$30M capped HAR - Gold drilling in the USA in weeks with permitted processing plant in place - and what’s with these African gold results?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,185,066 HAR Shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The gold price just broke out to new all time highs again...

The past performance is not and should not be taken as an indication of future performance.

And gold stocks are back in focus - especially in the USA where there is interest in mining and resources companies again.

We were at the Beaver Creek Precious Metals Summit in the US a few weeks ago and the overwhelming consensus was that big funds are now finally willing to put capital to work in small caps.

So it’s a very strong backdrop for the $30M capped Haranga Resources (ASX:HAR) to drill two gold projects all inside the next 6 weeks.

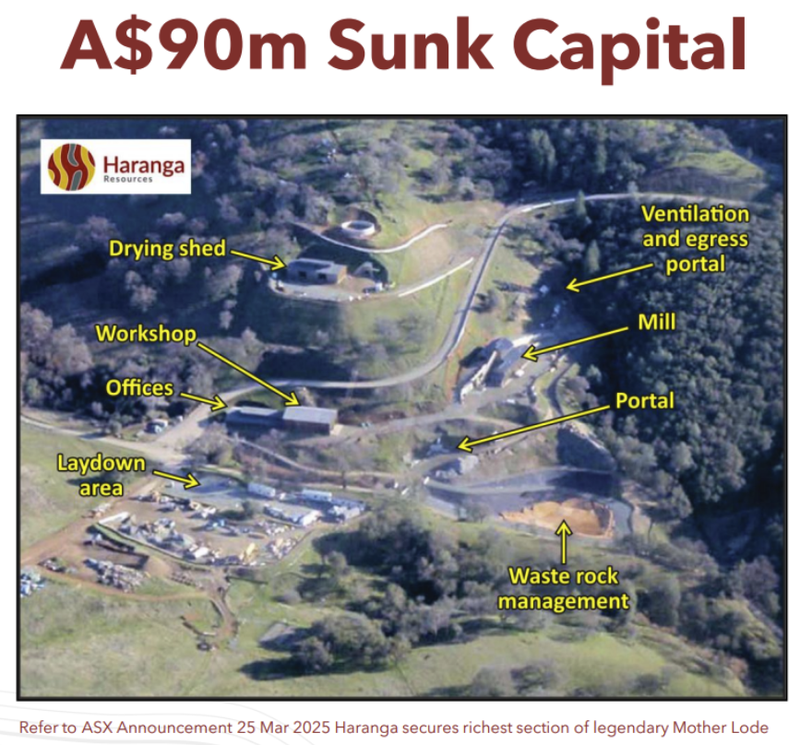

HAR owns a fully permitted gold project in California, USA, with over $90M in mine infrastructure built by the project’s previous owners.

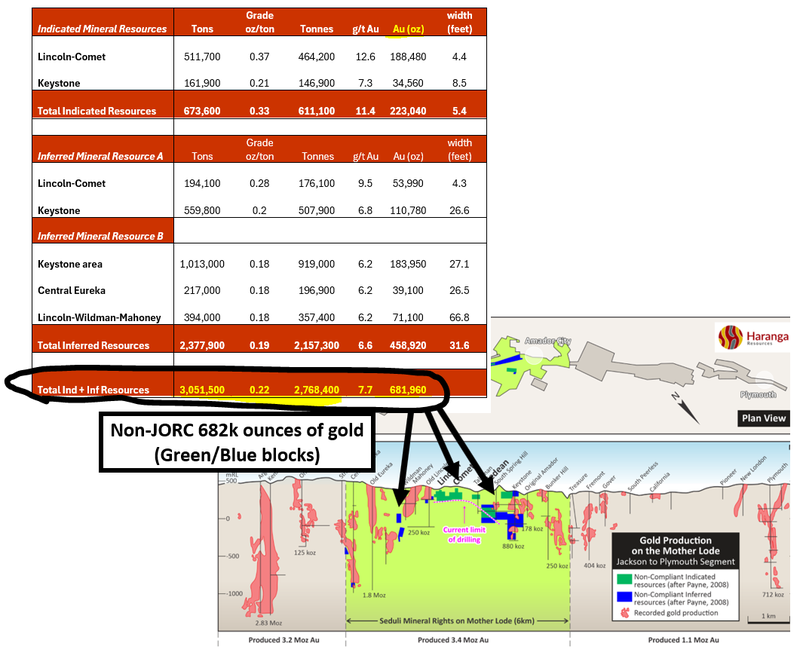

The project already has a Non-JORC 286,000 oz non-JORC gold resource at 9.28g/t.

