BKT – The Quiet Achiever – Ready to Unearth Graphite at Pilot Plant

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Next Mining Boom presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

Sharpen your pencils, and get ready to note down this graphite potential.

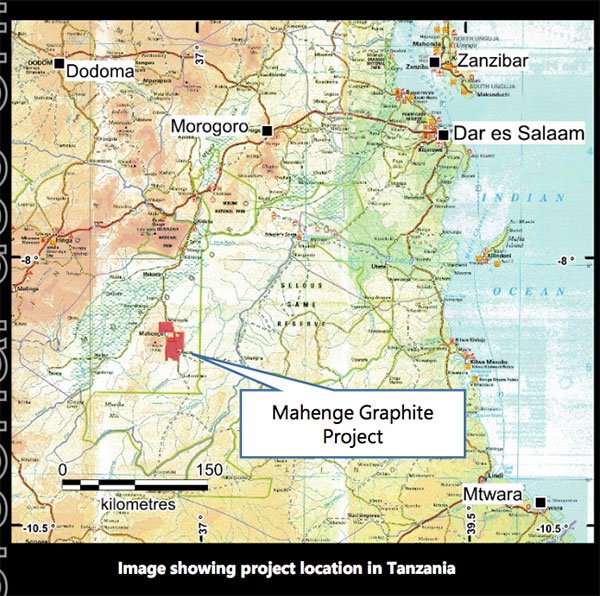

Black Rock Mining Limited (ASX:BKT) is ready to bring a pilot plant online at the largest high-grade flake graphite Resource in Tanzania.

The Mining Licence application process commenced on 5 February 2018 with the submission of the draft Environmental and Social Impact Assessment (ESIA) to the National Environment Management Council (NEMC) of Tanzania. The Company expects to lodge its final application in May 2018 post receipt of comments on the draft ESIA.

We have been following BKT’s steady rise for just over a year now, watching it just get on with the job and nail everything it needs to get its Mahenge Graphite Project into operation so that it can deliver on its promise.

BKT hopes to have its export approvals in place very shortly and its transport to port ready to run. It already has 140 tonnes in the lab in Canada ready to go.

BKT has also already produced sampling of excellent large flake distribution and a highly pure graphite product, pushing it swiftly to the top of the Tanzanian graphite table.

And with BKT about to bring its Pilot Plant 1 into operation imminently, and solid plans for infill drilling and bulk sampling for Pilot Plant 2 to be carried out shortly, validation of this extraordinary asset may be just around the corner.

Like everything BKT does, there is purpose behind the pilot strategy. It is about risk management – which is difficult to achieve in Africa. Pilot Plant 1 will provide a Life of Mine (LoM) feed profile and data for testing and provide market samples to customers, whilst Plant 2 is about proof of flow sheet, vendor performance and an exact profile of BKT’s con production over the first five years. A second pilot plant run to complete variability test work focused on an initial five years of production is scheduled for September 2018.

Best of all, BKT has signed an MOU with Japanese conglomerate Meiwa Corporation, a graphite product user, giving it an entry into the global lithium-ion battery market.

Of course, BKT remains a speculative stock and investors should seek professional financial advice if considering this stock for their portfolio.

The organisation has been building muscle, getting it to a size where it’s ready to tackle the high calibre and quantity of graphite it is expecting to uncover at its site — the development has a pre-production capex of only US$90 million.

BKT is using what it calls a Crawl, Walk, Run strategy to reinvest cash flow and build out its business by adding modules at the end of years two and four. We would call this common sense, and it looks like much of the rest of the industry does also as a number of other players seem to be copying BKT’s formula.

The catalysts may be coming fast, but this is not one to rush.

BKT is a small exploration company in the graphite game, but it is already making its mark through a sure and steady development of Mahenge — the fourth largest graphite Resource in the world — and the second largest reserve. As CEO John de Vries says, the Resource is easy to add to, but the Reserve gets a lot harder as you now need to have the economics to support your case.

Mid-last year the company announced its Tanzanian graphite project had a valuation of US$905 million – or A$1.2 billion – with 16.6 million tonnes (Mt) of graphite sitting in its soil. Setting it apart from its peers, BKT’s valuation is after tax and includes the recently announced 16% free carried interest to the Tanzanian government.

It then successfully raised A$4.74 million to complete a Definitive Feasibility Study, which it commenced in December.

The global graphite total JORC Resource stands at 211Mt, and Mahenge contains nearly 16Mt of graphite at an average grade of 7.8% Total Graphitic Carbon (TGC), along with a high grade proportion of 25Mt at 8.6% TGC.

