2020 Market Outlook Part 2: A portfolio for all seasons

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Yesterday I underlined a number of reasons why I felt that the market could come under extreme pressure in 2020 and in doing so I suggested a broad strategy that could provide some insulation against a market shock should it eventuate.

Key company attributes I am looking for in trying to shock proof my portfolio are diversification, predictable earnings and financial stability.

In terms of predictable earnings, it pays to target companies that provide products and services that are close to being essential needs for businesses and consumers.

In the retail sector such companies are placed under the banner of ‘consumer staples’ (S&P/ASX 200 Consumer Staples index (ASX:XSJ))

There is a strong focus on food, beverages and pharmaceuticals with companies such as Coles Group, Coca-Cola Amatil and Blackmores Ltd respectively being examples of those three categories.

Identifying providers of essential services to businesses isn’t as clear-cut and there isn’t a dedicated sector that accounts for such companies.

However, I will identify a company that fits this category that appears to have the merits I’m looking for.

Diversification can be obtained in a number of ways

The need for diversification has long been recognised in terms of establishing a sound portfolio of stocks regardless of market sentiment.

But it could be argued that having a diversified portfolio moves from the beneficial end of the investment spectrum to being absolutely essential when markets are volatile.

However, diversification comes in many forms, some of which tend to receive little attention.

Some of the more common types of diversification relate to commodity exposure (base metals/precious metals etc), geographic presence (alleviating sovereign risk issues or exposure to weak economies) and having a broad spread of clients/revenue sources so that there isn’t an over-reliance on one particular income stream.

There are some other facets of diversification that are worth considering in the current market, and I will discuss those in outlining my stock selections.

S&P/ASX 200 Financials excluding A-REITs Index

The S&P/ASX 200 Financials excluding A-REITs Index (ASX:XXJ) contains companies involved in activities such as banking, mortgage finance, consumer finance, investment banking and insurance, excluding Australian Real Estate Investments Trusts (A-REITs), mortgage REITs, equity REITs, and real estate management and development companies.

While there is an index which combines both financial stocks and REITs and the like, the companies are driven by very different economic factors and are sought after by investors looking to achieve varied outcomes and financial benefits.

The sector has traditionally demonstrated defensive characteristics with the big banks being front and centre of most portfolios with strong and reliable yields being a key attraction, particularly for retirees seeking tax effective income through franked dividends.

However, the sector has been rocked in recent years as the Royal Commission opened Pandora’s box.

As a plethora of banking practices ranging from unethical to disreputable and downright illegal were unveiled, sentiment towards traditionally safe haven stocks plummeted, and so did their share prices.

The banks were forced to make massive payments in the way of compensation and fines for practices as severe as laundering money for terrorist organisations.

The most recent casualty was Westpac, with Australia’s financial intelligence agency (Austrac) launching legal action, accusing it of more than 23 million breaches of anti-money laundering and counter-terrorism finance laws involving $11 billion in transactions, including transfers potentially linked to child exploitation.

Last year, the CBA agreed to pay Austrac $700 million to settle a similar action against it in which the regulator alleged more than 53,000 breaches of anti-money laundering and counter-terrorism financing laws.

It is difficult to determine whether other financial institutions could be in Austrac’s sights, so in my mind I would prefer to stay away from entities involved in customer facing areas.

With the Royal Commission has come a levelling of the playing field with anti-competitive practices used by the big banks brought to a halt or diluted.

Consequently, a wide range of financial companies specialising in various areas have emerged, while some banks have chosen to exit sub-sectors where they were benefiting from harnessing business through a vertically integrated/cross selling strategy.

Existing companies as well as new entrants require specialist investment platform technology and providers of these services usually generate upfront income as well as annuity revenue, providing strong earnings visibility.

This ticks a number of my boxes, and the company I have chosen is...