... and data from 2008 showing it might be up to ~682,000 ounces, more on this below.

(HAR’s project also has a fully built and PERMITTED 350,000tpa gold processing plant)

HAR acquired its US gold project back in March, AND will be drilling it in the coming weeks with the gold price already up another US$800 per ounce...

The past performance is not and should not be taken as an indication of future performance.

HAR expects to be drilling in the US NEXT MONTH - and October starts next week.

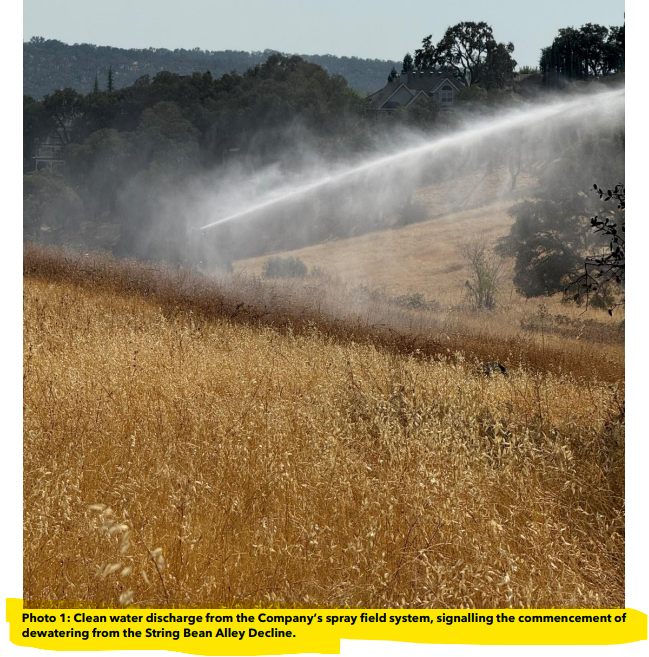

HAR will be drilling from inside its big underground decline (which is currently being de-watered) - here is a photo of us from the entrance to the decline a few months ago - see our full site HAR visit note here.

Drilling will be looking to convert that non-JORC resource estimate into a JORC compliant resource.

This is all why we are in HAR - mainly for its US asset...

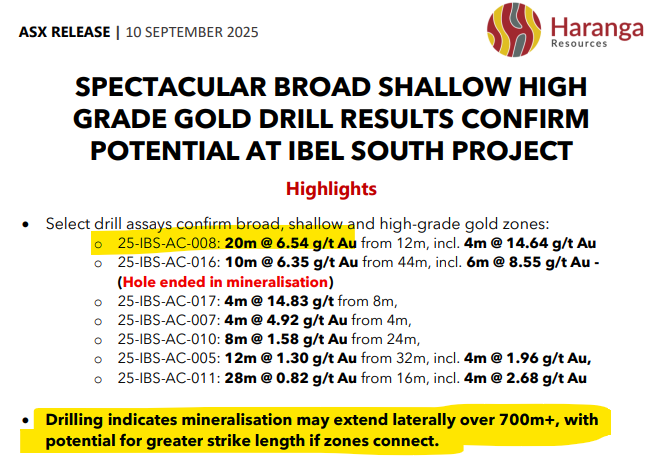

...but we have to admit the drill results from its gold asset in Senegal did catch our attention (and the market’s) a few weeks ago.

Over in Senegal, Africa, HAR still holds a non-core gold asset that it had already committed to do some shallow aircore drilling at before they acquired its USA gold project....

And oops...

... HAR hit a very impressive 20m with average gold grades of ~6.54g/t from only 12m depths in what could end up an unexpected high grade discovery...

(Source)

Nobody had any expectations from this drilling so the results are kind of like finding some cash in the pocket of a jacket you haven’t worn in a long time.

It also helps that the gold price has been marching to new all time highs most days this month.