The JORC Ore Reserve is at 69.6Mt at 8.5% TGC. With an initial 32-year life of mine (LOM) at less than half of the contained graphite, the production capabilities for the site are strong.

Mahenge is a high margin project and BKT has the peer leading percentage of large and jumbo flake sizes at its site.

This will attract premium pricing in a tight market.

With its first pilot plant ready to go, BKT should provide strong catalysts moving forward and with a small A$24.4 million market cap, we could see it blossom if it can prove its graphite assets.

BKT is ramping up the pace, so we’d better catch up...

![]()

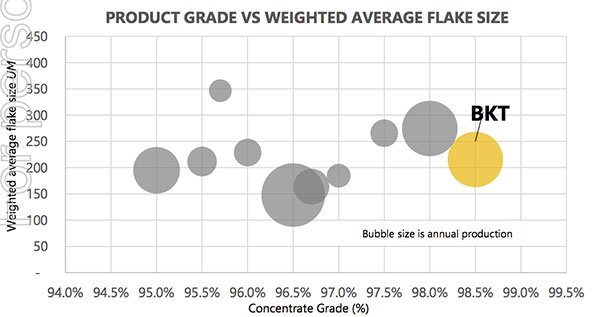

When it comes to graphite, the quality of the grade is absolutely crucial.

When we last wrote about Black Rock Mining Limited (ASX:BKT) back in November, with the article Graphite Resource Tonnage Leader BKT Looks to Capitalise on Emerging Market, the company had just revealed it had the highest grade-quantity mix of any other graphite explorer anywhere across the globe.

Since then it has continued to emerge as a key player in the Tanzanian graphite market, attracting attention for its strong, high-quality Resource grade.

It has also just announced it has begun its mining licence application which will allow it to commence construction in the second half of the year.

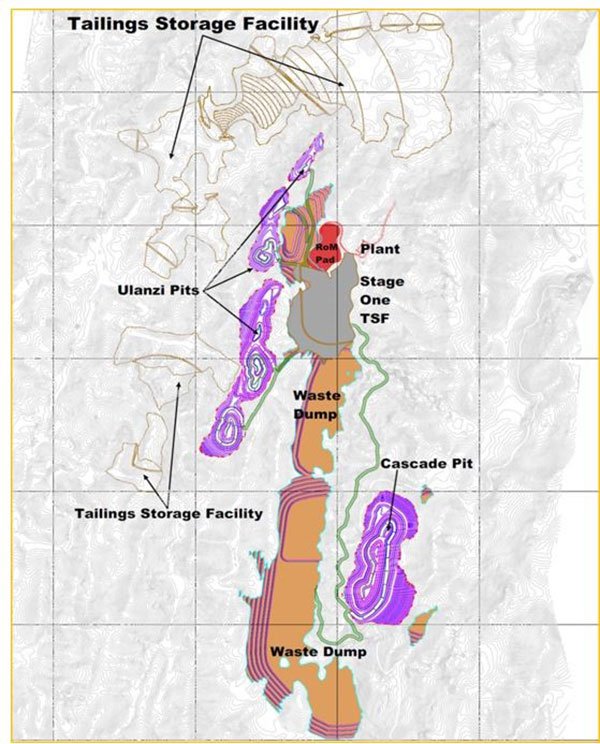

Here’s a look at the proposed mine layout:

The company has released further data showing the strength of its graphite size and grade – material it is poised to put through its pilot plant 1.

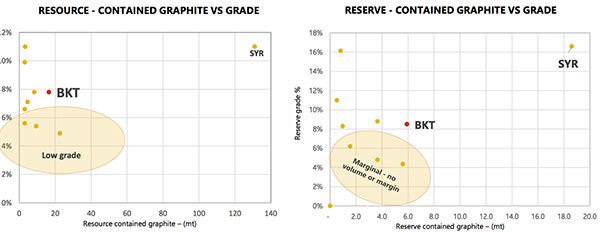

Here’s how the company’s graphite quality compares to others:

Note the high grade concentrate of graphite that was found in large portions of the Resource. Only Syrah Resources’ (ASX:SYR) Mozambique graphite facility is producing better results.

BKT is in a strong position, which is made clear in this short company video:

After watching that, it’s clear there’s only one way for BKT to head — and that is to dig down.