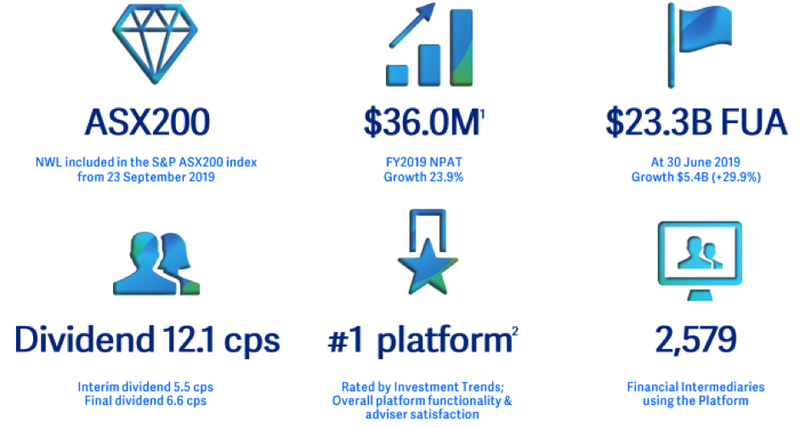

Netwealth Group (ASX:NWL)

The group is a technology company, a superannuation fund and an administration business rolled into one.

The digital platform supports delivery of the company’s financial products to the market, and through the platform financial intermediaries and clients can invest and manage a wide array of domestic and international products.

The platform is built, developed and maintained by Netwealth’s technology team, providing the group with total control from development to delivery of financial services.

As at June 30, 2019 the group had funds under administration of $23.3 billion, and management is forecasting this to increase to $30 billion by June 30, 2020.

The September quarter featured the strongest quarter on quarter net flow growth of approximately 40% since the company listed.

Consensus forecasts indicate that Netwealth should generate earnings per share growth of about 20% in fiscal years 2020 and 2021.

This is well above the normalised year-on-year earnings per share growth offered by the big banks.

For example, even on the back of negative earnings per share growth in fiscal years 2018 and 2019, consensus forecasts indicate the CBA will only achieve EPS growth of 0.5% in 2020 and 3.1% in 2021.

S&P/ASX 200 Real Estate

As the name suggests, this index (ASX:XPJ) is strongly leveraged to the property sector, and it has also traditionally posted companies that pay strong and predictable dividends from long-term rental income generated by properties that are part of their investment portfolio.

Some of the household names include Stockland, Mirvac and National Storage.

They tend to differentiate themselves by the property sectors they target.

For example, companies such as Stockland tend to have a heavy skew towards residential developments.

Mirvac is more diversified with a portfolio of assets that spans the office, retail, industrial and residential sectors.

While I value the diversification that Mirvac offers, as I said earlier there are other forms of diversification that are also worth considering.

My pick stock in the sector is...

Goodman Group (ASX:GMG)

Goodman has a strong track record of delivering reliable earnings and dividends from a property portfolio that is continually revised to minimise risks and maximise the company’s exposure to emerging trends.

Goodman Group is an integrated property group with operations throughout Australia, New Zealand, Asia, Continental Europe, the United Kingdom, North America and Brazil.

The group comprises the stapled entities Goodman Limited, Goodman Industrial Trust and Goodman Logistics (HK) Limited.

Goodman is the largest industrial property group listed on the ASX and one of the largest listed specialist investment managers of industrial property and business space globally.

Management recognises sustainability as the key to achieving strong business outcomes.

The company recently acknowledged structural changes are continuing to drive the momentum for improving supply chain efficiency.

This has prompted the deliberate urban logistics concentration of its portfolio which is the critical factor supporting the group’s customers’ supply chain evolution over the next five to ten years.

This strategy is expected to generate resilient cash flows while also providing opportunities for higher and better uses in the long term.

Management recently noted that its customers have an increasing requirement for well-located, high-quality industrial real estate, and the group has specialist management and infrastructure to meet this demand as it continues to incrementally acquire sites in high barrier to entry markets around the world.

Yesterday I mentioned the need to identify companies with industry leading positions ideally in niche markets, and Goodman’s strategy of entering high barrier to entry markets is appealing.

Goodman is well leveraged to the long term positive outlook for industrial and logistics properties which are being supported by rapid growth in e-commerce/online retail sales and a growing middle-class demographic in developing countries.

