AVM: Announces 33 million ounces silver equivalent JORC resource (116 million ounces if you include the non-JORC foreign resource)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,120,002 AVM Shares and the company’s staff own 119,905 AVM Shares at the time of publishing this article. The Company has been engaged by AVM to share our commentary on the progress of our Investment in AVM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Is this morning the start of silver’s next run up?

It’s up nearly 5% in the last hour.

Silver is one of our highest conviction themes for the next couple of years.

And after spiking to touch US$121 per ounce in January, silver has been trying to find a base over the last 3 months, bouncing between the ~US$70 and US$90 range.

(ahead of what we hope will be its next leg up above its January highs)

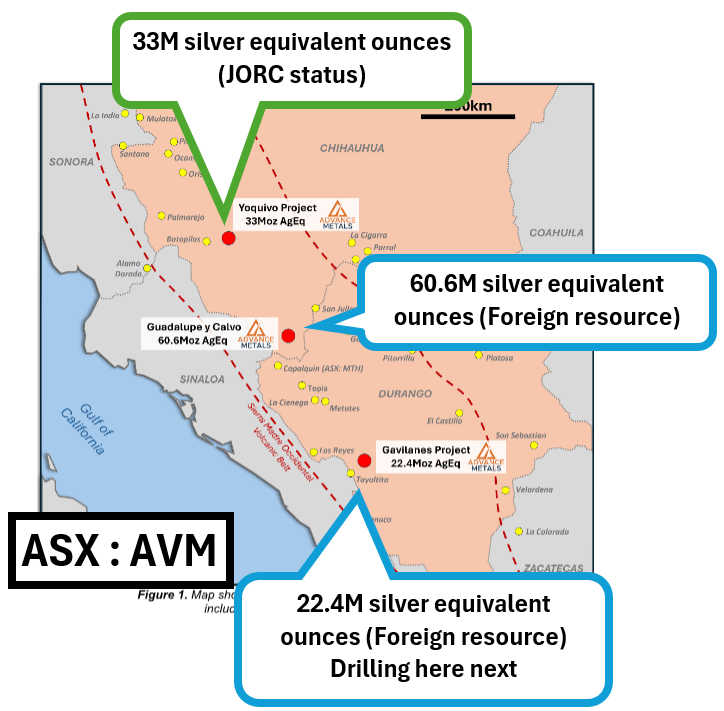

With this morning's near 5% bounce it’s a great time for our silver Investment Advance Metals (ASX:AVM) to have announced a 33Moz silver equivalent JORC Mineral Resource at just one of its Mexican projects.

Adding this to AVM’s non-JORC foreign resources on its other two nearby projects, that's a total of 116Moz silver equivalent across its Mexico projects.

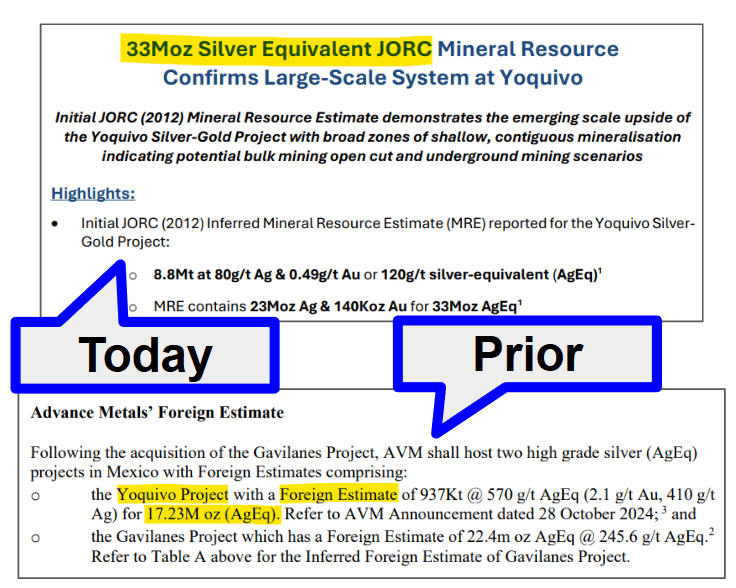

This 33Moz resource was converted from a foreign resource to the stricter JORC reporting standard used by the ASX.

And it actually almost doubled in size, instead of the generally accepted market assumption that converting to the stricter JORC standard will REDUCE a resource size (more on this in a second).

Next we want to see AVM convert more of these foreign resources to JORC classification plus deliver more drilling to expand its total silver resource estimate even further.

(And of course for the silver price to go on another face melting run... even though no one can predict what will happen next and there’s no guarantee it will in fact go on a face melting run. It could go on a run and no faces are melted, or not go on a run at all)

Another key takeaway from today’s announcement was that the resource at this project could potentially be “open-pittable” - the cheaper, easier, faster way to mine.