Potential, promise and plans to profit

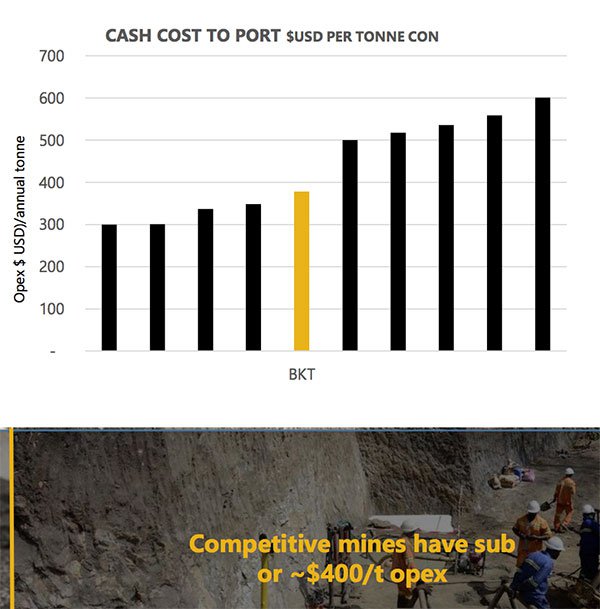

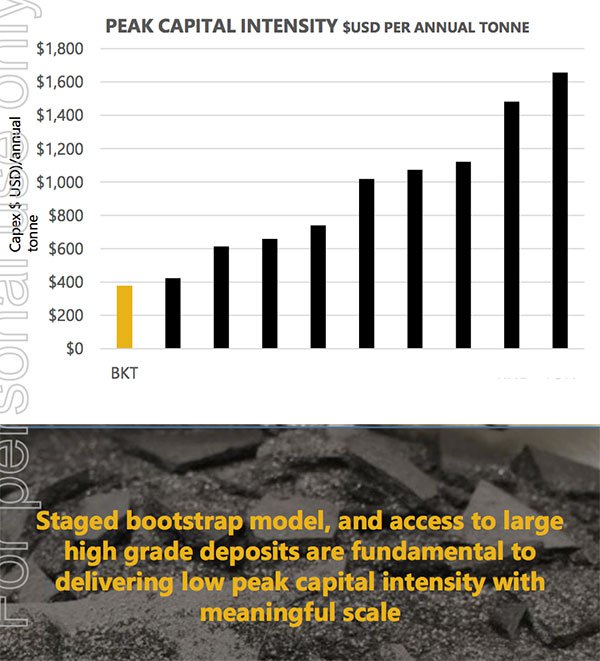

With a credible operating expense (OPEX) estimate, BKT is well positioned within its peer group. The bottom quartile LoM cash costs to port are US$382/t, a function of low LoM strip ratio of 0.8:1.0, and high grade.

Take a look below to see for yourself:

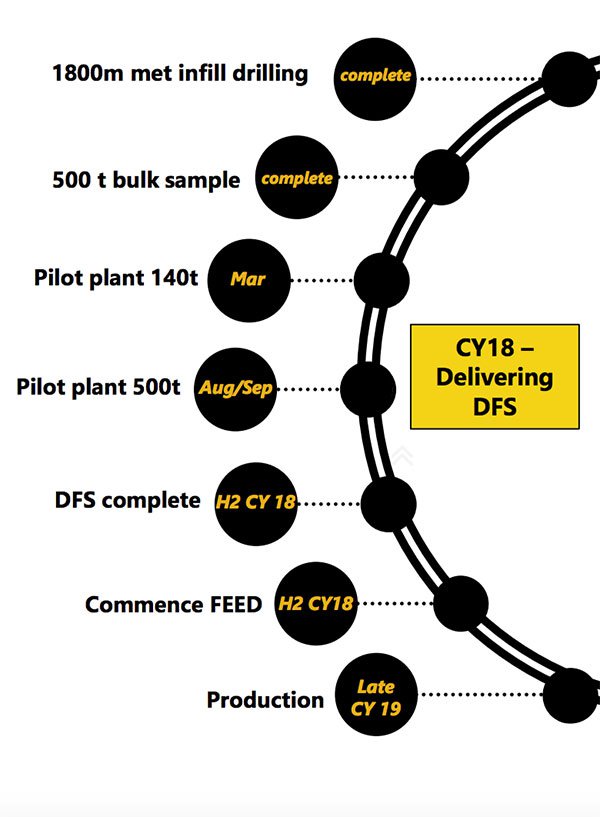

Let’s take a quick look at the production process BKT plans to undertake to get its Pilot Plant 1 off the ground:

Just US$90 million (A$115M) will be used to deliver the phase one production of 83.3ktpa, which is planned for 2019.

Just US$90 million (A$115M) will be used to deliver the phase one production of 83.3ktpa, which is planned for 2019.

