$31M FYI’s HPA Peer Pushes Past $1BN Market Cap

Published 21-JUL-2023 11:00 A.M.

|

14 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,097,000 FYI shares at the time of publishing this article. The Company has been engaged by FYI to share our commentary on the progress of our Investment in FYI over time.

Over the last few years we have seen immense growth in capital flows into companies that mine critical raw materials.

By one estimate, critical raw materials mining now has the same market size as iron ore.

What doesn't get as much focus however, is the processing of critical raw materials - which promises to be just as valuable as countries race to shore up supply.

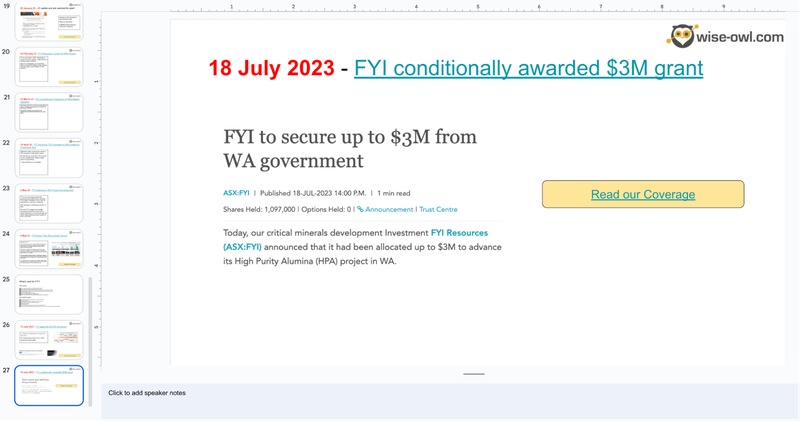

This week, our late stage mineral processing investment FYI Resources (ASX: FYI), received a conditional $3M government grant to support its High Purity Alumina project in WA.

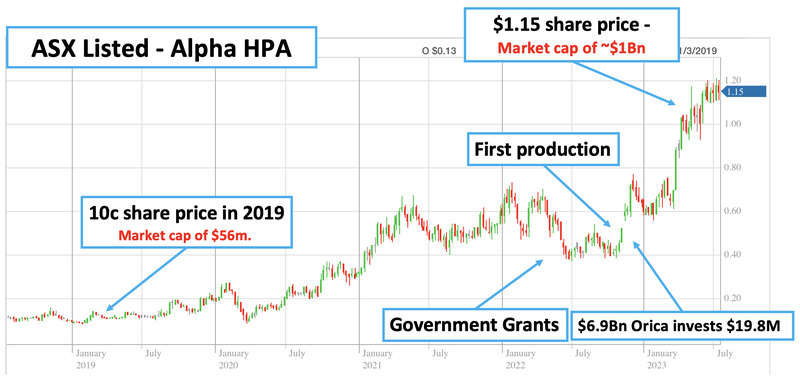

Ultimately, FYI is looking to follow the success of the ASX listed Alpha HPA, which has a High Purity Alumina project in QLD.

FYI is at an earlier stage to Alpha HPA, and is capped at $31M. Alpha HPA went from a market cap of ~$56M to now trade at $1BN and is now producing from its project.

Alpha pulled in circa $40M of government grants in recent years... more on the Alpha HPA story below.

FYI’s $3M government grant news follows Australia's recent publication of its Critical Minerals Strategy, which has a big focus on bringing home mineral processing projects.

According to the Opportunities for Australia chapter of the strategy:

Building downstream refining and processing capability and securing a greater share of trade and investment could generate $139.7 billion in GDP in Australia.

We don’t normally get too excited about government white papers, but this one really caught our eye, as the key “winners” clearly were companies looking to process critical minerals in Australia...like FYI.