The commentary from AVM’s management for the “open-pit” topic should be interesting in the webinar being run tomorrow - 9th April 2026 at 11:00am AEST / 9:00am AWST

(more on why we like an open-pit mine later in today’s note)

AVM now has three projects with ~83M silver equivalent ounces in foreign resources and NOW ~33M silver equivalent in JORC resources.

(source)

Stepping back from the recent pull back in the silver price, we think most ASX silver companies (like AVM) are actually in a pretty strong position.

Silver is still way above the three previous all time highs of around US$50/oz. Silver stocks in our Portfolio are relatively cashed up, having raised money late last year when silver was running.

And now, those companies can advance their projects, while the silver price thrashes around, putting in a new base.

(we are hoping a new base from which to start running again).

AVM raised $13M in October 2025 at 10c per share - at the time it was done at a premium to its share price.

We put money into this raise at 10c, AVM shares last traded at 8.2c per share.

When the silver price was running in January, AVM hit 18c.

(past performance is not an indicator future performance)

That October raise included some heavy hitting institutional funds - like Jupiter Asset Management, Tribeca Investment Partners, Lowell Resources Fund, and APAC Resources (and we participated too).

AVM’s share price is currently trading below the capital raise price at 8.2c per share - capped at $39M and still had $11M cash in the bank at Dec 31.

Point is - AVM has had plenty of money to “do stuff” on its silver project while the silver price has been busy finding a new base.

We Invested in AVM because we saw the potential for value uplift on its Mexican silver projects as AVM goes about drilling and defining large silver resources...

And timing these announcements into a running silver price.

And today, AVM’s three projects have a combined resource base of ~116M ounces silver equivalent (foreign and JORC status).

(We also really like AVM’s gold asset in Victoria - more on that in a second)

Today, AVM announced a maiden JORC resource on one of its three Mexican projects.

Why is this a big deal?

A JORC resource is put together according to the standard the ASX requires when reporting how much metal a company estimates is in the ground from what is show in in its drill holes.

A foreign resource is an estimate done under a different country's reporting standards - the ASX allows companies to report them, but the market tends to put more weight behind a JORC number.

Usually, the ASX applies a discount to any non-JORC resource, expecting the resources to get smaller as they are drilled out/defined.

So before today, the market would have been expecting the resource at AVM’s project to get smaller BUT more “real” under the stricter JORC standard.

A foreign resource getting smaller under JORC standard is pretty common and a general expectation in the market.

BUT...

AVM has almost doubled the foreign resource on one of its projects to now sit at 33M silver equivalent JORC standard ounces:

(and the market likes positive surprises against commonly held assumptions)

Which makes us think - just how much silver JORC silver resources AVM could define across its other projects currently measured using foreign resource standards.

AND some more drilling.

(Today’s resource at Yoquivo is based on 99 diamond holes over just ~26,000m of drilling)

With some more drilling across all three projects - how much bigger can AVM’s resource base get?

We think after today’s announcement, the market could start to value AVM a lot differently - potentially removing that foreign resource discount AND maybe even start to price in growth in that overall resource number across the three projects.

And while the silver price tries to find a base, AVM can use the consolidation phase in the silver price (as well as that cash raised last year) to de-risk its projects and grow its resources even more.

It’s AVM’s version of deleting all your social media through winter and then rolling back around just before summer with a six pack (in AVM’s case, JORC resources)...

AVM is:

- Considering more drilling on Yoquivo (where the JORC resource was announced today)

- A drill program to start on its Gavilanes project (imagine if that 22.4M ounces doubles there too)

- And eventually, drilling at its most advanced asset Guadalupe y Calvo (imagine if that 60M ounces doubles...)

No guarantees AVM can replicate what it’s done at Yoquivo, there is always a risk the foreign resource estimates don't carry over into JORC status, OR that the resource numbers get smaller too.

We remain bullish silver - the industrial demand story (solar panels, EVs, AI chip packaging, defence electronics) hasn't gone away.

And sometimes it's hard to understand why the market is so downbeat with silver still trading above any all time high it hit in any previous gold bull run.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The current sentiment makes us think that IF silver finds a base around these levels and starts running to US$200/oz plus like we think (hope) it might, then the silver stocks will really start to run.

(no guarantees it will run to US$200/oz of course - this is pure speculation on our part)

We think that the market feels like it doesn't want to believe the silver move is real just yet - but if we get another big leg up, all of that questioning could turn into FOMO...

Our favourite silver analyst Michael Oliver thinks silver’s going to US$300-500 THIS YEAR.

Hopefully he is right...

Of course no guarantee that he will be.

Michael called the run to US$100+ - so we are giving him the benefit of the doubt (and letting him provide us with that sweet, sweet confirmation bias).

(but again - it might not happen)

Check out his latest call here: SILVER Headed to $300 - $500 THIS YEAR and 'It Will STAY There': Michael Oliver

Another thing that’s different this time is that the market has had a bit of a “war” sell off with everything happening between the US and Iran.

