Why do different commodities suddenly become “hot”?

Published 22-JAN-2024 10:00 A.M.

|

14 minute read

Ever tried to move house?

Or change your internet provider?

Convince your partner (or parents) to let you get a dog?

The process can be excruciating, take a lot longer than expected, and require more lobbying and negotiating than you ever anticipated.

And that’s just working with one or two stakeholders.

Now imagine trying to convince the whole world to switch to electric vehicles and a cleaner energy mix.

Electrification will not only be good for the environment, but importantly it will reduce the West's risk from reliance on fossil fuel imports from geopolitical “frenemies”.

The process of aligning governments, communities, capital, incumbent corporations, and securing supply and supply chains for the electrification transition is NOT a quick or easy task.

The process is going to take decades.

It’s going to require a lot of batteries and clean energy sources AND also new sources of fossil fuels during the decades-long transition period.

Our strategy is to Invest in small cap stocks developing the commodities that are needed for the energy transition - battery metals, clean energy AND fossil fuels (still needed while the transition is occurring).

And sometimes certain commodities suddenly launch into favour...

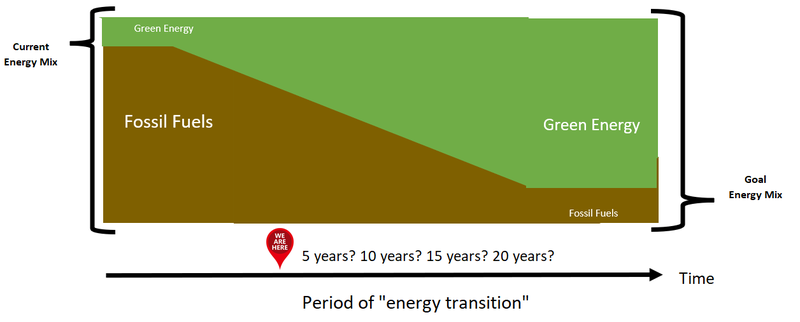

Right now ~80% of the world’s power is generated using fossil fuels.

Here is our rough approximation of how we think the energy mix will develop over time:

Key point, it is going to take ages.

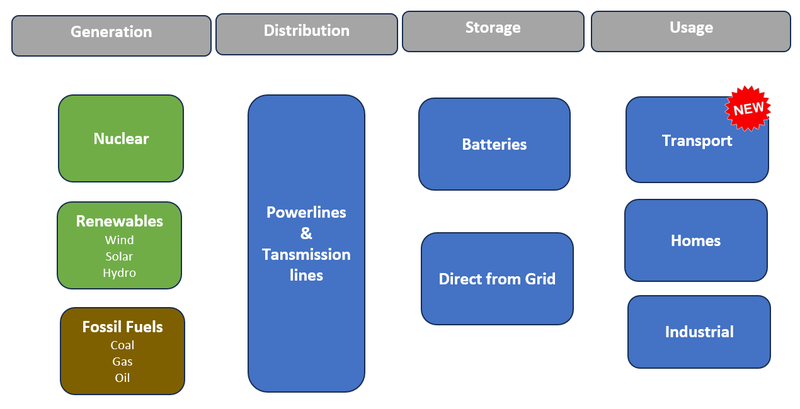

Electrification and a cleaner energy mix can be broadly summarised in this simple diagram, which shows how electricity is generated, moved, stored and used:

We have shown “transport” as a new area of electricity use to reflect the shift to electric vehicles.

Each of the boxes in the image is going to need multiple cycles of capital during the next couple of decades to eventually achieve the move to electrification and a cleaner energy mix.

From the capital markets side, investor attention and capital will cycle in and out of different subsections of the “global electrification” goal.

We are long term holders so we expect to hold through the cycles as they come and go.

Over the last few years batteries and battery metals have captured investor attention as the first cab off the rank in the energy transition.

Capital flowed aggressively into battery metals companies, allowing them to progress battery metals projects - we hold many investments across battery materials like lithium, graphite, nickel and manganese.

Lithium and nickel appear to be taking a breather for the moment as spot prices go through a period of weakness - possibly due to temporary flooding of spot markets by China and Indonesia respectively to maintain their top exporter positions.

