WRM Receives Further Backing: Sandfire Pours More Millions into Red Mountain Project

Published 16-JUL-2019 10:57 A.M.

|

10 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

For the second time in six months, the $1.1 billion capped Sandfire Resources (ASX:SFR) has had an acquisition crack at MOD Resources (ASX:MOD) and this time, it looks to have stuck.

The Karl Simich led Sandfire announced a $166 million agreed scrip-and-cash takeover of copper explorer MOD in late June, following a failed bid in January that would have given the junior a much greater value than its then $55 million market cap.

MOD is now capped at around $127 million. It has been biding its time, growing its value and waiting for Sandfire to come back with a bigger offer.

It was a smart play, because it knew Sandfire wasn’t done — the mining giant has a soft spot for well-performing ASX juniors, or at least those with high expectations and great underlying assets.

White Rock Minerals (ASX:WRM) is in that category and Sandfire has shown continuing interest.

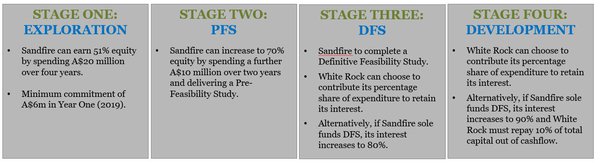

Sandfire has entered a joint venture (JV) with WRM, with the pair conducting an exploration program at the globally significant Red Mountain high-grade zinc and precious metals VMS project in central Alaska.

The billion capped Sandfire is providing the funding for the project which amounts to A$20 million over four years ($6 million in 2019) to earn a 51% interest. This can increase to 70% following the delivery of a further $10 million along with a Pre-Feasibility Study (PFS). This investment immediately puts a healthy valuation on this Alaskan asset, currently owned 100% by White Rock.

Sandfire obviously sees a great deal of upside in Red Mountain, because it has just upped the ante, committing another US$1.5 million (~A$2M) on top of the A$6 million for 2019, taking total exploration budget for this year to A$8 million.

That is the strongest endorsement of the district-scale potential of this project that you can get.

Red Mountain is said to hold a substantial resource, with two high grade deposits containing an Inferred Mineral Resource of 9.1 million tonnes at 12.9% zinc equivalent (ZnEq) for 1.1 million tonnes of contained ZnEq.

Drilling is currently underway, as WRM and Sandfire focus on testing new targets with the potential to yield a significant discovery that will support a greenfields development scenario.

The Red Mountain project looks to be going from strength to strength, so let’s catch up with all the latest news from...

Share Price: $0.007 (as at July 15)

Market Capitalisation: $11.46 million

Here’s why I like WRM:

All systems go

Drilling commenced at White Rock Minerals’ Red Mountain site in late May, following the completion of the company’s first ever modern high powered airborne EM survey over its 475km2 strategic belt-scale regional tenement package.

Red Mountain is certainly in a good location: it is close to major road and rail access, can be serviced by the mining hub at nearby Fairbanks and it has no community or environmental legacy issues.

It is also important to note that most of this tenement package is underexplored, which is probably one of the reasons Sandfire is in the picture and why WRM is so confident in its exploration program.

Exploration has advanced so rapidly that more than 2000 soil samples and 260 rock chip samples have been collected. A portable XRF device will provide rapid geochemical results, indicating that significant news flow could emerge in the short term.

As one of the highest grade and more significant zinc deposits held by any ASX listed company, I’d expect the emergent news to be pretty strong.

If you would like some background reading, check out our previous articles:

- Sandfire Puts its Money on High-Grade Alaskan Zinc & Precious Metals VMS Project

- White Rock Minerals Triples VMS Zinc Project Area in Alaska with a Little Help from $1BN Sandfire Resources

- New Massive Sulphide Mineralisation at WRM’s Red Mountain High-Grade Zinc Project

- WRM On Verge Of Major Program At Alaskan High-Grade Zinc Project

The first piece of the coming news flood, is based on Sandfire’s growing commitment.

Sandfire commit a further US$1.5 million for 2019

Sandfire has injected an additional US$1.5 million to extend the current on-ground exploration activities into September at WRM’s Red Mountain Project.

This is the first stage of a four stage exploration program that sees Sandfire taking an increasingly large stake in Red Mountain.

As you can see by the chart below, there is a great deal of work to be done, but Sandfire is all in:

The important takeaway from Sandfire’s interest is the upside for WRM and its shareholders. There is plenty of blue sky here based on historic exploration, with a low capital commitment. It is essentially free news flow for the White Rock shareholder as Sandfire use their balance sheet on White Rock’s Alaskan asset.

