Lithium Boom: EMH offtake surely coming soon?

Today we take a look at a deep dive video interview with the CEO of lithium development company European Metals Holdings (ASX:EMH), Keith Coughlan .

We invested in EMH at $1.40 back in March as we are big believers in the European battery metals theme and we reckon EMH must surely be pretty close to announcing an offtake agreement...

You might have heard over the last few weeks — it’s boom-time for lithium.

Joe Biden’s push to switch the US to electric vehicles seems to have stoked a global wave of excitement around lithium companies that provide the critical battery metal.

The ASX’s most well-known and established lithium companies including Orocobre, Pilbara Minerals, and Galaxy Lithium are each at all time highs, while Wise-Owl’s OTHER lithium investment, early-stage German Zero Carbon lithium company Vulcan, has increased by more than 3600% in just over a year.

The market doesn’t seem to have caught on to EMH yet.

We believe we are still early in the lithium cycle. Worldwide, we are facing a supply shortfall of the Electric Vehicle battery-making ingredient for at least the coming decade, driven by surging adoption of EVs combined with lithium supply constraints.

EMH is developing the largest hard rock lithium resource in the European Union, and its flagship Cínovec Lithium Project at an advanced stage of development.

While EMH has no doubt performed well over the past year, the stock is yet to attract the levels of market attention of many of its lithium peers. But the $210 million company has all the hallmarks of a major lithium success story...

You’re best hearing it straight from EHM Managing Director Keith Coughlan.

In the following video, he discusses EMH’s partnerships with ČEZ, Germany's world class EPCM SMS Group, and the company’s planned works over the coming 9-12 months to definitive feasibility study, final investment decision, and financing.

The half hour video is worth a watch for EMH shareholders like OR anyone considering an investment in EMH.

The end to lockdowns (outside of Australia at least) has revealed major pent-up demand for EVs that has taken a hit on surplus supplies of the metal, while governments worldwide — particularly in Europe — are pledging to invest in clean-energy projects .

But the EU has no local supply of lithium, so EMH is racing to become the first local EU battery grade lithium producer to deliver to this emerging local industry.

EMH’s globally significant Cínovec Project is in northern Czech Republic — the epicentre of over a dozen new and planned lithium-ion battery factories and on the doorstep of dozens of potential customers.

EMH shares its Cínovec Project with a majority Czech government owned local partner, the €10BN eastern Europe energy conglomerate ČEZ.

Along with its partner Volkswagen, ČEZ also has plans to invest $2 billion in a new battery Gigafactory that’s just 64km from its Cínovec Project that it shares with EMH.

One of the interesting points made in the video is that a pre-feasibility study (PFS), completed in 2019, valued the project at $1.1 billion (NPV). As EMH owns half the project (CEZ 51%), that’s a ~$550M project valuation to the company. In comparison, EHM is now trading at $1.68 per share for a $218M market cap — that's just 40% of EHM's share of the project's 2019 valuation.

Yet it’s important to note that the project value in the PFS was based on the much lower lithium price at that time, so we can expect a higher project valuation even today.

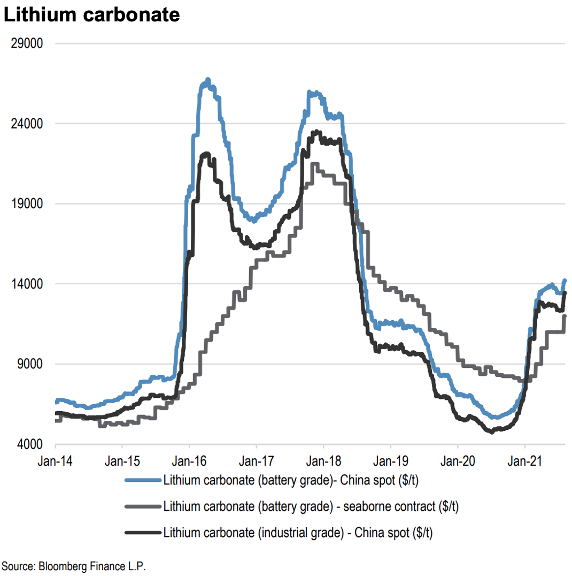

As you can see in the chart below — from a new report from J.P. Morgan on Monday, " Lithium" Raising long-term price forecasts and moving to an Overweight rating on all ASX lithium miners we cover" — lithium carbonate prices are in the early stages of a recovery from the sharp fall of 2018-19.

Over the next few years, J.P. Morgan forecast "prices to equal or surpass the previous cycle highs (reached in 2018) on strong EV sales related demand".

It raised its long-term lithium spodumene price by 31% to $850/t, long-term carbonate price by 11% at $12,250, and long-term lithium hydroxide price by 12% at $14,000/t.

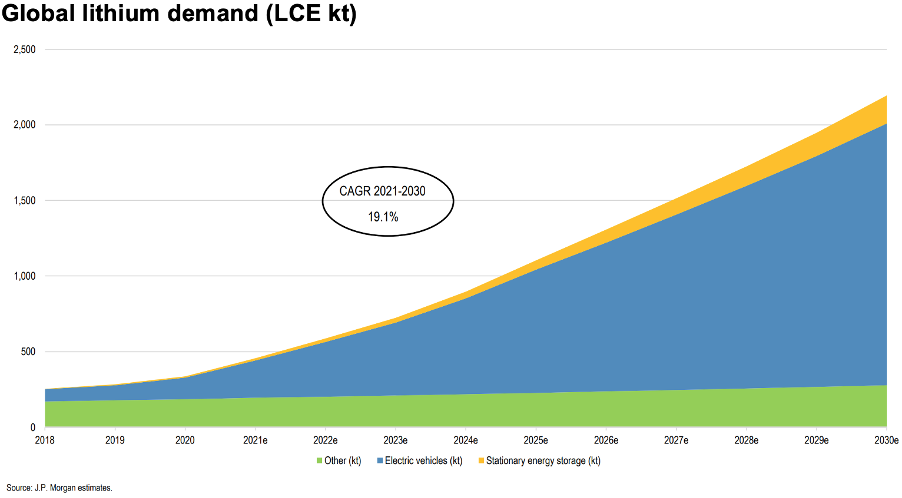

The report saw the bank upgrade the ASX lithium sector, taking the view that there’s not enough lithium to meet demand for the foreseeable future.

The bank says there will be 19% per year increase (compound annual growth rate) in demand for lithium over the coming 10 years to 2030. This is primarily based on rising demand for electric vehicles and batteries and a lack of supply, and it sees "a perpetual deficit visible beyond 2030 until more projects are defined by the industry".

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.