So silver stocks have had a double whammy of selling (war-induced and silver price pullback induced).

Which is why we think anyone who has needed a reason to sell has probably already done so.

(Meaning there might not be very many sellers if sentiment turns - and far less paper to go around, because most silver stocks raised capital last year).

Those exact same dynamics played out during that post-COVID period.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The positive for AVM from all of this is that IF sentiment for silver stocks turns - AVM could be in a position where its projects can be compared to peers on a like for like basis without the question marks over the classification of its resource estimates.

(especially now that AVM’s shown it can double those foreign resources, when converting them into JORC compliance).

Here's how AVM compares to its peers now:

- Canadian Vizsla Silver - EV of ~$1.5BN trading at ~$4.20 EV/ounce

- ASX listed Andean Silver - EV of ~$363M, trading at ~$3.20 EV/ounce.

And Advance Metals capped at $39M with ~33M JORC silver equivalent ounces and 83M silver equivalent ounces as foreign resource estimate.

Using even just the JORC component alone, AVM trades at ~$1.18 EV/ounce (a lot lower than its peers).

When we combine the foreign resource and the JORC resources - the EV/ounce metric is ~$0.30.

Now, that AVM’s shown those foreign resources convert to JORC status (and can grow), we are hoping that EV/ounce metric starts closing the gap to its peers.

(One obvious thing to note is that AVM is a lot earlier stage than its peers, so the current discount in valuation could also be attributed to the stage AVM is at).

Why we like AVM’s three Mexican silver projects

Here is a quick overview of why we like each asset.

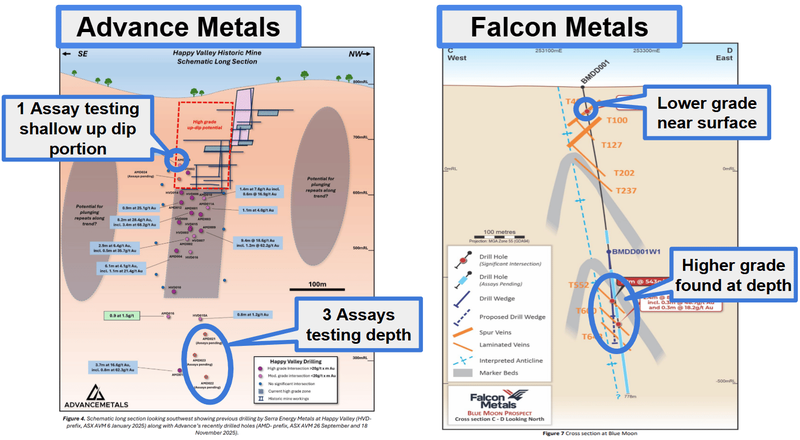

Project #1 Yoquivo (33M ounce silver equivalent JORC resource)

This is the project that today’s announcement relates to.

This project until today, was more of a thin vein system - basically where grades are much higher but the system is made up of small veiny structures.

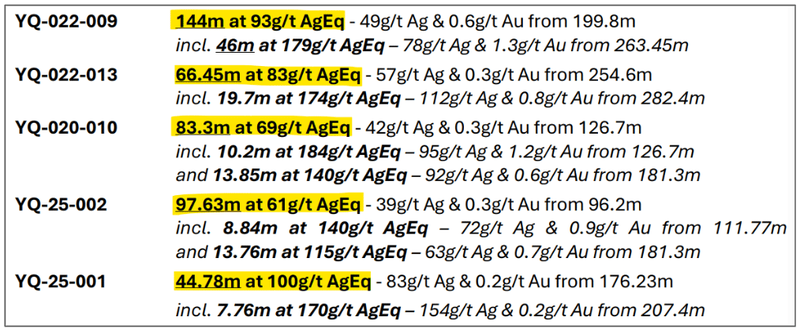

One hole from AVM’s recent drilling actually hit 0.4m at 21,447g/t silver which is outrageous.

(source)

The project now has a JORC resource estimate of ~33M Ounces silver equivalent based on an average grade of 120g/t silver equivalent.

With the recent resampling program and the last round of drilling AVM’s returned results with broad intercepts - 60m+, which could build a case for an open-pit development scenario on the project.

