AVM step out drilling hits visible gold - assays in coming weeks

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,500,002 AVM Shares and the Company’s staff own 200,000 AVM Shares. The Company has been engaged by AVM to share our commentary on the progress of our Investment in AVM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

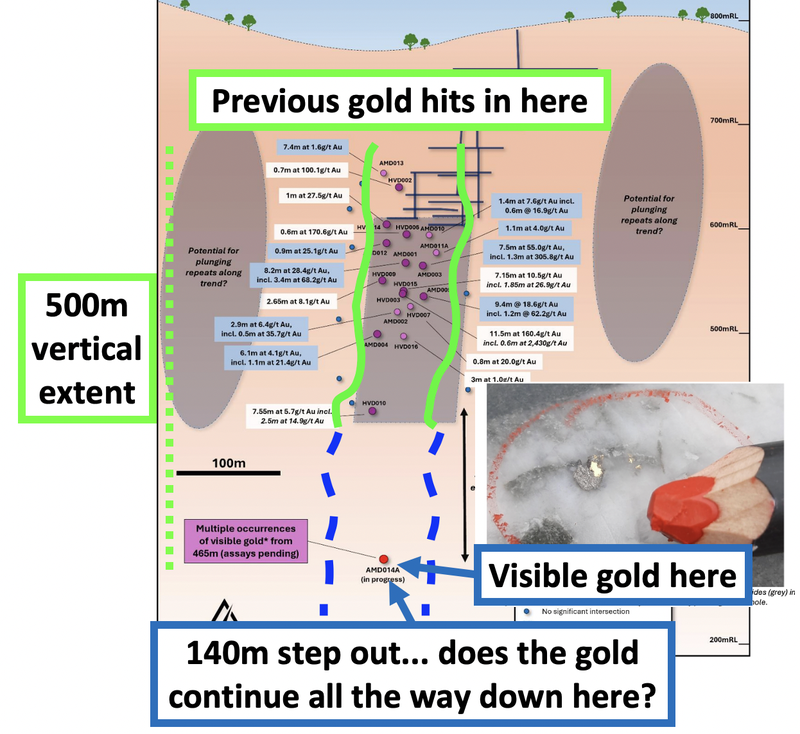

There it is...

Visible gold in the deepest hole from our Investment Advance Metals (ASX:AVM) Victorian gold exploration project.

(Source)

The visible gold came from a 140m step out hole - which (pending assays in 4-5 weeks) could mean AVM’s gold system runs over ~ 500m vertically.

A decent set up for a potentially regionally significant gold discovery...

Given today’s news, AVM is already considering a strategy to get another rig on site - maybe multiple rigs that can make new discoveries will be the trigger for comparisons being drawn between the $1.1BN Victorian gold explorer Southern Cross Gold and AVM?

AVM’s high grade gold project has in the past produced gold at average grades of 31 g/t.

AVM is now drilling below the old workings, to see if the high grade gold extends beyond the previous mine shafts AND the previous drilling on the project.

The visible gold in today’s announcement is from the deepest hole ever drilled on the project...

(while it’s deep - it's much shallower than Falcon’s 600m drill hits in Victoria that sent its share price from ~10c to $1.18 per share a few months ago and a ~$230M market cap - more on this later).

