WHK Quarterly: We are pleasantly surprised - here’s why

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 6,828,547 WHK shares and the Company’s staff own 195,000 WHK shares at the time of publishing this article. The Company has been engaged by WHK to share our commentary on the progress of our Investment in WHK over time.

Our cybersecurity Investment WhiteHawk Ltd (ASX:WHK) has surprised us with some revenue growth, positive operating cashflow and partnership traction in its latest quarterly report.

Like most tech stocks, WHK took a beating in the 2022 tech wreck.

We are hoping that 2023 will be the year that it all comes together for WHK - via a couple of the big deals we have been waiting for, partnership revenue to start coming in, combined with a rebound in tech sentiment.

Today’s WHK quarterly report marks a great start for 2023.

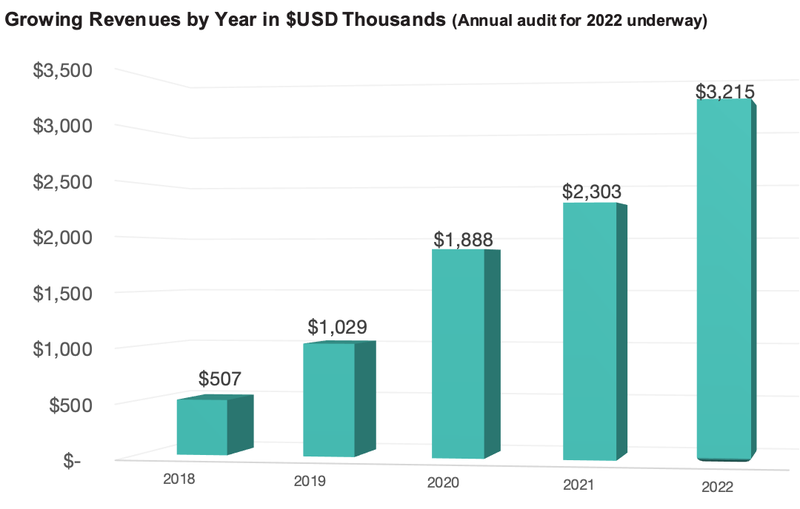

The first thing that jumps out is the steady revenue growth in this chart, especially in what was a tough year for tech companies in 2022:

In today’s quarterly, WHK also listed a sales pipeline of large deals that could materially increase this revenue growth if they are signed.

We believe the signing of these deals will re-rate the share price - it’s our view that the market has penalised the WHK share price for ongoing delays in these deals.

In other words, a pipeline of deals is great, but the market wants to see them convert into actual revenue, and show bigger year to year revenue jumps.

Aside from deals, another key, expected revenue stream for WHK is through distribution partners.

WHK has signed partnerships with Dun & Bradstreet, Amazon Web Services (AWS) Corporate, Sontiq, and Peraton - to essentially push the WHK cybersecurity products to their clients.

Partnerships with big names in tech often sound great when announced to the market, but are notoriously difficult and slow to convert to actual revenue.

In today’s quarterly report, we were particularly impressed that WHK has sold licences through one of its partnerships (Dun & Bradstreet).

This early traction with a key partner is an extremely positive proof point that WHK’s partnership model is truly symbiotic (meaning both sides of the partnership extract value) and has the potential to grow across the multiple partnerships WHK has signed up.

We have been investing in tech companies for a long time, and have seen many small cap tech stocks sign partnerships with big, global partners.

In tech, most of these types of partnerships look exciting on paper, however, ultimately many don’t deliver revenue. That’s because the value exchange is often too one sided towards the smaller company for the larger partner to be interested in putting energy or resources into the partnership.

We can’t stress the importance (in our opinion) of this early traction from a WHK partnership, and what it signals for the potential of its other partnerships.

