Francis views ABR as potential ten-bagger

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Former Macquarie and HSBC resources analyst, Simon Francis, has identified American Pacific Borate and Lithium (ASX:ABR) as a potential ten-bagger on the back of its impressive definitive feasibility study (DFS) relating to the Fort Cady (US) project.

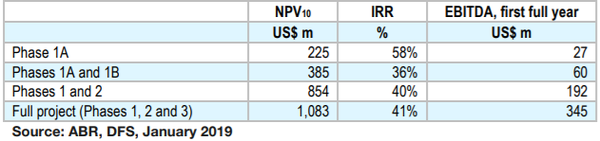

The project boasts a post-tax NPV10 (net present value at a 10% discount rate) of approximately US$1.1 billion.

In January 2019, ABR released a low-capex ‘enhanced’ version of the DFS that splits Phase 1 into two parts, and is now considered ‘base case’.

The DFS is built around the production of sulphate of potassium (SOP) and commercial scale boric acid.

The second stage of development (Phase 1B) should see full production from the 82,000 tonnes per annum Phase 1 boric acid plant.

One of the key benefits of adopting a phased approach is access to early-stage revenues that will assist in funding latter stage development.

Taking this approach will also make it much easier for the company to achieve more modest debt financing, and in the case of raising capital through the issue of shares, the earnings per share dilution will be minimised.

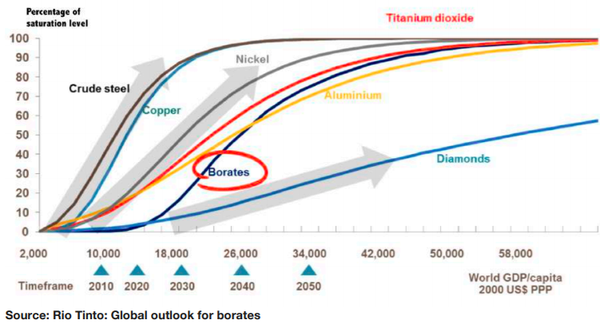

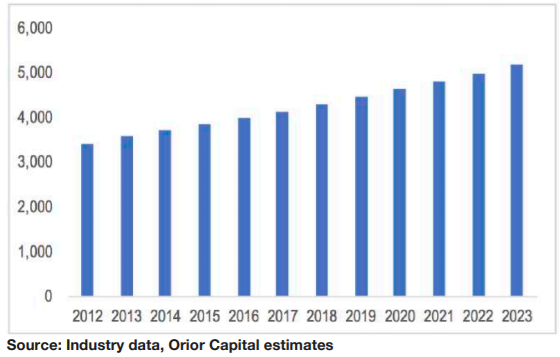

As indicated below, the demand outlook for borates indicates a substantial uptick around the time that Fort Cady comes into production, a level that is expected to continue to grow out to 2050 and beyond.

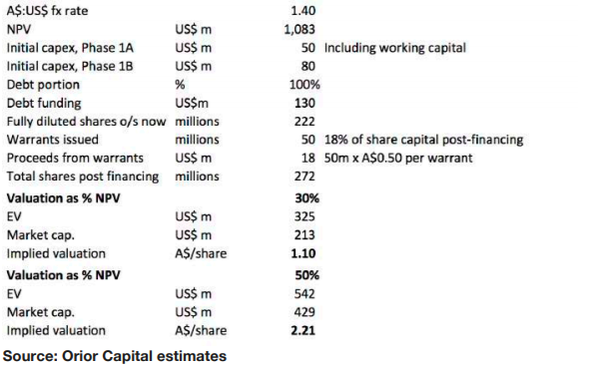

Mid-point valuation of $1.65 per share

Francis’ ten-bagger projection implies a share price of $1.60 relative to Tuesday morning’s opening share price of 16 cents.

Putting this in enterprise value (EV) terms, Francis crunched the numbers on a mix of financing scenarios, projecting that ABR could attract an EV in a range between US$325 million and US$542 million within 12 months.

This would equate to a valuation of between $1.10 and $2.21 per share, representing multiples of between 6.9 and 13.8 relative to a share price of 16 cents.

The following is a valuation based on the January 2019 DFS base case.

The release of a comprehensive report by Francis has evoked significant interest in ABR with the company trading as high as 18 cents on Tuesday morning, up 16% on yesterday’s closing price.