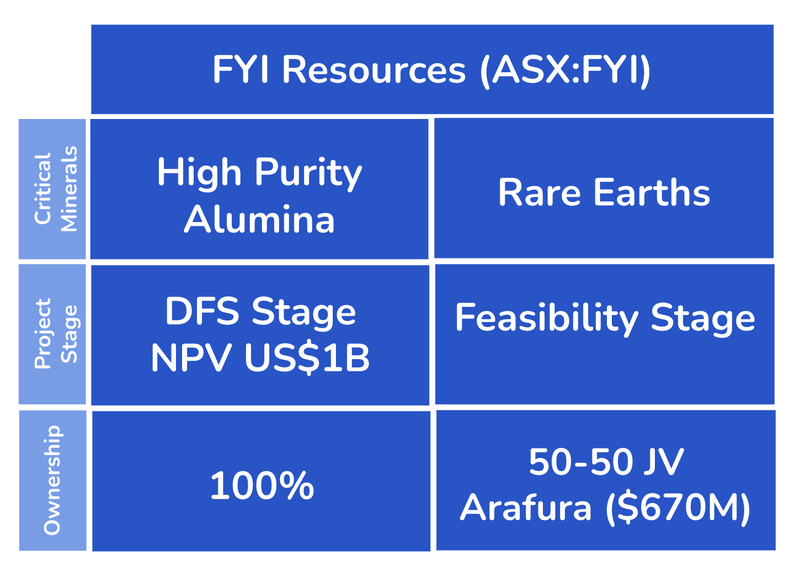

FYI is looking to develop two processing facilities across two critical raw materials:

- High Purity Alumina processing project in WA; and

- A rare earths processing project in the NT with the ~$670M Arafura Resources

Both rare earths and HPA are listed as critical raw materials on the US, EU and Australia’s critical raw materials lists.

FYI has managed to put itself in a position where, should Australia look to move further up the value chain (from mining into processing), it has the advanced projects that are ready to take advantage of this shift.

FYI’s HPA project

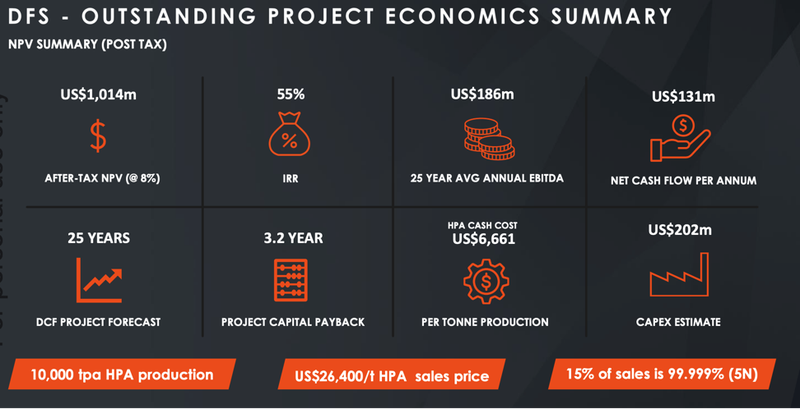

FYI has a DFS stage project for High Purity Alumina.

The project has an NPV (net present value) of US$1.1BN NPV off a CAPEX investment of US$202M.

FYI’s process has been proven at the pilot plant stage, with positive customer responses.

FYI is taking a staged approach to production, with an initial 1,000tpa “small scale plant” in the works. This plant will produce bulk samples for potential customers to test and qualify.

FYI is planning on starting this plant up in the second half of 2024.

What success in HPA looks like on the ASX

Ultimately, FYI is looking to follow the success of the ASX listed Alpha HPA, which has a High Purity Alumina project in QLD.

FYI is at an earlier stage to Alpha HPA, and is capped at $31M.

Alpha HPA went from a market cap of ~$56M to now trade at $1BN and is now producing from its project.

Along the way, Alpha HPA managed to lock in a strategic investment from $6.9BN Orica and ~$40M in government grants.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

FYI’s rare earths project

Right now ~80% of the world's rare earths processing happens in China.

Rare earths have one of the most fragile supply chains for critical minerals in the world.

Even though Australia is a major producer globally, it has very limited processing capacity domestically.

Even Australia’s biggest rare earths producer, Lynas, sends its stuff off to Malaysia to be processed.

FYI is working towards a feasibility study for its rare earths processing project in early 2024 with $670M capped Arafura.

Why we like Australia for mineral processing

Most of the bottlenecks in supply chains across the critical minerals come at the processing stage.

Elon Musk even weighed in on the debate with his comments on lithium processing saying - “constraints were in the refining process” since refining was “much harder” than mining.