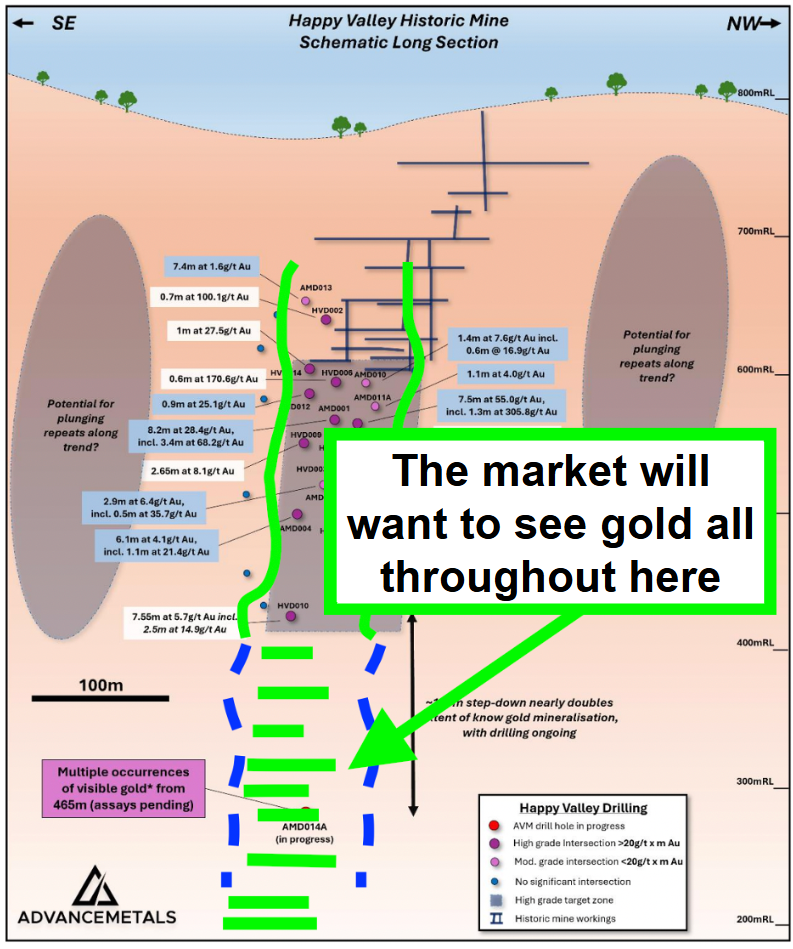

We said in our last note that the market will be wanting to see continuity of gold mineralisation as AVM drills deeper to really start to get interested in this project.

Now AVM’s got visible gold 140m below any of the previous drilling...

AND the whole system is open in all directions (meaning it can get a lot bigger with some step out holes to the north, south, east and west).

Again, here is what it looks like:

(Source)

The caution here is that visible gold in drillcores doesn’t guarantee high grades in relation to lab assay results - we will need to see final lab results before we can comment about how that “worm” in the image above has grown with any certainty.

AVM expects to have final assay results in the next 4-5 weeks.

IF assays come in and confirm grades similar to the previous holes (50-150g/t gold) then it could be game on for AVM...

A recent peer comparison shows the upside for AVM...

AVM is following the same playbook that re-rated another Victorian gold explorer Falcon Metals from ~10c to $1.18 per share (now it trades at ~65c per share).

Falcon had visible gold in the first parts of its first hole. AVM just hit visible gold today.

The main differences between AVM and Falcon is that the two assets are in different parts of Victoria AND AVM is hitting gold at much shallower depths.

Falcon was hitting gold mineralisation at 600m+ depths. AVM is hitting gold from ~300M depths.

Final assays really started moving Falcon’s share price, and then more visible gold (and assay results) took its share price to a high of $1.18 where Falcon’s market cap peaked at ~$250M.

AVM is capped at $32M, having just raised $13M... so the company’s enterprise value is somewhere around ~$19M (we should see a quarterly any day now which will give us a look at an updated cash balance too).

We think that any assays from AVM that are even remotely close to Falcon’s results could really get the market going here.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now we just need to wait for the assays from today’s visible gold sections...

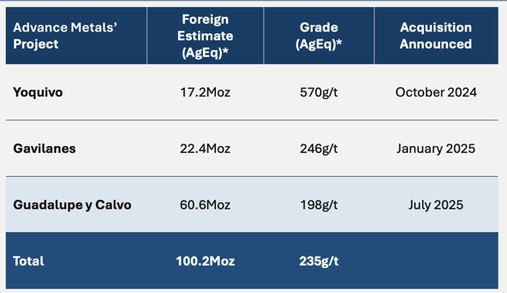

As well as the Victorian gold exploration asset, AVM also has a portfolio of Mexican silver assets - with a combined ~100M ounce silver equivalent foreign resource estimate across the three projects.

(more on the Mexican silver in a second)

What we want to see next from AVM’s Victorian gold project

What we want to see here is continuity...

It's not so much about size, as long as the grade is high and it continues over a long enough area it could be game on for AVM.

(Source)