(source)

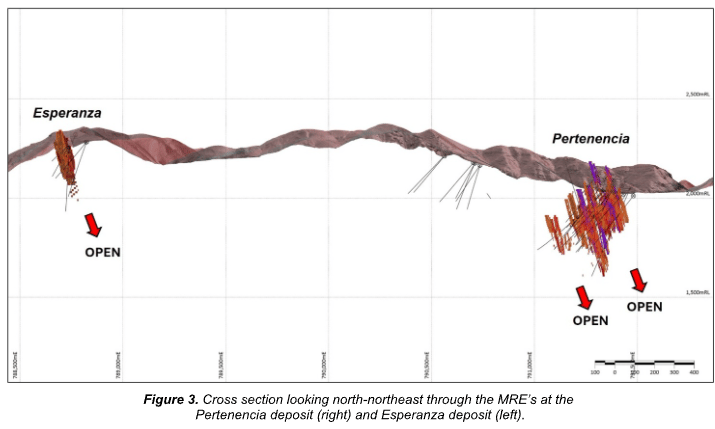

Here is how that looks in a cross section:

(source)

Usually with deposits like this a company would go in and develop underground adits to get to the high grade thin veins holding all the silver.

What that cross section shows is that instead, the resource is starting to look structured in a way where putting together a big open-pit may also be an option:

(source)

We like that, with drilling, AVM’s given itself optionality and now we want to see whether or not with some drilling that open-pit theory improves.

(Open-pits, on higher grade systems can often lead to lower operational costs and simplified mining).

Next, we want to see what AVM can come up with on potential open-pit development scenarios.

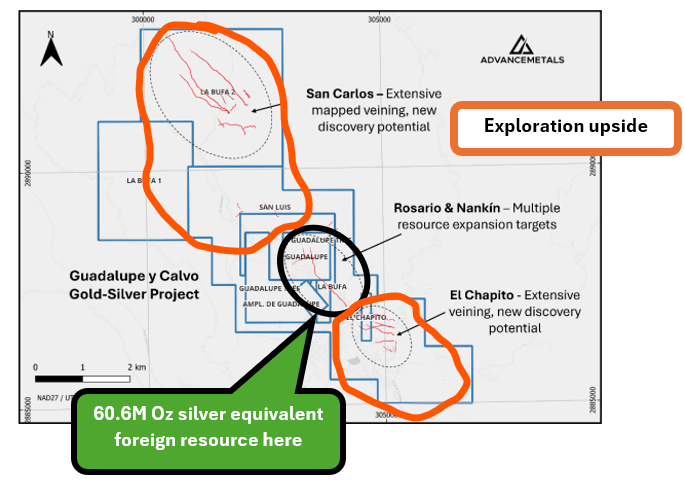

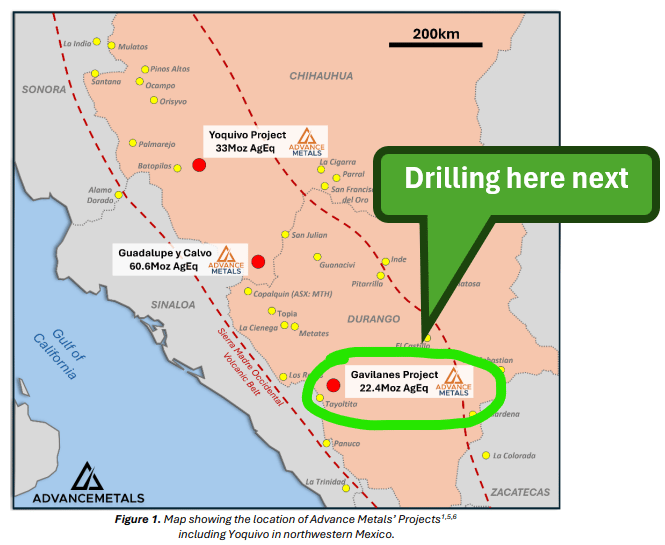

Project #2 Guadalupe y Calvo (60.6M oz silver equivalent foreign resource estimate)

This is AVM’s biggest and most advanced asset.

AVM acquired the asset from then $2BN (now $4BN) Endeavour Silver in July for a total consideration of $4M to be paid over 4 years. (source)

The project has an existing foreign resource estimate of 60.6M ounces silver equivalent (816 Koz gold equivalent).

The project has mining history dating back to 1835 - with over 2Moz of gold and 31Moz of silver produced on the asset historically.

The project has also had 86,000m of drilling to define the 60.6M ounce silver equivalent foreign resource estimate the project has right now.

AVM’s strategy is to convert the current foreign resource into a JORC resource estimate.

And we think that the resource can get a lot bigger with some drilling:

A good comparison for this asset on the ASX is Andean Silver’s Cerro Bayo project in Argentina.

That asset is bigger, higher grade and more advanced than AVM’s, but we think it's a good benchmark for where AVM can take this project with some additional strategic drilling...

Andean’s resource estimate sits at ~90.7M ounces silver equivalent with an average silver equivalent grade of 342g

(source)

Andean is currently capped at ~$399M.

AVM is capped at just $39M...

AND this is just one of AVM’s three silver projects...

What is AVM doing on this asset right now?

Back in October AVM released the planning for work programs across the 3 projects, aiming to double the combined resources across the 3 projects. (source)

Maiden drilling at GyC was a part of this planning and IF AVM can do what it did with Yoquivo today it would change the size/scale of AVM’s Mexican silver project portfolio.