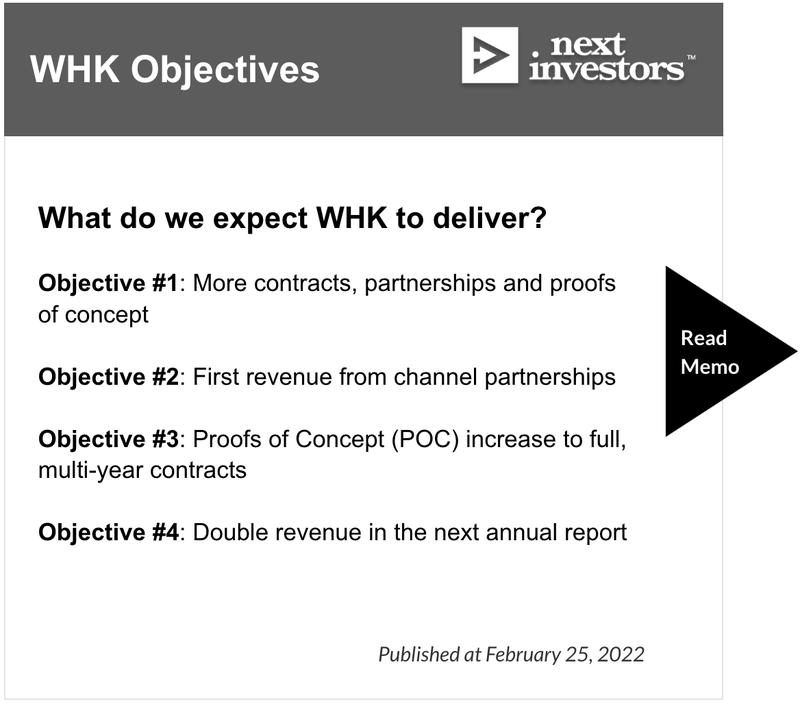

To that end, we think that in this latest quarterly, WHK has made progress across all the objectives we set in our WHK Investment Memo almost a year ago.

We will cover some of them today.

Looking back, here is what we wanted to see WHK achieve over the course of 2022:

A Quick Background on WHK

WHK has been in our Portfolio since 2019.

WHK’s clients and partners include the U.S. federal government and defense force departments as well as industry leading corporations and Fortune 500 companies.

These are large, complex and slow moving organisations and they like to keep their names out of the spotlight — especially when it comes to the sensitive topic of cybersecurity.

It can take months upon months of negotiation to get these deals over the line, however when they do land, they tend to be highly sticky clients that present huge scope for ongoing and expanded services for years to come.

We are confident that if a few of the big deals that WHK has in its pipeline land and partnerships start firing, the jump in revenue growth will lead to the share price re-rate we want.

Led by CEO Terry Roberts, a former deputy director of US Naval Intelligence and 35-year veteran of the US national security and cyber intelligence community, we think WHK has the networks needed to negotiate at the highest levels.

To further drive sales WHK has partnered with some of the biggest names in the business, including Dun & Bradstreet, Amazon Web Services (AWS) Corporate, Sontiq, and Peraton, and has just demonstrated first traction through one of these partnerships.

What’s to come?

WHK ended the quarter cash flow positive and with US$2.17M in the bank.

Heading into 2023, revenue projections are on track with current contracts, an active commercial pipeline and government request for proposals (RFPs).

The A$16.1M-capped WHK has a pipeline of US$20M worth of new sales bookings to reach its growth benchmark of US$5.5M. Included in this is:

- US$4.5M for its Cyber Risk Radar

- US$2M for its Cyber Risk Program

- US$10.5 from the Sontiq-WHK Business Suite.

On top of those expected new sales bookings, WHK expects to upsell/cross sell to its existing customers and is targeting a 80% customer renewal rate.

Specifically, it anticipates a further US$500,000 from its federal government Chief Information Security Office (CISO) contract, US$1.5M from its commercial clients, and another US$1M from its manufacturer client.

We added WHK to our Portfolio in May 2019 and have Increased our Position four times.

However, after a strong start, the company’s share price was underwhelming for the past two years — falling from its 46.5c per share peak in January 2021 to below 7c per share today.