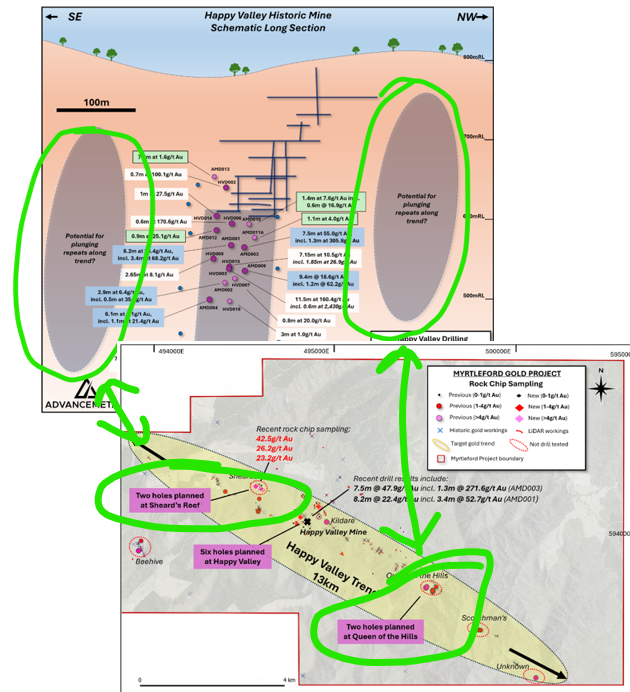

Given the significance of today’s result, AVM is now developing a follow up exploration strategy which may include sending additional drill rigs to site.

AVM also plans to start drilling regional targets in mid-November to get a better picture of the broader mineralisation trend

So there is still a lot to play out on this project over the coming weeks/months.

AVM previously said it would start drilling “undrilled prospects along strike to the northwest and southeast immediately following the completion of the current hole”. (source)

Both those areas have historic gold workings and rock chips at surface (some grading as high as 42.5g/t gold...

And they have never been drilled before...

(Source)

AVM’s board and register are now a lot stronger

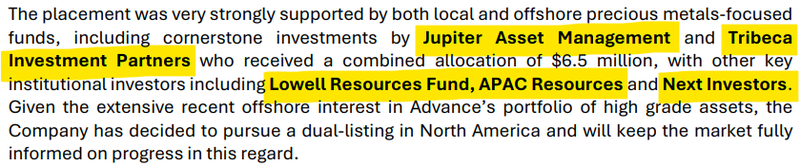

AVM recently closed a $13M capital raise at 10c (above where AVM is trading today).

The $13M capital raise triggered a complete corporate restructuring of the company.

The capital raise brought onto AVM’s share register multiple institutional investors including - Jupiter Asset Management, Tribeca Investment Partners, Lowell Resources Fund and APAC Resources.

(Source)

Jupiter Asset Management and Lowell Resources coming into AVM was especially interesting to us.

Both Jupiter and Lowell are investors in Falcon (see above) - so they will know what a good Victorian gold exploration project looks like. (Source) (Source)

Both Jupiter and Lowell are also investors in Mithril Silver and Gold (ASX: MTH) - so they know what good assets in Mexico look like too. (Source)

(MTH is one of the biggest positions in our Portfolio and the only other Mexican silver/gold stock on the ASX)

Since we Invested in AVM, and following the capital raise, AVM has strengthened its board adding:

- David O’Connor as Chairman - ex-Chief Geologist at AbraSilver where he grew the company's Diablillos Silver-Gold Project from 129Moz to 350Moz silver and a $1BN+ market cap.

- Douglas Coleman (Mexican advisory board member) - Founder of the Mexico Mining Center and previously held senior roles with Appian Capital Advisory who “collectively brought 60+ mines into production and managed transactions in excess of US$200 billion.” (source)

- Trevor Woolfe (Mexican advisory board member) - Extensive global experience in exploration and corporate development, including as Director and former VP Exploration & Corporate Development at GR Silver Mining, a $100M+ company with silver and gold projects in Mexico.

The Chair appointment especially got us interested - with a very strong track record working up Mexican assets with Abra.

We are hoping he can do something similar with AVM’s portfolio of assets in Mexico...

More on AVM’s silver assets in Mexico

First let's talk about the silver price.

It has recently come off a little from its all time highs.

We’ve been watching the volatility like a hawk... and there have been some nervous moments on the days when there are 5% price swings.

We have also seen some of the early enthusiasm come out of the silver stocks with share prices selling off over multiple days.

We think the market is now in a bit of a stand-off moment waiting for the silver price to decide which direction it wants to head in next.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are still bullish on silver and think AVM’s assets will get re-rated if silver starts running again.

AVM has three silver assets in Mexico, which combined have an estimated ~100M silver ounces in foreign resources:

(Source)

(Source)

Across the three projects, AVM has committed to exploration programs over the nextenxt 12 months with a target of resource estimate upgrades to 200M ounces silver equivalent.