Here are the milestones we are tracking on this project over the coming months:

- 🔄 Drilling permitting

- 🔲 Drilling starts

- 🔲 Assay results

- 🔲 Maiden JORC resource

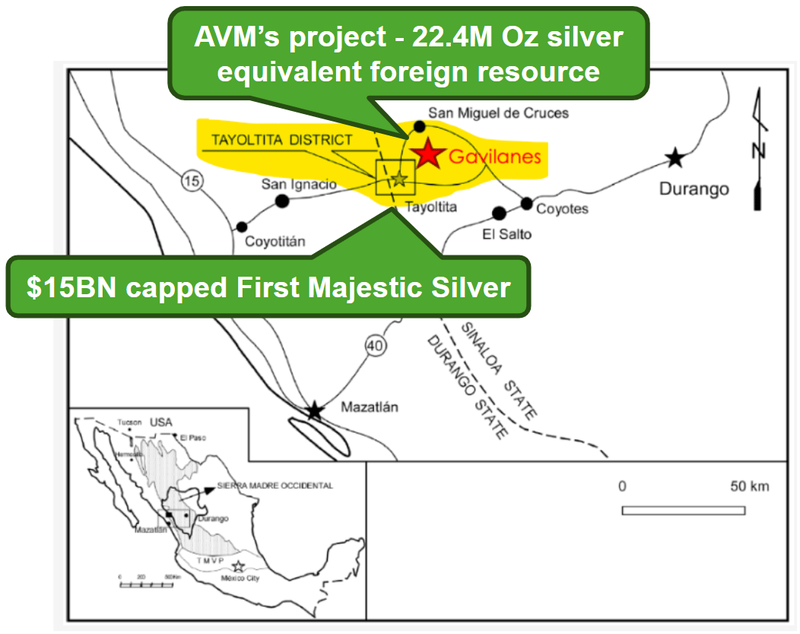

Project #3 Gavilanes (22.4M Oz silver equivalent foreign resource estimate)

This is AVM’s earliest stage project.

The project has a foreign resource estimate of 22.4M oz of silver equivalent at an average 246g/t silver equivalent grade.

This project has had by far the least amount of drilling done on it...

Which means there is a lot that can go right on this with some more drilling... i.e, there’s a fair bit of upside here that is harder to predict.

To date, drilling has only tested ~0.2km^2 of the project area while the ~15km^2 of KNOWN veins are undrilled.

The kicker for this project is its proximity to an existing mine owned by $15BN First Majestic Silver.

Right now, the project as it sits might not be big enough to become a standalone development asset BUT even if the resource stays where it is today, it could make for good feedstock to a much larger company's operations.

First Majestic’s San Dimas Tayoltita mine (134Moz of silver) sits ~23km northeast of this project.

(source)

This project is one of those that you just never know how big it might be, until AVM drills it out.

What we do know is that the bigger the project gets, the more likely it becomes that a major like First Majestic starts to take notice.

AVM has a drilling program planned on this project and in today’s announcement said AVM would “follow an identical pathway to an upgraded JORC resource including sampling

of historic core” on the project.

So basically we see the Yoquivo playbook rolled out on Gavilanes.

(Which we hope translates to a similar outcome (doubling of the foreign resource estimate).

(source)

Here are the milestones we are following for Gavilanes:

- 🔲 Sampling program on historic drillcore

- 🔲 Target generation work ahead of drilling

- 🔲 Maiden drilling program

- 🔲 Maiden JORC resource (hopefully upgrading the 22.4M ounce silver equivalent resource)

What’s happening in Mexico right now - why we like the region

A big part of the reason we Invested in AVM was because we think the ASX doesn't really understand Mexican silver assets YET.

All of the big Mexican producers are listed in Canada, where all of the big M&A deals are happening so the Canadians are more willing to bid up the value of the Mexican silver stocks.

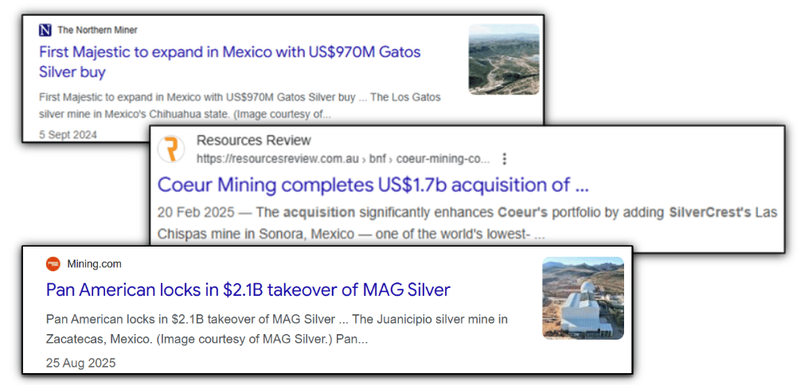

We have already seen:

- Coeur Mining buying Silvercrest in a deal worth US$1.7BN, $28BN

- buy Gatos Silver for US$970M, and; $15BN First Majestic move and

- took over MAG Silver for US$2.1 billion. Most recently, $34BN Pan American Silver

Three deals. US$4.77BN spent on Mexican silver assets with all of those deals finalised in the last 15 months.