Sandfire’s additional investment by the group is an acknowledgement of the quality of the project, perhaps more specifically its read on what appears to be positive early stage exploration results in 2019.

Given its interest in these results, perhaps a MOD type takeover of WRM is in the back of SFR’s mind. It is to be noted that Sandfire has form here – they moved to 70% of its joint venture partner Talisman in 2018 before taking that asset over for $70M last year. As WRM is the manager of this year’s program, it will allocate funds to extend drilling by a further five weeks to allow a number of new high priority targets to be drill tested.

Drilling is focused on testing new targets defined from the ongoing field activities that include geological reconnaissance, surface geochemistry and modelling of the recent 2019 airborne electromagnetic (EM) survey.

The increased funding will also facilitate additional geological reconnaissance, surface geochemical sampling and ground electrical geophysics surveys across the 475 square kilometre strategic land package, identifying new priority targets for drill testing in 2019 and subsequent field seasons.

This should allow follow-up modelling and interpretation of airborne EM targets to assist in drill hole targeting and the continued use of down hole EM surveys.

Highlighting the significance of the additional funding, White Rock’s managing director, Matthew Gill said, “The additional US$1.5 million committed by Sandfire, over and above the A$6 million already committed for the 2019 field season, is a strong endorsement of the quality and potential of the strategic land holding we have and the targets being generated for drill testing.”

Positive early-stage exploration

We mentioned above that recent drill results may have fast-tracked Sandfire’s interest, so let’s take a more detailed look at these results.

On 24 June, WRM reported that summer field exploration activities, which had commenced in late May, had progressed rapidly with more than 2000 soil samples and 260 rock chip samples collected and significant news flow to come.

Importantly, White Rock has a portable XRF device to provide rapid geochemical results, indicating that significant news flow could emerge in the short term.

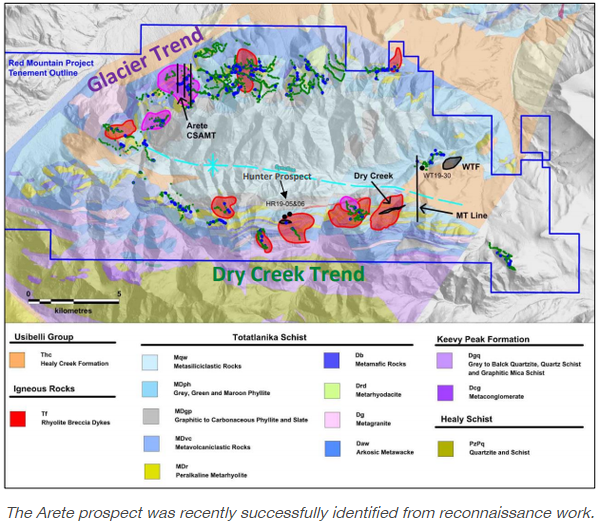

The big news from the current exploration program comes from prospecting of the Glacier Trend, a spatially extensive alteration zone with 10 kilometres of strike.

This Trend has identified sulphide accumulations, chert and iron formations, all believed to be proximal to horizons prospective for base metal rich massive sulphides along strike and down dip.

Work is now proceeding to identify drill targets with initial ground electrical geophysics (CSAMT) to define conductivity features having commenced with three lines completed at the Arete prospect as seen in the map above.

You can read more about it in this Finfeed article.

Drilling of the Arete and other targets along the Glacier Trend is due to commence shortly.

There’s a lot to like about Red Mountain. Deposits remain down dip and in some places along strike, which could lead to resource increase potential. There is also high grade zinc and silver VMS potential from identified targets surrounding known Red Mountain deposits within a large stratigraphic tenement package.

Finally, the Sandfire investment is an enormous endorsement of the quality and potential of the project.