That came even as the company accrued contracts and grew revenues.

The issue seems to be that WHK faced a couple of key contract delays, there were delays to new U.S. cybersecurity supply chain legislation, and the 2022 NASDAQ tech wreck that battered even the largest U.S. tech stocks.

You might wonder why we would keep Investing into and supporting a falling stock?

Firstly, it provided an opportunity to average down our entry price — we consider this a long term Investment.

Secondly, we continue to back WHK and its management’s ability to secure more contracts at the highest levels of the US government and industry, especially given the consistent revenue growth WHK is achieving.

We recognise the opportunities for WHK in this space, particularly given the credentials of its CEO along with its current partnerships, not to mention the highly supportive macro outlook as supply chain companies must adopt adequate cybersecurity measures.

In summary, we believe in the management, the business plan and the macro theme over the long term.

Like many early stage stocks, this one just needs some patience.

And as always, there are risks that could materialise (which we summarise in our Investment Memo), and in WHK's case the “sales risk” and “market risk” we initially flagged both impacted the share price over the last 12 months.

Looking at today’s quarterly report and the huge list of opportunities that WHK and its partners are chasing, our view is that the share price sell off may have been overdone, especially if WHK can deliver the deals we have been waiting for.

Our Big Bet:

“WHK becomes a $500M technology company by securing new contracts and partnerships as legislation and public pressure force governments and companies to invest in cybersecurity”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our WHK Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

How does WHK’s quarter stack up against our February 2022 Investment Memo?

Today’s quarterly report reveals that WHK has made some real progress against our objectives that we set for the company in our Investment Memo we set out for WHK in February 2022:

Objective #1: More contracts, partnerships and proofs of concept

WHK management has proven they can sign contracts and partnerships with top tier large organisations.

This is the progress it made in the past quarter on that front:

- CONTRACT SIGNED: Renewed Cyber Risk Radar contract with Global Social Media Platform Company for 12 months, with engagement for expansion to additional business units.

- PIPELINE OPPORTUNITY: Responded to the U.S. Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA) National Risk Management Center (NRMC) supply chain risk management (SCRM) small business Sources Sought opportunity — a 3 year US$30M contract.

- PIPELINE OPPORTUNITY: Responded to a Department of Energy Cyber Resilience of Rural Utilities Request for Proposal (RFP).

- PIPELINE OPPORTUNITY: Working with AWS Federal, scoping a Cyber-Supply Chain Risk Management (C-SCRM) proof of value for a U.S, Department of Defense Program.

- PIPELINE OPPORTUNITY: Finalising a Cyber Florida Critical Infrastructure Cyber Risk Assessments Pilot to be conducted across 150 entities in 1st QTR 2023.

- PIPELINE OPPORTUNITY: Contracting paperwork being finalised for a U.S. city, Cyber Risk Program FEB23.

Objective #2: First revenue from channel partnerships

WHK has already signed some interesting partnership deals (Dun & Bradstreet, Amazon Web Services) which have big potential.

We’re also closely watching developments to come out of the Sontiq-WHK Business Suite. Sontiq is a division of TransUnion - an American consumer credit reporting agency (market cap US$13BN).

Our hope is that Sontiq can help push WHK’s product out to their network.

We want to see the first revenue coming in from these partnerships.

Here’s WHK’s progress in the last quarter:

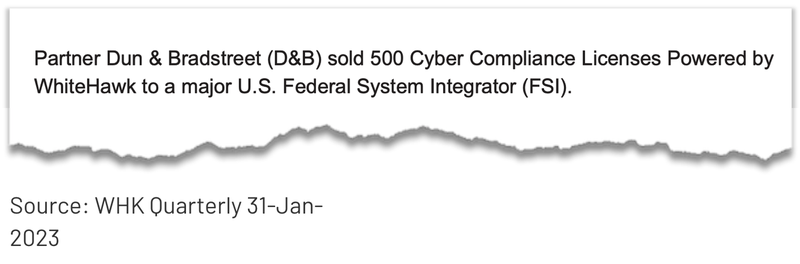

- TRACTION ACHIEVED: Partner Dun & Bradstreet (D&B) sold 500 Cyber Compliance Licenses powered by WhiteHawk to a major U.S. Federal System Integrator (FSI).

