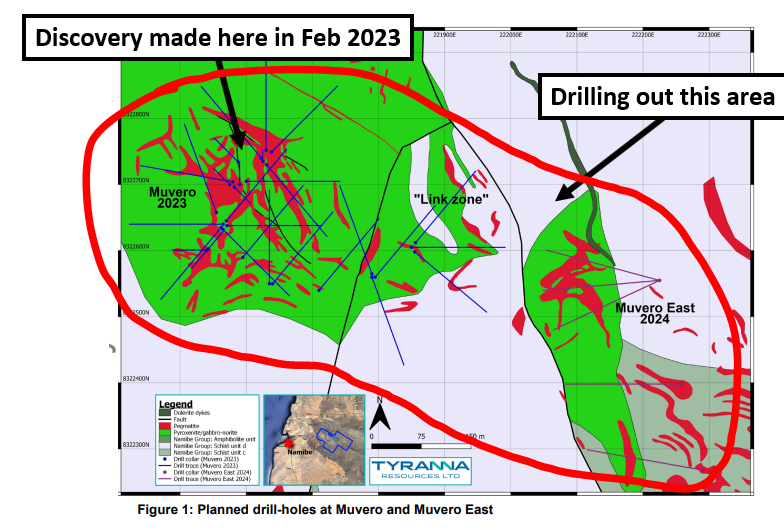

Are these two zones connected? TYX is going to find out by drilling the potential “Link Zone”…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 23,420,000 TYX shares and 10,000,000 options at the time of publishing this article. The Company has been engaged by TYX to share our commentary on the progress of our Investment in TYX over time.

21 more assays in and another 11 to come before the end of June.

And a new set of drilling to test if two separate mineralised zones are actually one giant mineralised zone...

Our lithium Investment Tyranna Resources (ASX:TYX) has been drilling non stop at its discovery in Angola.

To date TYX has drilled less than 2% of the pegmatites sitting inside its ~200km^2 project area.

From that small part of the project TYX has already declared one discovery.

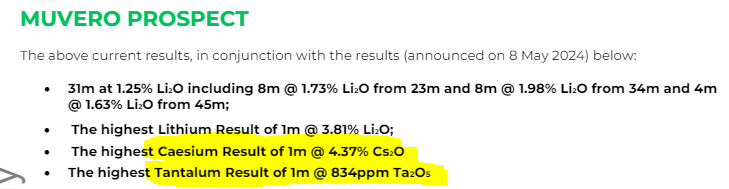

In February, 2022 TYX made its discovery at its Muvero prospect, hitting over 20m of lithium at ~2%.

The discovery managed to attract a multi-billion dollar Chinese conglomerate to the project.

TYX ended up signing a deal with Sinomine worth up to ~A$31M together with a binding offtake agreement.

Sinomine provided TYX with an upfront payment of ~$14.5M in cash which has been funding the company for almost a year now.

TYX now trades at a market cap of ~$32M with ~$9M cash in the bank (as of 31 March 2024).

Post the funding deal, TYX got a big chunk of cash to go and drill out its discovery.

Since October last year TYX has drilled ~50 holes in and around its Muvero discovery.

After today’s announcement, we have assay results from 39 out of the 50 holes.

The remaining 11 assays are all expected before the end of June.

(Back in March some delays from issues with assaying caused the TYX share price to come off a bit, these have now been fixed and all the assays are starting to be announced)

Our take on the results are as follows:

- Some of the holes exceeded our expectations - the 31m intercept from hole 22 was above our expectations, especially with the peak grades up to 1.98% in that hole.

- Some holes underwhelmed - some holes hit thin intercepts which didn't really extend the discovery. What those holes did was give us a better understanding of how the pegmatites are trending underground.