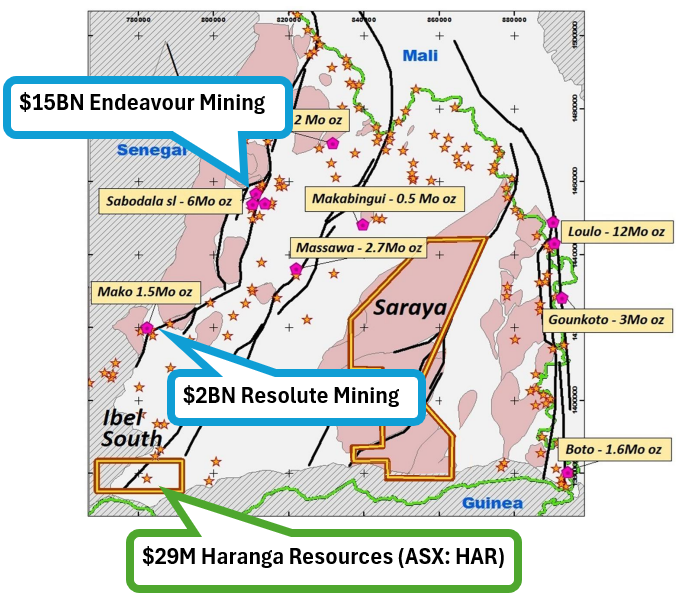

The drill results came from HAR’s project next to $15BN Endeavour Mining and $2BN Resolute Mining’s operating assets...

(The region has a few other gold discoveries too, so its not in the middle of nowhere either).

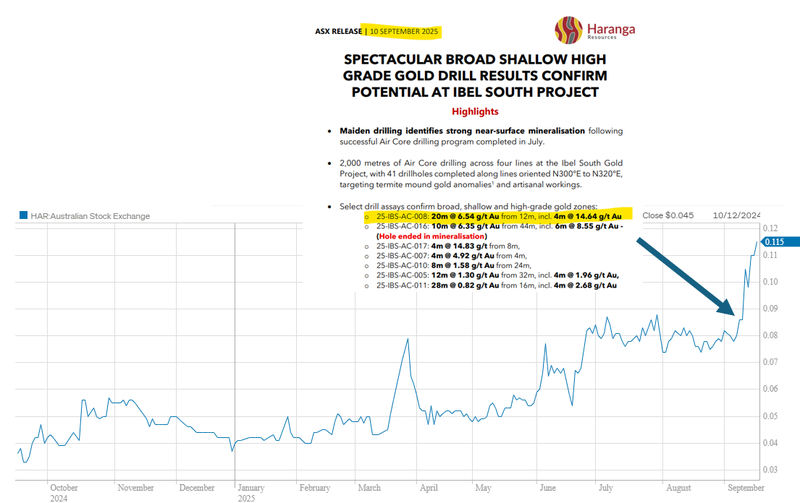

HAR’s results were a lot better than we expected (we had zero expectations actually, because we are focused on the new USA gold project) - especially from a small aircore program - and the market seemed to like them too.

HAR’s share price went from ~8c to ~12c adding ~$11M to its market cap:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It’s far too early to say what HAR has on its hands, but the buying is probably because the market wants exposure just in case HAR’s aircore holes are the first into what becomes a giant discovery...

(similar to another African gold success story like the $1.1BN Predictive Discovery).

Anyone who followed the Predictive Discovery story will know what good aircore hits can lead to...

Predictive’s first ever hits were from an aircore drill program, then after those hits were followed up with deeper holes and the market understood what Predictive had, the stock started running.

Predictive when the aircore results came out had a share price of 0.5c, today its capped at $1BN and is trading at ~48c per share.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It’s still very early days but those results from HAR don't look all that different to Predictive's first batch of results.

We will need to see some deeper drilling before we really know what HAR has in Senegal.

HAR has already brought forward a second drill program on the asset planned for late October...

All the while, the gold price is running and looks like it wants to run to US$4,000 per ounce.

So over the next six months while the gold price runs and small cap gold stocks are seeing capital inflows HAR will be:

- Drilling its US gold project looking to convert the existing non-JORC resource into a maiden JORC resource.

- Drilling its gold project in Senegal next to $15BN Endeavour Mining and $2BN Resolute Mining’s projects.

Main reason we are in HAR is for the USA gold project.

