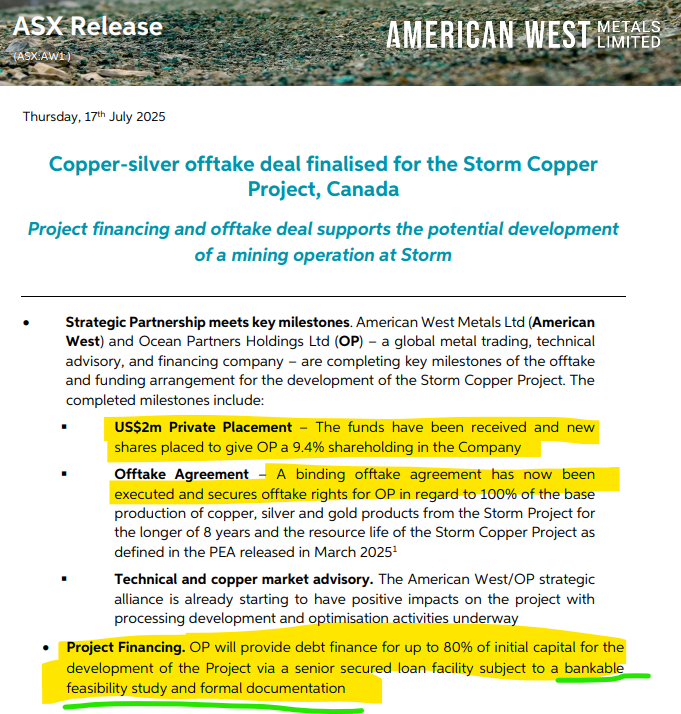

Another reason we like AW1’s copper project is that it has attracted two project financing deals.

AW1 did a deal with Ocean Partners for the project via a 9.4% equity stake in the company and a binding offtake agreement which could see ~80% of the project’s CAPEX financed...

(Source)

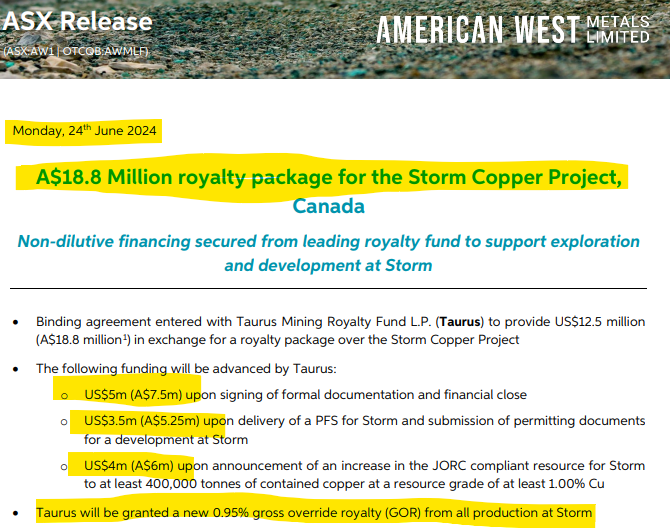

Back in June 2024, AW1 also did a royalty deal for A$18.8M in non-dilutive financing for the project.

(Source)

Despite how advanced the project is and the funding deals underwriting it, AW1 still only trades at A$70M.

(and of course there is that wildcard USA indium asset we mentioned early in today’s note).

With the copper price running now, we think the market could start to take a look at AW1’s asset a lot more seriously again.

Ultimately though, we originally went into AW1 for something big from the US indium asset:

Our AW1 Big Bet:

“AW1 receives capital from either the US government, a strategic partner or the capital markets to progress its Indium project in the USA, re-rating AW1 to a valuation that is multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AW1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for AW1

Sampling of previous drilling on US critical minerals project 🔄

We are looking forward to the results from the re-sampling on the US asset.

We are especially looking forward to seeing if the indium resource gets bigger AND if AW1 can define a large gallium resource to go with its current resources.

Results from the sampling are expected in 3-4 weeks.

(Source)

Pre Feasibility Study (PFS) for Canadian copper project 🔄

We are looking forward to news from the company’s Canadian copper project.

Especially now with copper prices running.

We want to see AW1 deliver its Pre-Feasibility Study this quarter, and in time, the key permits related to developing the project.

Here are the milestones we will be tracking:

🔄 Pre-Feasibility Study

🔄 Environmental Studies

🔄 Mining/development permits

What are the risks?

In the short term the two key risks are “critical minerals macro thematic” and “permitting risk”.

First, the US asset is heavily reliant on the macro thematic for US critical minerals being strong.

If there are downturns in sentiment then the likelihood of AW1’s project being developed decreases.

Critical Minerals Macro risk

A big part of our Investment is related to critical minerals macro sentiment strengthening and resulting in a funding deal for AW1’s US indium project. IF macro sentiment was to turn, then the chances of that asset being funded/brought online would reduce significantly. This could mean a re-rate lower in AW1’s share price.

Source: “What could go wrong” - AW1 Investment Memo 16 October 2025

For the Canadian copper project, the key risk is permitting.

Like all mining projects, it's possible that permits are rejected or delayed which could push back the development timelines of the project.

Permitting Risk

AW1 will need to get permitting in order for its Canadian copper project. If this permit is delayed or rejected it may be a drag on the AW1 share price.

Source: “What could go wrong” - AW1 Investment Memo 16 October 2025

Other risks

Like any small cap resource exploration & development company, investing in AW1 involves a range of risks, some known, some unknown (this is the nature of investing in early-stage companies).

Here we aim to identify a few more risks.

AW1’s indium project, while large and strategically located in the US, is still at the pre-development stage. There is a risk the project does not progress to production or that feasibility studies show weaker-than-expected economics.

The indium market itself is small, opaque, and subject to significant price swings. Limited transparency around pricing and supply chains could impact project valuation and investor sentiment.

Although AW1’s US project is fully permitted for an open-pit mine, the company will still need to secure ancillary approvals for development and production. Any delays or regulatory changes could push timelines back.

There is also the risk that AW1 is unable to attract US government or strategic funding despite being well-positioned in the critical minerals thematic.

AW1 remains reliant on capital markets to fund project development. Future equity raisings could dilute existing shareholders, while debt funding may not be available on favourable terms.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our AW1 Investment Memo

You can read our AW1 Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our AW1 Investment Memo covers:

- What does AW1 do?

- The macro theme for AW1

- Our AW1 Big Bet

- What we want to see AW1 achieve

- Why we are Invested in AW1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.