Ardent’s challenges stretch beyond theme park business

Published 10-JAN-2017 16:10 P.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

There has been a mixed response on a number of fronts to the trading update provided by Ardent Leisure Group (ASX:AAD) last Friday. Firstly, the immediate reaction was difficult to fathom as the company’s shares traded between $2.09 and $2.27 before closing at $2.23, slightly down on the previous day’s close of $2.24.

However, on Monday the company’s share price finished up 3.6% under relatively strong volumes. But the jury is still out in terms of whether Ardent represents compelling value at this level with some analysts indicating a return to business as usual at its theme parks could result in a positive rerating.

Analysts at Credit Suisse see Ardent’s current trading range as a buying opportunity and it has an outperform recommendation on the stock.

In defiance of this there is a sense of uncertainty filtering through from analysts at Macquarie and Morgans CIMB. Importantly, they are looking beyond the theme park business, in particular the Main Event area of its operations where like-for-like sales in the first half of fiscal 2017 were down 2.9%.

It should be noted here that broker projections and price targets are only estimates and may not be met. Also, historical data in terms of earnings performance and/or share trading patterns should not be used as the basis for an investment as they may or may not be replicated. Those considering this stock should seek independent financial advice.

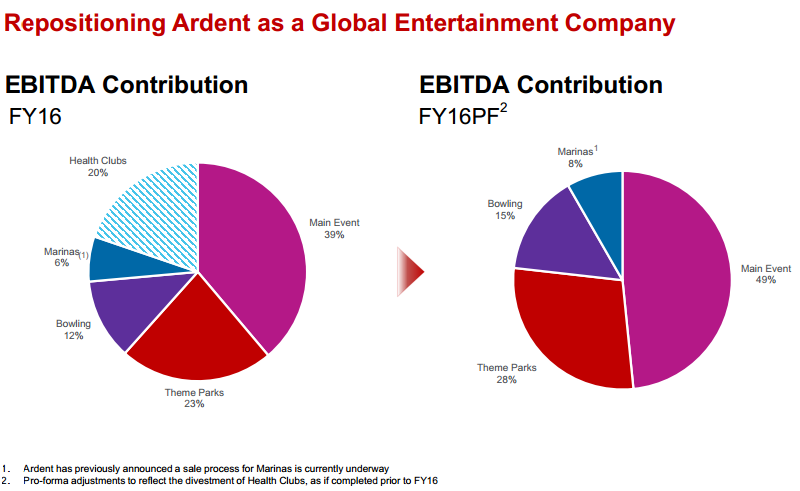

Main event crucial in transitioning to a global entertainment company

As can be seen below, this area of the company’s operations accounted for nearly half of pro forma EBITDA in fiscal 2016, and it is also central to the group’s repositioning as a global entertainment company.

Macquarie said this could be attributed to softness during the election period, but with low single digit like-for-like sales growth flagged in the second half of 2017 it saw the update as ‘disappointing’.

The broker has subsequently maintained its neutral recommendation while reducing its DCF based price target from $2.21 to $2.19.

This is broadly in line with Morgans CIMB. The broker maintained its hold recommendation following the trading update while lowering its price target from $2.26 to $2.16.

Morgans also pointed to weak same centre growth in the Main Event business and lowered its earnings per share forecasts between fiscal years 2017 and 2019 inclusive by 8.1%, 3.5% and 4% respectively.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.