Our bet was that eventually the ASX would see what’s happening in North America and translate those peer comps into the valuations of ASX listed Mexican silver companies...

So far that hasn’t really happened, especially after the Viszla Silver incident in Mexico earlier this year (our thoughts are with the workers and families involved in that incident.) (source)

Understandably, the perceived risk for Mexican silver companies went up briefly on the ASX (and in North America).

But that whole time, AVM (and our other Mexican silver Investment Mithril Silver and Gold) have been drilling uninterrupted.

So those incidents may have been isolated to Vizsla.

We were also on site in Mexico - close to AVM’s Guadalupe y Calvo asset, and never really felt unsafe at any point in time:

(check out our site visit here)

Oh, and Mexico is still the #1 silver producer in the world...

So we think Mexico is still the place to be for silver juniors... and clearly from all the M&A the producers are willing to do in country, they also see it as the place to be (and commit billions of dollars of capital for deals on).

We think that when/IF the silver price starts running again, Mexican companies will run the hardest...

It’s not just us who think that.

Here is a video we have shared before of fund manager Adrian Day of Adrian Day Asset Management from a video published about twelve months ago:

"The opportunity for a company to go in and start acquiring some good Mexican assets - producing or non-producing - and acquire them relatively cheaply, is probably very compelling. Someone's going to do that sooner or later."

That part starts at 6:00 into the video - and now... those “cheap” assets Adrian talks about are even cheaper...

(source)

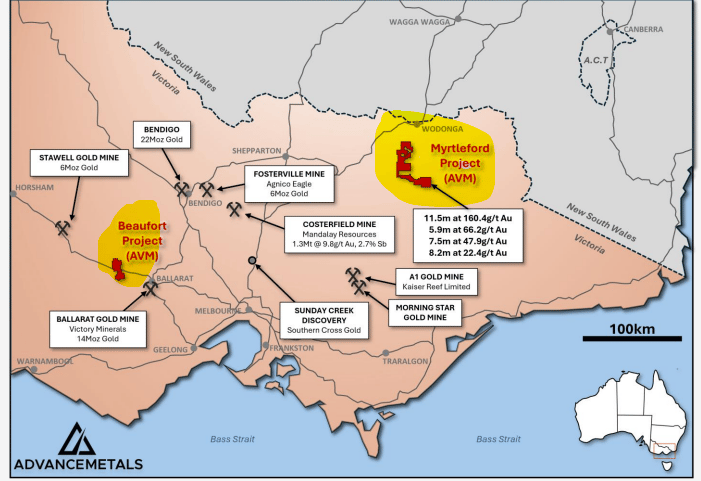

We also like AVM’s Victorian gold exploration asset

We think AVM’s current valuation more than justifies AVM’s current $39M market cap, especially at its current market cap.

Here’s where the two projects sit on the map:

(source)

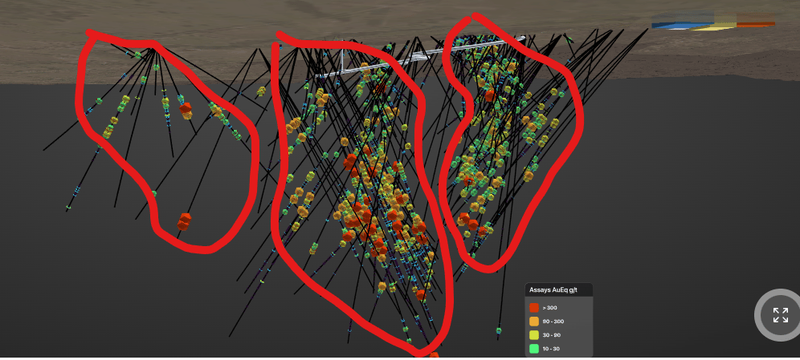

The asset AVM is drilling right now is Myrtleford which sits across a ~13km gold trend with scattered historic workings on the project.