While being able to boast a US$1 billion project is headline-grabbing in its own right, arguably one of ABR’s most compelling investment metrics is its relatively near-term production outlook.

In many cases, large-scale projects involve long lead times, but ABR expects first production from Phase 1A to occur in the December quarter of 2020.

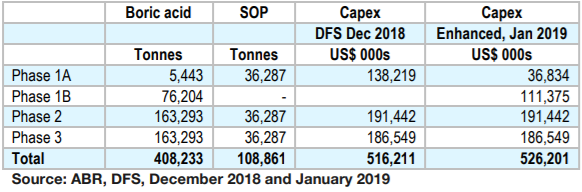

Phase 1A comprises the Phase 1 sulphate of potassium (SOP) line plus a commercial scale boric acid plant. Phase 1B would see 82,000 tonnes per annum Phase 1 boric acid plant at full tilt.

Based on the DFS, phases 1B, 2 and 3 are expected to start two, four and six years after 1A.

ABR to assume prominent global position

According to the DFS, Fort Cady will ultimately produce approximately 408,000 tonnes per annum of boric acid and nearly 110,000 tonnes per annum of SOP.

Francis noted that ABR will become only the second major producer of calcium-based borates globally, and only the second producer of SOP in the US.

Also working in ABR’s favour is the fact that few new projects are in the pipeline, and the borates market is essentially a duopoly with Eti Maden and Rio Tinto controlling 80% of global demand.

Boron and borates are used in many modern applications from abrasives to water treatment, and from soap to nuclear power plants, as well as being a product of need for emerging new age technologies such as devices requiring lithium ion batteries and hydrogen fuel cells.

The global market for boric acid (H3BO3) reached 3.9 billion tonnes in 2017, with the market expected to continue growing at approximately 4% per annum.

Borates demand is being driven by the ‘big picture’ trends of urbanisation, energy efficiency, and food security.

To put the value of the borates market into perspective, Francis said that it is about the same size as the US$3 billion lithium market.

Fort Cady carries less risk

The prospect of early production and easier financing at potentially less onerous rates is definitely an attraction, but it also pays to look behind the scenes to get a full appreciation of what Fort Cady has to offer in terms of potential development and predictability of outcomes.

Understanding Fort Cady’s past provides an insight to what may lie ahead for ABR.

The Fort Cady project is a past-producing asset, with US$60 million invested in extensive historical development.

The deposit was first discovered in 1964 and limited scale solution mining was undertaken in 1981, and some 450 tonnes of boric acid were produced from pilot scale operations in 1987-1988.

The project was fully approved for commercial scale operations in 1994.

Extensive feasibility studies, detailed engineering and test works occurred in the late-1990s and early-2000s.

This included a second pilot plant from 1996 to 2001 that used sulphuric acid as the leachate and produced some 2,300 tonnes of a synthetic colemanite product called ‘CadyCal’.

Francis explains that colemanite is a calcium-based borate that does not contain sodium, an important property because in applications such as E-glass, the most common form of glass fibre, and some types of borosilicate glass, such as those used in TFT-LCDs, low- or no-sodium borates are used.

Colemanite resources are rare and vital, and currently Turkish state-owned entity Eti Maden has a virtual monopoly in mining colemanite on a commercial scale.

Fort Cady hosts the only other major, commercially viable colemanite deposit in the west, potentially providing a valuable alternative source of supply.

Interest from China

With China being the largest market for borates and a net importer of the product, it wasn’t surprising to see ABR secure cooperation agreements with two leading players in Sinochem Hebei Corp, a subsidiary of China’s state-owned Sinochem Group, and with China National Fiber Corp, a subsidiary of China National Machinery Industry Corp (usually known as Sinomach).

On this note, Francis said, “That two of China’s largest and most established state-owned enterprises have entered into these agreements is a testament to the strategic value of the Fort Cady project.”

He also highlighted the potential for securing offtake financing with one of the Chinese partners.

However, given that there is also strong demand in the US and Europe, there is the potential for partnering with a major glass or glass fibre manufacturer.

Fort Cady hosting a strategically important mineral with extremely low capital expenditure costs, and it is the most advanced borates project in the market.

Given the current share price only implies 2% of the net present value of the project, Francis believes ABR offers compelling investment metrics.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.