Graphite sentiment has been increasingly positive over the last few months and looks like it may be entering its time in the sun this year.

Fossil fuels are coming off a long period of underinvestment, with many having over estimated the speed with which renewable energy would come online as a replacement.

Nuclear energy is suddenly having a run of positive sentiment and we expect capital to cycle into uranium projects in the near term and hopefully into the medium term as well.

And once all these new energy sources come online and electric cars make up more of the global fleet, existing power grids are going to need an upgrade and new transmission lines will need to be built - that’s going to need a lot of copper and steel (iron ore).

It’s hard to pick when and for how long sentiment and capital will cycle into a particular segment of the energy transition, so we maintain long term positions across all segments of the “electrification” thematic.

We fully expect capital to cycle in and out of the different areas as and when sentiment dictates.

Electrification to drive a multi-decade commodities supercycle

Whether it is control over food, water, oil or gold - the nations that control the supply of in-demand resources gain power and status in the world order.

Decades of under-investment in new mines for commodities has created fragile and heavily concentrated supply chains all over the world.

Think of Europe's dependence on Russian gas...

Or the world’s dependence on Chinese processing power for the entire Electric Vehicle supply chain.

The green energy revolution has exposed how unprepared the world is to meet the raw-materials demand of a world transition towards clean energy.

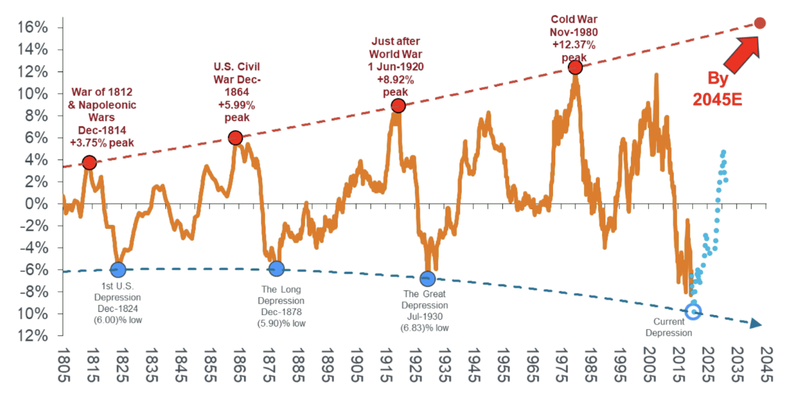

This is what we think is the main driver for a “Commodities Supercycle”.

Commodities supercycles have happened in the past:

- US industrialisation - Late 1890s through to a peak in 1917 - the US was rapidly industrialising, and the supercycle peak coincided with the entry of the US into World War 1 - it continued until the early 1930s.

- World War and the rebuild - The next supercycle began in the lead up to the Second World War. The war itself and rebuilding in the aftermath required lots of materials - it peaked in 1951, and this demand continued through to the early 60s

- Cold war and Nationalisation - The early 1970s marked the start of the third cycle as commodity supply was disrupted as the Cold War saw countries nationalise industries and foreign investors pulled out. In the mid 1980s producers managed to shore up supply and the cycle faded.

- China Industrialisation - The most recent supercycle started in 2000 when China joined the World Trade Organisation (WTO) and started to modernise. The raw materials China needed to do this sparked a long bull run for commodities. The 2008 GFC put a spanner in the works but Chinese stimulus made the cycle continue through to 2014 when oil cratered on oversupply.

AND now...

We think the world has entered a whole new commodities supercycle based on a single macro thematic: The “clean energy transition”.

Source: Forbes: Are We About To Enter A Commodity Supercycle?

The four components of the Electrification supply chain

At a very high level “Electrification” has four key parts:

- Generation - how the energy is made.

- Distribution - how the energy is moved from generation points to consumption points.

- Storage - how the energy is stored before being used.

- Usage - how the energy gets consumed.

All four components come together to form the supply & demand functions for the thematic.

The first wave of capital flowed into “Storage” and “Usage”

For the last ~3 years, the capital markets have focused on supply chains for “usage” and “storage”.

The poster child for this is electric vehicle batteries.

Investors and governments around the world put their money on batteries to perform the storage function (batteries get charged) and facilitate the consumption function (batteries get depleted).