- PIPELINE OPPORTUNITY: With D&B Public Sector in lead, awaiting Board of U.S. Federal Reserve Bank decision on a Cyber Risk Monitoring contract across all 5,000 U.S. financial institutions, due in 1st QTR 2023.

- PIPELINE OPPORTUNITY: Commenced Cyber-Supply Chain Risk Management (C-SCRM) IRAD (independent research and development) first phase with Peraton in December 2022 and scoping phase 2 for 1st QTR 2023. [Peraton is a private company that brings in US$7BN per year. Peraton was formed when Perspecta, Northrop Grumman's federal IT division, Harris Corp’s government IT services division, and Hewlett Packard Enterprise Services’ were rolled into one.]

- PIPELINE OPPORTUNITY: Signed a Letter of Intent with Peraton as a Cyber Technology Insertion and Cyber-Supply Chain Risk Management (C-SCRM) partner on the Dept Homeland Security CISA (Cybersecurity and Infrastructure Security Agency) cybersecurity contract vehicle ACTS.

- PIPELINE OPPORTUNITY: Advancing Sontiq WHK Business Suite SaaS EMBED sales to global Managed Service Providers, financial and insurance firms for their SME business clients.

Objective #3: Proofs of Concept (POC) increase to full, multi-year contracts

WHK is signing Proofs of Concept (small paid contracts to try the product, that lead to bigger contracts if successful). We want to see WHK successfully convert several POCs to large contracts.

Progress in the last quarter WHK:

- PIPELINE OPPORTUNITY: Awaiting decision on a 60-day U.S. Government Cyber Risk Radar, Cyber-Supply Chain Risk Management (C-SCRM) Proof of Value, for US$350K.

Objective #4: Double revenue in the next annual report

Objectives 1, 2 and 3 will lead to the ultimate goal of growing revenue.

Early last year we said that “we want to see WHK double its revenue this US financial year (December 31st 2022)- targeting a topline revenue of US$4.6M”.

Here’s how they’ve tracked with revenue over time:

While WHK didn’t double its 2021 revenue in 2022, it did grow its revenues by around 40%.

And considering the tech wreck of 2022, delayed US Defense force cyber supply chain legislation and contract delays for WHK, we are satisfied with its progress on this front.

We anticipate a sharp rise in revenue if WHK, with its partners, can lock in some new deals and continue to re-sign existing clients.

Of course, that's no guarantee - in the past we have seen how long things can take with WHK, and how this can damage the share price - the market can get impatient. At the end of the day WHK is a high risk investment.

US cybersecurity legislation the big catalyst for WHK?

In May, the US Government is set to roll out cybersecurity legislation that could provide the urgency to drive cybersecurity sales for WHK.

These rules will require the 330,000+ U.S. Department of Defense (DoD) supply chain companies to have adequate cybersecurity protections.

We think this will significantly help WHK achieve its objectives.

The DoD has developed the Cybersecurity Maturity Model Certification (CMMC), a security framework to assess the security and capabilities of every one of its contractors and subcontractors.

The legislation was first floated in February of 2020, and after delays as the incoming Biden administration worked to put its own stamp on it, the legislation is now finally set for release in May 2023.

If you thought small cap stocks can move slowly - imagine working in government.

But this one looks like it's finally happening.

Soon every company along the supply chain that does business with the U.S. DoD will require CMMC certification — that’s more than 330,000 U.S. Defense Industrial Base companies, all needing to have their cybersecurity house in order.

WHK is in a prime position to provide immediate cybersecurity solutions for supply chain companies from the smallest to the largest.