Here is a brief overview of the three assets and what we want to see next from AVM on them:

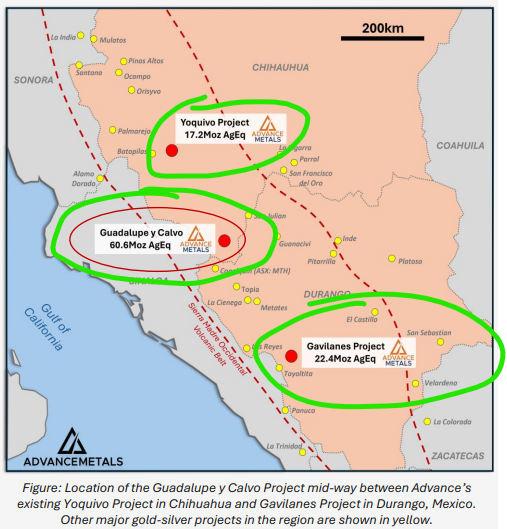

Project #1 Guadalupe y Calvo (60.6M oz silver equivalent foreign resource estimate)

This is AVM’s biggest and most advanced Mexican sasset.

AVM acquired the asset from ~A$3.6BN Endeavour Silver in July for a total consideration of $4M to be paid over 4 years. (Source)

The project has an existing foreign resource estimate of 60.6M ounces silver equivalent (816 Koz gold equivalent).

The project has mining history dating back to 1835 - with over 2Moz of gold and 31Moz of silver produced on the asset historically.

The project has also had 86,000m of drilling to define the 60.6M ounce silver equivalent foreign resource estimate the project has right now.

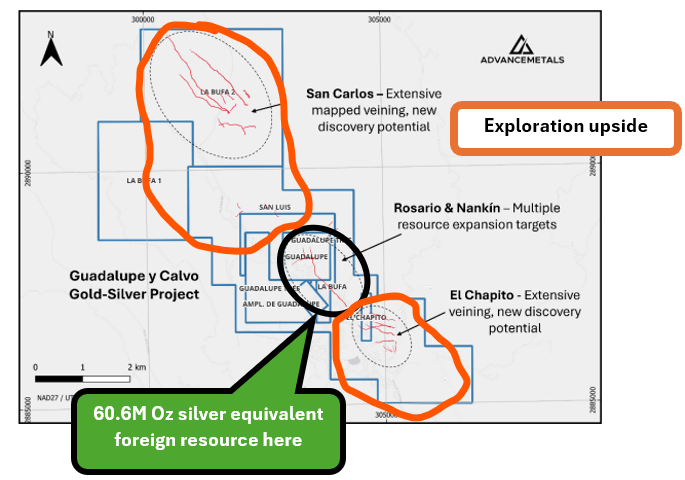

AVM’s strategy is to convert the current foreign resource into a JORC resource estimate.

And we think that the resource can get a lot bigger with some drilling:

What we want to see next:

Now that AVM has locked away a $13M capital raise the company is looking to start its first drill program on the asset. (Source)

Project #2 Yoquivo (17.2M Oz silver equivalent foreign resource estimate)

This project has thinner vein systems compared to GyC - but is a lot higher grade...

The project’s foreign resource estimate is 17.2M oz silver equivalent based on an average grade of 570g/t.

The foreign resource is based on ~70 diamond holes across three drill programs between 2020 and 2022, where previous drilling hit intercepts such as 0.4m at 21,447g/t silver and 0.3m at 7,480g/t silver...

