Super woes prompt calls for APRA intervention

Published 16-FEB-2017 09:57 A.M.

|

3 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

There’s an ongoing discussion in Australia right now around the poor performance of a number of super funds, with APRA – the Australian Prudential Regulation Authority – indicating that several funds could be forced to merge if to do so would be in the best interest of members.

Lobby group Industry Super Australia claims the financial regulator should make greater use of its powers and push for the change, with its CEO David Whiteley telling The Australian Financial Review that APRA has this capability via a scale test that was introduced in 2012.

The success or failure of these ailing funds is not just the business of members, which is why the discussion is a heated one. With slowing birth rates, and a growing demographic of retirement aged Australians, we could be looking at a very lopsided equation of taxpayers to pension receivers in the years to come.

The last thing the situation needs is for the funds, being faithfully funnelled into by members, to provide poor returns on investments.

APRA’s deputy chairman Helen Rowell said today the body will be ‘honing in’ on the worst 25 of the nation’s 250 largest managed super funds. The association’s advisory team is currently reviewing funds on a range of performance and cost criteria that involves net cash flows, risk levels and the quality of governance as well as asset allocation.

Industry funds still trumping retail

At the same time, industry funds have yet again outperformed their retail rivals according to ratings agencies Chant West and SuperRatings who reported on industry performance for 2016. The numbers show industry funds have not only outperformed retail funds over the year, but also the last decade.

Ms Rowell has commented in the past about super funds ruled by ‘self-interested’ boards, reemphasising the purpose of superannuation which is to benefit members looking to shore up their retirement futures.

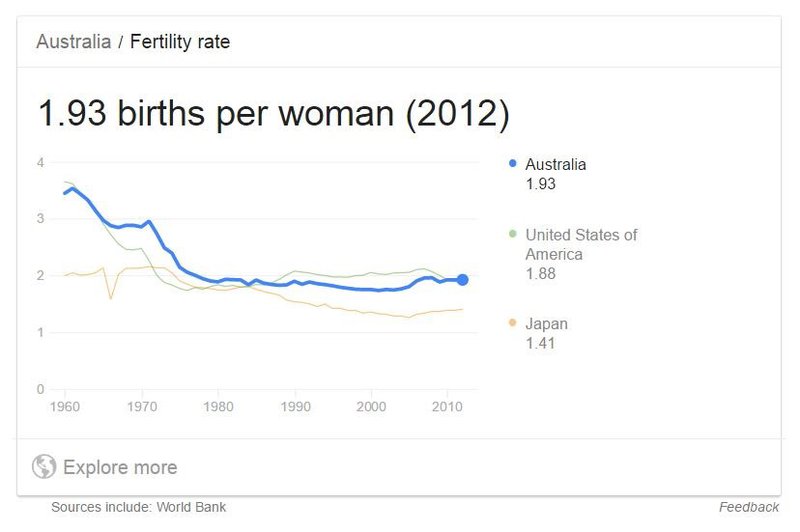

It’s also about working in the country’s interests. As mentioned, Australia’s birth rate has been in decline for decades:

As shown in the graph above, Japan’s rates are even lower than Australia’s and the US. Interestingly, the country finds themselves in the highest debt to GDP ratio for any developed nation – and also in an aged pension crisis.

It was suggested just last month in an article in The Japan Times that as welfare costs go up, some groups are proposing a higher age for the definition of ‘elderly’. That seems a bit like the Australian government shifting the ‘poverty line’ so that it can then claim there are less impoverished people. Problem solved – or not.

As Vern Gowdie wrote late last month in The Daily Reckoning, the risk is that the “base is not going to be strong enough to support the apex”.

In other words, there’s a chance that ‘pension overpromise’ will meet a structural shortage of taxpayers to fund it.

Smaller underperformers pack a punch

According to APRA, there are a number of smaller super funds in Australia which are haemorrhaging money and losing members.

Consultancy Chant West estimates there are about 80 funds with less than $5 billion in the tank that could fail to meet the regulator’s scale test. That’s a lot of potential disruption.

Complete failure of a super fund is a lot more catastrophic than simply a business going bust. For members impacted, the loss is to their entire life savings. Given that the older your age, the more difficult it is to earn income, these situations are likely to cause lasting financial wounds. And accordingly, a greater reliance on the government pension.

Not only would that scenario hurt in real terms, it could also put a dangerous dent in consumer confidence in the super system – something which consecutive governments have worked hard to cultivate.

There are examples of funds considering mergers already, with Rio Tinto’s staff superannuation fund holding advanced discussions with Equip Super to create a $14bn industry fund – which could see fees reduced by 0.15 per cent. APRA’s figures put Rio’s MySuper fund at a loss of 6 per cent of its members last financial year.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.