Prairie Mining surges nearly 30% following Debiensko Scoping Study

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Shares in Prairie Mining (ASX: PDZ – LSE:PDZ) spiked substantially on Thursday morning after the company released the results of a Scoping Study in relation to its Debiensko coal project located in the south-west of the Republic of Poland.

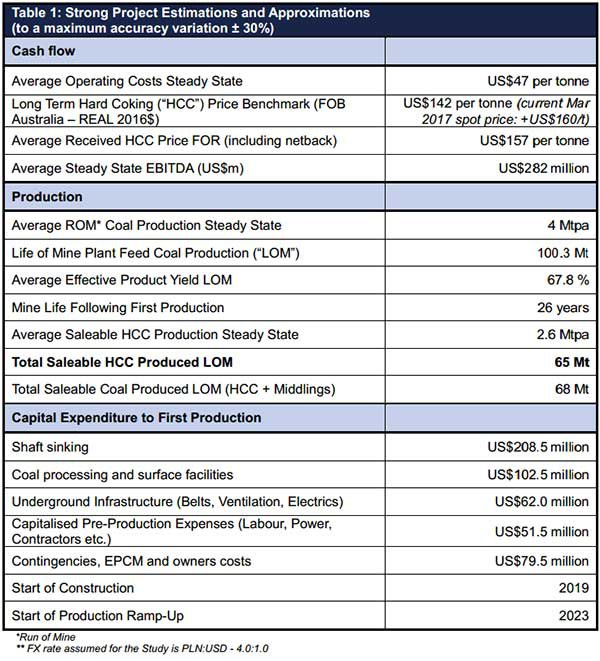

The study pointed to the prospects of developing a large-scale, low-cost, long life premium hard coking coal project which could generate annual EBITDA of up to US$282 million over a mine life of 26 years.

PDZ’s share price increased from the previous day’s close of 47 cents to hit a high of 60 cents in the first 15 minutes of trading, representing an increase of 28%. By midday it had settled in a range between 55 cents and 57 cents, still making for a substantial increase, and also representing a near three-year high.

It should be noted that this is an early stage stock and share trading patterns should not be used as the basis for an investment as they may or may not be replicated. Those considering this stock should seek independent financial advice.

With quality, low-cost, long life hard coking coal projects located in stable jurisdictions difficult to come by it wouldn’t be surprising to see PDZ continue to trade strongly, particularly given there is the prospect of corporate activity from global players with nearby operations.

Debiensko to benefit from premium coal quality and proximity to end markets

PDZ’s Chief Executive, Ben Stoikovich, highlighted the key takeaways of the Scoping Study in saying, “The Scoping Study results confirm Debiensko’s potential as a Tier 1 premium hard coking coal asset by virtue of the significant potential production scale and resource size, exceptionally low estimated cash costs and low capital intensity of the mine”.

Another key factor that Stoikovich pointed to was the fact that the project has existing rail, road, power, water and other mine infrastructure already in place.

Debiensko will also have pricing power with its premium hard coking coal comparable with internationally traded benchmark hard coking coals. Stoikovich is of the view that there is the potential to obtain significant pricing premiums against imported seaborne coals owing to transport advantages of some US$15 per tonne.

Heavy industrial activity in the Central European region creates substantial demand for hard coking coal, which should work in PDZ’s favour. Based on PDZ’s data, Europe consumes 47 million tonnes of hard coking coal annually with 85% currently imported.

Debiensko offers strong cash flow, low costs and long mine life

Life of mine saleable hard coking coal production is estimated to be 65 million tonnes. Estimated steady-state cash costs are an extremely attractive US$47 per tonne. The group has the benefit of leveraging off existing infrastructure at the Debiensko mine site, and it is important to note that permitting is already in place.

As a backdrop, the mine was originally opened in 1898 and was operated by various Polish mining companies until 2000 when mining operations were terminated due to a major government led restructuring of the coal sector caused by a downturn in global coal prices.

In early 2006, New World Resources plc acquired Debiensko and commence planning to comply with Polish mining standards with the aim of accessing and mining hard coking coal seams, and in 2008 a 50 year mining license was granted.

PDZ has been quick to move on progressing this venture having only acquired it in October 2016. The company’s strategy has been aimed at revising the development strategy in order to potentially allow for early mining of profitable premium hard coking coal seams, whilst minimising upfront capital costs.

The fact that Debiensko is a former operating mine and is in close proximity to two neighbouring coking coal producers in the same geological setting reaffirms the significant potential to successfully bring the mine back into production.

Commenting on capital expenditure, Stoikovich said, “Leveraging off existing infrastructure at the Debiensko mine site potentially results in exceptionally low capital intensity of US$197 per tonne of annual saleable production capacity compared to an industry average of over US$400 per tonne for global hard coking coal mines developed in the last decade”.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.