Phase two is self-funded from cash flow to add another 83.3ktpa in 2021, for a combined 167ktpa. And once the third facility comes online, production will hit 250ktpa.

Using the company’s cautious low-risk strategy, BKT is creating a project that strikes a balance between the scale to attract investment against its ability to fund the project. That is why they have done the hard engineering that will underpin its coming DFS.

That hard work includes CPC Design’s commencement of engineering design of the plant and infrastructure for Module 1 at Ulanzi, Mahenge. The study remains on budget and schedule for delivery in H2 2018.

Furthermore, process design criteria, including flow sheets and mass balances will be finalised once the first pilot plant run scheduled for March 2018 is completed.

Pre-feasibility study shows strong promise

If the potential of Mahenge isn’t yet clear enough, the statistics shine a light. A pre-feasibility study carried out in August last year showed an estimate of 212 million tonnes of graphite at BKT’s Ulanzi location.

Kicking off with a modest investment, BKT will ramp up production at the site to 240,000 tonnes a year, leading to a net present value (NPV) of US$905 million (A$116), or when calculated using a 10% discount rate (NPV10) at US$624 million (A$799) post tax.

Post tax unlevered Internal Rate of Return (IRR) therefore stands at a favourable 48.7%. This is based on realistic basket pricing of US$1241 a tonne, and the NPV10 jumps up to US$1.1 billion when using a basket price of highest peer.

In fact, compared to its peers, BKT does very well, especially considering its low pre-production capex profile.

So what do these numbers mean for BKT? Put simply, this pre-feasibility study has shown Mahenge has the potential to be developed into a site using low capital and operating costs, but giving strong financial results.

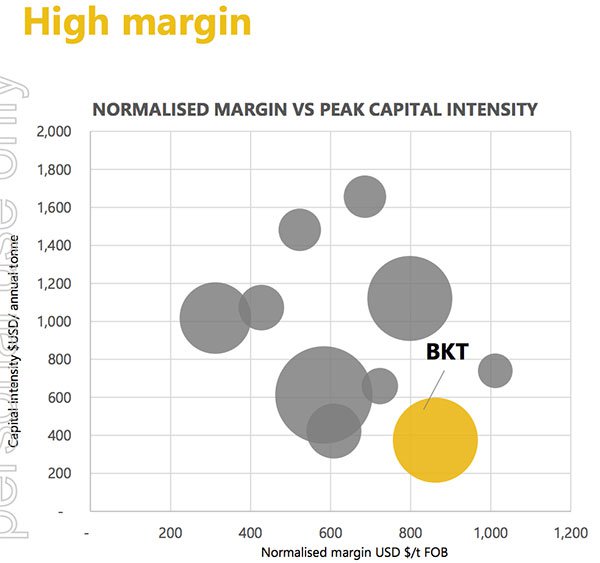

Have a look at the graph below for a visual representation of BKT’s high margin potential:

With the largest graphite Resource in Tanzania, straight forward processing and simple mining, BKT is on track to create the lowest cost operation in the country.

However BKT does have a lot of work still to undertake, so investors should take a cautious approach to any decision made with regard to this stock.

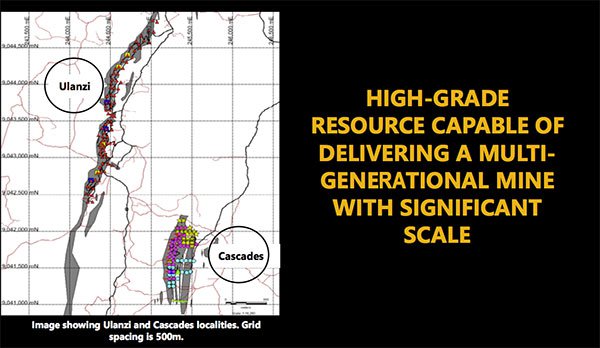

Neighbouring site shows Resource is strong

Investors only have to look next door to BKT’s other site, Cascades, to see the graphite glistening.

Cascades is one kilometre south-east of Ulanzi and is an estimated 60 million tonne Resource with 8.3% Total Graphitic Carbon (TGC) and 15 million tonnes at 12.2% high grade TGC. Drilling was carried out in 2016, unearthing these solid results.

When Ulanzi’s drilling program was completed in 2016, it also showed continuity of mineralisation across a 2.5 kilometre drill portion of a 5 kilometre structure.

Just take a look at the high quality Resource and scale of production below:

A solid plan for low cost growth

BKT is taking what it has dubbed a ‘crawl, walk, run’ method to get its first Mahenge plant up and running. The company explains that this is a low-risk approach which involves minimal capital investment to bring the site into operation.

