LNR farms into ground 400m from one of Australia’s largest lithium mines currently being built

Published 06-DEC-2023 10:19 A.M.

|

9 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 55,656,915 LNR shares and 9,250,000 LNR options at the time of publishing this article. The Company has been engaged by LNR to share our commentary on the progress of our Investment in LNR over time.

Lithium in Western Australia is certainly in the spotlight at the moment.

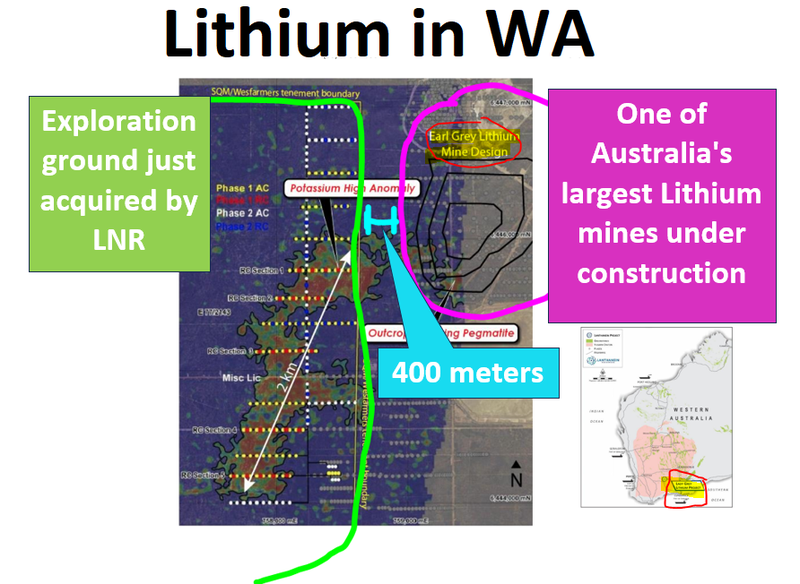

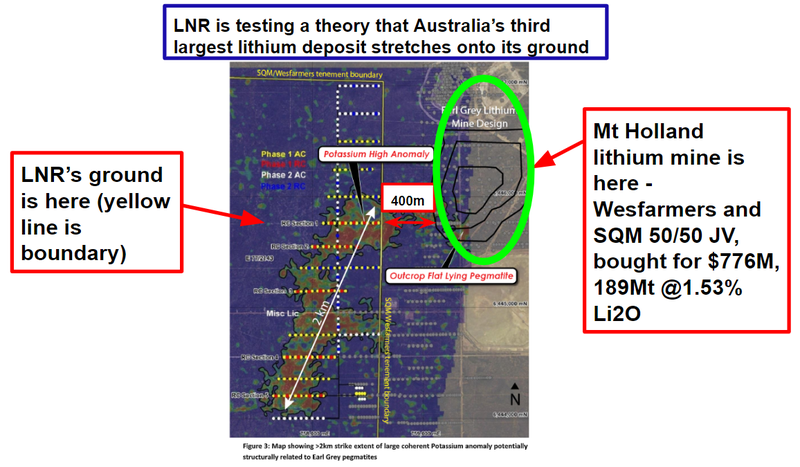

Our Investment Lanthanein Resources (ASX:LNR) has just farmed-in into lithium exploration ground that is 400m away from the giant 189Mt @ 1.53% Li2O Earl Grey lithium deposit.

A deposit where they are currently building one of Australia’s largest lithium mines, owned 50/50 by Wefarmers and SQM.

This exploration ground is an early stage asset - and we are now looking forward to LNR running the first ever drill campaign on this ground in February/March.

Early stage also means this is high risk exploration, where there is a chance nothing will be found.

We have written recently that we are on the hunt for early stage WA lithium explorers with near term drilling to hold during 2024, in anticipation of what we think could be a consolidation of lithium projects in Western Australia in the medium term.

Preferably exploration near existing deposits or mines (where roll ups are more likely to occur if they do happen).

This is the second WA lithium exploration “roll of the dice” we now have in our Portfolio.

Earl Grey is Australia’s third largest lithium mine (currently under construction), which has 189Mt @ 1.53% Li2O and is jointly owned by Wesfarmers and SQM - the largest producer of lithium in the world.