Investment capital concentrated on battery metals, things like - nickel, copper, cobalt and of course lithium.

Prices for all of these commodities went on a run, and the commodities with the least developed markets went for the strongest runs...

Lithium, which was one of the least developed, saw its price go up by over 10x, and the share prices for companies in the sector went exponential.

We hold quite a few Investments across the battery metals space.

A few of them have already paid off delivering us 10x returns in that timeframe, and of course, we had a few in our Portfolio that didn't quite work out for us - mainly around “early stage” exploration, which is par for the course.

The most important takeaway for us was to have exposure to the “storage” and “usage” thematic as the capital inflows and government support eventuated.

While nickel and lithium in the “storage” and “usage” part of the electrification thematic are taking a breather for now, we think nickel and lithium will have their moments again soon so we continue to hold these Investments.

We are currently looking at a couple of later stage lithium stocks (in construction OR producing) that have been beaten down by negative sentiment, and may look to take position in anticipation of a quick reversal in sentiment.

Keep an eye out for a turn upwards in the lithium spot price - that will be the first step for a turn in sentiment.

Battery material graphite, on the other hand, appears to be just about to deliver the “price run that hasn’t happened yet”.

Capital is currently flowing into Generation

Over the last ~6 months the uranium price has doubled, and share prices for some uranium stocks are trading near all-time highs.

The reason?

Governments, companies and investors have made a commitment to reach net zero emissions.

As coal projects are wound down, another source of energy is needed - particularly if the world is electrifying at a rapid pace.

And having a majority fleet of electric cars defeats the purpose if they are powered by electricity created by power plants burning fossil fuels.

Energy prices are moving up, and governments cannot bring online renewable energy fast enough to meet the impending demand shortfall.

Enter nuclear power.

Nuclear power (which is generated using uranium) is one of the cleanest, most affordable forms of baseload energy generation.

Even after almost a decade of investments in wind and solar, governments have realised that these new energy sources require massive amounts of resources, land and ‘grid rewiring’ to bring them online.

This all takes time.

Also, the volatile nature of energy generation by wind and solar power means that they need to be coupled with large amounts of energy storage to be a viable baseload solution.

We still think that wind and solar have a strong place in the future energy mix, but nuclear is presenting as a very attractive and reliable option for base load power.

At COP28 in Abu Dhabi this year 22 countries committed to tripling their nuclear power by 2050.

We expect this number to grow next year.

Almost out of nowhere, the mainstream focus turned to nuclear power and uranium supply.

The spot price for uranium continues to run, and Kazatomprom (who supplies 40% of the uranium market) has flagged near-term uranium supply shortfalls.

Right now we have three uranium Investments in our portfolio, GUE, HAR and GTR. We wrote about each of these companies this week, more on that later.

~80% of the world’s power is generated using fossil fuels, and in order to meet the ambitious net zero goals over the next 20 years, more clean energy will need to come online.

Nuclear will play a part.

Solar & wind power will play a part.

Energy storage will play a part.

And, contrary to popular belief, fossil fuels will play a part.

Fossil fuels are energy dense, and there is existing infrastructure in place to get energy from fossil fuels to the market.

We continue to hold positions in oil & gas explorers, and are looking to add more.

Fossil fuels are an efficient solution to meet energy demand - but they are not considered “green”.

So, our view is that the current wave of capital pouring into uranium is because the problem most immediately anticipated is “clean power generation”.

EDUCATION: Here is a short 10 minute video explaining how fossil fuels, nuclear and renewables generate electricity (it’s pretty old but a good, quick explainer):

Although the spotlight has moved from energy transition metals that target “usage” and “storage” like lithium, nickel, manganese and cobalt - we think it is just a matter of time before they return to the limelight.

For us, our overarching bet is that this energy transition will require A LOT of new mines to come online in the next ten years.

And this is why we have a diversified Portfolio of small cap commodity juniors that give us exposure to a range of minerals across “Usage”, “Storage”, “Generation” and “Distribution”.