Once demand increases, production will ramp up and cash flow will be used to build a further two plants.

Take a look at how BKT’s capital investment compares to its investors:

BKT has big plans to be the lowest cost operating plant in Tanzania by starting off small and growing only when the first phase has seen success. The company will have the lowest peak capital intensity of its peer group but the highest normalised margin of any mine with meaningful scale.

The simple pilot plant structure will be modular in design and feature a drying circuit, crushing circuit, ore mill, flotation circuit and screening circuit.

Strong transport links to shift graphite

As part of getting into the low-cost game, BKT has established strong transport links to make moving its graphite easy.

Once the graphite has been processed within the plant, it will be loaded up on to trucks and shipped 60 kilometres north to the town of Ifakara.

Ifakara is on the railway to the city of Dar Es Salaam which features a major port, giving BKT access to the worldwide market.

Take a look at BKT’s advantageous location below:

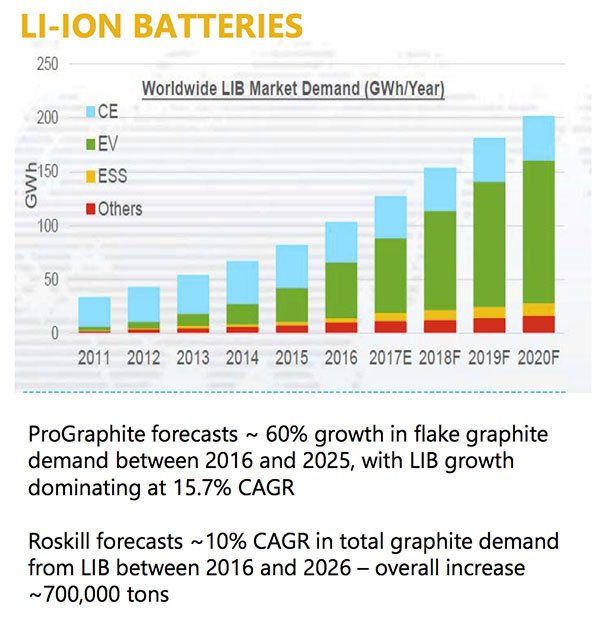

And the worldwide market is ready for these graphite deliveries more than ever, with a global graphite shortage and a strong lithium battery supply need.

Lithium battery supplies are decreasing but demand is rising

Just take a look at the increasing demand for graphite thanks to the expansion of the lithium battery market:

It should be noted though that commodity demand does fluctuate and caution should be applied to any investment decision here and not be based on spot prices alone. Seek professional financial advice before choosing to invest.

We know the demand is there for BKT’s Resource. But what about the quality of the graphite? Is it good enough to be turned into a lithium battery?

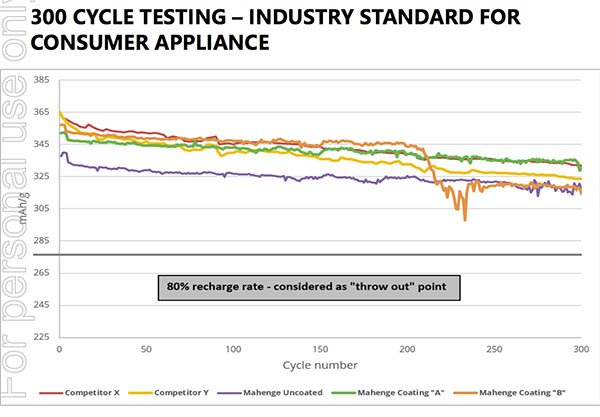

Let’s just say that testing has not disappointed BKT. Studies have shown its graphite quality surpasses competitors with battery cell testing showing near-perfect battery performance.

Long-term 300 cycle cell testing showed results that were superior to current commercial cell graphite.

Let’s see how Mahenge’s batteries compares to its competitors:

This clearly shows Mahenge’s graphite could strongly outperform commercially available products currently on the market.

With this high-grade battery potential, BKT has what it needs to cement itself in the battery market, even leading the way in establishing new battery performance benchmarks.

Overall graphite game strong

High grade Resource? Check.

Pilot plant one ready to go? Check.

Transport in place and a purchaser lined up? Check.

Export approval in place imminently? Check.

So what’s next for BKT?

With the company’s strong position as a small exploration company with a lot of upside, we look forward to the news flow to come.

As BKT’s pilot plant one comes online in a matter of days, get ready for the results coming out of this promising Tanzanian graphite mine.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.