German economy looks stable in 2017

Published 07-DEC-2016 14:37 P.M.

|

5 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

According to Coface, a worldwide leader in credit insurance, the signs for the German economy and for further economic development are promising, with a high level of stability.

This year’s gross domestic product (GDP) is expected to grow by 1.8%, with a marginally smaller rate of 1.7% expected next year. The primary growth driver for 2017 will once again be private consumption, fuelled by the country’s record-high levels of employment. Risks for the German economy could occur on the export side, as a result of cooling down in some of the major target countries for German exports, particularly UK, China and USA.

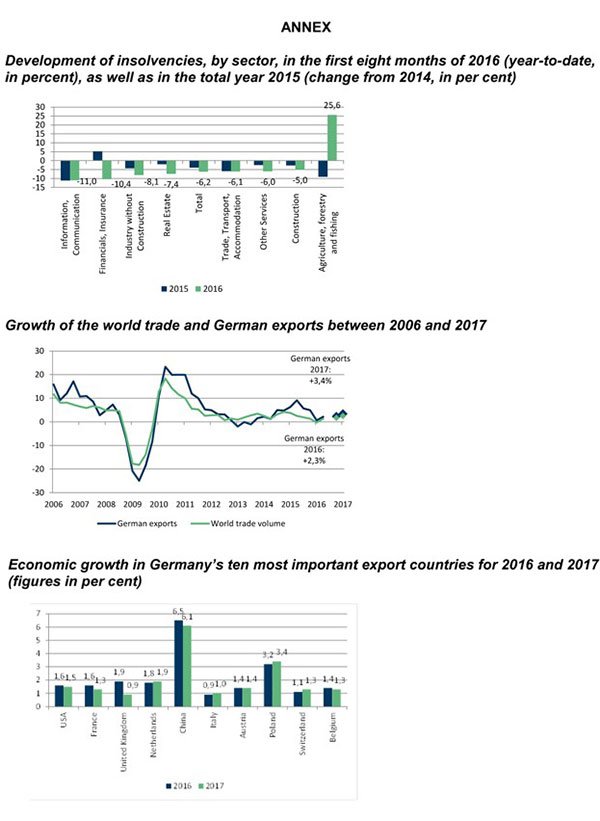

FEWER INSOLVENCIES BUT HIGHER LOSSES

Within this environment, Coface forecasts that the downward pressure on insolvencies will continue, with the fifth year in a row of record lows in 2017 (falling to a volume of around 21,000.) However, this downward trend is expected to continue at a slightly slower pace. After decreasing by 5% this year, Coface forecasts a further decline in bankruptcies by 4.2% in 2017.

Despite the positive outlook, the amount of outstanding claims in insolvency procedures could rise further, as larger companies in several sectors are under increased pressure from competition, costs and profit margins. There are more insolvencies among economically larger companies, such as Steilmann and Unister, despite a decreasing number of insolvencies in absolute terms.

“The stable outlook for the German economy does not mean that companies in Germany will be able to lower their guard in the coming year. There are a number of external risks THAT could particularly affect Germany’s export-oriented economy. In addition, after the reform fatigue of the Grand Coalition, we cannot expect to see new far-reaching economic policy measures from the next government. These uncertainties will dissuade companies from extending their investments beyond manageable limits in the coming year,” explained Dr. Mario Jung, Coface Economist for Northern Europe.

GROWTH RATE OF GERMAN EXPORTS CLEARLY SLOWING SINCE THE SECOND HALF OF 2015

Despite another record year for German exports in 2015, growth rates have distinctly contracted since the second half of 2015. In the first quarter of 2016, the growth of German exports came to a near standstill due to the slight decline in the volume of world trade for the first time since autumn 2010. The subsequent recovery has been far from dynamic. In the first half of 2016, both world trade and German exports were very weak. German exporters recorded a slight upturn in the second quarter, due to the mild growth of world trade.

The outlook for German exports in 2017 is cautiously optimistic and depends on the economic situation in the top 10 target countries that account for about 60% of all German exports. The economic slowdown in four of the five most important target countries will be of particular relevance. For the UK, the third largest target country, Coface expects a massive slump in growth, down from 1.9 to 0.9%, largely due to the Brexit. This is expected to seriously affect German exports. In China, the gradual slowdown in growth is expected to continue – as is the gloom in the USA – now Germany’s most important customer, accounting for a share of around 9% of all exports. France, Germany’s second largest export destination, is expected to suffer from another slight setback in economic growth in 2017.

These negative impacts will be partially compensated for by the slightly improved economic outlook for the remaining countries in the top 10 group, along with clearly higher growth expected for emerging and developing countries – which account for around 30% of German exports.

PRIVATE CONSUMPTION MAIN DRIVER OF ACTIVITY

“The solid growth prospects for the German economy mainly rely on the dynamic pace of private consumption,” explained Dr. Jung. “Private household consumer spending will further accelerate in 2017, to reach a high of 2.0% – up from 1.9% in 2015 and 1.6% in 2016. To put this into perspective, the average growth in private consumption between 2006 and 2014 was just 0.8% and the growth of the German economy mainly relied on net exports,” he continued.

Coface forecasts that these strong dynamics in private customer spending will ensure growth in gross domestic product of 1.7%, by contributing two-thirds (or 1.1 percentage points).

ELECTIONS IN 2017: WILL THE GRAND COALITION COME TO AN END?

The parties of the governing coalition are unlikely to escape unscathed during next year’s elections. According to current surveys, both the Union and SPD parties are scoring lower than the results they achieved during the last parliamentary elections (of September 2013.) They are also below the survey results taken at the turn of the year 2015/2016.

Nevertheless, the overall picture for the future of the Federal Government reflects stability and anything other than a renewal of the Grand Coalition would be a surprise. All available surveys still show that the Grand Coalition has a margin of security to obtain an absolute majority, while there is no majority for any other coalition of two parties. Even a tripartite alliance of the SPD, Left Party, and The Greens, which has been sought by several groups, would have little chance of obtaining an absolute majority.

A smaller Grand Coalition – as well as the likelihood of the AfD being an additional political power in the Bundestag – will hamper political consensus. For the first time since 1953, six parliamentary groups, covering a very broad political spectrum, will be represented in the Bundestag. Moreover, as the leaders (Merkel for the Union and Gabriel for the SPD) are anything but undisputed, the achievement of large reform projects under the next Grand Coalition – including those covering economic and social policy – will become more and more difficult.

These potential risks for political developments in Germany could fuel political uncertainties in the European community, creating an additional drag on consensus-building at European Union level.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.