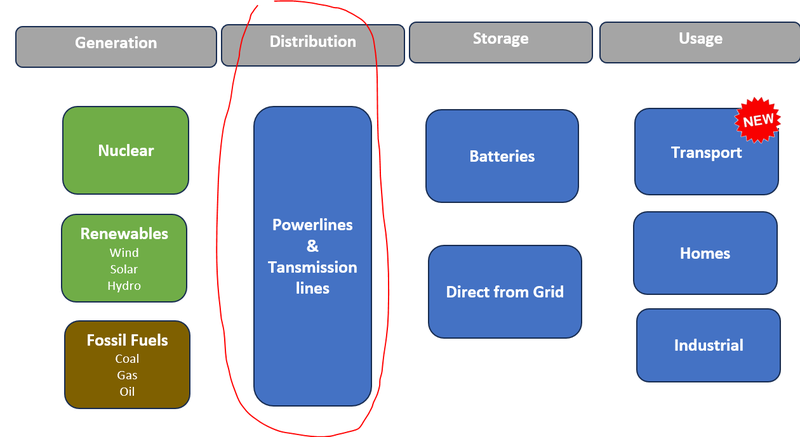

Where does capital flow next? Distribution?

Everyone wants to know what commodity will be in the spotlight next, first it was lithium and now it appears to be uranium.

We try to make bold predictions in this newsletter, so let’s see if we can predict where capital might flow next.

One possibility is that the next wave for the electrification revolution will be “transmission”.

Even after “Usage”, “Storage” and “Generation” see massive capital inflows, there is still a major limiting factor along the supply chain.

More electric cars on the roads, means more batteries to charge them, that all will need to be linked up to the grid...

New renewables projects like solar and wind, will need to be “rewired” to get energy to end users.

Solar farms aren’t built on top of coal mines, the transmission infrastructure doesn’t yet exist.

That’s why we think the “transmission” sector will need to see massive investment at some point over the next decade.

Things like copper for wiring transmission lines and iron ore for new infrastructure will be the big winners of the “transmission” phase of the global energy transition.

The hardest thing to predict is when all of this happens...

Our approach is less based on timing and more about finding the hidden gems that have high quality projects with exposure to these sub thematics.

Ideally, once the narrative and sentiment shifts, the company will be ready with a project to develop.

...and we already hold a position.

One commodity we are currently underinvested in BUT are actively looking for new Investments is copper...

Copper got some attention during the “Usage” and “Storage” boom but we think its superstar moment will come when “transmission” is all the market wants to talk about.

If you know any good copper stocks please respond to this email. We read all of the responses.

Everything is cyclical, but we think for the next decade at least it's all about energy - and this week we talked a lot about the energy commodity of the moment - uranium...

What we wrote about this week 🧬 🦉 🏹

Haranga Resources (ASX: HAR)

HAR added to its exploration portfolio in Senegal finding two new uranium anomalies worth drilling where soil samples had ~7x background uranium levels.

With uranium companies in favour right now, HAR is being led by Peter Batten who some may recall led the “best performing company on the ASX” in 2006 during the last uranium bull run.

We are hoping he can do the same thing again with HAR.

Read: HAR finds two large uranium anomalies, drilling and assays next

Global Uranium and Enrichment (ASX: GUE)

The US government just released a tender called High Assay Low Enrichment Uranium (HALEU) - the type of uranium that powers small modular nuclear reactors.

With the uranium spot price soaring and the US government looking for enriched uranium supply we think GUE finds itself in a good position...

Especially considering GUE is one of two companies on the ASX with uranium enrichment exposure - second only to $1.1BN Silex.

Read: Uranium Bull Market? GUE Aiming to Enrich

GTI Energy (ASX: GTR)

This week GTR announced a new “President of US Operations” - Matt Hartmann - a 20 plus year uranium veteran, with significant experience in ISR projects in the USA - including in Wyoming.

Matt held senior technical roles with many uranium companies, including the $20BN New York listed Cameco - the world’s biggest publicly traded uranium company.

With the Uranium spot price surging and the US scrambling to build out local supply chains we think Matt’s appointment can go a long way for GTR as it looks to drill its projects in Wyoming.

Read: GTR appoints USA Uranium expert to lead USA operations - good timing

Quick Takes 🗣️

GUE gets key permit ahead of busy 2024

KNI presents in front of Norwegian Parliament

PRL Completes PFS, Updates Project Timelines

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.