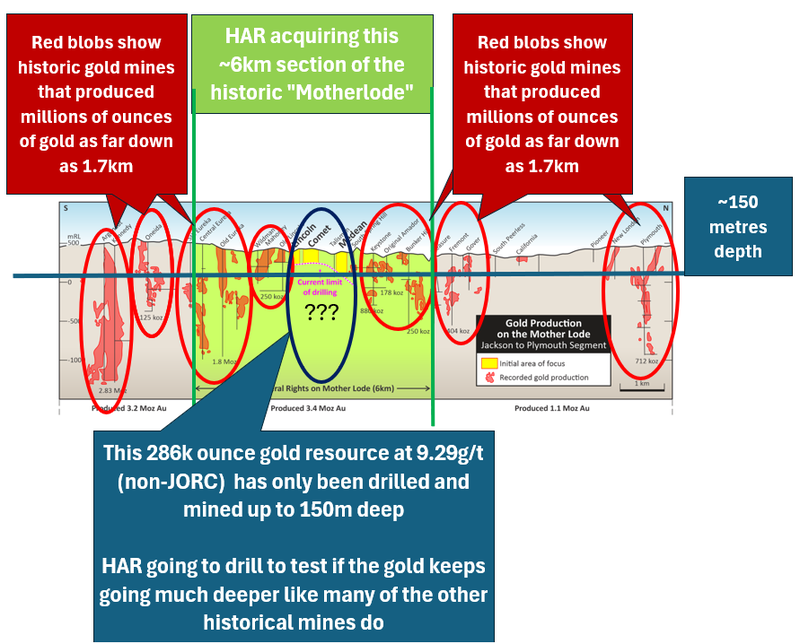

HAR’s US asset is in the richest section of the famous California gold rush Mother Lode...

(with a fully built and PERMITTED gold processing plant)

- A 100% owned built and permitted 350,000 tpa gold processing plant,

- An 880m decline (the tunnel that goes underground to get to the gold),

- Offices and a workshop,

- All up, $90M of sunk capital by previous owners to build it all.

HAR’s project already has a 286,000 oz non-JORC gold resource at 9.28g/t - with 2008 data showing it could, as it stands be up to ~682,000 ounces.

(that’s without doing any additional drilling)

(Source - non-JORC resource from 2008)

Taking a look at a cross section above you can see all the old mines in the area where there has been ~7.7 million ounces of historic gold production.

HAR holds all of the ground in the green...

Some of those old mines in the region were mined down to ~1.7km depths.

The area HAR will be drilling first hasn’t been tested below ~150M depths.

HAR’s existing non-JORC resource has an average grade of ~9.29g/t gold...

IF HAR can hit intercepts anywhere near those grades in the next round of drilling it could really start to get the market excited about the company’s assets.

Especially considering HAR has an existing high grade resource AND a permitted, ready to go processing plant.

Good drill results may bring attention to HAR, then the market might start to price into HAR’s valuation, a scenario where HAR is producing gold from its project relatively quickly.

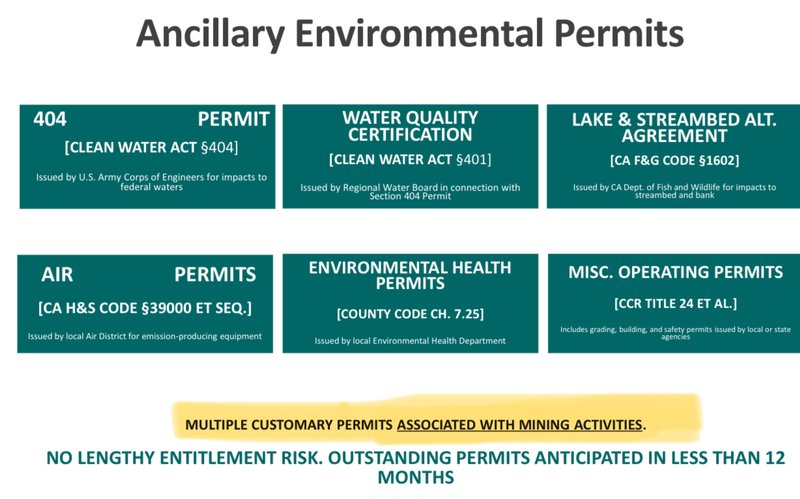

HAR actually presented the permitting status of its project saying the only outstanding “ancillary” permits were “associated with mining activities”.

HAR explicitly said that the process to get those permits would take LESS THAN 12 months:

See that presentation on the permitting status of the project here.

It’s been a few months now since HAR bought its US gold assets where we put $200k cash into the 5c capital raise associated with the transaction.

With a lot of luck HAR has managed to time its first drill program just as gold has broken out into new all time highs...

Since HAR acquired the asset, the gold price is already up by over US$800 per ounce...

We hope the higher gold price means the market is more willing to re-rate the stock (assuming the results come in), and HAR achieves our Big Bet which is as follows:

Our HAR Big Bet:

“HAR re-rates to a market cap greater than $200M by making new gold discoveries in California and progressing towards production or is acquired at a multiple of our initial entry price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our HAR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for HAR?