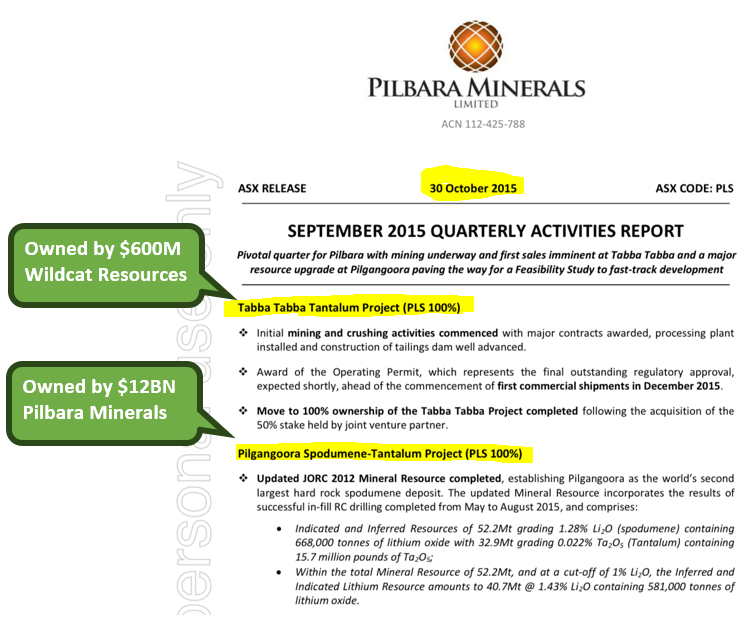

- The big surprise so far has been the high caesium and tantalum grades - TYX is primarily chasing lithium but has been putting out some strong tantalum/caesium grades. What’s interesting here is that some of the big lithium mines (like Pilbara Minerals Pilgangoora in WA) were previously tantalum mines (more on this later).

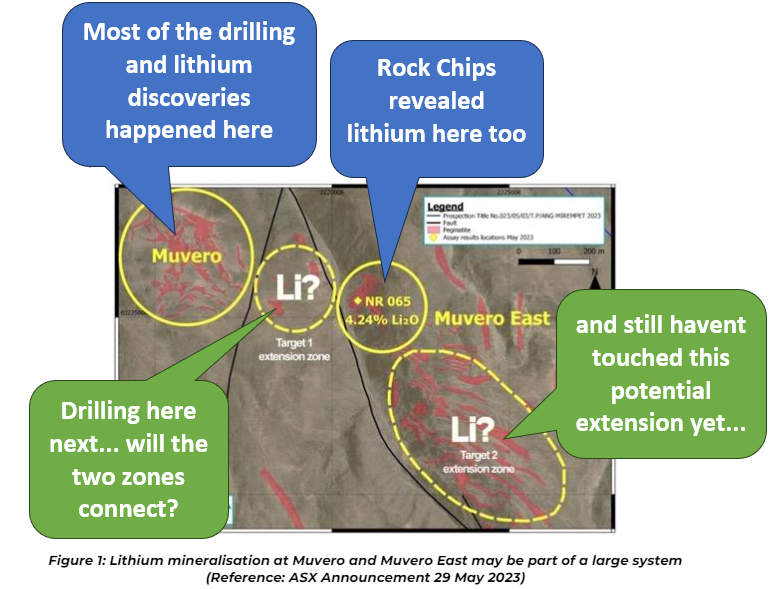

All of TYX’s drilling so far has been on its existing Muvero discovery...

TYX hasn't touched the sections between its discovery and Muvero East.

That’s where we think TYX could extend its discovery east to west.

Looking at the map above the pegmatites (shown in pink) look to be starting at Muvero and trending to the east.

The interesting bits in the middle is what TYX is calling the “Link” zone.

(get it? because it potentially links the two pegmatite bodies together into one giant body if they deliver some hits in that zone)

So far there hasn't been any drilling in the “link zone” part of the project.

AND it's where we want to see TYX drill and hopefully show that its discovery is a lot bigger than the market is pricing in right now.

TYX confirmed in today's announcement that the next round of drilling would be on “regional targets” and would start after some more field work was done.

When drilling starts up again, we are hoping it is to drill out that “link”.

Ultimately, we think that for TYX to achieve our “Big Bet” it needs to declare additional discoveries and prove to the market that its discovery is a lot bigger than the drilling results are showing so far.