S&P/ASX 200 Consumer Staples

As we mentioned earlier, this is a sector traditionally sought after because of the earnings predictability that it offers.

A decade or so back, the ‘go to’ stocks for mum and dad investors were Coles and Woolworths (ASX:WOW)

They had a virtual duopoly if you discount Metcash (IGA etc) as a competitor, but the landscape changed from a number of perspectives.

Firstly, Coles was rolled into Wesfarmers (ASX:WES) which has assets such as coal mines that lie well outside the consumer staples area.

Wesfarmers divested Coles in 2018 and the group relisted (ASX:COL) on the ASX with a price of $12.49.

While its shares have since traded as high as $16.60, I am not drawn to it or Woolworths.

Firstly, we have gone through a long period of low growth in food and grocery prices, a trend that appears likely to continue.

Also, the competitive landscape has changed dramatically with the entry of Aldi and Costco.

Coles and Woolworths no longer have a duopoly, and with the pending entry of multinational Lidl, price wars are expected to escalate, effectively driving down margins and earnings unless internal changes can be made in terms of optimising and rationalising their existing businesses.

It would seem there is not a lot of fat to be cut in terms of cost management, and their valuations look extremely stretched when weighed up against the forecast growth in earnings.

Regards the latter, Woolworth is trading on a fiscal 2020 PE multiple of 26 which is difficult to support given that the group is only forecast to generate earnings per share growth of approximately 7% per annum over the next two years.

The company isn’t even a good yield play these days with forward estimates implying yields of around 3% in 2020 and 2021.

My pick in the sector is...

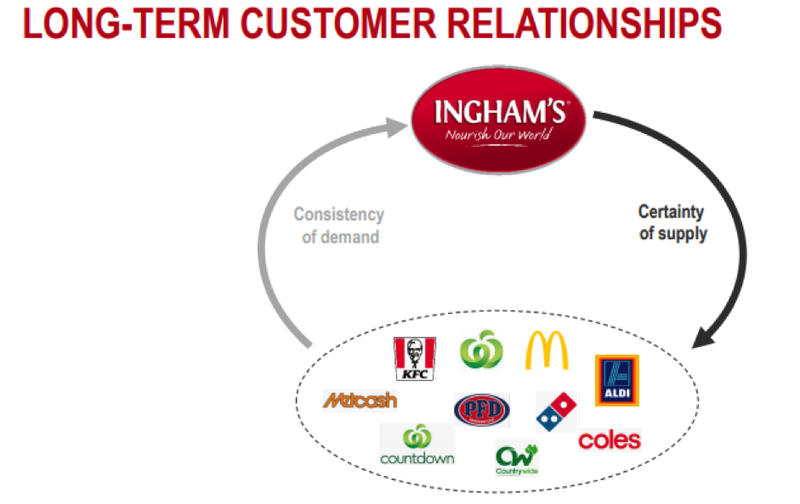

Inghams Group Ltd (ASX:ING)

Australia and New Zealand’s leading integrated poultry producer supplying retail, quick service restaurants and food service customers.

The company processes 4 million birds per week, and it operates twelve feedmills, breeder and broiler farms, eleven hatcheries, seven primary processing plants, seven further processing plants and nine distribution centres.

While there was some disappointment regarding the group’s fiscal 2019 result, the share price decline appeared to be exaggerated, and the rally that has occurred over the last two months seems to support this view.

Poultry demand continues to grow as consumers are attracted by the relative affordability of chicken as a healthy protein.

With the prices of beef and seafood soaring, there is scope for poultry prices to increase considerably while still being extremely affordable in comparison to beef and seafood.

Inghams is currently trading on a fiscal 2020 PE multiple of 14.3.

Based on consensus dividend forecasts for fiscal 2020, the company is yielding 4.8% which on a grossed up basis (taking into account franking credits) equates to a yield of 7%.

S&P/ASX 200 Consumer Discretionary

The S&P/ASX 200 Consumer Discretionary index (ASX:XDJ) encompasses those industries that tend to be the most sensitive to economic cycles, which in turn impacts consumer spending.

