Apiam shaping up as a growth by acquisition story in a niche market

Published 04-OCT-2016 11:55 A.M.

|

4 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Shares in Apiam Animal Health (ASX: AHX) fired up in mid-August after the company announced that it had signed an agreement to acquire Quirindi Veterinary Group (QVG), one of Australia’s largest rural veterinary groups with revenues of circa $12 million.

AHX’s share price increased from approximately $1.50 to hit an all-time high of $1.88 in response to the news, representing an increase of 25%. There was further good news to come with the group announcing a fiscal 2016 pre-tax profit of $1.1 million, 94.5% ahead of prospectus forecasts.

However while there is a strong economic outlook, market conditions can fluctuate, so as with any investment it is important to seek professional financial advice if considering AHX for your portfolio.

If Bell Potter analyst, Jonathan Snape, is on the mark the group will experience a significant increase in profit in fiscal 2017. He is expecting revenues to nearly double to $104.8 million in the coming 12 months, and is forecasting a net profit of $6.9 million representing earnings per share of 6.8 cents.

The recent retracement in AHX’s share price could present a buying opportunity, and the company is trading at a slight discount to Snape’s 12 month price target of $1.79. However, there was one caveat in his assessment of the stock, as he highlighted the level of business investment had been greater than he had expected.

However, looking at the bigger picture and the group’s long-term growth drivers he said, “With less than 1% share in the veterinary market and less than 8% share in the vetchem market AHX has the scope to act as a consolidator in a fragmented market sector”.

Snape estimates AHX has the scope to deploy approximately $10 million for acquisitions from internally sourced funding (assuming 30% scrip funding) which at target EBITDA multiples of between four and six suggests the scope for earnings per share accretion at full utilisation of between 10% and 20% on a pro-forma post synergy fiscal 2017 forecasts basis.

It is important to note that comparisons should not be drawn with Greencross (ASX: GXL) as the businesses are very different in terms of the markets they address. Also, GXL is a relatively mature business with a market capitalisation of $750 million, while AHX has been trading for less than 12 months as an ASX listed group and has a market capitalisation of $170 million.

However, the latter has the opportunity to grow quickly off a small base in the early stages (similar to Greencross), and if management executes well on its strategy this could provide share price momentum.

For example, when GXL started to accelerate its growth by acquisition strategy between 2012 and 2014 the company’s shares increased from approximately $1.40 to hit an all-time high of $10.78. However, it was arguably poor execution on the back of its largest acquisition that brought the company unstuck in recent years, and AHX will need to be careful that it doesn’t fall into the same trap.

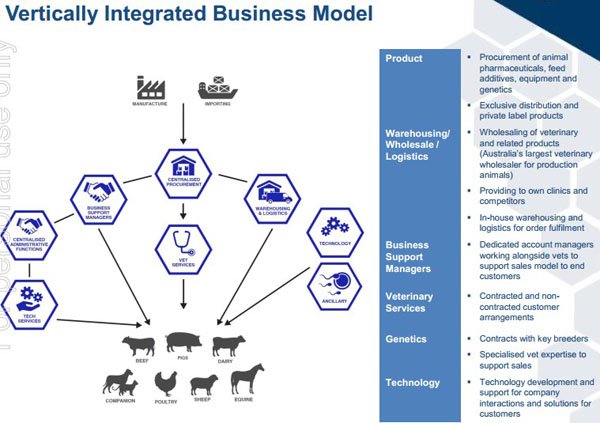

In terms of the group’s addressable markets, it is a vertically integrated animal health business providing a range of products and services to production and mixed animals. Its focus is more on the provision of care and services to livestock rather than pets, which is predominantly GXL’s corner of the market.

AHX’s position in the livestock market was strengthened with the acquisition of QVG, as it provides veterinary services to large beef production systems throughout Australia through its feedlot services business, as well as offering equine reproduction services at its custom-built centre near Scone in New South Wales.

QVG also runs a livestock and companion animal veterinary practice located in Quirindi. As part of the acquisition, AHX will acquire proprietary technology to improve clinic efficiencies, data analysis systems for feedlot cattle and specialised assets for reproduction services.

In reference to the QVG acquisition, AHX’s Managing Director, Dr Chris Richards said, “QVG is an excellent business that counts some of Australia’s most innovative beef producers as its customers and is a strong strategic fit with our core business with all three aspects delivering strong synergies and improving our capacity in the be feedlot sector while expanding our genetics business and presence in rural New South Wales”.

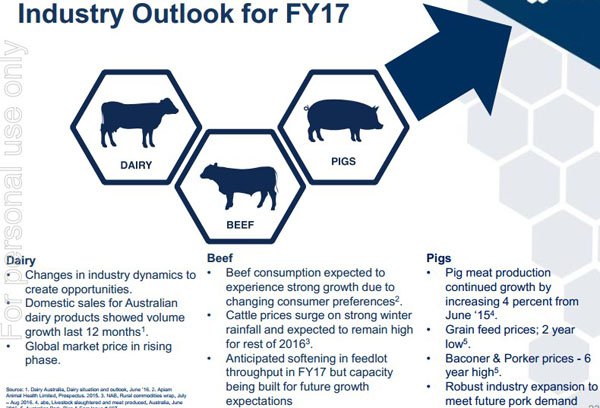

As indicated below, industry conditions should generally work in AHX’s favour in fiscal 2017. This suggests that the successful integration of the QVG business along with carefully targeted acquisitions could see the company prosper over the next 12 months.

It should be noted that broker projections and past share price performances are not an indication of future earnings and trading patterns, and should not be used as the basis for an investment decision.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.