Our TYX Big Bet is as follows:

Our TYX Big Bet:

“TYX discovers and defines a large, simple to process lithium resource, that is on par with world class multi-billion dollar ASX peers such as Pilbara Minerals, Core Exploration, and Liontown Resources, AVZ Minerals and Sayona Mining”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our TYX Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

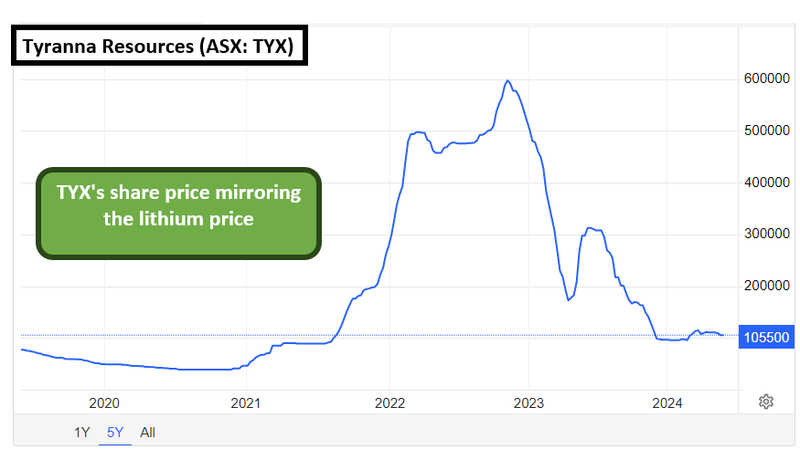

Why we think the TYX share price has been sold down

Over the last ~18 months TYX’s share price has off down a fair bit.

We think there are two key reasons for this

- Because of drilling/assay delays

- Because the macro sentiment for lithium was taking a breather.

Exploration drilling is hard.

Especially in remote locations.

Sometimes timelines can be pushed out and delays occur for things outside of the company’s control - which is what we think happened to TYX.

And the market penalises the stock for it until it can be sorted out.

TYX started drilling in October 2023 while investors were still showing more interest in lithium stocks.

First assays were expected in early January of this year (again, a period when market sentiment for lithium stocks wasn't that bad yet).

Unfortunately for TYX inconsistencies with the assay results meant the first 17 holes had to be re-sampled and be re-tested by labs in Australia.

TYX announced those delays in March.

(The assays were already late.. now they were delayed even further)

The first batch of assays didn’t come to market until May...

By then, almost every single lithium stock had been sold, and the market had fallen out of love with the macro thematic for the time being.

Lithium prices were ~90% off their highs, and TYX’s share price had gone from 1.6c when drilling started to ~0.9c when the first assays were announced.

TYX announcements against the Lithium Price chart:

Since then, lithium sentiment is back off the canvas, some interest has come back into lithium stocks, TYX has sorted out its assay issues and the results from the drilling campaign are being announced.

Since the assays have come out TYX’s share price has actually rebounded slightly from its recent lows:

Overall we think it was a combination of delays and market sentiment that impacted TYX’s share price.

The positive we can take away is that TYX has spent the last ~9 months improving its assay processes to avoid delays in the upcoming drill campaigns to test the “link zone”

(this is going to be a very interesting one to watch)

TYX now has a “drilling camp” fully operational which we hope speeds up future drill programs.

With some of the operational issues now fixed, we think that this could be a turning point for the company as it delivers faster newsflow and lithium drilling results that exploration investors live for.

Tantalum/Caesium and why it matters

Part of the exploration process is about learning what else your project may have.

For TYX, this is Tantalum and Caesium.

Most people may not know this, but a few of the big lithium mines currently in operation started out as tantalum/caesium mines.

Think ~$12BN Pilbara Minerals and ~$600M Wildcat Resources...

Both their main assets were once tantalum projects:

Then, when the lithium market became hot, these companies started to make a fortune on the “lithium” part of the mine.

The Tantalum/Caesium sales didn’t go away, these companies are still able to process and sell that ore - these are considered “credits” rather than a main source of revenue.

So far the Tantalum and Caesium TYX is hitting has been a surprise to us.

As long as the lithium keeps on coming in, as this is the name of the game for TYX, the tantalum and caesium by-products could add to stronger project economics when it comes time to run feasibility studies.