This deposit was found as a result of drilling for gold - there were no outcropping pegmatites.

And now LNR has exploration ground just 400m away from this deposit, with some lithium soil anomalies and a plan to drill in February/March.

LNR’s Technical Director Brian Thomas is also the Chairman of WA lithium success story Azure Minerals - which has recently been subject to a $1.6BB takeover offer by SQM - so he knows a thing or two about massive lithium deposits and cutting big deals.

So the question that LNR will be drill testing to answer in February/March next year: Do the pegmatites of Australia’s third largest lithium deposit extend onto LNR’s ground?

We may know the answer to that question in just three months.

Today, our microcap exploration Investment, Lanthanein Resources (ASX: LNR) announced it intends to acquire up to 70% of a sizeable swathe of exploration ground directly next door to the Earl Grey lithium mine in WA.

Earl Grey will be the third largest lithium mine in Australia once completed - with first production due in 2025.

LNR has previously had a crack at rare earths - exploration results to date have not set the market on fire, and with the price of NdPr down , it has led LNR to look for an additional project to grow shareholder value.

During its rare earths exploration and afterwards, we held onto ~80% of our LNR position and are well under water on the initial Investment, and are looking forward to seeing what LNR can do with its new lithium asset.

Today’s news represents LNR’s first foray into lithium at a time when the lithium world is very focussed on Western Australia - where billions of dollars are being thrown around for hard rock lithium assets.

We think being next door to a discovery is a good thing, and the market is re-rating exploration companies that fit into this category.

Even better, is being next door to a lithium mine - and the project LNR’s has acquired today is next to one of the biggest - the Earl Grey lithium mine which is slated to begin production in 2025.

Owned by 50/50 by Wesfarmers and the largest lithium producer in the world (SQM), the sale of Earl Grey made Kidman Resources one of the great early lithium success stories on the ASX.

Kidman Resources agreed to sell Earl Grey for $776M in May 2019.

Kidman shares were going for just 12 cents three years prior and that $776M transaction was done at $1.90.

That’s nearly a 1,500% re-rate in 36 months.

But imagine what Kidman could have received in today’s WA lithium market?

The WA lithium market is in overdrive right now - egged on by Gina Rinehart’s enthusiasm to purchase shares in what seems like any major lithium project worth its salt.

The US Inflation Reduction Act (IRA) and Gina have combined to create a market frenzy for lithium projects in WA, even while the lithium price remains depressed.

We’ve seen companies trading at market caps of sub-$5M re-rate to more than $60M off of just good lithium rock chips.

One example of this is Raiden Resources, which hit a peak market cap of nearly $190M after it found high grade rock chips in a tenement next door to the Azure Minerals high grade Andover lithium discovery.

The past performance of these lithium stocks is not and should not be taken as an indication of future performance for LNR. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

At the helm of LNR is Technical Director Brian Thomas who is on the board of BOTH LNR and Azure Minerals, where he is Chairman.

As we noted above, LNR’s Brian Thomas is no stranger to dealing with large lithium transactions - Azure Minerals is capped at ~$1.6BN after an approach by SQM was complicated by none other than Gina Reinhart.

Gina Rinehart climbed up the register of Azure and as of October, controlled ~18% of Azure’s shares - which at the time, threw a spanner in the works of a proposed $1.6BN takeover by SQM (Source).

And now, LNR investors are gaining exposure to this red hot macro thematic.

Again, LNR’s new lithium project is immediately next door to the Earl Grey mine - which is slated to go into production in the first half of 2025.

We do need to note that LNR is a micro cap exploration stock. This is a high risk, high reward Investment. There are no guarantees LNR will find anything of economic value. Its early days in its exploration.

And while the potential of the project is promising, the terms of today’s deal are also reflective of the current market sentiment around WA lithium exploration projects (see risks section, more on this below).

After the dilution from today’s deal LNR will have a market cap of ~$14M (at yesterday’s close price of 0.6c per share).

LNR had $1.6M in cash at September 30, 2023. While LNR is due to receive $500K in cash and $1.5M in shares from another company for the sale of its PNG gold assets - today’s acquisition required a $2M capital capital raise to pay the vendor of the project.

