PFE’s neighbour commissions USA’s biggest DLE plant

Last week $304M Standard Lithium put out news that it had “successfully commissioned and validated” the largest continuously operating direct lithium Extraction (DLE) facility in North America.

The move is a big step for the US lithium industry and for the specific region where Standard operates in.

(Source)

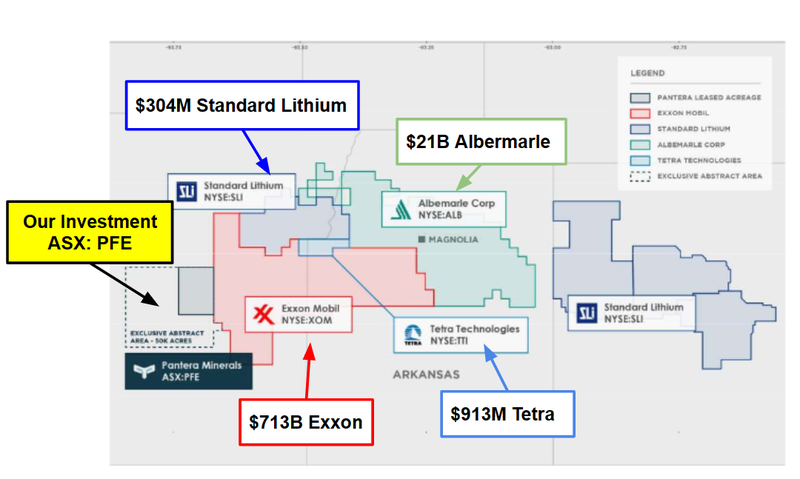

Standard’s project is in the Smackover formation in Arkansas, USA - neighbouring ground held by one of our portfolio companies - Pantera Minerals (ASX: PFE).

Some context on the area - it is the same part of the USA where Exxon paid >US$100M for Galvanic Lithium and where it plans to make it the centre of its lithium business in the US.

Exxon’s plan is to be producing enough lithium to power over 1m electric vehicles by 2030.

So it isn't just Standard lithium with projects next to Pantera… here is a map of PFE’s neighbours in the region:

Why does the Standard Lithium news matter for PFE?

At a very high level we think it increases the look through valuation for PFE’s assets.

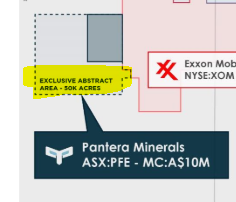

PFE holds ground in the Smackover inside a 50,000 acres AMI - the AMI is basically the area PFE has rights to negotiate leases in.

Across that 50,000 acre ground position PFE has already estimated a JORC lithium exploration target between 436,000 to 2,966,000 tonnes of Lithium Carbonate Equivalent (LCE).

Over the past few months PFE has been increasing its ground position (adding ~8,131 acres in the first 4 months of 2024).

Right now, of that 50,000 acre AMI, PFE holds ~18,570 acres.

PFE’s goal over the next 12 months is to re-enter existing wells on its ground, sample for lithium (Q2-2024) and put out a maiden JORC resource estimate for the ground it has managed to lease so far.

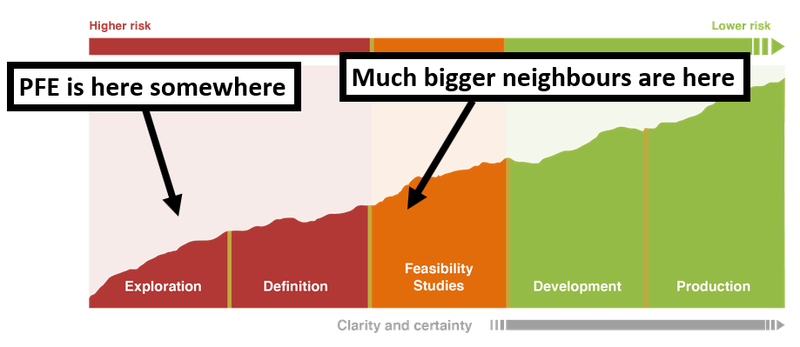

We think the JORC resource estimate will be a big catalyst for PFE as it will give the market a metric that can be compared to PFE’s neighbours.

PFE is the only ASX listed explorer with ground in the Smackover and if it can put together a resource estimate somewhere in the middle of its exploration target (436kt to 2.96mt LCE) then its market cap could re-rate higher.

PFE’s current market cap (~$10M) is relatively low considering the potential resource it has on its ground.

For context - Standard lithium has a Measured and Indicated resource of 2.8 Mt LCE and a market cap of $304M & Galvanic Lithium which Exxon paid over US$100M for had an inferred JORC resource of ~4mt LCE.

PFE is a lot earlier stage than its neighbours but as they work up their projects, we expect to see increased market/corporate interest in projects in the Smackover and in turn think the look through valuation for PFE’s project increase.

What’s next for PFE?

Continue leasing more ground 🔄

PFE has a 50,000-acre Exclusive Abstract Agreement (EAA) - we want to see PFE increase its ground position from its current ~18,570 acres to somewhere near the 50,000 number.

Acquisition of 2D Seismic & geophysical data 🔄

PFE plans to acquire existing 2D seismic data over its acreage.

The new data will ultimately be used to guide PFE’s drill programs in the future.

Re-enter a well 🔲

The first step toward converting its exploration target into a maiden JORC resource will be to re-enter historic oil & gas wells that sit on its acreage.

The goal for the re-entry programs will be to see how much lithium sits in the ground and at what concentrations.

DLE test 🔲

The re-entry will bring up samples which PFE can then send off to DLE (Direct Lithium Extraction) tech partners.