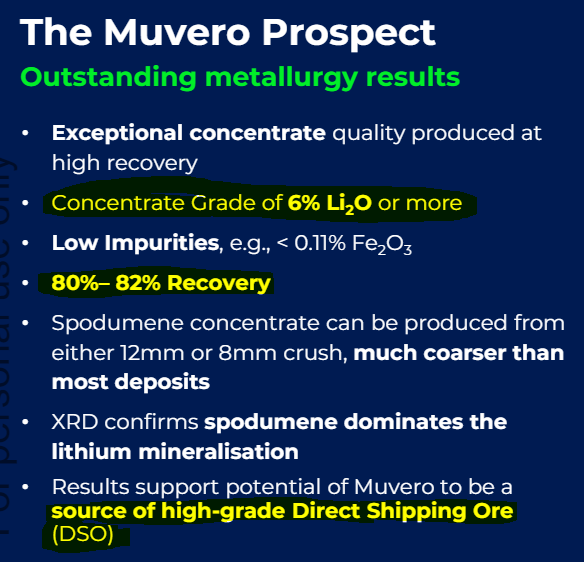

We also note that TYX’s metallurgy looks relatively good, which is usually an important input into economic studies. TYX is showing recoveries in the 80%’s, concentrate grades above 6%, and the potential to produce DSO lithium material...

(Source)

Catalysts we will be looking out for over the coming months:

Drilling the between Muvero and Muvero East (the “link zone”) 🔄

Once the drill program starts we will be watching for the following:

- During drilling - We want to see visual spodumene in the drill cores. Spodumene is generally the host rock for high grade lithium, visual spodumene will be a positive first indication of potential economic lithium mineralisation.

- After drilling - This will be all about waiting for the assay result — we’ll be looking for lithium grades above a level that is considered typically economic.

Assays for the next 11 holes 🔄

TYX has published assays now for 39 out of the 50 holes drilled with 11 more assays to come.

Given that TYX is undertaking extensional drilling of an existing discovery, we want to see TYX at least improve on its recent batch of assay results (and fingers crossed, beat them).

As a result, our expectations are as follows:

- Bull case (exceptional result) = Lithium grades >1.5% over 10m+ intervals.

- Base case (good result) = Lithium grades 1-1.5% over 5-10m intervals.

- Bear case (poor result) = Lithium grades <1% over <5m intervals.

Maiden Resource Estimate 🔲

Ultimately, we want to see TYX take all of the drilling results and feed it into a maiden resource estimate for its discovery.

If the drilling eventuated into a maiden resource number, we think that would mark a successful drilling program.

TYX expects to start resource modeling in the second half of this year after its next round of drilling.

What are the risks?

Exploration Risk

Most of TYX's drilling to date has been at its existing Muvero discovery.

The next phase of drilling will be much riskier as TYX looks for extensions between Muvero and Muvero East.

If the company isn't able to prove a link/mineralisation at Muvero East then the market may react negatively.

There is always a chance TYX finds nothing, as a result, the key risk in the medium term is “exploration risk”.

Sinomine Deal Risk

As mentioned earlier in today’s email, last year TYX signed a deal worth up to $31M with Sinomine.

That deal was split across two phases:

Phase 1 (Completed 17 July 2023 for $14.5M):

- Sinomine invests $4.5M in TYX at 2.5c per share.

- Sinomine invests $10M in exchange for a 10% stake in TYX’s Angolan lithium project.

Phase 2 (Sinomine option to exercise for $16.75M):

- Sinomine can invest $6.75M in TYX at a minimum of 3.75c per share OR a 25% discount to the 5-day volume-weighted average price of the TYX share (whichever is higher).

- Sinomine can invest another $10M in exchange for a further 10% stake in TYX’s Angolan lithium project.

The second phase can be exercised at any time within 24 months of phase 1 being completed which means Sinomine has until ~17 July 2025).

If exercised, Sinomine would have to pay at least 3.75c per TYX share, which is much higher than TYX’s current market price. Sinomine might try to renegotiate the deal terms or just not exercise the option.

There is still over a year to go for TYX to use its $9M cash to deliver some big drill hits, and the lithium sentiment to continue turning to help re-rate the TYX share price back up - which is what we want to see.

You can find all of the risk for TYX in our TYX Investment Memo.

Our TYX Investment Memo

In our TYX Investment Memo, you can find the following:

- What TYX does

- The macro theme for TYX

- Our TYX Big Bet

- What we want to see TYX achieve

- Why we are Invested in TYX

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.