Berkeley offtake agreement provides revenue visibility

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Emerging uranium producer Berkeley Energia (ASX | LSE: BKY) informed the market on Monday morning that it had signed a binding offtake agreement with Interalloys Trading Limited (Interalloys) for the sale of first production from the group’s Salamanca mine situated in Spain.

This represents an extension of an earlier agreement with Interalloys which was a Letter of Intent for the sale of up to 1 million pounds of uranium concentrate over a five-year period starting from the commencement of the mine and extendable thereafter by mutual consent.

The binding offtake agreement not only provides more certainty, but the terms are better with the average price of US$41.00 per pound contemplated in the Letter of Intent now formalised at US$43.78 per pound.

Furthermore, the binding offtake agreement is for 2 million pounds over a five-year period with the potential to increase annual volumes further, as well as extend the contract to a total of 3 million pounds.

Is this a buying opportunity

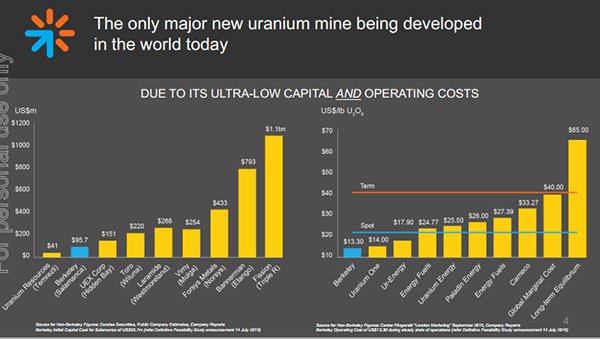

Shares in BKY have surged in the last six months, increasing 50% from circa 60 cents in June to a five-year high of 90 cents in October, mainly driven by promising exploration results and the completion of a Definitive Feasibility Study (DFS) which confirmed Salamanca would be one of the world’s lowest cost producers when it comes on stream in 2019.

The fact that the company’s shares have retraced slightly, closing on Friday at 73.5 cents could represent a useful entry point for investors who missed buying into the story on the way up.

Those considering this stock shouldn’t make assumptions regarding exploration outcomes, nor should they base investment decisions on share performances to date. It could be argued that the company’s share price doesn’t account for the value of its asset or its potential upside and investors should seek professional financial advice if considering this stock for their portfolio.

Offtake agreements provide material certainty in terms of future revenues, which in turn presents other benefits such as easier access to capital.

Consequently, this is a very favourable development and one which should provide positive share price momentum. However, share price trends are impossible to predict and potential investors considering this stock should seek independent financial advice.

Berkeley in discussions with other potential offtake partners

Chris Brown from Morgans CIMB has a high opinion of BKY, commenting after the recent capital raising, “Salamanca has a long life, a stable European jurisdiction with Nuclear Fuel Cycle experience, a relatively low capital intensity in terms of pounds of U30 in resource and annual pounds of production”.

With the project fully permitted and with a low projected cash cost of US$15.39 per pound U308, he sees the project as being attractive to power utilities. His add recommendation is supported by a 12 month price target of $1.31, upgraded from $1.12 in November following the capital raising.

Brown flagged ‘sales and marketing initiatives’ as one of the potential catalysts for an increase in valuation. Given the size and pricing of this agreement it should have brokers sharpening their pencils.

The pricing implies strong margins and BKY’s Chief Executive Paul Atherley underlined this aspect of today’s development in saying, “We are delighted to have converted the previously announced Letter of Intent into a binding offtake agreement with Interalloys, including the doubling of contract volumes and with fixed pricing at US$43.78 per pound which would give us a very strong margin above our steady-state cash cost of around US$15.00 per pound”.

Salamanca positioned to sell into Europe, China and the US

Another comment made by Atherley that won’t be lost on investors is the fact that the group is currently in discussions with other potential offtakers in relation to contracts with similar terms to those outlined in the Interalloys agreement with pricing at or around long-term benchmark levels for term contracts.

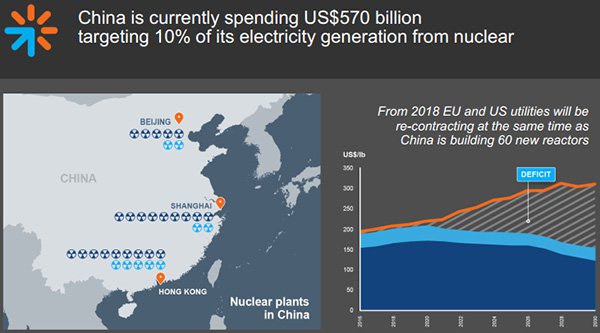

Atherley conceded that uranium prices are likely to remain flat in the near term, but post 2018 when Salamanca comes into production an uptick in pricing is expected, as US utilities looking to re-contract will be bidding against Chinese buyers looking to secure supply of product for their new reactors.

At the same time, the Salamanca project is ideally situated from a geographical perspective to sell into Europe where there is substantial demand for a low-cost producer.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.