Should we avoid quarterly capitalism?

Published 08-APR-2016 11:01 A.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

You can see by the headlines below, that when discussing quarterly capitalism, there is no real upside. Mike Cornips, Director at Options Educator, TradersCircle explains.

“First-Quarter Earnings Are Now Expected to Really Suck” – SeekingAlpha.com

“Wall Street analysts expect first-quarter earnings to slide 8.5%, according to FactSet. That would mark the fourth straight quarter of contraction, and the largest year-over-year decline since the third quarter of 2009 when earnings tanked 16%.” –Wall Street Journal

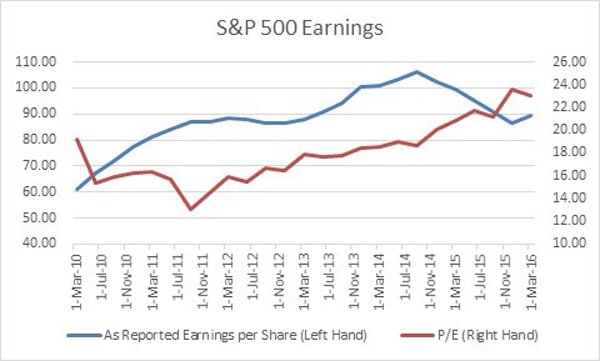

The Price/Earnings ratio for the S&P 500, based on a “as reported earnings per share”, is about 23 times earnings. (source: S&P ). The earnings for the year ending 31st March 2016 is estimated to be 89.28, and based on an Index level of 2059.

Factset.com has the 12-month forward Price/Earnings ratio at 16.6 times, based on earnings estimates of $124.43.

These are inflated earnings figures based on non-GAAP earnings that analysts use to make things look better than they really are. Nevertheless, Factset still expect that 2016 first quarter earnings for all ten sectors will fall compared to 31st December 2015 estimates.

These decreased earnings per share estimates also need to be seen in the context that Corporate America is expected to undertake as many share buybacks as financial engineering can possibly allow.

Stocks in the S&P 500 have undertaken about $600 Billion in share buybacks over the past 12 months, which theoretically should increase earnings per share. In addition, stocks pay dividends of nearly $400 Billion. The total payout of S&P 500 stocks is about $1000 Billion or about 5% of market capitalisation.

This financial behaviour can be termed ‘Quarterly Capitalism’, short-term, myopic, greedy and dysfunctional.

Hillary Clinton recently used the term, saying: “I am deeply distressed about quarterly capitalism because I think it is causing businesses to make decisions that are not helping the long-term profitability of American corporations or the success of our economy.”

Having identified the problem, we should expect nothing to change until the next financial crisis.

For a refreshing view on why we should start making long-term decisions, we can look to Australia’s own Future Fund.

Every day short-term decisions taken on behalf of long-term investors risk destroying value.

This is a structural flaw in the investment system that long-term investment institutions – superannuation funds, insurance companies, family offices and sovereign wealth funds like the Future Fund – are increasingly focused on fixing.”

Read more: www.afr.com

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.