The same processing bottlenecks exist across most critical minerals supply chains.

China controls most of the world's critical minerals processing and manufacturing capacity - as we noted above, up to ~80% of the rare earth's space.

The rest of the world is quickly realising it needs to build out local processing hubs.

For context - the US and Australia recently signed a deal that would see the US consider all production out of Australia as “friendly supplies”.

Our view is that, eventually, Australia will become a key player in the critical minerals processing sector.

As we noted above, a few months ago, Australia released its updated “critical minerals” strategy.

The key takeaway is that although Australia mines a lot of the minerals needed for the global energy transition, a lot of the value captured in the processing of these minerals is lost to other countries like China.

The Australian critical minerals strategy going forward includes processing minerals. And we think FYI is well placed to take advantage.

Here are the key highlights from the critical minerals strategy:

- Further $500M in funding for NAIF (North Australia Infrastructure Fund) - this covers the region where FYI’s rare earths project is planned

- Support for downstream mineral processing

- Establish the National Reconstruction Fund, which includes $1BN for value-add in resources and $3BN for renewables and low emissions technologies.

- Track and monitor foreign investment in Australian critical minerals projects

- Grants available for exploration programs

According to the “Opportunities for Australia” chapter, “Building downstream refining and processing capability and securing a greater share of trade and investment could generate $139.7 billion in GDP”.

Back in March 2022, FYI’s JV partner on its rare earths project, Arafura Resources received a $30M grant from the Federal Government’s $1.3BN Modern Manufacturing Initiative (MMI) fund for its NT rare earths separation plant.

Earlier this week, FYI was awarded $3M from the WA Government’s Investment Attraction Fund (subject to final agreement on key terms).

Our view is that Australia has all of the ingredients needed for it to become a processing powerhouse for the global critical minerals supply chain.

But there are two other key factors that Australia needs to support a prosperous mineral processing industry:

- Access to cheap energy

- Attractive foreign investment

Australia has access to cheap energy (particularly on the west coast)

Processing facilities are highly energy intensive and need access to cheap energy to be cost competitive.

Western Australia and the Northern Territory specifically have some of the lowest natural gas prices across all of the developed countries around the world.

(Source)

Australia is a major exporter of gas at the moment - the 7th largest in the world.

Australia also has access to some of the world's most abundant renewable energy supply, from wind, and solar to green hydrogen.

The chief operating officer of European Utility E.ON, Patrick Lammers even commented on Australia’s strengths saying the country had the potential to be “the new Saudi Arabia” of green energy and minerals.

(Source)

Australia can attract foreign investment capital

Australia is known as a Tier 1 investment jurisdiction.

This means that it is favoured by foreign investment companies given the reliability of legal tenure and access to skilled labour.

Relative to the rest of the world, foreign investment capital sees Australia as a “safe” place to park money and (hopefully) watch it grow.

This means that projects requiring funding are able to access global capital markets more easily.

Think of this as having a bigger audience ready to commit to projects when it is “go time” and projects are ready to build.

Ultimately, we hope that when it comes time for large investments to happen in the Australian critical minerals processing space, FYI is in a position where it benefits from the wave of capital flowing into the sector.

We are hoping FYI is positioned as an industry leader and the preferred partner for HPA and rare earths processing.

This forms the basis for our FYI “Big Bet” which is as follows:

Our FYI Big Bet:

“We want to see FYI significantly re-rate by moving into High Purity Alumina (HPA) production and scaling its technology to other HPA projects”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our FYI Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor FYI’s progress since we first Invested and to track how the company is doing relative to our “Big Bet”, we maintain the following FYI “Progress Tracker”:

FYI Resources

ASX: FYI

More on FYI’s HPA project

FYI’s High Purity Alumina project is aiming to commercialise a new processing technology that is cleaner, purer, and much less expensive than conventional processing methods.

At a very high level, FYI’s project’s competitive advantage comes from the difference in its flowsheet.

A flowsheet is a technical name given to the steps involved in taking alumina and turning it into high purity alumina (HPA).