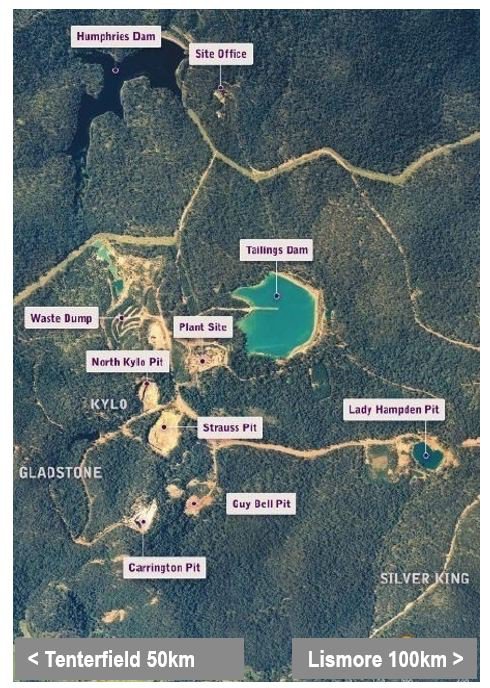

Red Mountain alone is a reason to consider WRM in your portfolio, but there’s also a lot going on at its Mt Carrington gold-silver-copper Project in northern New South Wales.

Climb every mountain

Whilst the recent focus has been on Red Mountain, WRM’s Mt Carrington Project is ticking along nicely in the background.

This development project has an advanced PFS and a maiden JORC Reserve and offers a reduced timeline to gold and silver production. The JORC Mineral Resource is 340,000 ounces gold and 23.2 million ounces of silver, whilst the maiden JORC Ore Reserve is 159,000 ounces of gold.

The PFS shows that gold will be mined first. The maiden Ore Reserve of 159,000 ounces, a production rate of 1,000,000 tpa, gold production of 35,000 ounces and total gold produced of 148,000 oz gold over the first four and a half years all lead to these impressive sums:

As with Red Mountain, there is key infrastructure in place (valued at ̴A$20M) at Mt Carrington and a reduced CAPEX, which reduces development risk, timeframe and cost. The project will be developed in two stages: stage one will focus on the Strauss and Kylo Gold deposits and stage two will focus on the Lady Hampden and White Rock silver deposits.

Then there is its net Present Value (NPV) which comes in at the ~A$60 range assuming the current gold price of >A$2000 per ounce:

The steady incline in the numbers above are impressive, but what stands out is this project has a one year payback and significant potential upside with silver adding another two-to-three years’ mine life. And further, the Gold First Stage only considers two of the four JORC resources to be mined, so there is the potential for more gold to follow also.

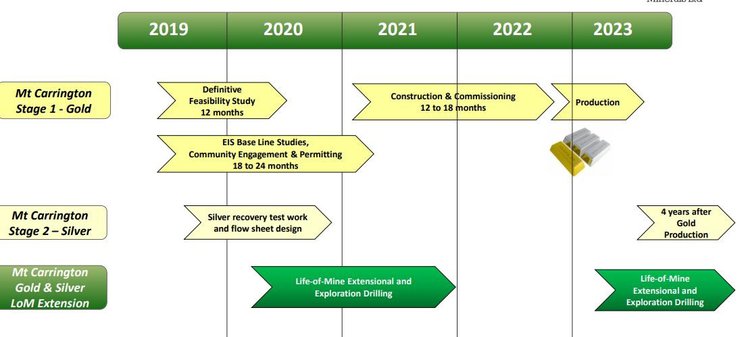

Production will occur in two stages, with stage one focusing on gold (subject to funding). Stage one goals are to complete the DFS by 2020, conduct baseline studies and submit the EIS in the same time and commence construction and commissioning in 2021.

Stage two will focus on silver — also subject to funding — and will include beginning the silver project mining plan, recovery and test work, concentrate sales discussions and completion of the flow sheet design.

Again, there will be plenty of news flow to come from this project.

Here’s a look at the Development Plan for Mt Carrington:

As you can see, all roads lead to gold production in less than three years.

In essence, Mt Carrington offers over 180km2 of highly prospective gold, silver and copper mineralised tenements. It has a larger number of targets, a broad number of mineralised zones and the overall upside looks like this:

The final word

White Rock is a diversified player, playing in two geographically friendly and stable environments.

It has a near development gold asset. A billion dollar partner. And a project in Red Mountain that is in the top quartile of undeveloped high-grade zinc VMS deposits globally.

In this Hot Copper interview, CEO Matt Gill offers his overarching thoughts on Red Mountain and Mt Carrington and what we can expect a few years from now.

However, WRM’s near-term success may very well happen in a shorter timeframe than even its CEO is predicting.

Gill has to be conservative, and to some degree The Next Mining Boom does as well, yet with Sandfire continuing to pour money into Red Mountain and wholeheartedly endorsing this project, a re-rate could very well be just around the corner.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.