Its manufacturing segments include automotive, household durable goods, textiles, clothing and leisure equipment.

The services segment includes hotels, restaurants and other leisure facilities, media production and services, and consumer retailing and services.

Some of the better-known names in the sector are Domino’s Pizza Enterprises, Flight Centre Travel, Harvey Norman and JB Hi-Fi.

With regard to consumer spending, economic data relating to retail sales and consumer confidence suggest we have been on a downtrend for some time, and this is unlikely to significantly improve in the near term.

Despite the government’s economic stimulus initiatives such as tax cuts along with the RBA’s decision to consistently place downward pressure on interest rates, consumers are still reluctant to spend.

Another factor that has negatively impacted the sector is the trend towards purchasing goods online which has made life difficult for bricks and mortar retailers who not only have fixed costs such as rents and wages, but in many cases they are attempting to contend with declining revenues.

While this backdrop sounds fairly gloomy, 12 months ago I had several stocks on the radar that I figured had been oversold, and in the medium term had the potential to make a solid recovery.

However, the sector seems to have been swept up in a surge of positive sentiment, perhaps driven by the potential for a further RBA cash rate cut in 2020 (many analysts are expecting this to occur in every 2020) and the expectation of tax cut related sales momentum.

But one needs to remember that rates are at an all-time record low with little room for the banks to pass on any further cuts.

In the last 12 months the XDJ has increased from about 2100 points to 2750 points, representing a gain of about 30%.

As we mentioned yesterday, the XJO has increased by about 25% over the same period.

If anything, one would expect the XDJ to be underperforming the XJO given the macro-economic headwinds which also include the increased cost of goods imported due to the depreciation of the Australian dollar.

In search of value, I have stepped outside the ASX 200, opting for...

Lovisa Holdings Ltd (ASX:LOV)...

a bricks and mortar retailer that is a growth by store expansion story.

While its PE multiple relative to other retailers suggests it may be overpriced, the growth implied by forecasts in 2020 and 2021 which is in the vicinity of 20% per year is superior to most if not all XJO retailers.

I also like the fact that it targets the low price point end of its core fashion accessories and jewellery market.

Global diversification alleviates some of the foreign exchange imposts

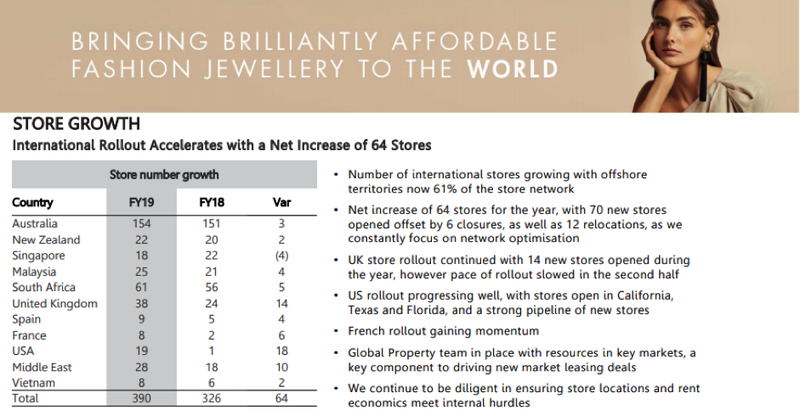

Generating robust cash flow is important in the retail industry, particularly for a company such as Lovisa that is reliant on global expansion to drive growth.

The company excelled in this area in fiscal 2019 with cash from operations before interest and tax of $66.7 million, supported by operating cash conversion at 107%, metrics that plenty of other retailers would love to boast.

Lovisa continues to manage its working capital well in the face of the ongoing investment into stock for new stores and to support eCommerce where it has been operational in Australia and New Zealand since 2018, and the European Union and the UK since July 2019.

International expansion continued with a further net 64 stores opening during the financial year and a total network of 390 stores at financial year end.

More than 60% of Lovisa’s store network is now located outside of Australia, and with the company expanding into the US and France, momentum continues to build.

In fact, as I write the store numbers stand at 421 with 33 stores currently trading in the US across five states.