WHK intends to provide solutions as a third party assessor and in assisting the DoD supply chain companies in conducting self assessments, and says it is uniquely positioned to provide an automated path for DoD contractors and is working alongside its U.S. federal focused partners.

These include AWS Federal, D&B (Dun & Bradsheet), and Peraton.

When we first Invested in WHK, we were expecting this legislation to come into effect shortly after and turbocharge WHK’s new client sign-ons.

So after years of delays it’s great for WHK that these new US laws are finally being implemented.

WHK’s recent funding agreement

From a financial perspective, WHK achieved its second cash flow positive quarter for the year.

Most growth companies can eke out one quarter of positive cashflow — but to do it on multiple occasions, for an early-stage tech company that is still growing, is a milestone event. We are hoping WHK can make it three in a row next quarter.

With the funding environment for tech companies a lot less positive all around the world we think WHK’s quarterly comes at precisely the right time too.

We also note that WHK recently secured a funding agreement from New York based Lind Partners for a total of $3M.

The arrangement saw WHK receive an initial $2M with the option of securing a further $1M.

(Note: the above is in USD).

The agreement is not a straightforward type of capital raise exchanging shares for cash, instead it appears similar to a convertible note where the funding is exchanged for shares over a period of time at differing prices.

Our high level summary of WHK’s deal with Lind is as follows:

- Lind can be issued a maximum of $150k in WHK shares in the first five months at 10c per share.

- After this, they get the right to convert and sell $150,000 at a 20% discount to the lowest 5-day VWAP (volume weighted average share price) of each month.

The key difference between this deal and some of the other convertible notes we have seen is that WHK was able to get a ~5 month grace period where the facility is repayable at a much higher share price than the current 6.8c share price.

This effectively bought WHK ~5 months of time to execute on a major catalyst and hopefully deliver a re-rate to the company’s share price.

When the 5 month period passes, we hope WHK’s share price is higher than the 10c conversion price, so that repaying the facility would not be a problem either via a capital raise or by issuing Lind the $2M at 10c per share.

We have seen other companies in our Portfolio pull off deals like this too.

Latin Resources signed a funding agreement with Lind back in early 2022 buying the company enough time to go and drill its lithium project in Brazil.

A few months later the company made a discovery, its share price re-rated from ~3c to ~23c per share and the facility was repaid with no impact on the company’s share price.

Of course we also note that sometimes companies are not able to deliver any major catalyst and the facility slowly starts getting converted on market.

If this were to happen we would expect there to be short to medium term pressure on the WHK share price as Lind converts its shareholdings and looks to sell some of those shares on market.

Click here to read more of our commentary on Convertible Note funding agreements.

There is still around 2 months remaining before Lind can be issued any WHK shares so we are hoping for a major catalyst (and hopefully a re-rate in WHK’s share price) before then.

We are pretty sure that WHK management will feel the same way and will be working towards it.

Our WHK Investment Memo

Risks

WHK is a small cap, high risk stock, and there are a myriad of factors that could contribute to WHK not delivering a positive return for investors.

Below is a snapshot of just some of the major risks we see for WHK - this by no means an exhaustive list (sometimes the biggest risks are the ones you can't see).

Sales risk means that there is the possibility that WHK doesn’t close the deals it needs to in order to achieve its revenue targets - this risk has impacted the share price over the last 12 months.

Market risk is still applicable, just because the US tech wreck of 2022 looks to have abated recently doesn’t mean the market could take WHK lower - this risk has impacted the share price over the last 12 months.

Competition risk is important as well - WHK is moving in circles where large cybersecurity companies are also operating. These companies could poach WHK’s contracts or offer services at cheaper prices.

Finally, if we’d had our time again we’d also have included funding risk in our Investment Memo, which is an ever present part of the small-cap market. See the section on WHK’s funding agreement above for further information.

Click here to see our full WHK Investment Memo, where you can also find:

- Key objectives we want to see WHK achieve

- Why we are Invested in WHK

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.