Still enough cash for a coldie: check into Redcape Hotel Group as our ASX stock of the week

Published 05-JUN-2020 12:07 P.M.

|

6 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

With the hospitality sector ready to kick back into gear, it is a good time to look at some stocks in the sector, particularly ones that have been sold down heavily where there is scope for significant share price upside.

Without there being barely a plane in the air and boarders still closed, travel stocks have already rerated strongly.

While Flight Centre’s (ASX:FLT) shares have been sold down heavily from about $40.00 to $10.00, in less than three weeks it has bounced 40%.

Webjet (ASX:WEB) was also hard hit, yet in the last month its shares have climbed 60%.

This demonstrates how one has to be ahead of the curve in terms of identifying stocks that are likely to be coming out with positive news rather than waiting for that news to hit the deck.

I am looking specifically at the hospitality sector this week.

No doubt the reopening of swanky restaurants will draw plenty of media attention, but my focus is on pubs as I see this sector as much more resilient and perhaps more in line with the spending capacity of consumers following the COVID-19 fallout.

Some people may have lost their jobs, while others have been on limited income for a number of months, but a reasonably priced pub meal with a few beers is more likely to still be within their budget than dining at an upmarket restaurant.

A sector that is back in favour

There has been noticeable support in the sector over the last two months with shares in the leading player ALE Property Group (ASX: LEP) rebounding 30% to $4.88.

ALE Property Group (ASX: LEP) is the owner of Australia’s largest portfolio of freehold pub properties.

As a Real Estate Investment Trust (REIT) group, LEP is geared for consistent returns in the form of distributions rather than delivering substantial share price growth.

The company generates income from rental returns rather than operating the pubs and having earnings directly linked to the financial returns generated through its operations.

This provides reliable and predictable income with regular rent reviews built into contracts in order to keep pace with CPI growth.

Because of its income predictability, LEP is well-suited to safe haven investors, but I am looking for a company that has the capacity to generate both share price growth and a reasonable dividend stream.

To this end, I am targeting a company that captures all of the revenues generated from a pub’s operations in the top line, and then through good management achieves organic growth, minimises costs and optimises margins, resulting in earnings and dividend growth.

Potential upside catalysts in the industry can include the acquisition of new pubs and the development of existing freehold land in order to generate additional revenue streams.

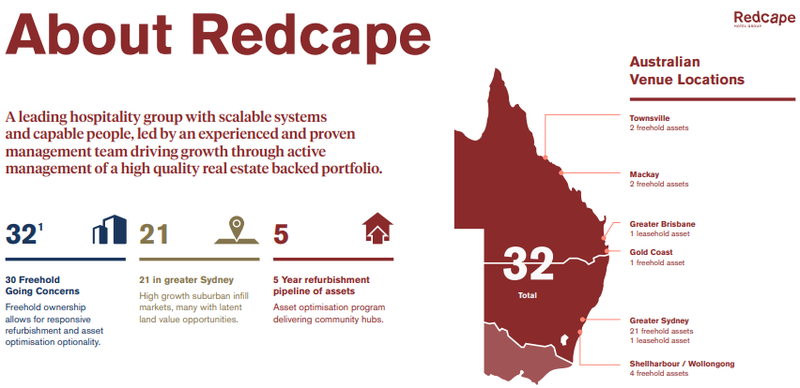

On this note it is important to understand the benefits of freehold versus leasehold.

With the former, as the business owns the land, buildings, work in progress and operational entitlements, there is scope for expansion such as converting part of the car park into an outdoor entertainment area.

My stock of the week is Redcape Hotel Group (ASX: RDC) a company that has 32 hotels in New South Wales and Queensland, 30 of which are freehold businesses.

Ten weeks downtime put to good use

While the company closed all of its pubs in line with COVID-19 restrictions, the group’s 16 bottle shop outlets and accommodation at two of its hotels were able to remain open.

However, as of June 1 the majority of Redcape’s venues have reopened, and the word from management is that the downtime has been put to good use in terms of undertaking renovations, making operational changes and upgrading systems.

As Redcape generates income from the sale of beverages and food, as well as gaming it takes an experienced management team to manage all facets of its operations.

Redcape was fortunate in that it had $100 million in cash on hand as the shutdowns started.

At the time, management estimated that cash expenses associated with maintaining the business were approximately $10 million per quarter, but importantly as the owner of most of its businesses there was little to be concerned about in terms of commitments to third-party landlords.

The pubs were closed for approximately 10 weeks, suggesting that the cash burn for Redcape should have been less than $10 million, leaving it cashed up to continue to grow the business and perhaps take advantage of some stressed sales within the industry.

Portfolio shuffle strengthens balance sheet

The company was tracking well leading up to downing tools, having completed the sale of the Royal Hotel in Granville for $51 million (a premium to book value) and acquired Kings Head Tavern, South Hurstville for $27 million.

Only a fortnight before shutdown, management had reaffirmed its full-year distribution guidance of 9.2 cents per share, having already paid 4.8 cents for the six months to December 31, 2019 which represented an 11% increase on the previous corresponding period.

While the second half distribution will either be trimmed or perhaps cancelled to strengthen the balance sheet, a return to normal distributions could be expected in fiscal 2021.

If they are to be in line with fiscal 2020 guidance this would imply a yield of 11.2%.

As a guide though, while there is limited coverage of the company, the latest broker projections are for a fiscal 2021 distribution of 7.2 cents, representing a yield of about 8.8%, still a very healthy return in a low interest rate environment.

It is worth noting that the average dividend yield across the sector based on fiscal 2021 projections is 5.3%.

Achieving strong organic growth and improving margins

There was plenty to like about the company’s interim result with operating underlying earnings up 19.8% on the previous corresponding period and margins increasing from 22.7% to 24.1%.

Organic growth was evident with like-for-like revenue up 6.2% compared with the six months to December 31, 2018.

The portfolio valuation as at December 31, 2019 was just over $1 billion, suggesting the company’s enterprise value of about $360 million is well short of fair value.

On this note, the net assets per stapled security as at December 31, 2019 were valued at $1.15 per share, implying a premium of more than 40% to the company’s current share price.

This not only suggests there is scope for significant share price upside, but the group could come under the spotlight as some of the larger players in the sector look to snare and acquisition at a discount price.

However, even if this were to eventuate it is a fair bet that any suitor would be paying a substantial premium to the company’s share price.

Even setting corporate activity aside as a potential share price catalyst, this will be a stock to watch in August when it releases its full-year result and most likely provides guidance for fiscal 2021.

It will be then that investors crunch the numbers and perhaps gain an appreciation for where the company should be trading to reflect fair value.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.