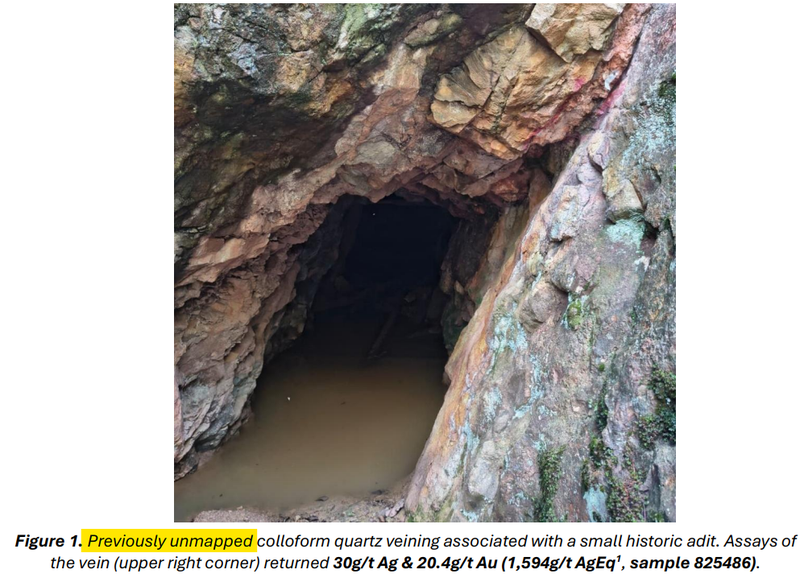

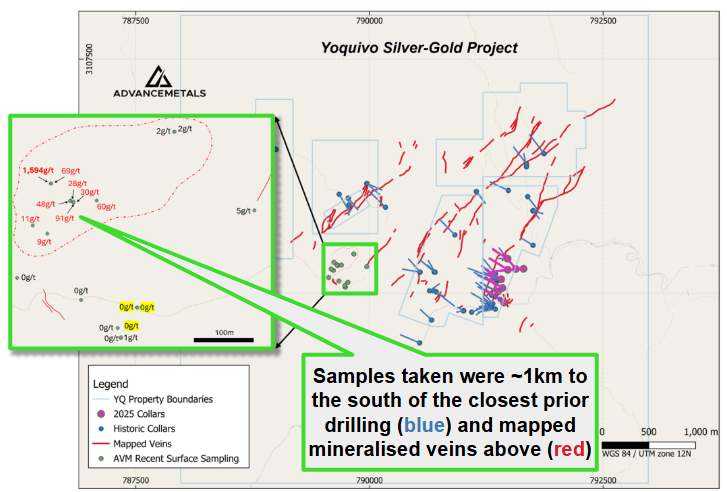

AVM recently did some sampling on the project and in one part of the project sampled rock chips with grades as high as 1,594g/t silver equivalent.

The rock chips came from a part of the project that had never been drilled before.

In fact, that part of the project hadn’t even been mapped before (despite the old underground workings that were found):

(Source)

So AVM found potential extensions to its project, in a part of the project that no one had really touched before...

And the rock chips (as well as the underground historic workings) are indicative of something being there that was worthy of the old timers mining the area out...

Here is where that newly mapped area sits relative to the known mineralised veins (in red) on the project:

(Source)

AVM is currently working on converting that to JORC status.

We think that an eventual JORC resource on this project could surprise to the upside, especially with the recent news from the assets over the last few weeks.

What we want to see next:

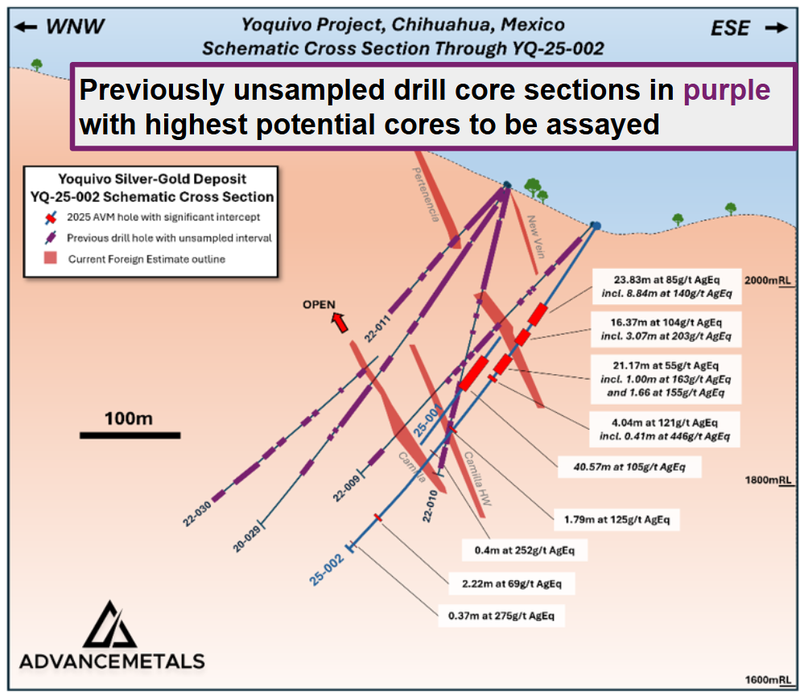

AVM has recently re-assayed ~3,500m of previously unsampled core with assays due in “late October” - which could mean assays are due any day now.