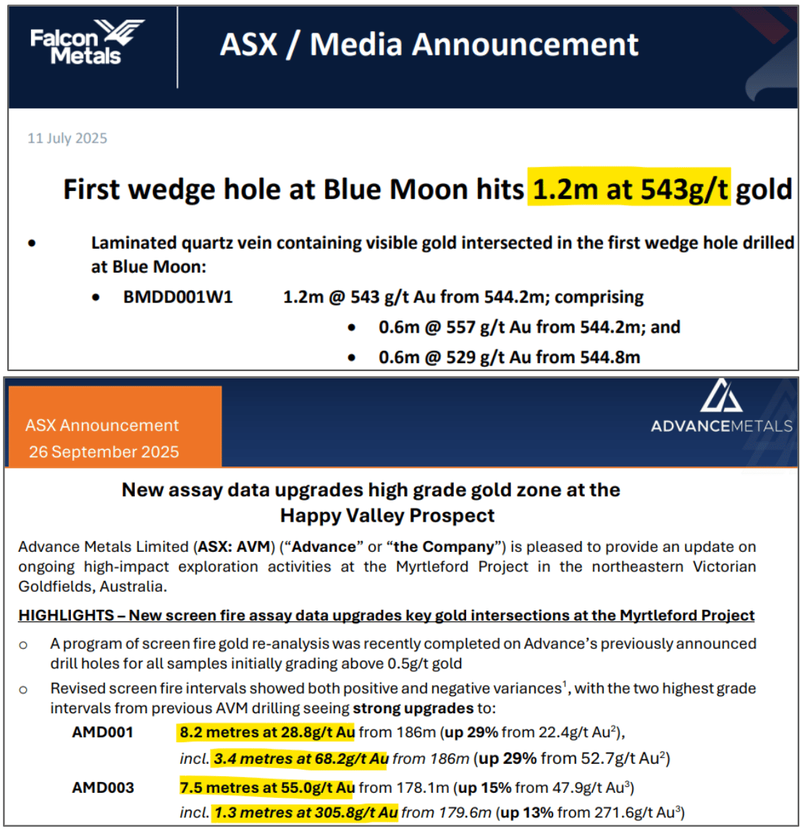

In our last note, we wrote about how, IF AVM can make new discoveries on step-out targets, the market could start to draw comparisons between it and ~$2.1BN Southern Cross Gold and ~$97M Falcon Metals, both operating in the Victorian Goldfields.

Falcon is similar to AVM because the company discovered a thin, but very high grade gold structure and quickly re-rated:

Falcon re-rated by 310% in the 7 trading days following the initial hit (going as high as ~640% within 2 months) off some similar intercepts to the ones AVM’s been hitting over the past few months too:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And here are those initial hits by both FAL and AVM:

As for the Southern Cross example - it's because Southern Cross managed to define multiple repeat high grade structures over a broader area.

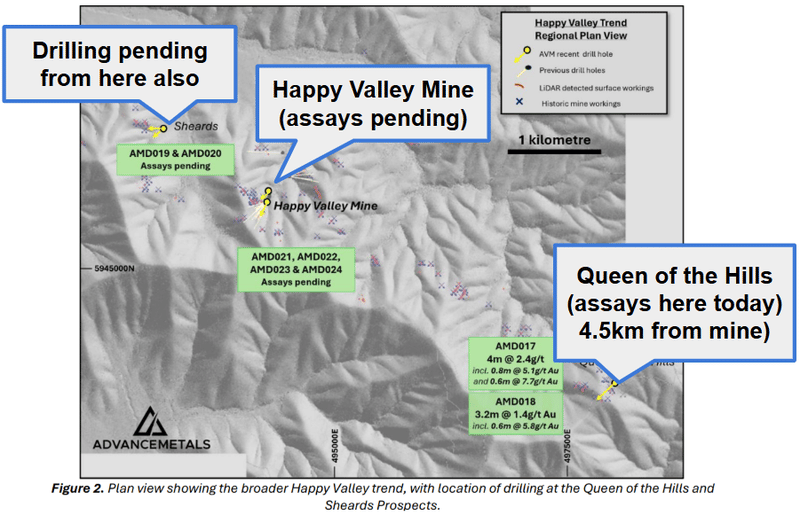

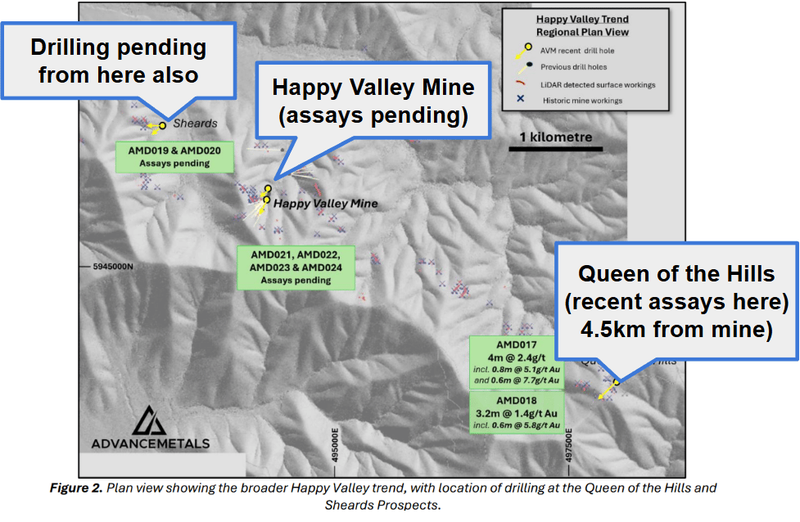

Basically, like AVM finding multiple high grade structures (like Happy Valley) scattered across its project area.