Drilling on HAR’s US gold project 🔄

First we need to see the dewatering process get completed.

HAR in its most recent update said “Dewatering of the Decline is progressing at maximum allowable rates”. (Source)

Once HAR is able to access its underground decline, it will be all about drilling.

HAR expects drilling to start in October and a maiden resource put out for its project by the end of the year. (Source)

Drilling on HAR’s gold project in Senegal 🔄

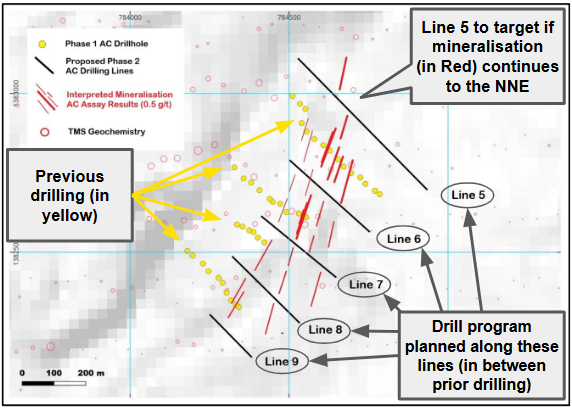

HAR’s plan is to drill ~3,000m aircore holes in Senegal in late October.

The main aim for the upcoming drill program is to test for extensions to what's been found already.

Here is where those holes will go:

(Source)

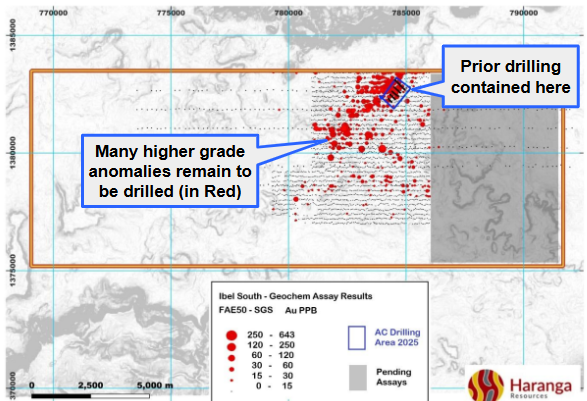

We also note that the area HAR is drilling is still just a tiny part of its project... so it's still very early days, and it's impossible to know how big what HAR has on this project is:

(Source)

What are the risks?

Given HAR’s drilling is still at least a month away on both its projects, the two key risks in the short term for HAR are “delay risk” and “funding/dilution risk”.

Delay risk, because there is always a chance the dewatering process in the US takes longer than expected and HAR isn’t able to drill in October.

Development/delay risk

Should any or all of the above risks materialise, HAR could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on HAR.

Source: “What could go wrong” - HAR Investment Memo 25 June 2025

Second is funding risk, because the dewatering process and bringing HAR’s project up to a condition where it is able to re-enter its decline may require a fair bit of capital expenditure.

There is always a risk that HAR need to top up their cash balance ahead of OR after its drill program.

We note HAR had ~$3.94M cash in the bank at 30 June 2025. (Source)

Funding risk/dilution risk

As a small cap, HAR is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, HAR could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong” - HAR Investment Memo 25 June 2025

Other risks

Like any stock market investment, investing in HAR carries a multitude of risks which may affect the value of the company, some of which may not be foreseeable (this is the nature of risks).

Here we aim to identify a few more risks.

HAR’s US project is still at the exploration and early-development stage. It is possible that drilling fails to convert the existing non-JORC resource into a JORC-compliant resource of economic significance.

The company is also exposed to fluctuations in the gold price. A sustained downturn could impact the perceived value of both its US and Senegal assets, and limit HAR’s ability to secure funding on favourable terms.

As a small cap explorer, HAR remains highly reliant on capital markets to fund exploration and development. Any capital raising may dilute existing shareholders, particularly if market conditions weaken.

There are also permitting and development risks. While HAR’s US project has significant sunk capital and existing permits in place, additional mining-related permits are still required, and any delays could affect timelines.

In Senegal, political, regulatory and operating risks are higher compared to more established jurisdictions, and may impact exploration or potential future development.

Finally, as with all speculative explorers, the current share price may already factor in future upside, particularly in a rising gold market, which increases the risk of sharp volatility around drilling results.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our HAR Investment Memo:

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our HAR Investment Memo where you will find:

- What does HAR do?

- The macro theme for HAR

- Our HAR Big Bet

- What we want to see HAR achieve

- Why we are Invested in HAR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.