FYI has already completed a Definitive Feasibility Study (DFS) for a 10,000tpa processing facility which returned the following results:

- Net Present Value (NPV) = US$1BN

- Internal Rate of Return (IRR) = 55%

- Capital Expenditures (CAPEX) = US$202M

- Payback Period = 3.2 years.

The DFS was based on a cost of production of ~US$6,661 per tonne versus a sale price of US$26,400 per tonne of HPA.

FYI’s current strategy is to build a Small Scale Production plant, with a capacity of a 1/10th the scale of above.

The goal here is to take a staged approach to scaling up production. This strategy will see it start to produce bulk samples quicker (and with less upfront costs), for potential customers to test and quality before committing to larger purchases.

FYI is planning on starting this plant up in the second half of 2024.

What is HPA used for?

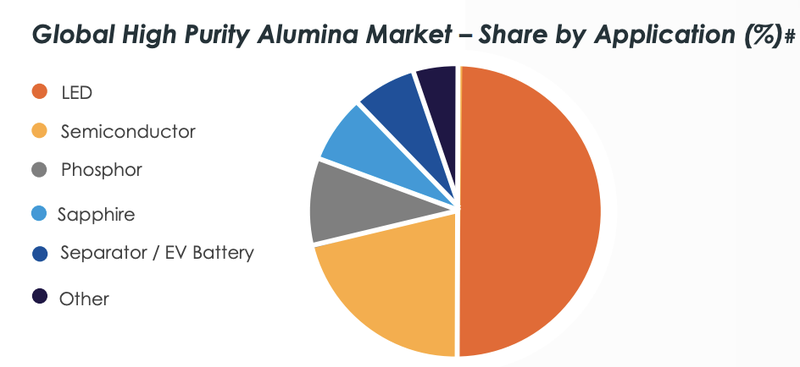

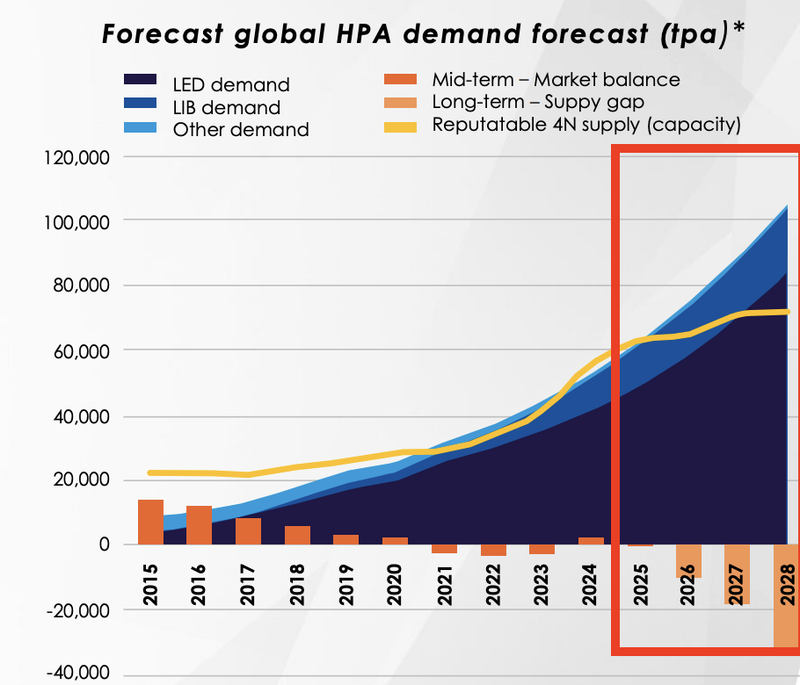

At the moment HPA is primarily used in the production of LED lights (~50%) and semiconductors (almost 25%).