S&P/ASX 200 Industrials

The S&P/ASX 200 Industrials index (ASX:XNJ) offers diversification by virtue of the fact that it hosts companies that generate income from a wide range of industries and geographic regions.

The index includes companies whose businesses are dominated by activities such as the manufacture and distribution of capital goods, including aerospace and defence, construction, engineering & building products, electrical equipment and industrial machinery.

There are also a large contingent of services companies that are involved in the provision of commercial services and supplies, including printing, employment, environmental and office services, as well as transportation services, including airlines, couriers, marine, road and rail, along with transportation infrastructure such as airports and toll roads.

Prominent names include Qantas, Seek, Brambles, Transurban Group and Sydney Airport.

However, I mentioned earlier that I would feature a company that provided essential services to business and this brings me to my stock pick in the industrials sector:

ALS Ltd (ASX:ALQ)

ALS is a group that appeals for a number of reasons.

ALS is a global market leading testing, inspection, certification and verification company headquartered in Australia.

The company services multiple industries, implying more than 13,000 staff in over 65 countries.

Predominantly through its laboratory services operations, ALS has built its reputation around technical innovation, quality, a deep client understanding, and by being a true technical services partner to many companies across a broad spectrum of markets covering most geographies.

For many businesses they have no option but to use the services offered by ALS.

In the mining industry, the company’s expertise in analysing mineral samples is vital in terms of shaping exploration and development strategies with a view to minimising costs and optimising production.

ALS has traditionally been heavily reliant on the resources sector, and the company has established a strong market leading presence in the industry.

However, this has also presented its challenges as the group became very much a cyclical play with earnings reliant on a buoyant resources sector.

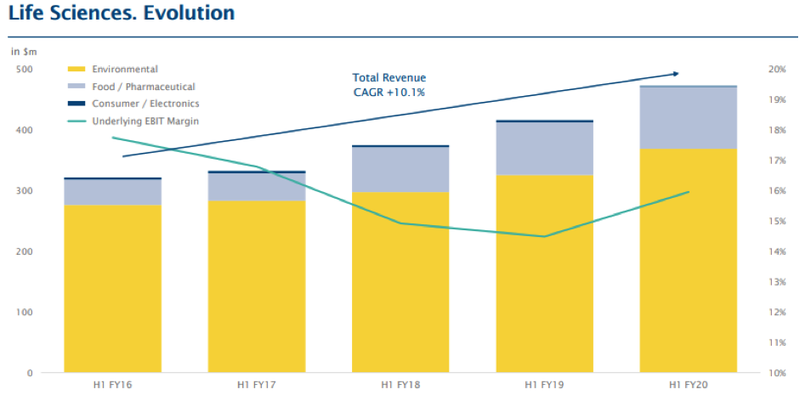

In recent years ALS has diversified into life sciences, providing exposure to all manner of consumer products from food to pharmaceuticals.

Consequently, the company is leveraged to activity in subsectors such as agriculture, food safety, pharmaceuticals, and the broader area of environmental health and safety.

With regulatory conditions tightening across these areas and an increase in technological expertise required to fully comply with those regulations, this presents as a good fit with ALS as it has demonstrated its ability over decades to be a market leader in developing technologies to enhance analytical outcomes.

This area of the company’s business was bolstered in August when the company acquired Mexico City based Laboratorios de Control ARJ S.A de C.V.

ARJ is the largest private pharmaceutical testing laboratory in Latin America with revenues of over $30 million.

The company specialises in providing quality control for medicines, biological products, generics, cosmetics and medical devices, and it services many of the largest global pharmaceutical companies.

Mexico is a growing part of the $20 billion global pharmaceutical testing market and an important hub for Latin and North America.

ARJ will complement the existing ALS Life Sciences Latin America operations and is expected to benefit from group’s regional and global presence to further expand their offering to clients.

Similar to the mining industry, the life sciences division provides services that are essential to the industries that operate within the sectors previously mentioned.

However, on the score of essential services the life sciences division is a beneficiary of government legislated regulations that enforce appropriate testing, quality control and compliance procedures.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.