Here are the current drilled out veins and all of the areas that were left unsampled (in purple), we are hoping to see those red veins get bigger once the results come back in October:

(Source)

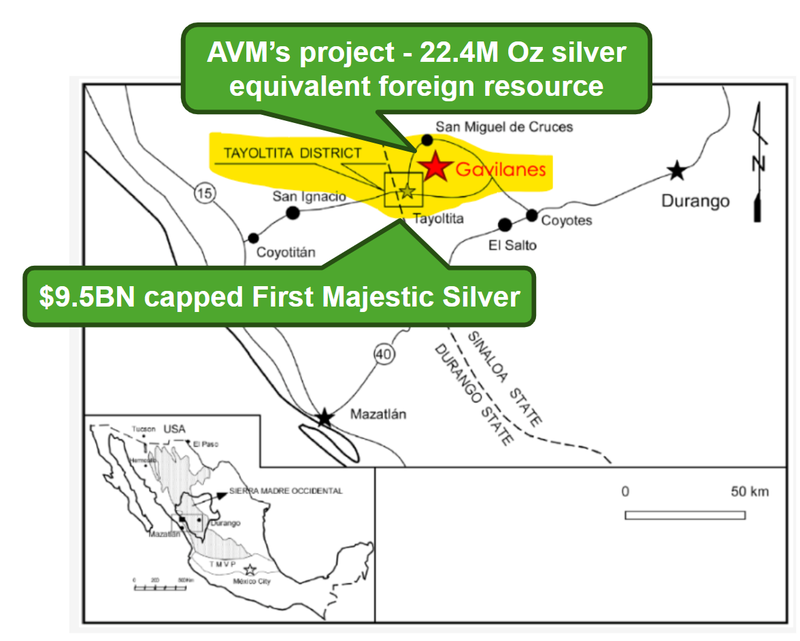

Project #3 Gavilanes (22.4M Oz silver equivalent foreign resource estimate)

This is AVM’s earliest stage project in Mexico.

The project has a foreign resource estimate of 22.4M oz of silver equivalent at an average 246g/t silver equivalent grade.

To date, drilling has only tested ~0.2km^2 of the project area while the ~15km^2 of KNOWN veins are undrilled.

The kicker for this project is its proximity to an existing mine owned by ~A$9.5BN First Majestic Silver.

Right now, the project as it sits might not be big enough to become a standalone development asset BUT even if the resource stays where it is today, it could make for good feedstock to a much larger company's operations.

First Majestic’s San Dimas Tayoltita mine (134Moz of silver) sits ~23km northeast of this project.

This project is one of those that you just never know how big it might be, until AVM drills it out.

(Source)

Ultimately we think progress on AVM’s silver assets are central to AVM achieving our Big Bet which is as follows:

Our AVM Big Bet:

“We want to see AVM reach a $150M+ market cap by converting its existing foreign resources into 100M+ silver equivalent ounces at the JORC level AND by making new discoveries”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AVM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What are the risks?

In the short term we think the key risk for AVM is “exploration risk”.

AVM is drilling its Victorian gold project right now and it’s possible that drilling doesn’t find economic mineralisation.

Poor drill results could mean AVM’s share price re-rates lower from current levels.

Especially after today’s announcement with the visible gold intercepts which might start to build in market expectations for high grade intercepts.

Exploration risk

There is no guarantee that AVM’s upcoming drill programs are successful. AVM may fail to find economic silver resources in which case we would expect the share price to re-rate lower.

Source: “What could go wrong” - AVM Investment Memo 19 September 2025.

Other risks

Investing in AVM carries other risks which may affect the value of the company.

There is also market liquidity risk. AVM is a small cap company, and its shares may be thinly traded.

This can lead to significant share price volatility or difficulties for investors seeking to buy or sell shares at their desired price.

Broader macroeconomic and commodity price factors could also impact the company’s prospects.

A fall in silver or gold prices, a global economic slowdown, or deteriorating investor sentiment toward the resources sector may negatively affect AVM’s valuation.

Political and jurisdictional risks must also be considered.

Although Mexico and Australia are established mining jurisdictions, changes in mining laws, royalty rates, or community sentiment could delay project development or increase operating costs.

Funding and dilution risk is another factor. As a pre-revenue company, AVM relies on external capital to progress its projects.

If market conditions turn unfavourable, the company may need to raise funds at a discount, resulting in shareholder dilution.

Finally, there is exploration and execution risk. Converting foreign resource estimates to JORC status, identifying new drill targets, and delivering positive drilling results are all critical steps.

There is no guarantee AVM will achieve these milestones on time, within budget, or with the success required to drive a material re-rating in its share price.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our AVM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our AVM Investment Memo where you will find:

- What does AVM do?

- The macro theme for AVM

- Our AVM Big Bet

- What we want to see AVM achieve

- Why we are Invested in AVM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.