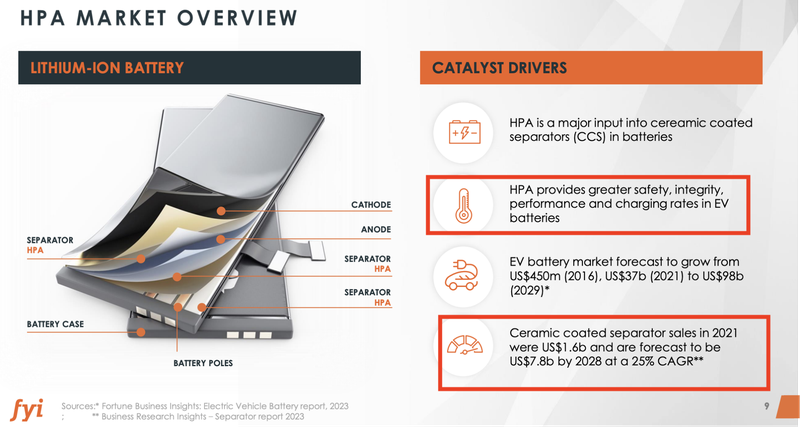

The big future demand driver though is in the battery space.

Batteries consist of three parts:

- Anode (this is where the lithium goes)

- Cathode (primarily graphite)

- Separator (this is where HPA is used)

HPA provides for a safe, higher utility separator that can cycle through high rates of battery usage increasing the performance and durability of a battery.

HPA demand is expected to outstrip supply from the year 2024 onwards, this gives plenty of time for FYI to bring its project up to a level where it is ready to start construction.

FYI is hoping to have its small scale production plant ready to build by May 2024 and hopefully in production at about the time when the market is expected to go into a supply/demand deficit.

What does success look like in the HPA space?

The success of ASX listed Alpha HPA gives an idea of what a successful project could look like.

Only ~ 4 years ago, Alpha HPA had a share price of ~10c per share and was looking to develop its own HPA technology.

Fast forward to today, the company has received ~$60M in federal funding and up to ~$22M in funding from the QLD government for its plant.

Alpha HPA attracted a strategic investment from ~$6.9BN Orica and has now put stage 1 of its project into production.

Alpha HPA’s project now produces with a capacity of ~400tpa and the company is capped at $1BN.

For context, once constructed FYI’s small scale production plant would have a capacity of ~1,000tpa, FYI is capped at just $28M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

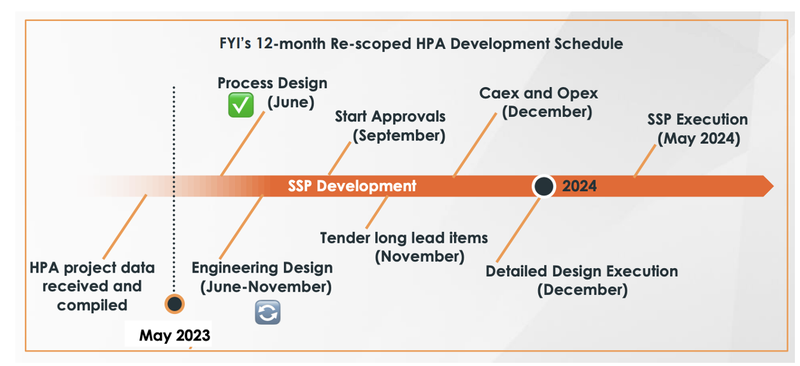

What is next for the HPA project

FYI is looking to develop its Small Scale Production plant by May 2024.

The company recently appointed CTE as its Engineering Services Provider and this week secured $3M government funding (subject to some conditions).

What’s next for FYI’s HPA project

✅ Select a preferred engineer for small scale production plant [Complete]

✅ Secure government grant funding [Complete]

🔲 Release CAPEX and OPEX figures for small scale production plant (December 2023)

🔲 Complete construction and commissioning of small scale production plant (May 2024)