More on LNR’s project next door to Earl Grey lithium mine

LNR has a permit for 193 Aircore and 50 RC drillholes and intends to start drilling between February and March next year.

LNR will be testing a theory that the mineralisation at Earl Grey extends west onto LNR’s ground, and LNR has potassium soil anomalies to help guide its drilling.

Potassium can be seen as a “pathfinder” element which helps explorers find lithium, along with lithium soil anomalies which go as high as 298ppm.

Below you can see the proximity of LNR’s ground, 400m from the Earl Grey mine and the 2km stretch of potassium anomalism which LNR will be testing with the drill bit in February to March of 2024:

We give this project at “3” on our nearology scale:

3. “Even Better” nearology - geographically close AND same geological structures AND supporting exploration work

This is when two projects have the same geology and structures WITH supporting drilling data/geochemistry and/or geophysics.

With these, we like to see either some drill intercepts showing something is where the company thinks it is rock chips in the area pointing at something, or geophysics showing massive EM targets that need to be drilled.

🎓Learn: How to evaluate “nearology” investments

Hopefully, after drilling LNR will hit good lithium mineralisation and prove their theory.

We have set our expectations for this drill program as follows:

What we’re looking for:

Bull case = Grades of greater than 1.5% lithium

Base case = Grades of greater than 1% lithium

Bear case = Grades of less than 1% lithium or no mineralisation is found

What is LNR paying for this project?

LNR has signed a farm-in agreement, where ownership is tied to exploration expenditure.

The more LNR spends, the closer it gets to a total of 70% interest in the project.

LNR is making an initial payment of $1.5M cash to the vendor.

If LNR spends $7M or more on exploration, it acquires a 50% interest in the tenement.

LNR needs to spend $1M on exploration in the first year - with the “start date” being when the initial payment is made.

LNR also needs to spend $3.5M on exploration in the first two years after this initial payment is made.

The vendors must also receive from LNR a $500K cash payment on the one year anniversary from the start date and a further $500K on the second anniversary of the start date.

If LNR decides to pull out of the agreement, a cash payment of $1M must be made to the vendor MINUS all of the exploration spending LNR has done up to that date.

To get to 70% ownership (a further 20%), within 7 years of the start date, an additional $2.5M is due.

LNR will also be paying another company that had an option over the tenement with the vendor ~533M LNR shares.

All up we see this farm-in agreement as reflective of the red hot WA lithium project market - i.e it is a high risk, high reward exploration project.

What’s next for LNR?

🔄 Drilling (February to March)

LNR has a permit for 193 Aircore and 50 RC drillholes and intends to start drilling between February and March next year.

🔲 Assays

This will give us a much better understanding of the project’s potential.

🔲 Heritage approvals for expanded drilling

If initial results are good enough, we expect LNR to seek heritage approvals for additional drilling.

🔲 Soil sampling across other targets

LNR intends to conduct soil sampling to help firm up additional targets across the project.

Risks

Exploration risk - Although LNR has potassium and lithium soil anomalies across its project next door to the Earl Grey mine, there is no guarantee that these correlate to economically recoverable lithium mineralisation. As with any exploration company, there is always a chance that after drill testing its targets, LNR returns uneconomic lithium grades or even no grades at all.

Funding risk - the farm-in agreement is reflective of the market sentiment for WA lithium projects at the moment. Should drilling not be successful, LNR like all small caps may need to raise additional funds to continue its operations which could result in additional dilution to shareholders.

Market risk - market conditions could deteriorate further, impacting LNR’s ability to raise additional capital and/or hurt LNR’s share price.

Commodity price risk - the price of lithium could decrease, hurting the economics of any potential project on LNR’s grounds.

Dilution risk - with the capital raise and vendor payments, once tranche two of the placement settles, LNR could have close to ~2.2BN shares on issue, where it once had ~1BN shares on issue. Additional options have been issued as part of the transaction. The impact on the capital structure from this type of raise and large increase in shares on issue may impact the ability of LNR shares to re-rate in the event of a discovery.

Our LNR Investment Memo

We intend to review our LNR Investment Memo upon completion of the company’s first round of drilling at its new lithium project.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.