Are small caps really outperforming the market?

Published 16-DEC-2015 08:52 A.M.

|

4 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The figures may indicate that small cap stocks have taken off, but it could simply be because the weakest members of the herd have been wiped out.

Smaller company-based indices have broadly outperformed the market this year, virtually reversing the last ten years of trend.

For the calendar year to date, the Emerging Companies index (ASX:XEC) has grown by 6.25% while the Small Ordinaries (ASX:XSO) Index has grown by 0.56%.

Compared with the likes of the ASX 200 (ASX:XJO) which was down by 8.57%, the All Ordinaries (ASX:XAO) which was down by 7.16% and the ASX 50 (ASX:XFL) which was down by 10.32%, the small cap space has been a safe haven of growth.

This has been especially pronounced since August, when the divergence between the big boys and the small gathered pace.

A chart showing the divergence of small and large cap indices since August

However, taking a longer-term view of the issue the XAO, XFL, and XJO have added 3.56%, 5.75%, and 4.25% respectively over the past five years.

This is against the broader trend of the XEC shedding 43.3% and the XSO bringing down 26.19%.

So what the hell is going on? Why has this year been the year small caps have started to perform?

“I think what’s happening is that small caps went through a period of retraction by the resources downturn already and that’s really started to catch up in the broader market this year,” David Paradice of Paradice Investment Management told Finfeed.com.

So it’s not really that small caps have gone really well, it’s that the likes of your BHPs have been hurt this year by continued softness in commodities and small caps already went through that.”

The commodity pain has been an ongoing feature for the year, with BHP shedding almost half its value this year (at the time of writing) while RIO has gone down by over 27%.

Both of these stocks are (or were) heavily weighted in the likes of the All Ordinaries and other broader market indices, simply because they had huge market caps.

So when they, along with other resources-exposed stocks, went down, the whole index was dragged down with it.

But the reason the small cap indices weren’t affected as much by the resources winds blowing through the market this year, Paradice says, is simply because the pain caused a lot of the companies to go bust altogether.

“Effectively what is happening at the moment is the Darwinian theory or survival of fittest. For ten years resources companies were basically having a party and we’re now seeing the hangover from that,” Paradice said.

“The commodity price support really masked a lot of bad companies and they’ve gone by the wayside.”

At the peak of the resources boom, Paradice estimated that resources companies made up about 45% of all small cap companies, and that doesn’t account for the plethora of mining services companies in the mix as well.

This was a huge exposure, so when commodity prices headed south a lot of companies simply went bust and were taken off the index list – effectively making the index look a better performing index than it may have been if these companies scrimped and saved to stay alive.

Senior Fund Manager with Pengana Capital, Ed Prendergast, told Finfeed.com that the company’s emerging company fund deliberately avoided resource-related stocks.

“We excluded resources from day one as we don’t see we have an advantage in forecasting commodity prices,” he said.

However, this hasn’t made the fund shy away from investing in cyclical plays.

“We do invest in cyclicals, as long as the potential return far outweighs the risk.”

One such cyclical play is the rise of the tourism industry, one of three picks for the year ahead from Pengana along with the aged care and telecommunications sectors.

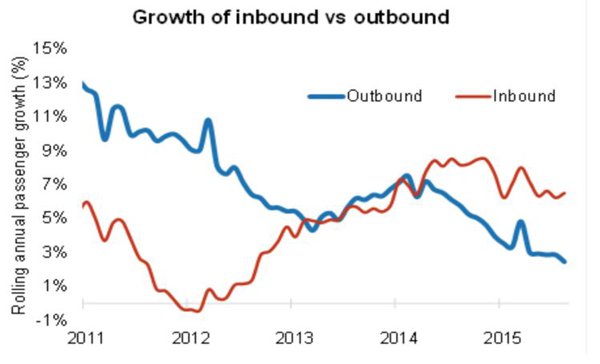

A relatively weak Australian dollar has driven a lot more domestic tourism, and a lot more inbound tourism.

Chart from the Australian Bureau of Statistics showing the changing of the guard in tourism.

He pointed to Australian Bureau of Statistics stats which clearly captured the trend, almost as a proxy to the Australian dollar.

With the resources pain set to continue in 2015, the likelihood is that the Australian dollar will remain weaker against other currencies which are not pegged to commodities to the extent that the Australian dollar was during the mining investment boom.

However, the macro picture is only part of the equation for both Prendergast and Paradice, with both saying the management of a potential investment had a huge role to play in choosing whether or not to invest.

“That’s where 90 per cent of our focus is,” Prendergast said. “Successful small caps are predominantly driven by key individuals, much more so than large caps.”

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.