🔲 Product qualification update

🔲 Enter into first MOU offtake agreement

🔲 Begin financing discussions for commercial plant

More on FYI’s rare earths project

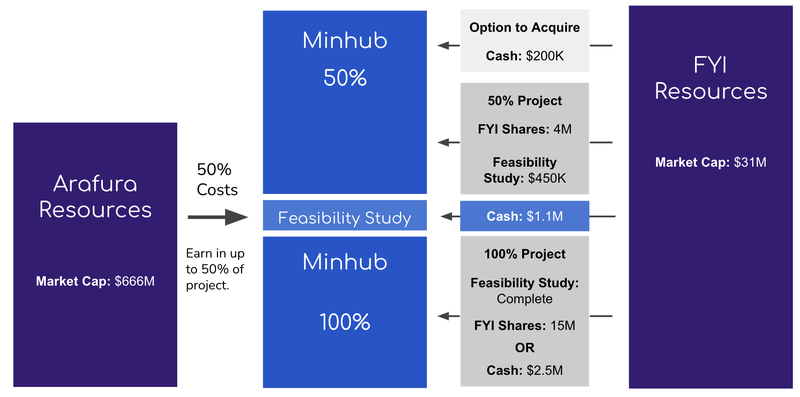

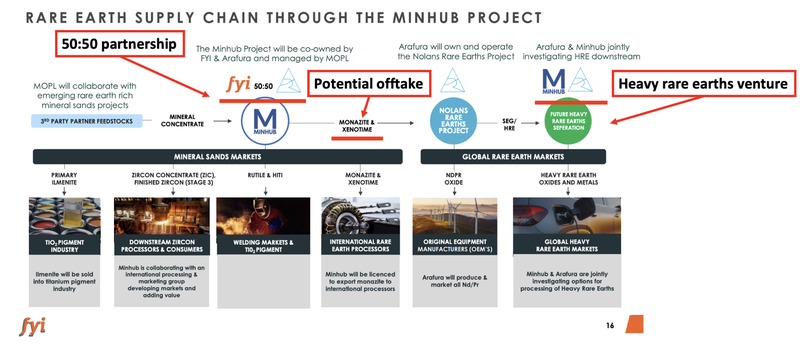

FYI is acquiring 100% of “Minhub” - a private company looking to develop a processing plant capable of processing products from heavy rare earth mineral sands projects.

As part of the deal, FYI is looking to bring on Arafura Resources as a 50% project partner.

Once the acquisition and the deal with Arafura is completed, FYI would own and operate 50% of the project Arafura own the remaining 50%.

The Arafura ownership is contingent on a binding agreement being signed between the two companies AFTER a feasibility study is completed.

The project will be looking to take rare earths heavy minerals sands feedstock (that was previously considered waste material) and process it into valuable heavy rare earth concentrates.

FYI will then look to sell some of that product into the open markets and some of it to Arafura who can process it further at the Nolan processing plant nearby.

At this stage, the project is at the “concept stage”, with technical work to commence leading into a Pre-Feasibility Study (PFS) expected to be delivered by early 2024.

In the background, the project will be looking to finalise agreements with existing and potential mineral sand producers for products that can be processed once the plant is up and running.

Details on the Arafura partnership

Arafura is currently building Australia’s only heavy rare earths separation plant, which it has already managed to lock away $30M of grant funding.

FYI’s project partner here clearly has experience in taking a processing venture from concept into development.

Arafura’s partnership with FYI will be via a co-operation agreement on a 50:50 basis through to a feasibility study being announced, the key points of the deal are as follows:

- Feasibility study - 50% funding from Arafura for a feasibility study. After the feasibility study Arafura can make a development decision and proceed with the project.

- Offtakes - Arafura has first rights of refusal on offtakes for two specific products (xenotime and monazite)

- Heavy rare earths demo plant - FYI and Arafura will also look at a potential partnership on a heavy rare earths downstream plant.

What’s next for FYI’s rare earths project

🔄 Technical work and offtake discussions with feedstock partners

🔄 Feasibility Study (due early 2024 - 50:50 funded by Arafura and FYI)

🔲 Binding agreements between FYI and Arafura (after the feasibility study)

🔲 Site identification and permitting in Darwin, NT

For a full list of milestones see our FYI Investment Memo

What are the risks?

In the short term, the key risks to FYI’s projects will be the technology scale up and delay risks.

FYI is looking to develop its HPA project into a small scale pilot production plant which may take longer than expected and have potential technical issues during the build out phase.

Longer term, funding risk is FYI’s biggest challenge.

Building and constructing processing plants can be expensive.

FYI will need to secure a pathway to funding for the HPA small scale plant, HPA large scale production facility and rare earths processing facility.

We have listed both risks in our FYI Investment Memo:

Our FYI Investment Memo:

Below is FYI Investment Memo, where you can find a short, high level summary of our reasons for Investing.

In our FYI Investment Memo, you’ll find:

- Key objectives for FYI for the coming year

- Why we are Invested in FYI

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.