(source)

As mentioned earlier, AVM’s project sits across a ~13km gold trend with scattered historic workings on the project.

All we really need is for AVM to hit a repeat Happy Valley style structure across that trend and the Southern Cross Gold comparisons could be on.

We note AVM did manage to hit some gold in an intercept ~4.3km away from Happy Valley, but at this stage we can’t claim it as a discovery...

(We need to see it get drilled out further and that gold be shown as part of a bigger system not just an isolated hit).

(source)

There are no guarantees here that AVM can make its Victorian gold asset like any of the two companies mentioned above but so far the exploration hits have been relatively strong.

We also note AVM is currently drilling on the project...

So we could see assays from the project at arbitrary times - IF the drilling keeps delivering we think the asset could start to build a case for backstopping a large chunk of AVM’s current $39M market cap.

(source)

Ultimately though, we are primarily Invested in AVM to see it drill out and define a large resource base across its silver assets in Mexico - which brings us to our Big Bet as follows:

Our AVM Big Bet:

“We want to see AVM reach a $150M+ market cap by converting its existing foreign resources into 100M+ silver equivalent ounces at the JORC level AND by making new discoveries”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AVM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's next for AVM?

AVM’s three silver projects in Mexico

Across the three silver assets, AVM expects to be drilling its Gavilanes asset next.

Here are the milestones we are tracking across the three projects:

Yoquivo:

- 🔲 Resource growth drilling at Yoquivo

- 🔲 Open-pit potential assessment

Guadalupe y Calvo (GyC)

- 🔲 Maiden drilling program, subject to permits and approvals.

- 🔲 Maiden JORC resource converting the 60.6M oz silver equivalent foreign estimate.

Gavilanes

- 🔲 Sampling program on historic drillcore

- 🔲 Target generation work ahead of drilling

- 🔲 Maiden drilling program

- 🔲 Maiden JORC resource (hopefully upgrading the 22.4M ounce silver equivalent resource)

(source)

Victorian gold (Australia)

At AVM’s gold project in Victoria, we want to see more assay results from all of the drilling AVM’s done over the last few months.

What could go wrong?

In the short term we think the key risk for AVM is “exploration risk”.

AVM is drilling its Victorian gold project right now plus has further exploration activities planned at its silver projects so it’s possible that drilling doesn’t find economic mineralisation.

Poor drill results could mean AVM’s share price re-rates lower from current levels.

Exploration risk

There is no guarantee that AVM’s upcoming drill programs are successful. AVM may fail to find economic gold or silver resources at its projects in which case we would expect the share price to re-rate lower.

Source: “What could go wrong” - AVM Investment Memo 19 September 2025.

Other Risks

Like any small-cap exploration company, AVM carries significant risk, here we aim to identify a few more risks.

A major specific risk for AVM is geopolitical and security risk in Mexico. An article earlier notes the recent safety incidents involving other silver explorers (like Vizsla Silver) in the region. Operating in areas with potential cartel activity and varying levels of local security requires intense logistics and risk management. Any safety incident involving AVM personnel could halt operations immediately and severely impact the company's share price.

Additionally, Mexico has recently seen shifts in its political landscape regarding mining laws and open-pit permitting. Any unfavorable regulatory changes could delay AVM's project development or increase its compliance costs.

AVM also faces resource conversion risk. While the Yoquivo project successfully converted to a JORC estimate, the Guadalupe y Calvo and Gavilanes projects still rely on historical, foreign estimates. It is possible that modern drilling fails to replicate the historical data, resulting in JORC resources that are much smaller or lower grade than the headline foreign estimates suggest.

Operating across two vastly different jurisdictions - Mexico for silver and Victoria, Australia for gold may also stretch management bandwidth. Advancing multiple exploration fronts simultaneously requires immense capital. While AVM is currently well-funded with ~$11M, aggressive drilling campaigns across two continents will burn cash quickly.

If the company does not make a significant discovery or convert its resources efficiently, it will likely need to tap equity markets again in the future, resulting in shareholder dilution.

Finally, AVM’s valuation is heavily leveraged to the price of silver. If the anticipated macro rally fails to materialise, or if industrial demand for silver slows down, the market appetite for junior silver explorers could dry up rapidly.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our AVM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our AVM Investment Memo where you will find:

- What does AVM do?

- The macro theme for AVM

- Our AVM Big Bet

- What we want to see AVM achieve

- Why we are Invested in AVM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.